Agency Model Preparation: How Dealers Can Adapt to Direct Sales Distribution - 2026 Guide

Manufacturers are testing agency models in Europe and watching the results carefully. Mercedes-Benz, Stellantis, and Volvo have moved European operations toward agency relationships where OEMs own inventory, set prices, and pay dealers commissions for facilitation.

Manufacturers are testing agency models in Europe and watching the results carefully. Mercedes-Benz, Stellantis, and Volvo have moved European operations toward agency relationships where OEMs own inventory, set prices, and pay dealers commissions for facilitation.

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

US franchise laws protect dealers today. But laws can change, and some manufacturers are exploring workarounds, especially for EV sales where Tesla's direct-to-consumer model has proven viable through company-owned stores and online sales, bypassing traditional franchised dealers entirely. Understanding agency models now gives dealers time to adapt operations, diversify revenue, and negotiate from positions of strength rather than desperation through proper dealership growth planning.

Understanding the Agency Model

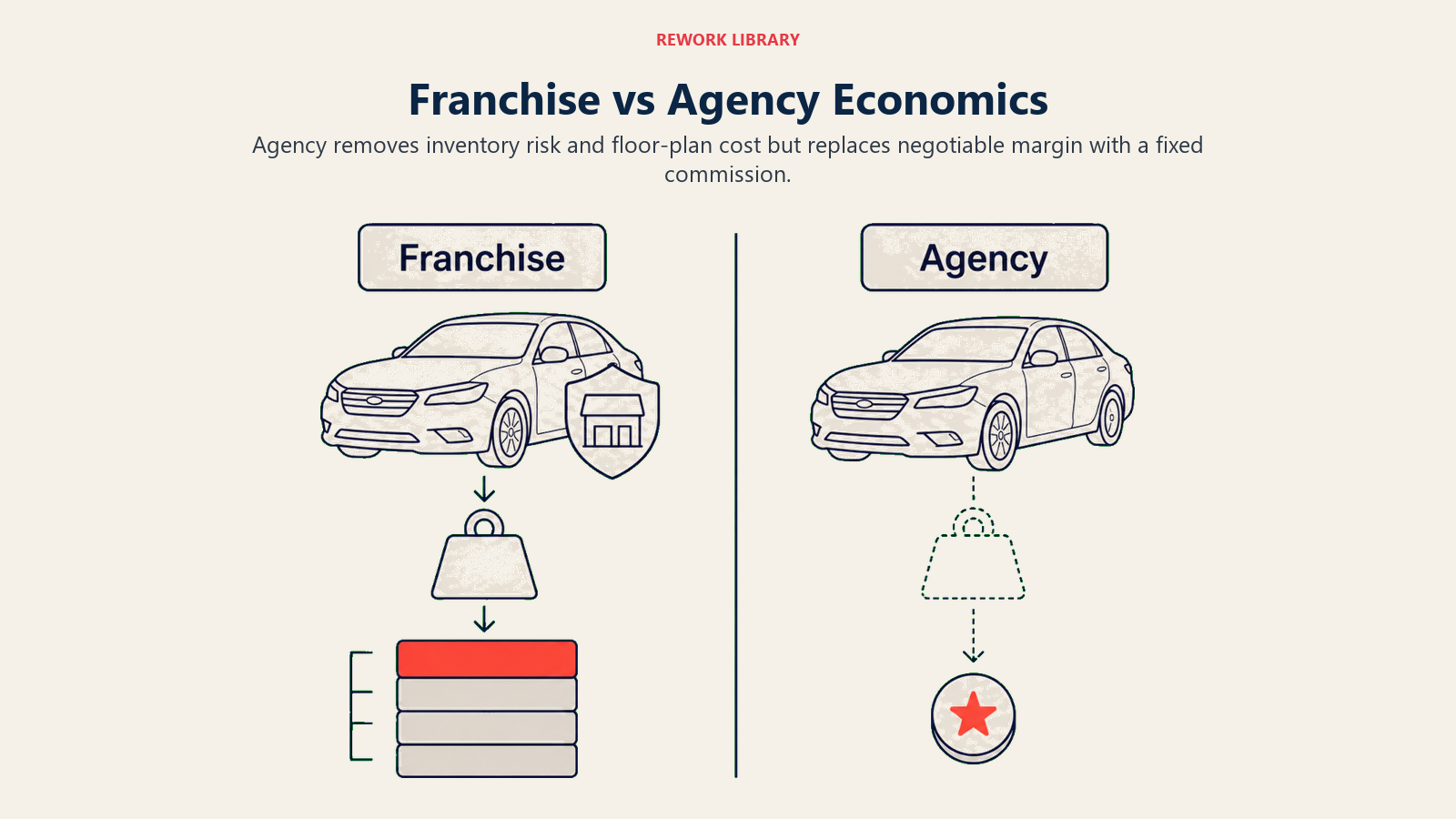

The traditional franchise model has dealers buying inventory from manufacturers, pricing vehicles themselves, negotiating with customers, and keeping the margin between invoice and sale price. Dealers own the vehicles, bear the floor plan costs, and control their own profitability. Under agency models, manufacturers own the inventory sitting on your lot. They set the sale price, no negotiation. You facilitate the transaction and receive a commission, typically 5-8% of the vehicle price. The customer relationship belongs to the manufacturer, who controls pricing, marketing, and often the digital customer experience. This model represents a fundamental shift from the franchised dealer model that has dominated U.S. automotive distribution since the early 20th century, when state franchise laws were established to prevent manufacturers from competing directly with their own dealers.

OEM motivations for agency are clear. They capture more margin currently going to dealers. They control pricing to eliminate the "race to the bottom" discounting that erodes brand value. They own customer data that dealers currently possess. And they create consistent customer experiences across their network.

European implementations show how this works in practice. Mercedes-Benz moved to agency in multiple European markets, targeting 80% of European sales through the agency model by 2025, with dealers receiving commissions around 5-7%. Mercedes handles inventory management and pricing. Dealers focus on customer experience, test drives, and delivery. However, the rollout has faced delays, with Spain's implementation postponed to late 2026, symptomatic of broader challenges with agency adoption across Europe.

US franchise laws currently prevent forced agency transitions. State laws require manufacturers to sell through franchised dealers and prohibit terminations without cause. But these laws aren't permanent. Lobbying continues from both sides. And manufacturers find creative structures, like agency for EVs only or "direct" programs alongside franchise, that test boundaries.

Financial Impact Analysis

Agency changes dealer economics fundamentally. Under traditional franchise, a dealer might generate $3,000-5,000 gross profit on a new vehicle sale through the combination of invoice-to-MSRP margin, holdback, dealer cash, and negotiation. Under agency with 6% commission on a $50,000 vehicle, the dealer receives $3,000, but without inventory risk or floor plan costs.

The comparison isn't straightforward. Traditional model requires substantial working capital for floor plan financing. Agency eliminates that capital requirement. Traditional model allows skilled negotiators to maximize margin. Agency standardizes income regardless of sales skill.

Impact on floor plan and inventory financing is significant. Dealers currently carry millions in floor plan debt. Under agency, that liability shifts to manufacturers. Your balance sheet improves, but so does everyone else's, no competitive advantage.

F&I revenue implications under agency remain uncertain. Some agency models let dealers retain F&I income. Others have manufacturers capturing that revenue too. This is a critical negotiating point. F&I often generates more profit than vehicle sales. Losing it would devastate dealer economics.

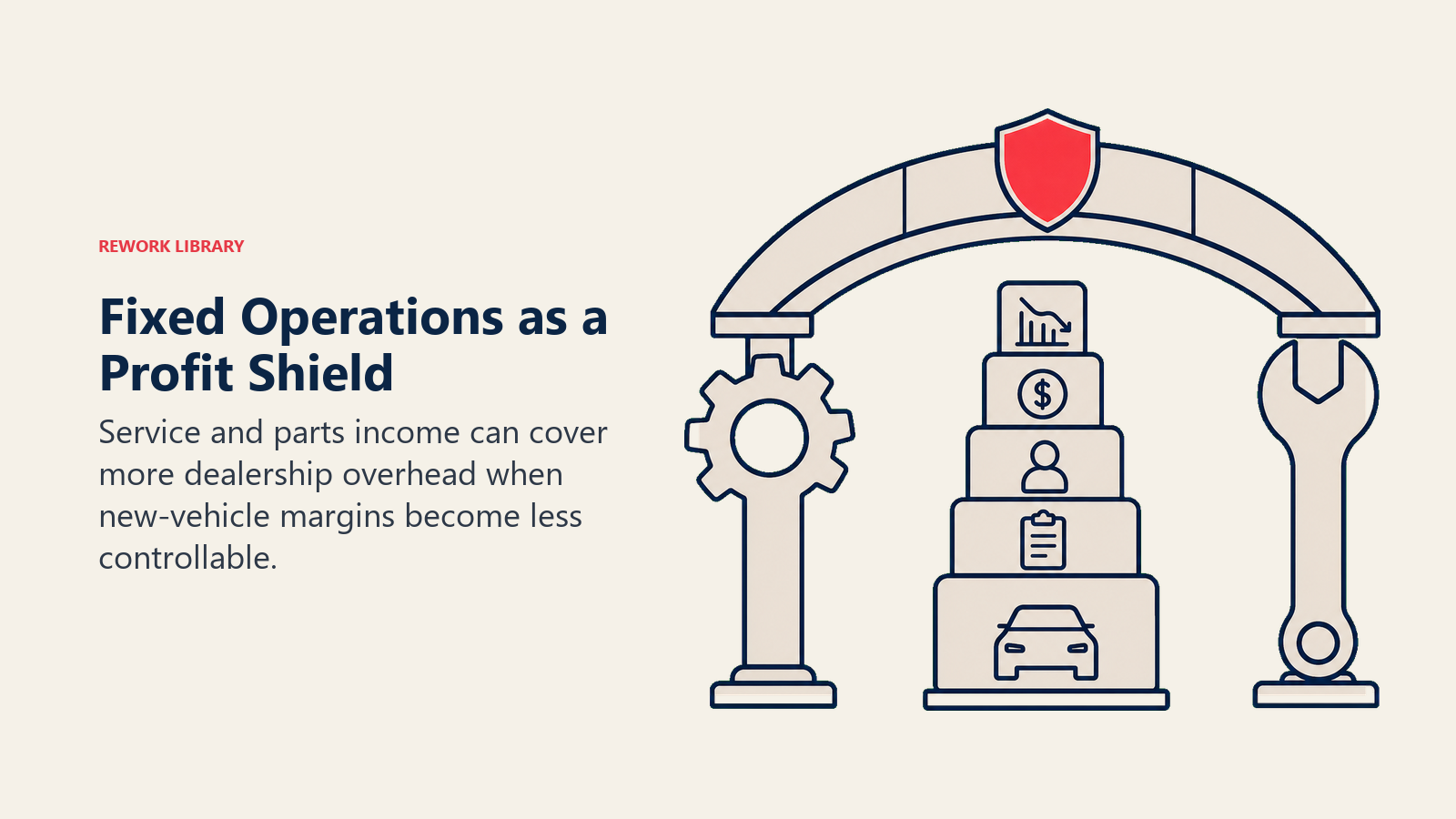

Service and parts revenue should remain unchanged under most agency proposals. Fixed operations stay with dealers because manufacturers lack service infrastructure. This makes your service department even more valuable as a profit center that's protected from agency transitions.

Working capital requirements decrease under agency. Less inventory financing means less capital tied up in floor plan. But commission-based income is also less controllable than margin-based income. Plan cash flow carefully during transitions.

Operational Changes Under Agency

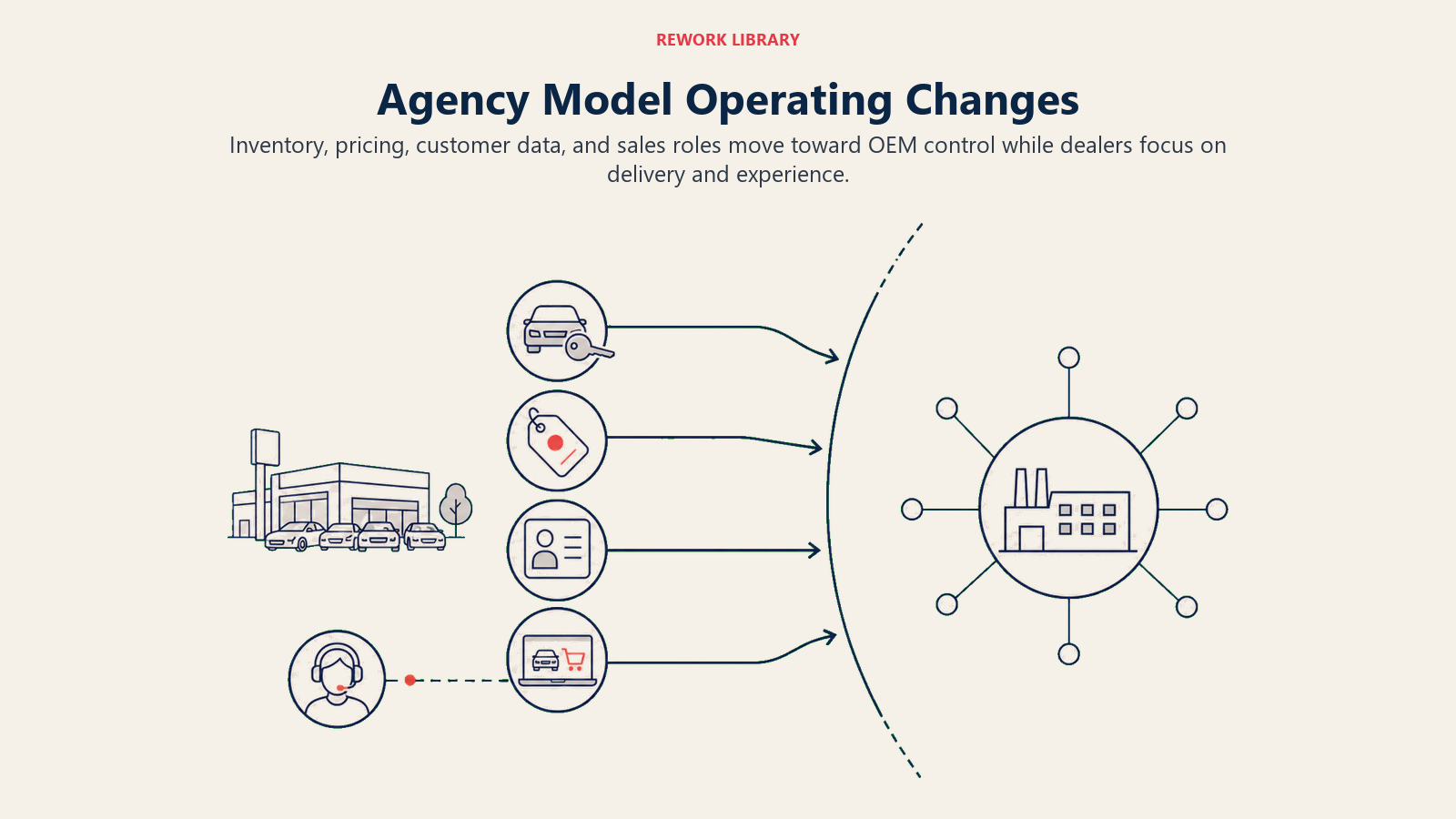

Daily operations look different under agency models. Inventory ownership and management shift to manufacturers. You'll display their vehicles, maintain them, and arrange delivery, but you won't buy them, price them, or bear depreciation risk. This simplifies inventory management but reduces control.

Pricing and negotiation disappear under true agency. The price is the price. Some dealers see this as liberating, no more adversarial haggling. Others see it as removing the skill that differentiated top performers. Either way, the sales conversation changes fundamentally.

Sales process simplification follows from fixed pricing. Without negotiation, the sales process focuses on product selection, test drives, financing options, and delivery experience. Transactions take less time. Customer satisfaction often increases because there's no "did I get a good deal?" anxiety.

Customer relationship ownership questions need resolution. Under agency, who "owns" the customer, the dealer who delivered the vehicle or the manufacturer who controls the data? This affects conquest opportunities, loyalty marketing, and long-term customer value.

Compensation structure adjustments become necessary. Commission-only salespeople might thrive under flat-rate compensation tied to unit volume. Negotiation-focused closers might struggle without opportunities to demonstrate skill. Plan for team changes.

Preparing Your Sales Operation

Adapting your team starts before any agency transition. Sales roles shift from negotiators to product specialists. Under agency, salespeople don't need closing skills, they need product knowledge, customer service orientation, and experience facilitation abilities. Hire and train for these different sales competencies.

Customer experience focus overtakes closing skills in importance. When price is fixed, customers choose dealers based on convenience, professionalism, and service quality. Every interaction matters more when you can't "save" a deal with a discount.

Staffing levels may decrease under agency. Faster transactions mean fewer salespeople needed. But customer experience focus might mean investing in concierge-style roles. Model your ideal staffing before changes occur through dealership benchmarking.

Compensation models need redesign. Fixed-price selling might support salary-plus-volume-bonus structures rather than traditional commission splits. Test new compensation approaches before they're forced by model changes.

Training shifts toward consultative selling. Instead of overcoming objections and closing, train on needs discovery, product matching, and experience delivery. The skills aren't completely different, but the emphasis changes.

Performance metrics under agency emphasize customer satisfaction, delivery quality, and conversion rate rather than gross profit. Measure what matters in the new model.

Maximizing Fixed Operations

Your service department becomes your most protected profit center. Service absorption becomes even more critical if agency reduces variable operations profitability. Target 80%+ absorption, where service and parts gross profit covers total dealership fixed expenses. That's challenging but achievable with focused effort.

Parts and accessories revenue growth strategies include online parts sales, accessories sales at delivery, wholesale parts operations, and fleet service contracts. Every additional dollar of fixed operations profit reduces dependence on variable.

Customer retention in a direct-sales world depends on service relationships. Even if manufacturers own the sales relationship, customers come to you for service. Excellent service creates loyalty that transcends model changes.

Service marketing and conquest opportunities exist regardless of sales model. Customers with older vehicles need service. Competitors' customers need alternatives. Market your service department aggressively to capture fixed ops revenue from every possible source.

Technology and efficiency investments in service improve profitability and capacity. Multi-point inspection tools, service scheduling optimization, and tech compensation structures all impact fixed ops performance.

Customer Experience Excellence

Under agency, customer experience becomes your primary competitive advantage. When price is fixed, customers choose dealers based on experience. Who made buying easy? Who provided excellent service? Who remembered their preferences? These soft factors become hard differentiators in the customer experience.

Differentiate when price is fixed through convenience, amenities, expertise, and relationships. Covered delivery bays. Comfortable lounges. Knowledgeable staff. Personal follow-up. These investments pay returns when price isn't a lever.

Build loyalty that survives model changes by earning it through service, not discounts. Customers who chose you for price will leave for better prices. Customers who chose you for experience stay even when prices equalize.

Digital experience and convenience services, online scheduling, pickup and delivery, mobile service, transparent communication, matter more when transaction experiences standardize. Invest in digital tools that improve customer convenience.

Community presence and local market knowledge differentiate you from distant online transactions. You're the dealer who sponsors local teams, employs local workers, and understands local needs. That matters to many customers, even in an agency world.

Diversification Strategies

Reducing OEM dependence protects you from model changes you can't control. Used vehicle operations expansion reduces reliance on new car commissions. Dealers control used car sourcing, pricing, and margins regardless of OEM relationships. Strengthen your used car operation now as insurance against new car margin compression.

Multi-franchise considerations spread risk across multiple OEM relationships. If one manufacturer moves to agency with unfavorable terms, others might maintain traditional models. Franchise diversification provides options.

Non-automotive revenue opportunities exist for dealers with real estate, facilities, and customer relationships. Detail shops, accessory installations, body shops, and car washes generate income independent of new car sales. Some dealers add tire stores, quick-lube operations, or collision centers.

Service contract and aftermarket expansion builds recurring revenue. Extended warranties, maintenance packages, and appearance protection generate income over years. These products often survive agency transitions because manufacturers focus on vehicle sales rather than aftermarket.

Real estate and facility optimization matters when income models change. Is your location worth more as a dealership or as something else? Could you sublease unused space? Understanding your real estate's value provides options.

Negotiating with OEMs

When agency discussions happen, preparation determines outcomes.

Understand OEM objectives before negotiations start. Manufacturers want margin capture, pricing control, and customer data. Understanding their goals helps you identify where you have leverage and where you don't.

Commission rate negotiation requires market data. What are dealers receiving in European agency markets? What commission covers your costs plus reasonable profit? Build financial models that demonstrate minimum viable commission rates.

Territory and customer allocation discussions determine who gets credit for sales. If a customer researches online, visits your showroom, then buys from another dealer's delivery point, who earns the commission? Define these rules clearly.

Investment protection and facility requirements need attention. If you invested $10 million in a manufacturer-required facility, agency transitions shouldn't strand that investment. Negotiate facility requirements reductions or investment recoupment.

Dealer association and collective bargaining provide strength in numbers. Individual dealers have limited leverage. Dealer associations representing hundreds of points have more. Engage with your state and national associations on agency issues.

Scenario Planning

Prepare for multiple possible futures, not just one. Full agency implementation would have manufacturers owning all inventory and setting all prices. You'd earn commissions, focus on experience, and maximize fixed operations. This is the European model some manufacturers are pursuing.

Hybrid models might have agency for online sales and traditional franchise for in-store sales. Or agency for new vehicles and traditional for used. Or agency for EVs and traditional for internal combustion. These hybrid approaches are likely transition states.

EV-only agency with ICE traditional is one plausible scenario. Manufacturers might use agency for EV sales (where Tesla set expectations) while maintaining franchise for traditional vehicles. This creates operational complexity but might be politically feasible.

Status quo continuation is possible. Franchise laws might hold. Dealer opposition might succeed. European agency experiments might fail. Don't bet everything on agency happening, prepare for it while maintaining current capabilities.

Timeline considerations matter for planning. Full agency transitions take years. European implementations happened over 2-3 year periods. You have time to prepare, but not unlimited time. Start now rather than scrambling later.

The agency model isn't inevitable, but it's possible. Dealers who prepare, diversifying revenue, strengthening fixed operations, building experience capabilities, and understanding their options, will thrive regardless of how distribution models evolve. Those who assume the status quo continues forever may find themselves unprepared for changes they should have seen coming.