F&I Department Overview - Finance & Insurance Profit Center Fundamentals - 2026 Guide

Here's a number that should get every dealer principal's attention: the F&I department typically produces 40-60% of a dealership's net profit while representing only about 15% of total gross sales. No other department delivers that kind of profit density.

Here's a number that should get every dealer principal's attention: the F&I department typically produces 40-60% of a dealership's net profit while representing only about 15% of total gross sales. No other department delivers that kind of profit density.

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

A well-run F&I department generates $2,000-2,500 per vehicle retail (PVR) at profitable stores. That's not a fluke or good fortune. It's the result of skilled managers, proper product selection, compliant processes, and strategic integration with the sales department.

But F&I is also the department most exposed to regulatory scrutiny, legal liability, and reputation risk. A single compliance violation can trigger lawsuits, regulatory sanctions, and brand damage that wipes out years of profit. Understanding how F&I generates revenue while maintaining compliance is essential for any dealership leader.

F&I Department Role

The F&I department is far more than a paperwork processing center. It's a profit-generating, customer-serving, compliance-managing operation that touches every vehicle sale. Finance source management means building and maintaining relationships with lenders across the credit spectrum. Your F&I managers need to know which lenders to submit deals to based on credit profile, loan-to-value, and approval likelihood. They negotiate buy rates, manage dealer reserves, and optimize finance penetration.

Product presentation and sales is where most F&I profit comes from. Your managers present vehicle service contracts (extended warranties), GAP insurance, maintenance plans, and ancillary products through consultative selling processes. This isn't order-taking, it's needs-based selling that protects customers and generates profit.

Compliance and documentation protects the dealership from regulatory violations and legal exposure. Every finance contract must comply with federal lending laws (TILA, ECOA, FCRA) and state-specific regulations. Documentation must be accurate, complete, and properly disclosed. F&I managers are the gatekeepers. Proper compliance best practices are essential.

Customer experience final impression happens in the F&I office. The customer has agreed to buy the vehicle. They're excited. Your F&I manager either reinforces that excitement with professional service and valuable protection products, or they kill the deal with aggressive tactics and transaction friction. CSI scores often reflect F&I experience as much as sales experience.

Revenue Streams

F&I departments generate profit through multiple channels. Understanding each revenue stream helps you optimize the mix. Finance reserve (rate markup) is revenue earned when you mark up the buy rate from the lender. If a lender approves a customer at 5.9% (buy rate) and you charge the customer 7.9% (sell rate), that 2% spread generates dealer reserve. Regulations limit how much you can mark up (typically 2-2.5%), and reserve is subject to chargeback if the customer pays off early.

Reserve on a $30,000 72-month loan at 2% markup is about $1,800-2,000. That's significant profit, but it requires finance penetration. Cash deals and outside financing generate zero reserve.

VSC/extended warranty commission is usually the largest F&I product revenue source. Dealerships earn 30-50% commission on VSC sales. A $2,800 VSC generates $840-1,400 in commission. At 50% penetration on 100 monthly sales, that's $42,000-70,000 in monthly gross.

GAP insurance commission provides 40-60% commission on a lower-cost product. A $795 GAP policy generates $320-475 in commission. GAP penetration rates are often higher than VSC (60-70%) because the value proposition is simpler: it covers the difference between insurance payout and loan balance if the vehicle is totaled.

Ancillary product sales include maintenance plans, tire & wheel protection, theft deterrent systems, key replacement coverage, and appearance protection. These products generate lower per-unit revenue ($50-200 commission each) but can add up with volume and penetration.

Documentation fees are administrative fees charged to process paperwork. Most states regulate doc fee maximums ($200-800 depending on state). This isn't a profit center so much as cost recovery, but it contributes to overall department revenue.

Key Performance Metrics

You can't manage what you don't measure. F&I departments live and die by specific KPIs. Per Vehicle Retail (PVR) by product shows you which products drive profit. Track VSC PVR, GAP PVR, maintenance PVR, and ancillary PVR separately. This reveals whether low total PVR is a penetration problem (not selling enough units) or a value problem (selling cheap products).

Industry benchmarks: VSC PVR of $600-900, GAP PVR of $200-350, maintenance PVR of $150-300, ancillary PVR of $150-250.

Total backend PVR combines all F&I revenue sources including reserve. Top-performing F&I managers generate $2,200-2,800 backend PVR. Average performers hit $1,500-1,800. Underperformers struggle to reach $1,200.

Finance penetration rate measures what percentage of deals are financed through the dealership vs. cash or outside financing. Target: 75-85%. Below 70% and you're leaving significant reserve on the table. Above 85% is exceptional and requires strong lender relationships and competitive rates.

Product penetration rates show selling effectiveness by product. VSC penetration: 45-60% is good, 60%+ is excellent. GAP penetration: 55-70% is standard, 70%+ is exceptional. Maintenance plan penetration varies by brand and customer demographic: 25-50% is typical.

Chargeback rate measures how often you're paying back commission because customers cancel products or refinance loans within chargeback periods (typically 90-180 days). Target: under 8%. Above 12% indicates poor product presentation or buyer's remorse issues.

Time in F&I office affects customer satisfaction and department throughput. Target: 35-50 minutes per deal. Under 30 minutes suggests rushed presentations and low penetration. Over 60 minutes creates customer frustration and operational bottlenecks.

The F&I Manager Profile

Not every salesperson makes a good F&I manager. The skill sets are different. Compliance knowledge and discipline is non-negotiable. F&I managers must understand lending regulations, product disclosure requirements, and documentation standards. They need to care about compliance, not view it as bureaucratic hassle. A manager who cuts corners on disclosure or discrimination policies creates massive liability.

Sales ability is still critical, but it's different from vehicle sales. F&I managers aren't creating demand, the customer already decided to buy. They're presenting protection products through consultative, needs-based selling. The best F&I managers ask questions, listen actively, and position products as solutions rather than pushing transactions.

Customer relationship management matters because F&I is the last touchpoint before delivery. A skilled F&I manager enhances the experience with professional service, clear explanations, and genuine care for customer protection. A weak manager creates friction with aggressive tactics or confusing presentations.

Technology proficiency is increasingly important. F&I managers use multiple systems daily: dealer management systems (DMS), electronic menu tools, lender portals, e-contracting platforms, and compliance monitoring software. Comfort with technology directly impacts efficiency.

Ethical standards and integrity protect the dealership and customer. F&I managers have access to sensitive customer information, authority to structure financing, and control over product disclosures. They must operate with integrity even when it costs a sale.

F&I Office Setup

The physical and technical environment impacts F&I performance. Office location and environment should be professional but comfortable. Locate F&I offices near the sales floor for easy handoffs but away from noise and distraction. Customers need to focus on paperwork and product presentations without sales floor chaos.

Professional doesn't mean intimidating. A desk, two chairs, good lighting, and a clean environment work better than imposing power dynamics with big desks and formal arrangements. Many dealerships use round tables or side-by-side seating to create collaborative rather than adversarial feeling.

Menu presentation technology has evolved from paper four-squares to electronic menu systems. Tools like Route One, DealerTrack, or manufacturer-specific menu systems present products visually with payment comparisons. Electronic menus improve presentation consistency and compliance documentation.

Finance portal access to lender systems is essential. F&I managers need real-time access to credit decisioning, rate sheets, and funding status. Integration between your DMS and lender portals reduces data entry errors and speeds deal processing.

Document management systems store completed contracts, product applications, and compliance documentation. Digital document management (e-contracting) is becoming standard, reducing paper storage requirements and enabling faster audits.

Compliance monitoring tools track required disclosures, flag potential fair lending violations, and ensure documentation completeness. Tools like Compliance Depot or DealerPolicy provide automated compliance checks before deals are funded.

Finance Source Management

Your lender network directly impacts approval rates, reserve potential, and finance penetration. Captive vs. independent lenders serve different purposes. Captive finance companies (manufacturer-owned) offer subvented rates, higher approval rates on franchised brands, and program incentives. But they're selective on credit quality and focus on new vehicle financing. Learn more about finance source management strategies.

Independent lenders (banks, credit unions, sub-prime companies) fill gaps. They finance used vehicles, approve lower credit scores, and sometimes offer more competitive rates on prime credit deals.

Buy rates and rate markup determine reserve. Buy rates are what lenders charge. Your markup within regulatory limits generates dealer reserve. Competitive buy rates let you mark up while remaining attractive to customers.

Approval rates and credit tiers vary by lender. Some lenders specialize in prime credit (720+ scores), others in sub-prime (600-660), and special finance companies handle deep sub-prime (below 600). Your lender mix needs coverage across all tiers.

Program participation requirements from captive lenders often include manufacturer certification, training requirements, volume commitments, and customer satisfaction standards. Meeting these requirements maintains access to subvented rate programs and incentive bonuses.

Product Portfolio

F&I profitability depends on having the right products at the right price points. VSC/extended warranties are the most profitable F&I products. Commission rates of 40-50% and average retail prices of $2,200-3,500 generate significant PVR. VSCs cover mechanical and electrical failures after manufacturer warranty expires. Customer value is clear: a single transmission repair can cost $4,500-6,000.

GAP insurance has high penetration because the value proposition is simple: if your financed vehicle is totaled, GAP covers the difference between insurance payout and loan balance. With long loan terms and slow depreciation, most customers have GAP exposure in the first 2-3 years.

Maintenance plans pre-package scheduled maintenance (oil changes, tire rotations, inspections) at a discounted price. These products generate moderate commission ($150-300) with decent penetration (30-45%) on new vehicles. They also drive service retention.

Tire & wheel protection covers damage from road hazards (potholes, nails, curbs). Average cost: $695-995. Commission: $200-400. Penetration varies by geography, higher in areas with bad roads or harsh winters.

Key replacement coverage addresses a real pain point: modern key fobs cost $300-600 to replace. For $295-495, customers get lost key replacement. Easy sale with low cost and clear value.

Theft deterrent products include VIN etching, tracking systems, and theft recovery services. These products have fallen out of favor due to compliance scrutiny (sometimes viewed as low-value compared to price).

Appearance protection (paint protection, fabric protection) generates good commission but lower penetration. Customers often view these as lower priority compared to mechanical protection.

Compliance Requirements

F&I is the most regulated department in the dealership. Violations create serious liability. Equal Credit Opportunity Act (ECOA) prohibits discrimination in lending based on race, color, religion, national origin, sex, marital status, or age. F&I managers can't ask prohibited questions or make credit decisions based on protected characteristics. The Consumer Financial Protection Bureau enforces ECOA compliance across all creditors, including automotive dealerships. Violations trigger lawsuits and regulatory penalties.

Fair Credit Reporting Act (FCRA) regulates how you access and use credit reports. You need customer authorization before pulling credit. You must provide adverse action notices if you deny credit or charge higher rates based on credit information. FCRA violations carry statutory damages of $100-1,000 per violation.

Red Flags Rule requires identity theft prevention programs. F&I managers must verify customer identity and watch for red flags like inconsistent information, suspicious documents, or unusual account activity. The FTC Safeguards Rule, which took effect in June 2023, requires dealerships to maintain comprehensive information security programs to protect customer data.

State-specific F&I regulations vary significantly. Some states cap doc fees. Others limit rate markup. Some require specific product disclosures or cooldown periods. California, Texas, and Florida have particularly detailed F&I regulations.

Documentation requirements include complete credit applications, truth-in-lending disclosures (TILA), rate and term confirmations, product disclosure forms, and customer signatures acknowledging receipt. Missing documentation creates funding delays and compliance exposure.

Rate and product disclosure must be clear and accurate. Customers need to understand the interest rate, total finance charge, payment amount, and product costs separately from the vehicle price. Bundled pricing or unclear disclosures violate lending laws.

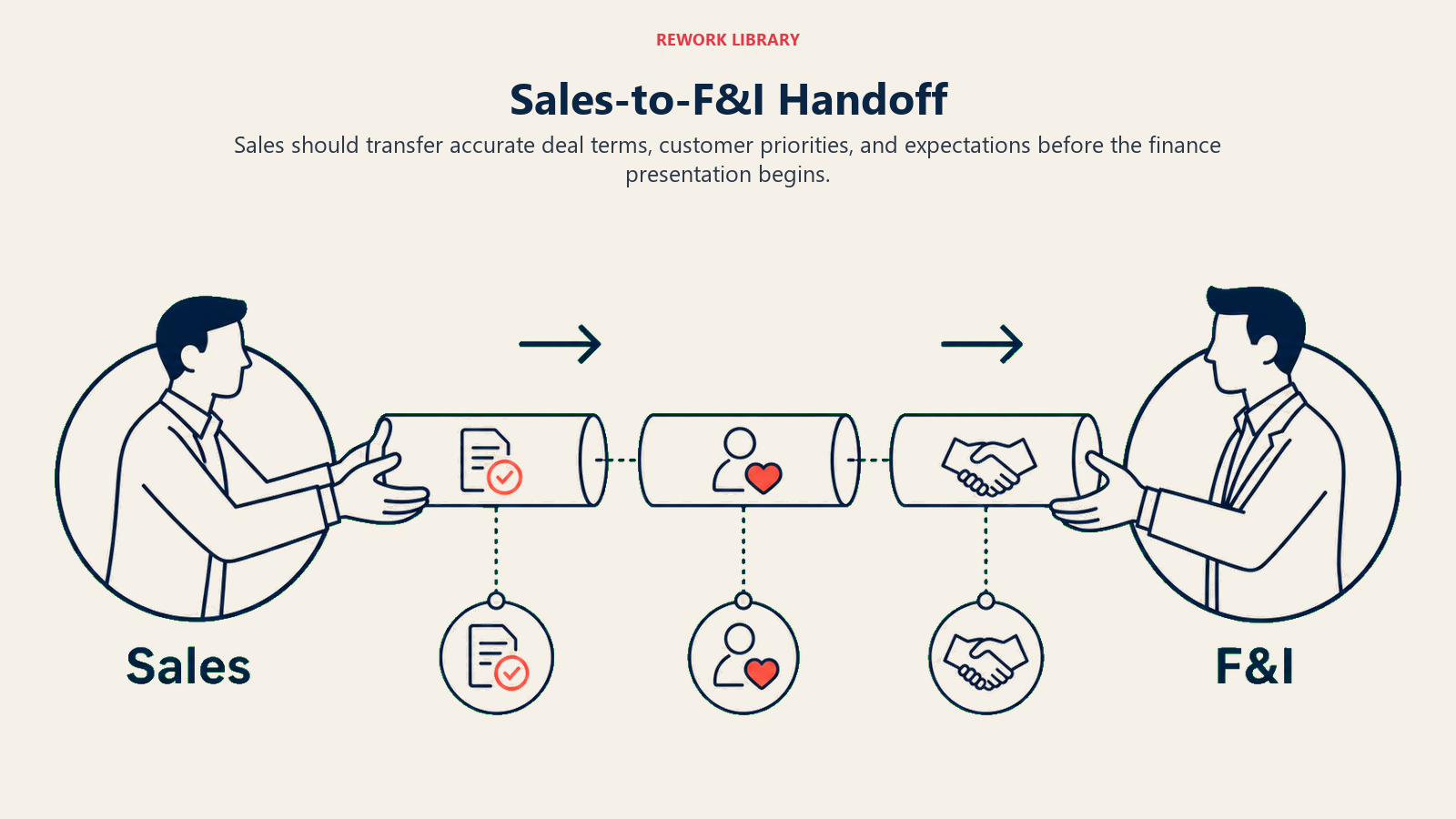

Sales-to-F&I Handoff

The transition from sales to F&I impacts both customer experience and backend gross.

Information transfer should be complete before the customer enters F&I. The F&I manager needs to know the vehicle sold, agreed price, trade details, credit application status, and any product pre-selling that occurred. Incomplete information forces the F&I manager to ask redundant questions that frustrate customers.

Setting customer expectations starts in sales. Sales consultants should prepare customers: "Our finance manager will review your payment options and show you some protection products you might be interested in. Plan for about 45 minutes to complete paperwork." This prevents surprise when customers expect to "just sign and leave."

Pre-selling products during sales negotiation plants seeds for F&I. "The payment we're agreeing to covers the vehicle. Our finance manager will show you warranty and protection options that would add about $30-40/month if you're interested." This makes F&I presentation an expected part of the process.

Timing and momentum matter. Don't make customers wait 45 minutes after they agree to buy. That kills enthusiasm and creates buyer's remorse. Target handoff within 15 minutes of deal agreement. Keep momentum moving toward delivery.

F&I is where dealerships make real money, but it's also where they take on real risk. The best F&I departments balance profit generation with compliance discipline, customer service with product presentation, and efficiency with thoroughness. Get it right and F&I becomes your most valuable profit center. Get it wrong and you're looking at lawsuits, regulatory sanctions, and brand damage that takes years to repair. Track your F&I PVR performance to optimize profitability.