GAP Insurance Sales - Payment Protection & High-Penetration Strategies

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Here's a fact that should inform every F&I presentation: 75% of financed vehicles will have negative equity at some point during the loan term. That's three out of four customers who owe more than their vehicle is worth. When total loss occurs during that window, customers face a devastating scenario, continuing payments on a vehicle they no longer own.

GAP insurance eliminates this exposure. It's also the easiest F&I product to sell when positioned correctly. Monthly payment impact runs $5-$15. The risk it mitigates? $5,000-$15,000 of exposure. And unlike extended warranties that require explaining coverage details, GAP presents a simple value proposition: if your car gets totaled, this pays the difference between insurance settlement and loan balance.

Top FF&I managersI managers achieve 70-80% GAP penetration. Average performers sit around 40%. The difference isn't salesmanship, it's positioning. When you frame GAP as default protection rather than optional add-on, penetration soars. This guide shows you exactly how to make that shift.

GAP Insurance Fundamentals - What It Covers

Guaranteed Asset Protection does exactly what the name suggests. When your vehicle is declared a total loss or stolen and not recovered, your auto insurance pays actual cash value (ACV). Your lender expects full loan payoff. GAP insurance covers the difference.

Coverage Trigger: Total Loss or Theft

GAP only activates in specific circumstances:

- Vehicle declared total loss by insurance company

- Vehicle stolen and not recovered within specified timeframe (typically 30 days)

- Insurance settlement is less than loan payoff

Normal wear, mechanical breakdown, or minor accidents don't trigger GAP. This is specifically total loss protection.

Gap Between ACV and Payoff

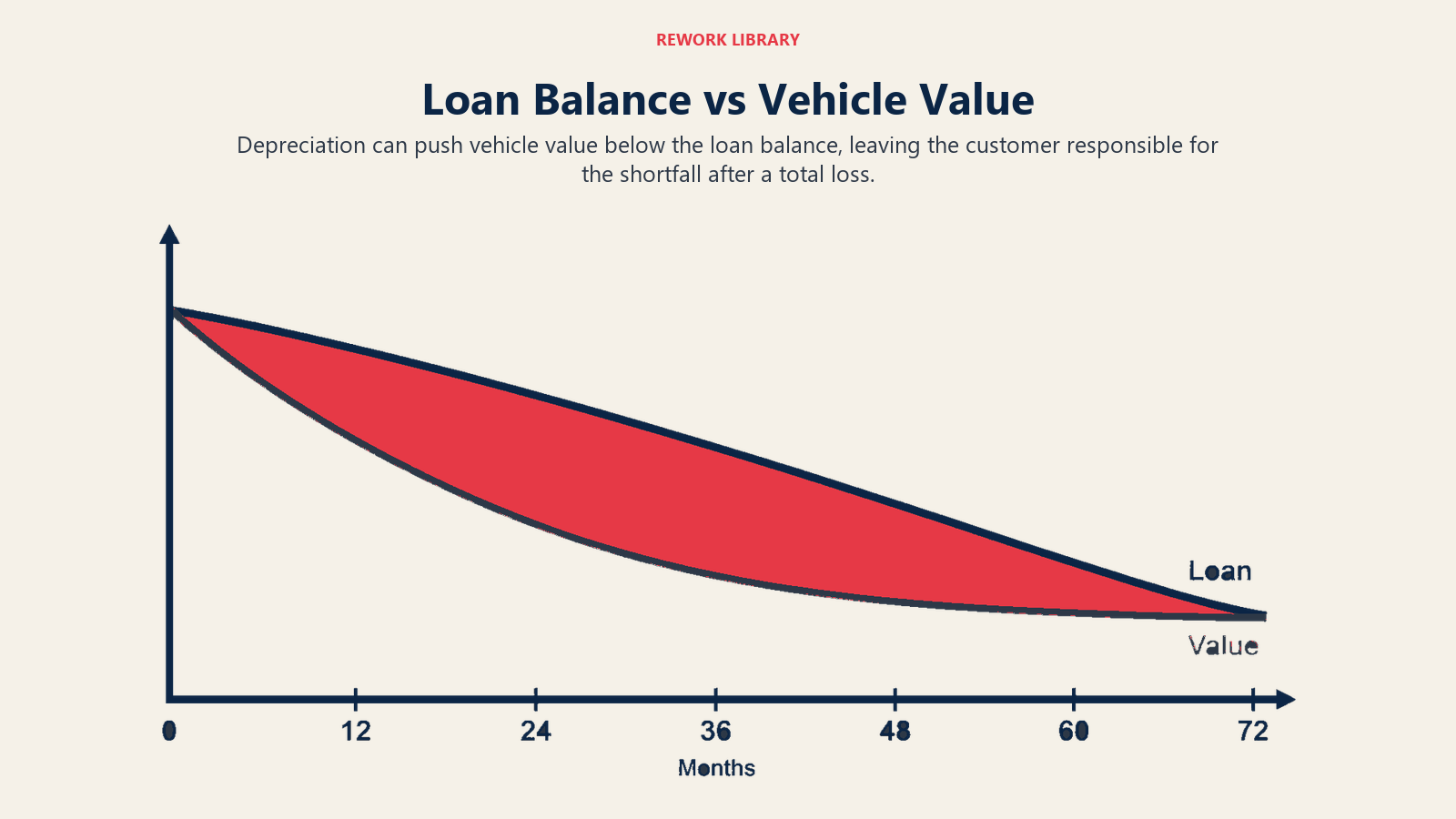

Insurance companies determine actual cash value using market comparables, vehicle condition, and depreciation. This almost always comes in below loan balance during the first 2-4 years of ownership. Here's why:

New vehicle loses 15-20% value immediately upon purchase. Add 15-20% annual depreciation for the first three years. Meanwhile, your loan amortization pays mostly interest early on, barely touching principal. By month 12, you might owe $28,000 on a vehicle worth $22,000. That's $6,000 of exposure.

GAP insurance pays that $6,000 difference (up to coverage limits, typically 125% of ACV).

New Vehicle vs. Used Vehicle Applicability

GAP works for both new and used vehicle purchases, but the risk profile differs.

New vehicles experience steeper initial depreciation. Drive off the lot, lose 20%. This creates immediate negative equity, especially with low or no down payment. New vehicle buyers need GAP from day one.

Used vehicles depreciate more slowly but often finance for longer terms or at higher rates. A 2020 vehicle purchased in 2026 with 60,000 miles still carries depreciation risk, particularly if financed for 72 months at 9% interest. Used vehicle buyers with long-term loans need GAP protection too.

Lease Gap Coverage

Lessees face similar exposure. Lease agreements specify vehicle value at lease end. If totaled before lease expiration, insurance pays ACV while lessor expects remaining lease payments plus residual value. The gap can run thousands. Most manufacturer lease programs include GAP automatically, but aftermarket leases often don't. Verify coverage on every lease transaction.

Why GAP Matters - Real-World Scenarios

Theory doesn't sell GAP. Real scenarios do. Paint the picture clearly so customers understand the nightmare you're preventing.

Rapid Depreciation (New Car Loses 20% Driving Off Lot)

"You're purchasing this vehicle for $35,000. Drive home today, and market value drops to about $28,000. That's just reality with new vehicle depreciation. If someone hits you tomorrow and totals the car, your insurance pays $28,000. You still owe $34,000 after down payment. Without GAP, you're writing a check for $6,000 on a vehicle you no longer own."

This scenario is terrifying because it's immediate. The exposure starts today.

Negative Equity from Trade-In (Burial)

Many customers walk in owing more on their trade than it's worth. You're rolling $4,000 of negative equity into the new loan. Now they owe $39,000 on a vehicle worth $35,000, before driving away. Depreciation amplifies the problem.

"We're financing $39,000. Vehicle value today is $35,000. That's $4,000 underwater before depreciation. Six months from now, you'll be $8,000-$10,000 upside down. If total loss occurs, that's your out-of-pocket expense without GAP coverage."

Customers with negative equity trades need GAP. Period. This should be 100% penetration.

Extended Term Financing (72-84 Months Underwater Longer)

Long-term financing keeps customers underwater longer. A 72-month loan takes 3-4 years to reach positive equity. That's 36-48 months of exposure.

"You're financing over 72 months. For the first three to four years, you'll owe more than the vehicle is worth. GAP eliminates that exposure during the entire period you're underwater. The coverage lasts as long as you need it."

Extended terms create extended risk. GAP becomes more valuable, not less.

Low/No Down Payment Deals

$0 down deals maximize negative equity. You're financing 100% of purchase price plus fees, taxes, and possibly rolled negative equity. First payment hasn't been made and you're already underwater $5,000-$10,000.

"With zero down, you're starting upside down. That's not a criticism, it's just the math. GAP coverage protects you during the period it takes to build equity through payments."

No down payment customers should view GAP as essential, not optional.

Total Loss Insurance Settlement Reality

Most customers assume "full coverage insurance" covers everything. It doesn't. Insurance pays market value, not payoff amount. Clarify this misconception explicitly:

"Your insurance policy covers actual cash value, what the vehicle is worth on the open market. That's usually thousands less than your loan payoff, especially in the first few years. The difference comes out of your pocket unless you have GAP coverage."

Customers can't make informed decisions if they don't understand how insurance settlements work.

High-Penetration Selling Strategy - Making It Automatic

The secret to 70%+ GAP penetration? Make GAP the default, not the exception. Your menu design, and presentation positioning all work toward this goal.

"Do You Want Coverage or Waive Coverage?" Approach

Don't ask "Would you like GAP insurance?" This frames GAP as optional add-on. Instead:

"GAP coverage is included in your protection package at $8 per month. This protects you from owing money on a totaled vehicle. Do you want to keep this coverage or waive it?"

You're not selling GAP. You're asking if they want to remove included protection. Penetration skyrockets with this simple language shift.

Negative Equity Customer (100% Penetration Goal)

If your customer has negative equity from their trade-in, GAP should be non-negotiable in your mind. Don't make it optional.

"You have $4,000 of negative equity we're rolling into this loan. That means you start underwater and stay underwater for 2-3 years. GAP coverage isn't optional in this situation, it's essential protection. We're including it automatically."

Then don't discuss removing it unless the customer explicitly objects. Treat it as required coverage for their situation.

Payment Impact Messaging ($5-15/Month)

GAP pricing typically adds $500-$900 to amount financed. On a 72-month loan, that's $7-$13 per month. Always position GAP in monthly terms, not total cost.

"GAP coverage adds $9 per month to your payment. That $9 protects you from potentially owing $8,000-$12,000 if total loss occurs. The math strongly favors having this coverage."

The monthly cost is trivial. The exposure is massive. Make that contrast crystal clear.

Lender Requirement Positioning (Where Applicable)

Some lenders require GAP on high LTV loans or extended terms. When this applies, use it to your advantage:

"Your lender requires GAP coverage on loans over 110% loan-to-value. They understand the risk exposure and won't fund the loan without this protection. That's built into your contract."

Lender requirement eliminates negotiation entirely.

Value Positioning Techniques - Payment Protection Framing

How you frame GAP determines penetration rates. Shift from "optional product" to "essential protection."

"Insurance for Your Insurance" Concept

Your customers have auto insurance. They understand its necessity. Position GAP as insurance for their insurance:

"Your auto insurance covers vehicle damage. GAP insurance covers the gap between insurance payment and loan payoff. It's insurance for your insurance, making sure a total loss doesn't leave you paying for a vehicle you no longer own."

This framing leverages existing insurance acceptance to position GAP as equally necessary.

$5,000-10,000 Potential Exposure Examples

Use specific numbers. "You could owe money" is abstract. "$7,500 out of pocket" is concrete.

"Let me show you the exposure we're protecting against. Purchase price: $32,000. Current value: $26,000. Loan balance: $33,000. If totaled today, insurance pays $26,000. You owe $33,000. That's $7,000 you'd have to pay without GAP coverage. This $9 per month eliminates that $7,000 exposure."

Math sells GAP better than fear.

Continuing Payment After Total Loss Nightmare Scenario

The worst-case scenario resonates powerfully:

"Here's the nightmare situation GAP prevents: Your vehicle gets totaled. Insurance pays $24,000. You owe $31,000. That $7,000 difference is your responsibility. You're still making payments on a vehicle sitting in a salvage yard. No car, but still paying. For $9 per month, GAP eliminates that scenario entirely."

Customers can visualize making payments on a totaled vehicle. It's an easy decision from there.

Protecting Down Payment and Trade Equity Investment

If customers put significant cash down or have positive trade equity, frame GAP as protecting that investment:

"You're putting $5,000 down. Smart move, that builds equity immediately. But you won't have positive equity for another 12-18 months due to depreciation. GAP protects your $5,000 investment during that period. If total loss occurs, you don't lose that down payment."

This reframes GAP from "owing money" protection to "investment protection."

Customer Profiling - Who Needs GAP Most

While GAP makes sense for most financed buyers, certain profiles represent essential coverage candidates.

Negative Equity Trades (Essential)

Already covered, but worth repeating: negative equity trades need GAP automatically. This should be 100% penetration in your dealership. No exceptions.

Long-Term Financing (60+ Months)

Loans extending beyond 60 months keep customers underwater longer. GAP value increases with loan term.

"You're financing over 72 months. You won't reach positive equity until year four. GAP covers the entire period you're upside down. Given the loan term, this is essential protection."

Low Down Payment or Zero Down

Less down payment means more negative equity. $0 down deals start thousands underwater before depreciation.

"With zero down, you're financing the full amount. That creates immediate negative equity. GAP isn't optional in this situation, it's fundamental protection against starting upside down."

High Depreciation Vehicles (Luxury, Certain Brands)

Some vehicles depreciate faster than others. Luxury brands, electric vehicles, and certain makes lose value rapidly. These amplify GAP necessity.

"This vehicle depreciates about 30% in the first year, that's higher than average. Starting value is $48,000. One year from now, it'll be worth $33,600. You'll still owe $44,000. That's $10,400 of exposure. GAP coverage is particularly important on vehicles with above-average depreciation."

Young Drivers (Higher Accident Risk)

Statistics show younger drivers have higher accident rates. When selling to parents buying for teenage drivers, emphasize this:

"Statistically, drivers under 25 have higher accident rates. That increases total loss probability. GAP coverage provides extra protection given the driver's age and experience level."

This isn't ageism, it's statistical reality. Use it appropriately.

GAP Provider Options - Administrator Comparison

Who provides your GAP coverage affects cost, claims experience, and customer satisfaction.

Lender-Provided GAP (Captive Programs)

Most manufacturer finance arms offer GAP coverage. Ford Credit, GM Financial, Toyota Financial Services, etc. These integrate directly into financing, offer competitive pricing, and provide reliable claims handling. Customer perception runs high because it's backed by the manufacturer name.

Commission is typically lower than dealer-provided GAP, but penetration rates are often higher due to brand trust.

Dealership GAP (Higher Commission)

Aftermarket GAP administrators allow higher dealer gross profit. You might pay $300 dealer cost on coverage retailing for $895. That's $595 gross profit vs. $200-$300 on captive GAP.

Higher profit comes with responsibility. Choose reputable administrators with solid claims reputation. A-rated companies like Zurich, Liberty Mutual, and Assurant handle claims reliably. Unknown or poorly-rated administrators create customer nightmares when claims get denied.

Insurance Company GAP Addendum

Some insurance carriers offer GAP as an addendum to auto insurance policies. State Farm, GEICO, and Progressive provide this option. Cost is typically lower than dealer GAP, but you earn no commission.

When customers mention this option, acknowledge it positively: "That's a good alternative. Compare coverage limits and cost. If it's a better value, take it. I want you protected either way."

This honesty builds trust and often results in customers buying from you anyway.

Coverage Differences and Limitations

Not all GAP is equal. Review these key differences:

- Coverage limit: 125% of ACV vs. 150% vs. unlimited

- Deductible coverage: Some GAP pays insurance deductible, others don't

- Lease vs. retail: Separate lease GAP products exist

- Transfer terms: Can coverage transfer to replacement vehicle?

- Refund policy: Pro-rated refund on early payoff or cancellation?

Compare options and recommend appropriate coverage for each customer's situation.

Pricing and Refund Policies

GAP pricing ranges from $500-$995 retail. Dealer cost runs $200-$400. Shop administrators for best dealer cost while maintaining coverage quality.

Refund policy matters for customer satisfaction. Most GAP provides pro-rated refund based on time or mileage remaining if cancelled or paid off early. Some deduct claims from refund. Explain this clearly during sale.

Common Objections - Overcoming Hesitation

GAP objections are predictable and easily overcome with proper responses.

"I Have Full Coverage Insurance"

This is the most common objection and reflects a fundamental misunderstanding.

"Full coverage insurance covers vehicle damage. It pays actual cash value if totaled. But actual cash value is almost always less than your loan payoff, especially in the first 2-3 years. GAP covers that difference. Your regular insurance and GAP work together, insurance pays vehicle value, GAP pays the remaining loan balance."

Draw it out if necessary. Show ACV at $24,000, payoff at $31,000, gap at $7,000.

"I'll Never Total My Car"

Nobody plans to total their vehicle. That's why it's called an accident.

"You're right, nobody plans to total their car. But statistics show that 1 in 8 vehicles will be involved in a total loss incident during a typical 6-year ownership period. That's about 12% probability. For $9 per month, you're eliminating $8,000 of potential exposure. The math strongly supports having coverage even if probability is low."

Don't argue about whether they'll total the vehicle. Focus on risk mitigation math.

"That's Expensive"

$895 sounds expensive. $12 per month doesn't.

"The total coverage cost is $895 over 72 months. That breaks down to $12.43 per month. Your exposure without coverage can easily run $8,000-$12,000 in the first few years of ownership. $12 per month to eliminate that exposure isn't expensive, it's inexpensive insurance."

Always reframe to monthly cost and compare to exposure amount.

"My Insurance Covers That"

Some customers genuinely believe their auto insurance includes GAP. Don't argue. Verify.

"Let's confirm that. What's your insurance company? Call them right now and specifically ask if your policy includes GAP coverage. If it does, we don't need duplicate coverage. Let's verify before moving forward."

Most of the time, they'll discover they don't have GAP. When they do have it, you've built trust by helping them verify rather than arguing.

Compliance Considerations - Proper Disclosure

GAP sales require careful compliance attention. Violations create legal exposure and customer complaints.

State-Specific Regulations

GAP regulations vary by state. Some states regulate GAP as insurance, requiring insurance licenses to sell. Others classify it as a debt cancellation agreement, regulated differently. Know your state requirements.

Lender GAP vs. Dealer GAP Disclosure

If selling dealer GAP when lender GAP is available, you must disclose this:

"Your lender offers GAP coverage at $. We're offering dealer-provided GAP at $ with the following coverage differences: [explain]. You can choose either option."

Don't hide lender alternatives. Disclosure is required and ethical.

Refund and Cancellation Terms

Provide clear, written explanation of:

- Pro-ration method (time vs. mileage)

- Cancellation fee (if any)

- Claims deduction from refund (if applicable)

- Notice requirements for cancellation

Don't hide cancellation terms. Customer satisfaction depends on transparency.

Duplicate Coverage Prohibition

Never sell GAP to customers who already have it through their lender or insurance company. This violates regulatory requirements and ethical standards.

"Do you have GAP coverage on your current loan or through your auto insurance?" Ask explicitly. If they do, don't duplicate.

Documentation Requirements

Maintain complete documentation:

- GAP disclosure and agreement

- Customer signature acknowledging optional nature

- Coverage terms and refund policy

- Administrator contact information

- Cancellation procedure

Complete documentation protects against disputes and regulatory audits.

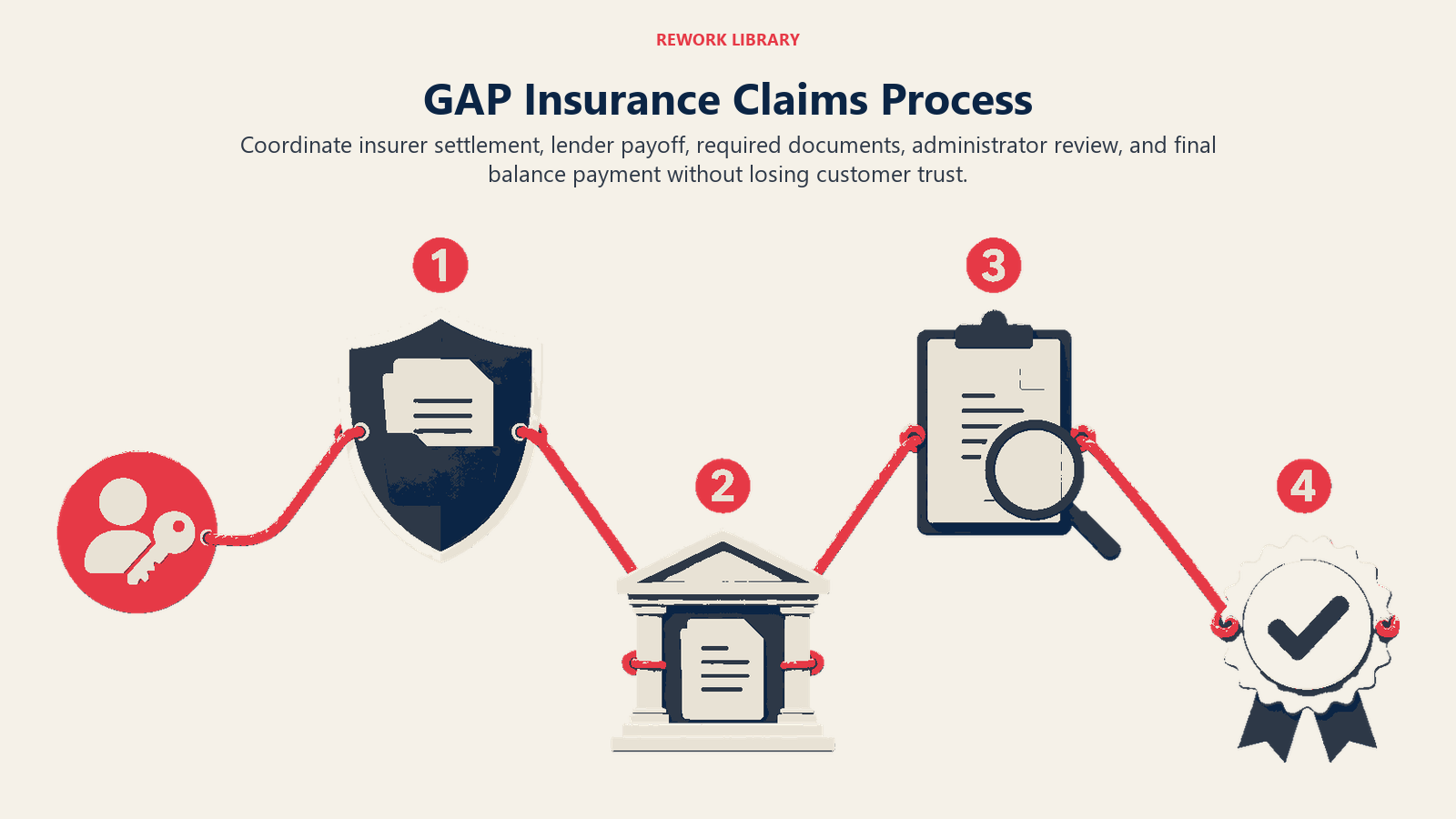

Claims Process - Post-Sale Support

GAP value is proven or destroyed during claim time. Set customers up for success.

Total Loss Scenario Walkthrough

Before customers leave, explain the claim process:

"If your vehicle is totaled, here's what happens: First, file a claim with your auto insurance. They'll determine actual cash value and issue payment. Second, contact GAP administrator at this phone number. Provide insurance settlement details and loan payoff information. GAP administrator pays the difference directly to your lender. You're not out of pocket for any covered gap."

Knowing the process prevents panic during stressful total-loss situations.

Administrator Contact and Claim Filing

Provide administrator phone number, website, and mobile app details. Program the number in their phone before they leave. Include claims contact in the vehicle document packet.

Insurance Settlement Coordination

GAP claims require coordination between insurance company, lender, and GAP administrator. Explain that your dealership or F&I office can assist with this coordination. Provide your contact information for claim support.

"If total loss occurs, call me. I'll help coordinate between your insurance, lender, and GAP administrator to make sure everything processes smoothly."

This offer provides immense comfort and increases perceived value.

Refund Process for Early Payoff/Trade

If customers pay off early or trade in before GAP expires, they're entitled to refund. Explain this clearly:

"If you pay off the loan early or trade in before GAP expires, you'll receive a pro-rated refund based on unused coverage. Contact the administrator to request cancellation and refund. Process typically takes 4-6 weeks."

Knowing refunds are available reduces reluctance to purchase.

Customer Service and Satisfaction

Post-sale GAP support determines whether customers recommend your dealership. When claims arise, be proactive:

- Follow up after total loss to ensure claim filed

- Assist with documentation if needed

- Check claim status with administrator

- Resolve any processing issues

This service approach turns crisis into customer loyalty opportunity.

GAP Sales Implementation Checklist

Pre-Presentation Preparation:

- Verify customer's down payment amount

- Calculate LTV ratio

- Check for negative equity trade

- Note loan term length

- Identify vehicle depreciation profile

Value Positioning (Choose Approach):

- "Insurance for insurance" concept

- Specific exposure amount calculation

- Nightmare scenario prevention

- Down payment protection framing

- Default coverage, opt-out language

Coverage Options Review:

- Lender GAP pricing confirmed

- Dealer GAP pricing confirmed

- Coverage limits compared

- Deductible coverage noted

- Refund policy explained

Essential Disclosure Points:

- Optional nature stated clearly

- Alternative lender GAP disclosed

- Refund/cancellation terms provided

- Duplicate coverage verified absent

- Coverage limits and exclusions explained

Objection Response Prepared:

- "Full coverage insurance" → ACV vs. payoff gap

- "I'll never total" → statistics and risk math

- "That's expensive" → monthly cost vs. exposure

- "Insurance covers that" → offer to verify together

Post-Sale Support:

- Claims process explained

- Administrator contact provided

- Phone number programmed in customer's device

- Offer made to assist with claims if needed

- Refund process explained for early payoff

GAP insurance represents the easiest F&I product to sell at high penetration when positioned correctly. Monthly cost is minimal. Risk exposure is massive. Customer benefit is clear. And nearly every financed customer needs coverage during the first 2-4 years of ownership.

Shift your approach from "selling GAP" to "explaining payment protection." Make coverage the default. Frame removal as waiving protection rather than adding optional coverage. Your penetration rate will climb to 70%+ and customers will thank you when total loss occurs and GAP eliminates thousands in out-of-pocket expense.

That's sustainable F&I profit built on genuine customer protection.

External Resources

- What is GAP Insurance? - Consumer Financial Protection Bureau - Official federal guidance on GAP coverage and consumer rights

- GAP Insurance Consumer Protection - CFPB - Federal regulations on optional product requirements

- CFPB Supervisory Highlights - Auto Finance - Recent enforcement actions and compliance guidance

Senior Implementation Consultant

On this page

- GAP Insurance Fundamentals - What It Covers

- Why GAP Matters - Real-World Scenarios

- High-Penetration Selling Strategy - Making It Automatic

- Value Positioning Techniques - Payment Protection Framing

- Customer Profiling - Who Needs GAP Most

- GAP Provider Options - Administrator Comparison

- Common Objections - Overcoming Hesitation

- Compliance Considerations - Proper Disclosure

- Claims Process - Post-Sale Support

- GAP Sales Implementation Checklist

- External Resources