Desking & Deal Structure - Maximizing Front and Backend Gross Profit - 2026 Guide

The average dealership generates around $1,500 in front-end gross and $1,800 in backend gross per vehicle. But here's what separates the best-performing stores from the rest: optimized desking can improve both numbers by 30% or more, according to NADA dealership performance data. That's an additional $900+ per deal, which translates to hundreds of thousands in annual profit for a typical volume dealership.

The average dealership generates around $1,500 in front-end gross and $1,800 in backend gross per vehicle. But here's what separates the best-performing stores from the rest: optimized desking can improve both numbers by 30% or more, according to NADA dealership performance data. That's an additional $900+ per deal, which translates to hundreds of thousands in annual profit for a typical volume dealership.

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Deal structuring isn't about gimmicks or manipulation. It's about understanding the variables you control, knowing how to position them effectively, and creating space for both front-end profit and F&I product penetration. When you desk a deal correctly, everyone wins: you protect gross profit, the customer gets a payment they're comfortable with, and your F&I manager has room to present valuable protection products.

The Desk Manager Role

The desk manager holds one of the most critical positions in the dealership. You're the profit gatekeeper, the negotiation strategist, and the bridge between sales and F&I. Your job isn't just to approve deals. It's to structure them in a way that maximizes total gross while maintaining customer satisfaction. When to involve the desk: Don't wait until the customer says they're ready to buy. Get involved early. Review the needs assessment, look at the trade appraisal, understand the payment range. The best desk managers are already thinking about deal structure before the customer even asks for numbers.

The relationship between desk manager and sales consultant needs to be choreographed. The consultant is the customer's advocate and relationship builder. You're the authority figure who "has to check the numbers" and "see what we can do." This isn't dishonest. It's role differentiation that allows for natural negotiation progression.

Customer perception matters here. When the sales consultant comes to you, it should feel like they're going to bat for the customer. "Let me see if my manager can get you to that payment." This positions you as the decision-maker while keeping the consultant in a relationship-building role.

Pre-Desk Preparation

Before you write the first pencil, you need complete information. Incomplete information leads to wasted time, customer frustration, and deals that fall apart in F&I. According to Cox Automotive research, dealers using connected workflows and AI-powered desking tools are seeing up to 15% higher back-end profit. Start with a thorough needs assessment review. What vehicle did they test drive? What features are non-negotiable? What's motivating this purchase? The answers inform how much negotiation room you have. A customer who's been looking for six months and finally found the perfect vehicle has different flexibility than someone who's casually shopping.

Credit application analysis comes next. Don't wait to send it to lenders. Pull the credit yourself if you have that capability. Look at the score, the payment history, the debt-to-income ratio. This tells you which lenders to target and what buy rate to expect. A 740 beacon score gets you prime rates and maximum reserve. A 620 score means you're working with sub-prime lenders and different reserve structures.

Trade appraisal verification is critical. Walk the trade yourself or review the appraiser's worksheet. Understand the actual cash value and how it compares to payoff. Positive equity gives you negotiation leverage. Negative equity constrains your options and needs to be addressed in the structure.

Payment range confirmation isn't about asking "what payment do you want?" It's about discovering their actual budget through conversation. "Most customers financing this vehicle are in the $500-650 range depending on down payment and term. Where does that fit your budget?" This gets them to reveal their ceiling without anchoring too low.

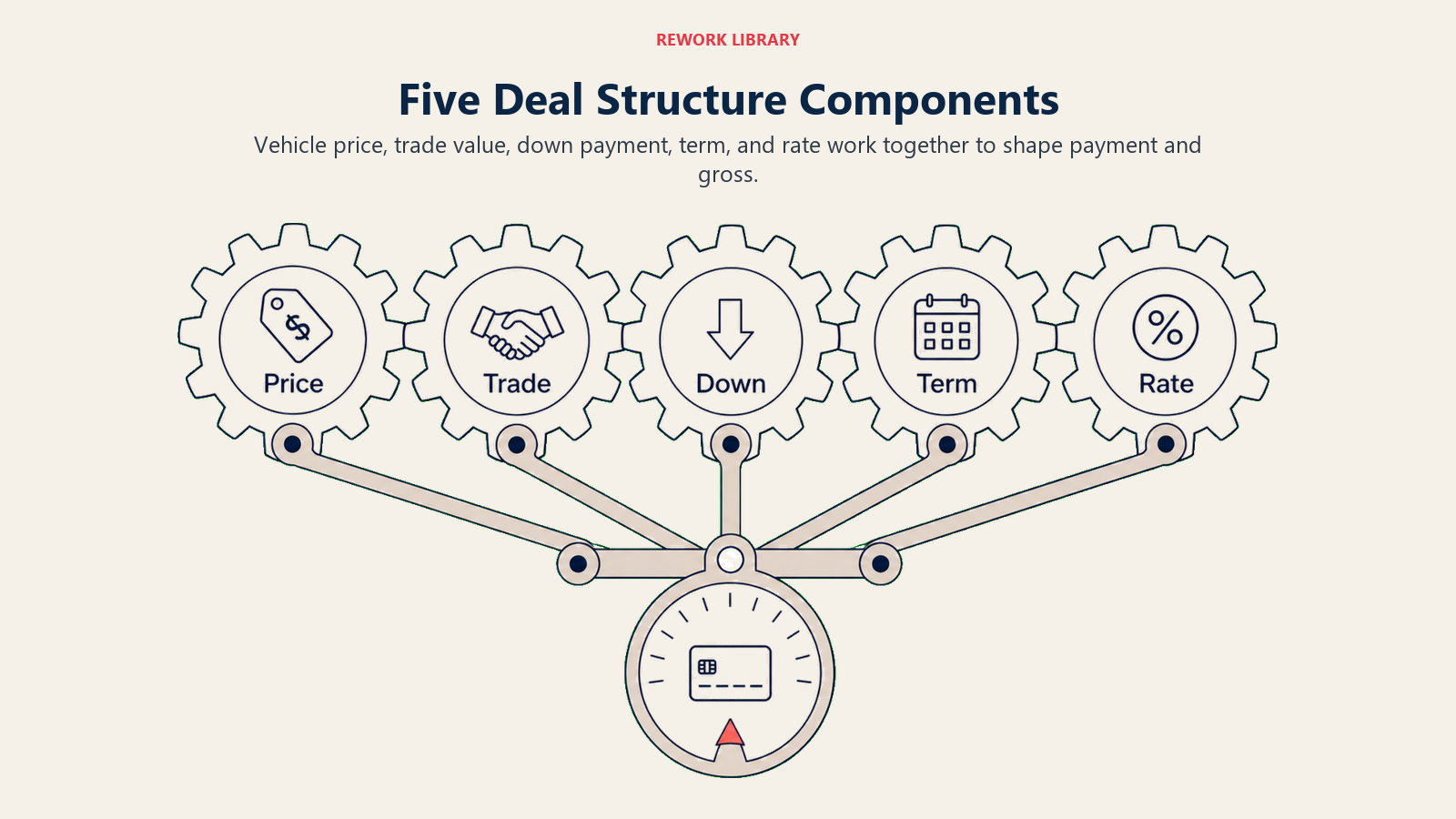

Deal Structure Components

Every deal has five primary variables you can adjust: vehicle price, trade allowance, down payment, finance term, and interest rate. Understanding how these components interact is essential to successful desking. Vehicle price starts with three reference points: MSRP, invoice, and your actual cost (including holdback and any dealer cash). On new vehicles, your starting point depends on market conditions. Hot-selling vehicles with limited inventory? You're starting closer to MSRP. Aged inventory or soft-selling models? You've got more room to move off sticker.

Used vehicles are priced to market, but that doesn't mean there's no profit. You should know your all-in cost (acquisition cost plus recon) and your desired gross. A CPO vehicle priced competitively at $32,995 might have $4,200 of gross in it. Don't give that away in the first pencil.

Trade allowance is where many deals are won or lost. You have the ACV, what the vehicle is actually worth. And you have the allowance, what you're offering. The spread between these two numbers is part of your front-end gross. But trade value is often more negotiable in the customer's mind than vehicle price, so this is where you create room to move.

Down payment or cap reduction directly impacts monthly payment and customer equity position. More down payment means lower payment, less negative equity risk, and often better interest rates from lenders. But not every customer has cash available. Understanding their down payment capability early avoids wasting time on structures they can't execute.

Finance term is your most powerful payment management tool. A $35,000 loan at 7% APR for 60 months is $693/month. Extend that to 72 months and it drops to $595. That's $98/month difference. Terms have extended over the years: 72 and 84-month loans are common now, especially on higher-priced vehicles. Just be aware of the negative equity implications of long terms combined with slow depreciation.

Interest rate affects both payment and dealer reserve. The buy rate from the lender is what they're willing to charge. The sell rate is what you charge the customer. The difference is your reserve (within regulatory limits, typically 2-3% markup maximum). A customer with a 5.5% buy rate can be sold at 7.5%, generating significant backend gross.

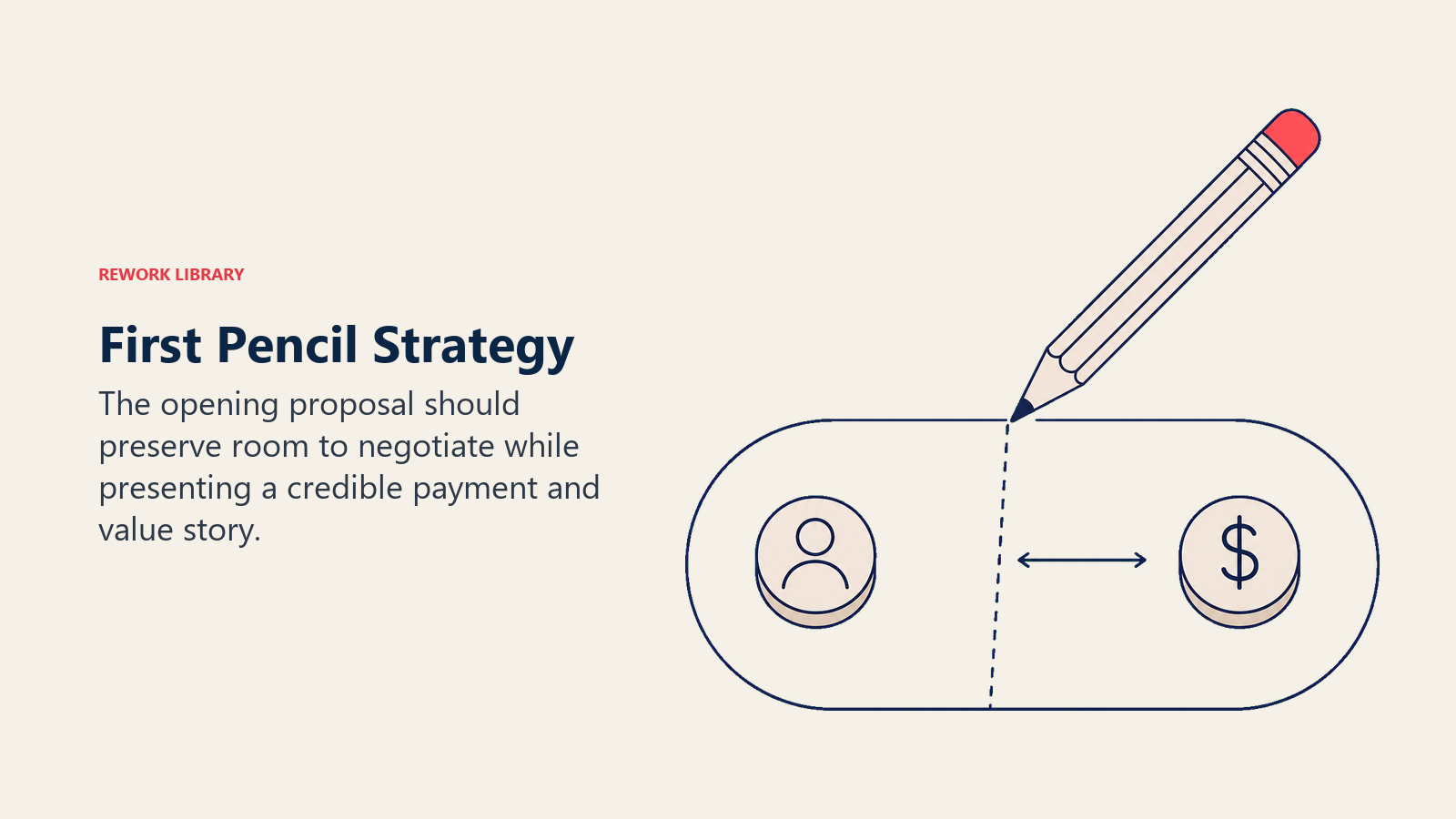

First Pencil Strategy

Your first pencil sets the tone for the entire negotiation. Too aggressive and you lose credibility or blow up the deal. Too soft and you leave profit on the table. The philosophy debate: aggressive vs. reasonable first pencil. The aggressive approach starts high, close to MSRP on price, below ACV on trade, maximum payment. The idea is that you can always come down, but you can't go back up. This works in hot markets or with buyers who expect negotiation.

The reasonable approach starts with a defensible number, one you can justify based on market pricing, trade value, and payment reality. This builds trust and often leads to faster closes. It works better with educated buyers who've done their research.

Payment-based vs. price-based presentation matters. Most customers think in payments, not prices. If you can structure a deal where the payment fits their budget, they'll often accept price points they'd reject if you led with price. "Based on your trade value and desired down payment, we can get you into this vehicle for $587 per month at 72 months." That's more palatable than "this vehicle is $38,500."

Trade value reveal timing is strategic. Some managers show all four numbers at once: price, trade, down, payment. Others reveal payment first, then break down the components if questioned. The four-square method was built on this concept.

Always leave negotiation room. Your first pencil should have concessions you can make during turns. If you blow your load on the first pencil, you have nowhere to go when they inevitably counter.

The Four-Square Method

The four-square worksheet is one of the most controversial tools in automotive sales. Critics call it manipulative. Defenders say it's just a negotiation framework. The truth is somewhere in between. The four-square has four boxes: selling price, trade value, down payment, and monthly payment. The idea is to control the negotiation by having four variables you can adjust. Customer wants more for their trade? Fine, but the payment goes up or the down payment increases. They want a lower payment? Extend the term or reduce the trade allowance.

Here's why it works: it prevents the customer from focusing exclusively on one variable (usually price) and forces consideration of the total deal. It also creates the perception of multiple concessions. "I can't give you that trade value and that payment, but I can improve your trade allowance by $500 if you can increase your down payment by $1,000."

But here's why it's fallen out of favor: transparency has become a customer expectation. Online pricing tools, dealer reviews, and consumer advocacy have made the four-square feel like a shell game to many buyers. If a customer perceives they're being manipulated, you lose trust and often the deal.

The modern application is more subtle. You still work with the four variables, but you present them transparently. Show the math. Explain the trade-offs. Use technology to build payment scenarios in real-time. The principle remains, you're structuring a deal with multiple levers, but the presentation is consultative rather than combative.

Payment Structuring

Most deals are won or lost on payment. That's what customers budget for, what they qualify for, and what determines whether they can afford the vehicle. Payment range discovery should happen during the needs assessment, but it often needs refinement at the desk. You need to know their maximum comfortable payment and their desired payment. These are often different. "I'd like to be around $450 but could go to $525 if needed." That $75 spread is your working room.

Term extension is your primary payment reduction tool. But it's not without consequences. An 84-month loan on a vehicle that depreciates faster than the loan amortizes creates negative equity risk. If the customer trades in three years, they could be $5,000-7,000 upside down. Some dealers limit terms based on vehicle age or depreciation profile.

Rate impact on payment and reserve creates an interesting dynamic. A lower rate makes the payment more attractive but reduces your reserve. A higher rate increases reserve but might push payment beyond the customer's budget. You need to find the balance where the payment works and you still capture reasonable backend gross.

Down payment negotiation is about finding cash the customer might have. "If we could get your payment to $495, could you put another $1,000 down?" Sometimes the answer is yes. They have cash but were holding it back. Sometimes it's legitimately no. They're tapped out.

Trade Equity Management

Trade equity, or the lack of it, dramatically impacts deal structure. Positive equity is a beautiful thing. The customer owes $12,000 and the trade is worth $16,000. That's $4,000 you can use as down payment on the new vehicle. This improves their equity position, lowers their payment, and might get them a better interest rate. Don't give this away. Position it as value they're bringing to the transaction.

Negative equity is more challenging. They owe $18,000 and the trade is worth $14,000. That's $4,000 you need to bury in the new deal. This increases their loan-to-value ratio, which might affect interest rate approval. It also increases their payment.

The presentation matters: "Your current vehicle has a payoff of $18,000. Based on current market conditions, we're showing an actual cash value of $14,000. That creates a $4,000 difference we need to account for in the new vehicle structure. Here's how we can make that work..."

Then you show the math. The new vehicle is $32,000. Add the $4,000 negative equity and you're financing $36,000. At 72 months and 6.9% that's $607/month. Can they afford that? If not, you need to extend the term, increase down payment, or find a less expensive vehicle.

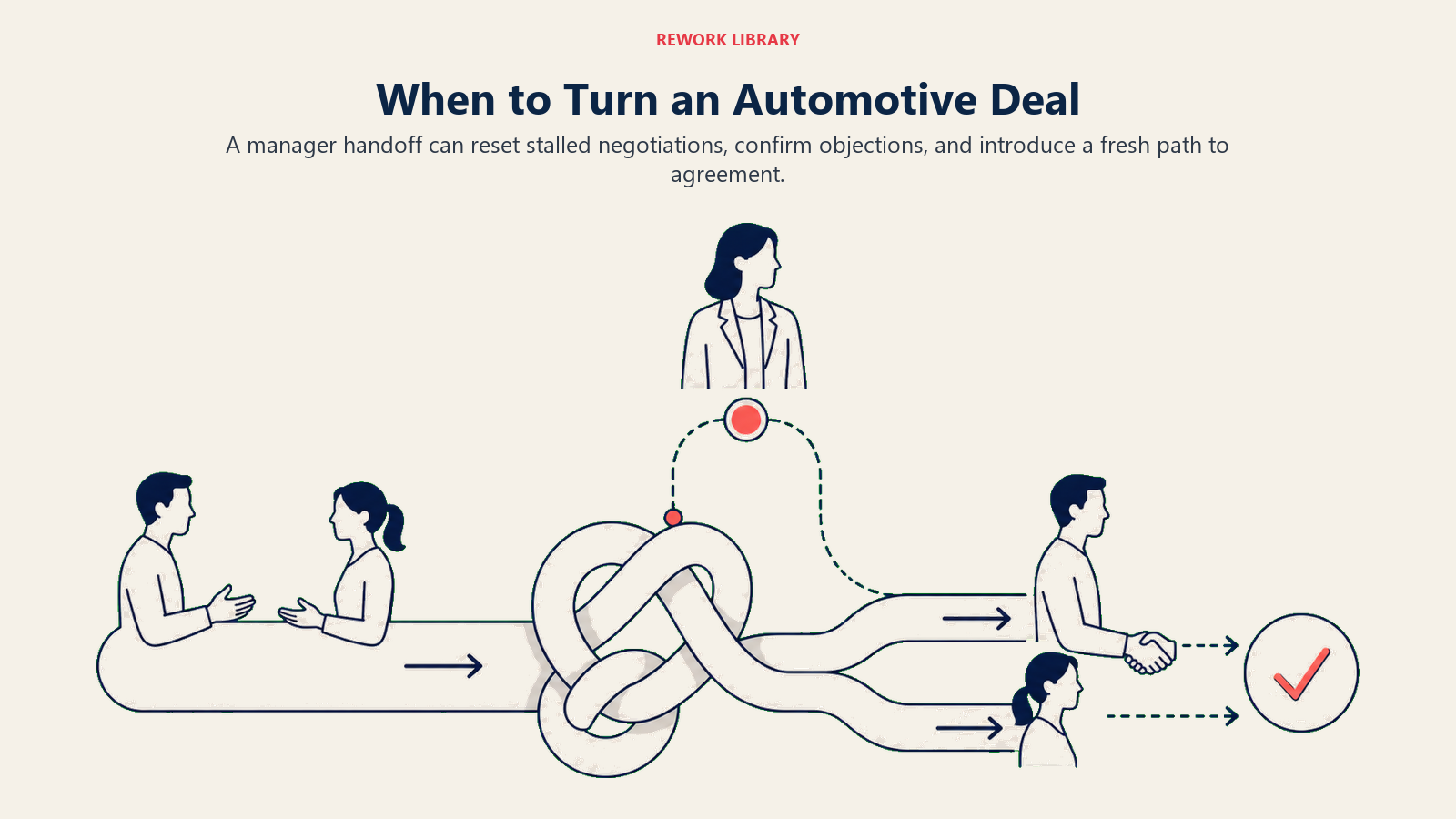

Turning the Deal

The turn is where deals are made or lost. The customer presents a counter-offer. How you respond determines whether you close or they walk.

Manager bump strategy is simple: you make one significant move that shows good faith but doesn't give away the farm. "Let me see what I can do" (go to your office, wait a few minutes, work the numbers). Come back with an improved offer that addresses their primary objection. "I was able to get approval to improve your trade allowance by $750 and reduce your payment to $545. That's as close as we can get to your target."

Incremental concession pattern is basic negotiation psychology. Your first concession is larger than your second, which is larger than your third. This creates the perception that you're running out of room. Move $500, then $300, then $100. They understand they're approaching your limit.

Walking from unprofitable deals is necessary. Not every deal makes sense. If you're into a vehicle for $28,500 and they're offering $27,800 with nothing down and a $3,000 overallowance on trade, you're looking at a $4,200 loser. Some managers will take a small loss to move aged inventory or hit a volume bonus. But chronic money-losing deals will destroy your department's profitability.

Final turn techniques include the takeaway ("I understand we're not close on numbers. Let me get your keys and pull your trade back around") and the summary close ("So if I can get to a $525 payment with your $2,000 down and the $15,500 trade allowance, we have a deal?"). These negotiation closing techniques separate experienced desk managers from novices.

F&I Setup

The desk manager's job doesn't end when the customer agrees to terms. How you structure the deal and hand it off to F&I dramatically impacts backend gross. Setting payment expectations below maximum is critical. If the customer qualifies for $600/month but you agree to $565, you've created $35/month of room for F&I to add products. The F&I manager can present a VSC and GAP that add $27/month and still come in below the customer's stated maximum. If you use all their budget on the vehicle deal, F&I has nowhere to go.

Leaving room for product adds means understanding the payment impact of typical F&I products. A $2,500 VSC at 72 months adds about $35-40/month. GAP at $795 adds $11-13/month. If you know the customer can afford another $50-75/month beyond the agreed payment, you're setting up F&I for success.

Pre-selling products during negotiation is increasingly common. "The payment we're agreeing to covers just the vehicle and your trade. When you meet with our finance manager, they'll show you some protection options that would add about $30-40 per month if you're interested." This plants the seed and prevents payment shock in F&I.

Smooth hand-off to F&I means clear communication. What did you promise the customer? What's their approved buy rate? How much room do they have on payment? What's their credit profile? The F&I manager needs this context to structure their presentation effectively.

Good desk managers think beyond front-end gross. You're structuring the entire transaction, front and back. A deal with $1,200 front-end gross and $2,200 backend gross is better than one with $1,800 front and $800 back. As industry experts note, optimum deal structure requires getting vehicle gross first while leaving room to maximize backend profit. Protect both sides of the deal and you'll maximize total profitability while delivering value customers appreciate.