Automotive Digital Retailing: 2026 Guide (With Examples)

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

76% of car buyers want to complete most of the purchase process online before stepping into a showroom. In fact, 91% of buyers now complete some or all purchase steps online according to Cox Automotive's 2025 Car Buyer Journey Study. Understanding the full automotive customer journey helps you meet buyers where they are. That's not a future trend. It's today's reality. And dealers who treat digital retailing as just another lead generation tool are missing the bigger opportunity. This isn't about creating a better form. It's about redesigning how vehicles get sold.

The question isn't whether your dealership should offer digital retailing. It's how you'll implement it without sacrificing the profitability that comes from face-to-face F&I presentations, trade-in negotiations, and skilled sales professionals who know how to structure deals.

Digital retailing done right increases both customer satisfaction and dealership profit. Done poorly, it becomes an expensive lead capture tool that trains customers to grind you on price.

The Digital Retailing Landscape

COVID-19 didn't create the demand for online car buying. It accelerated a shift that was already happening. Carvana and Vroom demonstrated what was possible. Tesla proved that consumers would buy $60,000 vehicles without a test drive. And traditional dealers scrambled to respond with technology that often fell short of consumer expectations. McKinsey research shows that almost 60% of potential car buyers under 45 prefer to purchase their vehicle online, representing a fundamental shift in buyer expectations.

The result? A gap between what buyers expect and what most dealerships deliver. Buyers research for weeks online, configure their ideal vehicle, calculate payments, and estimate their trade-in value. Then they arrive at the dealership expecting a quick transaction, only to spend four hours in the showroom reliving the entire process.

That disconnect doesn't just frustrate customers. It leaks gross profit. When customers have already done all the work themselves online, they've often anchored to payment amounts that don't include F&I products, realistic trade-in values, or proper finance structures.

True digital retailing gives customers the option to complete as much of the transaction online as they want, while creating opportunities for your team to add value, build relationships, and protect profit margins.

What is Digital Retailing

Digital retailing is end-to-end online transaction capability. Not a payment calculator. Not a lead form with extra fields. It's the ability for a customer to select a vehicle, value their trade, structure financing, choose F&I products, sign contracts, and complete a purchase entirely online, if they want to.

The components include:

Vehicle selection and configuration - Customers browse inventory, compare vehicles, and build their ideal specification with available options and accessories. Strong dealership website optimization provides the foundation.

Trade-in appraisal tools - Instant valuations based on condition, mileage, and market data, with photo uploads for more accurate assessments.

Payment calculation and structuring - Real-time payment estimates based on actual rates, terms, and down payment options. Not theoretical rates that fall apart when the credit app runs.

F&I product presentation - Menu-style presentation of extended warranties, GAP, maintenance plans, and other protection products with clear value propositions.

Credit application and approval - Soft credit pulls that show real financing options without impacting credit scores, followed by full applications that route to your lender network.

Digital contracting and e-signature - Legally compliant electronic signing of all purchase documents, retail installment contracts, and required disclosures.

Home delivery vs pickup options - Customer choice of having the vehicle delivered to their home or scheduling a convenient pickup time at the dealership.

The key word is "option." Digital retailing shouldn't force customers into a purely online experience any more than traditional dealerships should force everyone into a four-hour showroom visit. It's about meeting customers where they are in their buying journey.

Digital Retailing Platform Options

You've got two choices: build or buy. Building your own digital retailing platform sounds appealing until you calculate the development cost, integration complexity, ongoing maintenance, and the fact that you're now competing with well-funded technology companies that do nothing but this.

Most dealers buy. The major providers include:

Roadster - Known for strong user experience and design. Good integration with major DMS platforms. Higher price point but comprehensive feature set including desking tools for your team.

Upstart - Strong on the lending side with their own finance network. Good for dealers who want to streamline credit decisions and offer more financing options to subprime customers.

Shift Digital - Solid middle-market option with good CRM integration. Less expensive than Roadster but fewer advanced features.

DealerSocket - Part of the larger CRM ecosystem, so integration is seamless if you're already using their platform. More focused on lead management than pure digital retailing.

Platform costs typically range from $1,000 to $3,000+ per month depending on features, transaction volume, and integration requirements. Implementation takes 30-90 days for most dealers.

The critical factors aren't just features and price. It's integration with your existing DMS, CRM, and website. A digital retailing platform that creates manual work for your BDC or requires double-entry into your DMS won't get used. Your team will find workarounds that defeat the entire purpose.

The Digital Retailing Journey

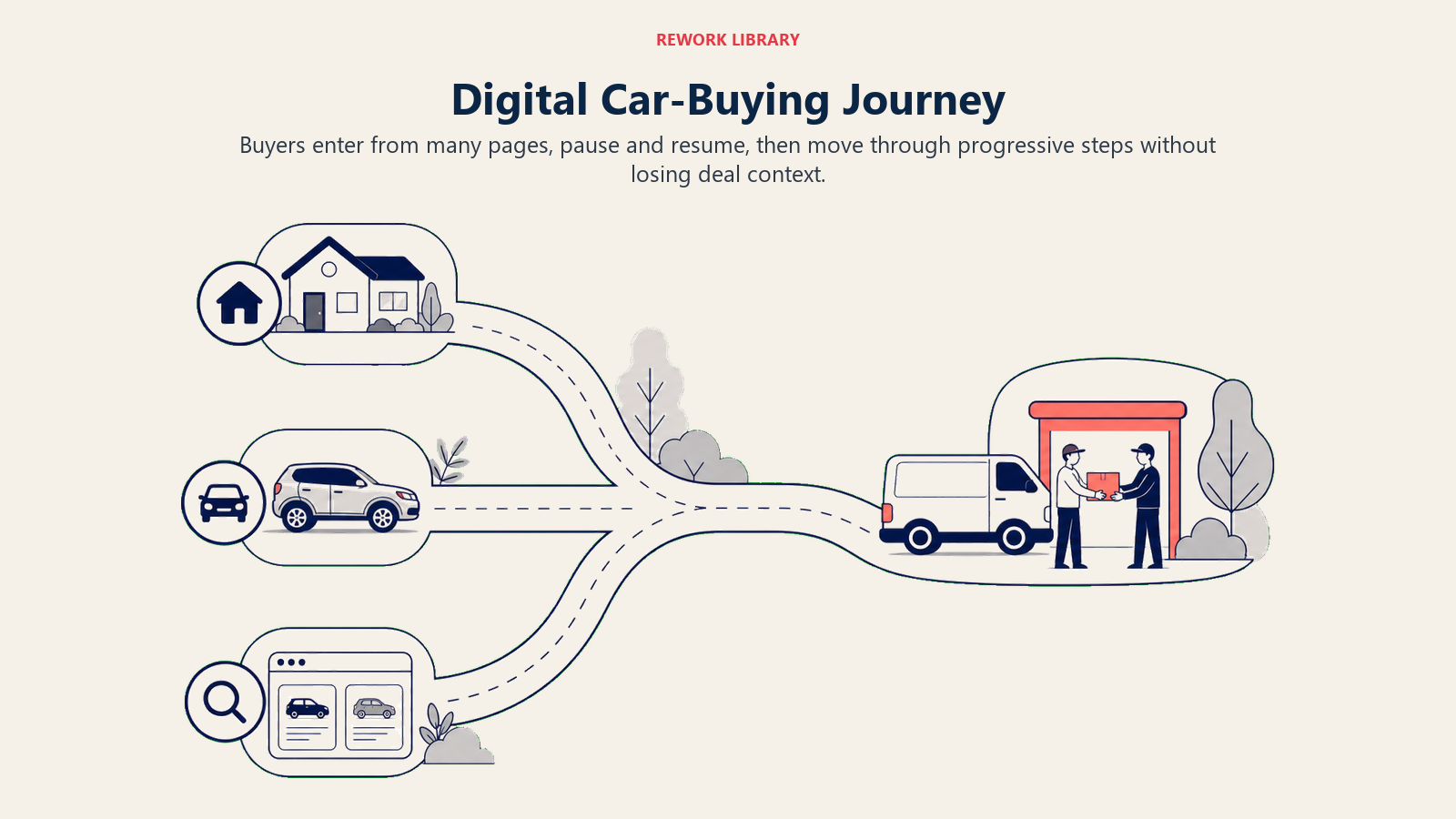

Not every customer enters digital retailing the same way. Some start from your homepage. Others arrive at a specific VDP from a search ad. Many abandon and resume days later. Your platform needs to accommodate all these entry points.

Progressive disclosure is the key. Don't force customers to answer 47 questions before they see a payment estimate. Start with the vehicle price and one or two basic inputs (down payment, trade-in yes/no), then progressively disclose more detail as they engage.

Most platforms now allow customers to pause and resume their session. They can start on their phone during lunch, continue on their laptop at home, and finish on their tablet over the weekend. Session persistence is critical because the average car buying journey spans 14-30 days.

Human assistance touchpoints matter. Even customers who want to complete everything online often have questions. Live chat, SMS, and phone support integrated into the digital retailing experience convert better than forcing customers to leave the flow to contact you.

The final step, showroom visit vs delivery, depends on your state's legal requirements and your operational capability. But even customers who choose home delivery often benefit from a brief delivery appointment where you demonstrate vehicle features, ensure satisfaction, and create a relationship for future service business.

Trade-In Appraisal Online

This is where digital retailing often breaks down. Customers enter their vehicle info and get an instant valuation that's $3,000 higher than what you'll actually pay. They structure their entire deal around that number. Then they show up and you have to reset expectations.

The best platforms integrate with Kelley Blue Book Instant Cash Offer, Black Book, or similar tools that provide market-based valuations. But they're still estimates until you inspect the vehicle.

Set clear expectations. Use language like "estimated value pending inspection" or "conditional offer subject to vehicle condition verification." Show a range rather than a specific number when possible.

Some dealers are using photo upload and AI inspection tools that let customers document their vehicle's condition. The more information you gather online, the more accurate your appraisal can be, and the fewer surprises when they arrive.

But here's the truth: trade-in valuation will always require human judgment for accuracy. The goal isn't to eliminate the appraisal process. It's to give customers a realistic starting point and collect the information your team needs to make a fast, accurate offer when they arrive.

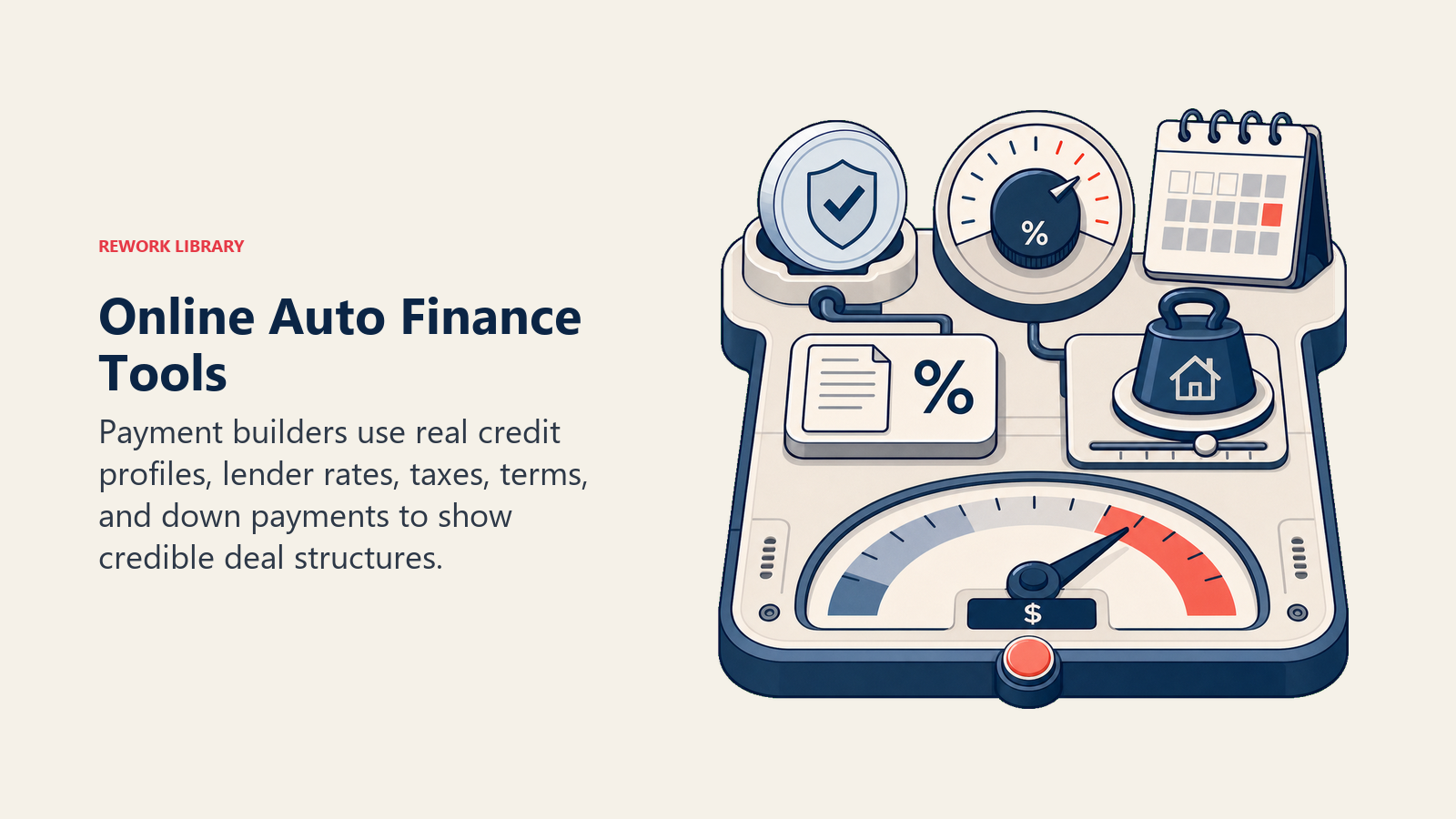

Online Finance & Payment Tools

There's a huge difference between a payment calculator and a payment builder. Calculators show theoretical payments based on inputs the customer makes up. Builders show real payments based on their actual credit profile and your lender rates.

Real-time lending decisions are possible now through platforms like Upstart and RouteOne that do soft credit pulls. Customers see their actual approval odds and real rate ranges without impacting their credit score. This is dramatically better than showing everyone 2.9% APR rates that only 15% of customers qualify for.

Show multiple finance offers when possible. Cash vs finance. Different term lengths. Lease options if applicable. Give customers real choices instead of steering them to whatever maximizes your finance reserve.

Transparent pricing builds trust. But transparency doesn't mean giving away all your profit. It means showing customers what they're getting and why it costs what it costs. Structure payments that include realistic F&I product assumptions so customers aren't shocked when you present the full menu.

The dealers doing this well are actually maintaining or increasing their F&I PVR because they're setting proper expectations online and educating customers about product value before they arrive.

Digital F&I Product Presentation

This is the part that terrifies most dealers. If customers are buying online, how do you present F&I products with the same effectiveness as a skilled F&I manager in a closing room?

You don't. At least not with the same conversion rates. But you can get close if you do it right.

Present F&I products as part of the payment structure, not as add-ons at the end. Show payments with and without protection products. Use clear, simple language that explains what's covered and why it matters. Include customer testimonials and claim examples that demonstrate real value.

Video presentations work surprisingly well. A 90-second video from your F&I manager explaining GAP coverage converts better than three paragraphs of text. Customers can watch it multiple times. They can share it with their spouse. And it humanizes the online experience.

Most successful dealers present products online but complete the sale in-person or over the phone. The digital platform educates and gets customers thinking about protection. Your F&I manager closes the deal with personalized recommendations based on their driving habits, budget, and risk tolerance.

The compliance considerations are significant. All disclosures required for in-person transactions apply online. Your platform must capture acknowledgments, display terms clearly, and create an audit trail. Work with your compliance attorney to ensure your digital F&I process meets all state and federal requirements.

Implementation Strategy

Don't go live with digital retailing on Monday and expect customers to start buying vehicles online by Friday. Implementation requires a phased approach that gives your team time to learn, adjust processes, and build confidence.

Start with a pilot phase. Enable digital retailing for a subset of inventory or specific customer segments. Test with employees and friends first. Work out the bugs before promoting it broadly.

Staff training is critical. Your BDC agents need to know how to assist customers who start online. Your sales team needs to understand how to continue deals that began digitally. Your F&I managers need training on presenting products to customers who've already built their deal online.

Process re-engineering is often more challenging than the technology itself. Your desking process, credit submission workflow, and vehicle delivery procedures all need adjustment. Document new processes clearly and get buy-in from managers before rolling out to the full team.

Market digital retailing to customers once you're confident it works. Add it to your website prominently. Mention it in email campaigns and video content. Train your phone team to offer it as an option for customers who prefer to work from home.

The biggest mistake is launching half-baked digital retailing that frustrates customers and makes your dealership look incompetent. Better to take an extra month in pilot phase than to create a terrible first impression.

Balancing Convenience with Profitability

Here's what keeps dealer principals up at night: will digital retailing compress gross profit and F&I income to levels that make it unsustainable?

It can, if you let it. Dealers who treat digital retailing as just another race to the bottom on price will see exactly that result. But dealers who use it strategically see different outcomes.

Front-end gross typically compresses slightly in digital transactions, about $200-400 per unit on average. Customers who've done extensive research and compared prices online are less willing to pay large markups. But you save time and efficiency costs. Deals that took 3-4 hours now take 90 minutes. Sales people can handle more volume. In fact, 67% of dealers saw an improvement in gross profit per deal due to digital retailing, while 80% reported a positive impact on vehicle sales volume, according to Cox Automotive's 2025 study.

Back-end gross can actually improve if you present F&I products effectively online. Customers have time to research and understand product value without feeling pressured. They can discuss options with their spouse before making decisions. And they've already mentally committed to a payment amount that includes protection.

The net impact depends on your execution. Dealers who maintain the same value-added service, expert guidance, and relationship-building in a digital format maintain profitability. Those who compete purely on price and eliminate human touchpoints struggle.

Customer satisfaction scores typically improve with digital retailing options. Not because everyone wants to buy online, but because you're meeting different customers' preferences. Cox Automotive reports that 76% of new-vehicle buyers indicated they were highly satisfied with the process, an all-time high, with consumers who heavily engaged in digital retailing saving 42 minutes at the dealership. CSI improvement often leads to better manufacturer allocations, higher bonuses, and more referral business.

Measuring Digital Retailing Success

You can't manage what you don't measure. Track these metrics monthly:

Digital retailing start rate - What percentage of website visitors begin a digital retailing session? Industry average is 8-15%. If you're below 5%, your promotion or user experience needs work.

Completion rate - What percentage of started sessions result in a completed deal? This varies widely (2-15%) based on how you define "completion." Some dealers count online deposits. Others only count fully signed contracts.

Blended transactions - Most deals aren't purely online or purely showroom. They blend both. Track what percentage of deals involve digital retailing at some point in the process.

Deal structure comparison - Compare digital-started deals to traditional deals. Look at front gross, back gross, total profit, F&I penetration, and finance reserve. Identify gaps and coach your team.

Customer satisfaction scores - Survey customers who used digital retailing separately from those who didn't. If CSI is lower for digital customers, you've got user experience or process issues to address.

Total cost per sale - Factor in platform fees, implementation costs, and staff training. Calculate your true cost per sale including all digital retailing expenses. Compare to your customer acquisition cost from other channels.

The goal isn't perfect metrics from day one. It's continuous improvement over time as you learn what works for your market, your customers, and your team.

Moving Forward

Digital retailing isn't a temporary trend or a nice-to-have feature. It's fundamental to how vehicles will be sold for the foreseeable future. The dealers who figure it out early, who learn to balance convenience with profitability, technology with human relationships, and efficiency with value, will have a significant competitive advantage.

The dealers who resist, who cling to traditional processes because "that's how we've always done it," will lose market share to competitors who give customers what they actually want.

Start small if you need to. Test with a pilot program. Learn from your mistakes when the stakes are low. But start. Because your customers are already online, researching, comparing, and forming opinions about your dealership based on whether you make it easy or hard to do business with you. Strong automotive CRM implementation ties everything together.

For more on creating the foundation for digital retailing success, see Dealership Website Optimization, Automotive Customer Journey, and Mobile Experience for Buyers. To implement specific components, explore Online Trade-In Tools, Online Pricing Transparency, and Digital F&I Process.

Senior Implementation Consultant

On this page

- The Digital Retailing Landscape

- What is Digital Retailing

- Digital Retailing Platform Options

- The Digital Retailing Journey

- Trade-In Appraisal Online

- Online Finance & Payment Tools

- Digital F&I Product Presentation

- Implementation Strategy

- Balancing Convenience with Profitability

- Measuring Digital Retailing Success

- Moving Forward