F&I Compliance Best Practices - Legal Protection & Regulatory Excellence

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

The average F&I compliance lawsuit settles for $50,000-$500,000. Major violations? Try $2-5 million in class-action settlements. And that's before calculating reputation damage, lost customer trust, and future business impact. One discriminatory rate markup case or improper product disclosure can destroy decades of dealership reputation overnight.

Here's the reality: F&I compliance isn't optional. It's not bureaucratic overhead. It's fundamental business protection. Federal regulations from ECOA, FCRA, TILA, and GLBA create baseline requirements. State regulations add layers of specific disclosure rules, licensing requirements, and rate limitations. Lender and manufacturer audits enforce contract standards. And customer complaints trigger regulatory investigations that can snowball into costly legal battles.

But compliance doesn't have to kill profitability. The best FF&I operationsI operations achieve high PVR while maintaining perfect compliance records. The difference? Systematic processes, comprehensive training, rigorous documentation, and cultural commitment from dealer principal through F&I staff.

This guide provides the complete compliance framework covering federal law, state requirements, menu presentation, rate practices, product sale procedures, documentation standards, training protocols, and audit preparedness.

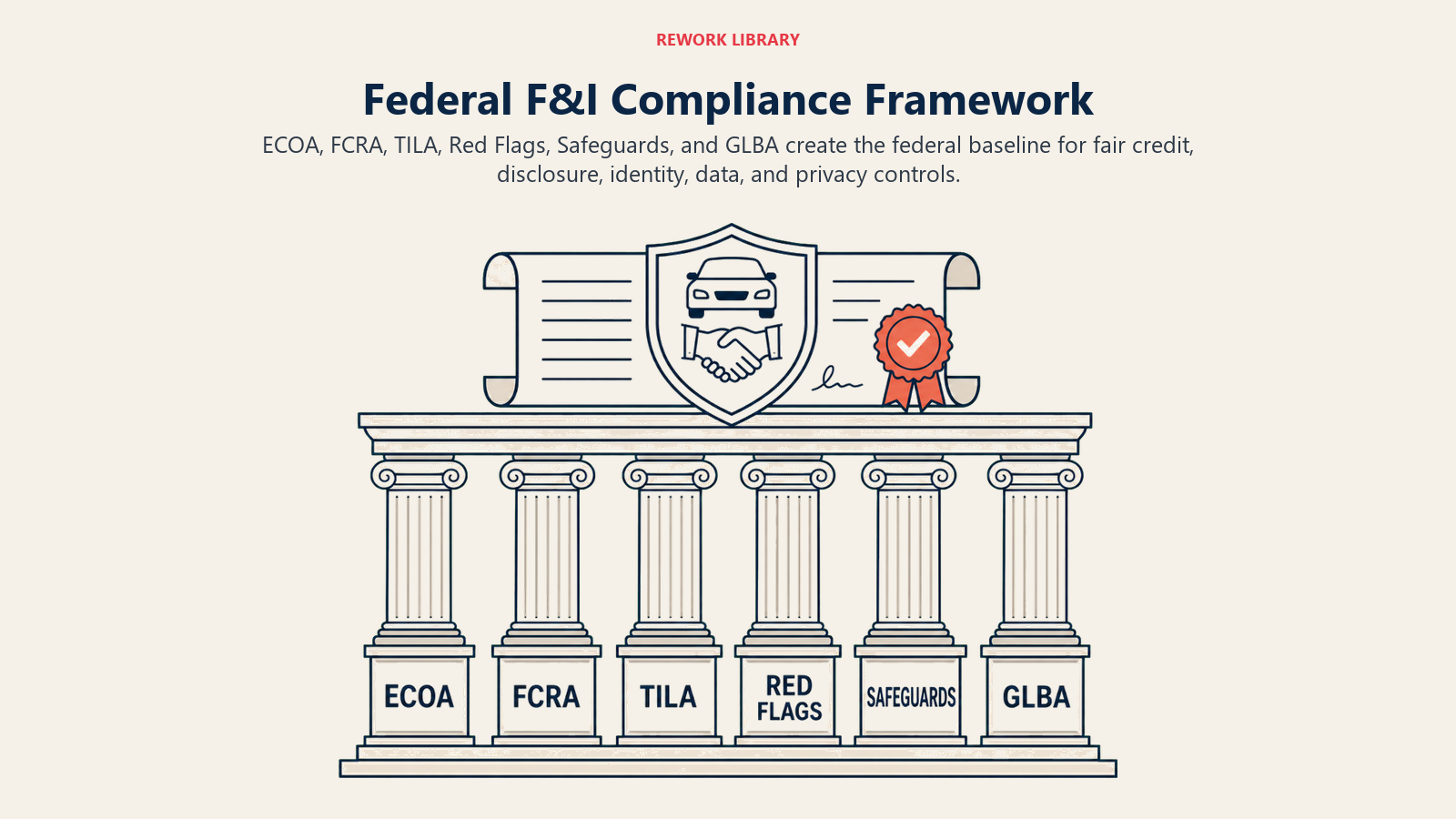

Federal Compliance Framework - Core Regulations

Federal law creates baseline F&I compliance requirements that apply in every state. Violations trigger federal agency action, lawsuits, and serious penalties.

Equal Credit Opportunity Act (ECOA) - Discrimination Prevention:

ECOA prohibits credit discrimination based on protected classes: race, color, religion, national origin, sex, marital status, age, or receipt of public assistance.

F&I implications:

- Rate markups must be consistent and non-discriminatory

- Credit decisions can't consider protected characteristics

- Dealer reserve practices must avoid disparate impact

- Documentation must justify all rate variations

Disparate impact matters even without discriminatory intent. If your rate markup practices result in higher rates for protected classes (even unintentionally), you've violated ECOA. Monitor rate data by demographics to identify problematic patterns.

Fair Credit Reporting Act (FCRA) - Credit Pull and Adverse Action:

FCRA regulates consumer credit reporting and requires specific disclosures when credit information affects customer outcomes.

F&I requirements:

- Obtain written authorization before pulling credit

- Provide adverse action notices if credit application is declined

- Disclose credit score used in financing decision

- Notify consumers if less-favorable terms are offered based on credit

- Dispose of credit information securely

Adverse action notice must include: specific reason for action, credit score used, credit bureau contact information, and consumer rights statement. This isn't optional, it's federal requirement triggering penalties for non-compliance.

Truth in Lending Act (TILA) - Disclosure Requirements:

TILA requires clear disclosure of credit terms before consumers commit to financing.

Required disclosures:

- Annual percentage rate (APR)

- Finance charge (total interest paid)

- Amount financed

- Total of payments

- Payment schedule

Federal credit disclosures must be clear, conspicuous, and provided before contract signing. Don't rush customers through these forms. Federal law gives consumers specific cancellation rights if disclosure requirements aren't met.

Red Flags Rule - Identity Theft Prevention:

Red Flags Rule requires dealers to implement identity theft prevention programs identifying, detecting, and responding to warning signs (red flags) of identity theft.

F&I implementation:

- Verify identification documents (driver's license, etc.)

- Confirm application information matches credit report

- Watch for inconsistent personal information

- Flag suspicious activity (multiple recent credit inquiries, fraud alerts)

- Respond to red flags by requiring additional verification

Document your red flags program and train staff on implementation. Regulatory audits verify compliance.

Safeguards Rule - Customer Data Protection:

Safeguards Rule requires protection of customer information through administrative, technical, and physical security measures.

F&I responsibilities:

- Secure storage of credit applications and contracts

- Restricted access to customer financial information

- Encrypted digital data transmission

- Secure document disposal (shredding)

- Regular security assessments

Data breaches create massive liability. Implement proper security protocols.

Gramm-Leach-Bliley Act (GLBA) - Privacy Notices:

GLBA requires privacy notices explaining how customer information is collected, used, and shared.

Provide privacy notice at loan origination, annually thereafter, and before sharing information with non-affiliated third parties. Notice must explain customer's right to opt-out of information sharing.

Most dealers use standardized privacy notices. Don't skip providing them, federal requirement applies to every transaction.

State-Specific Regulations - Varying Requirements

State regulations create a compliance patchwork. Requirements in California differ from Texas differ from New York. Multi-state dealer groups face complex compliance management.

F&I Licensing Requirements by State:

Some states require F&I managers to hold specific licenses:

- Insurance licenses: Required in states classifying F&I products as insurance

- Finance licenses: Required in states regulating F&I as finance activity

- Product-specific licenses: Some states require separate licensing for VSC, GAP, etc.

Verify your state requirements. Operating without required licenses creates massive compliance exposure. License requirements often include pre-licensing education, testing, and continuing education.

Rate and Reserve Limitations (Rate Caps):

Some states cap dealer participation (reserve/markup) on finance contracts:

- California: No caps, but robust anti-discrimination enforcement

- New York: 2.5% maximum markup over buy rate

- Pennsylvania: 3% maximum markup

- Other states: Various caps or no caps

Understand your state's rate limitations. Exceeding caps violates state law regardless of lender agreement.

Product Disclosure Requirements:

State law dictates specific F&I product disclosure requirements:

- VSC disclosure: "This is not insurance" statement required in most states

- GAP disclosure: Some states require specific language explaining coverage

- Cancellation terms: Most states mandate clear cancellation disclosure

- Optional nature: Products must be clearly disclosed as optional

Use state-approved forms and disclosure language. Don't improvise product disclosures.

Cooling-Off Periods and Cancellation Rights:

Some states provide consumers right to cancel contracts within specified timeframes:

- California: No general right, but spot delivery rules apply

- Florida: 3-day cooling-off period for certain transactions

- Other states: Variable requirements

Understand cancellation rights in your state. Failure to honor statutory cancellation creates liability.

Documentation and Record Retention:

State law (and federal lending regulations) require maintaining transaction documents:

- Minimum retention: 7 years for most records

- Longer retention: Some states require 10+ years

- Accessible format: Records must be retrievable for audits

Store documents securely with organized filing system. When audits come (and they will), you must produce complete documentation quickly.

Menu Compliance - Presentation Requirements

F&I menu presentation faces strict regulatory scrutiny. Regulators view menus as critical disclosure tools. Improper menu design creates compliance violations and lawsuit vulnerability.

Full Product Disclosure:

Your menu must disclose:

- Product name and coverage description

- Coverage term and limitations

- Retail price for each product

- Administrator or provider name

- Cancellation and refund terms reference

Don't use vague descriptions like "protection plan." Specify "vehicle service contract covering mechanical breakdown for 5 years/60,000 miles."

Cash Price Disclosure:

TILA requires clear cash price disclosure. Your menu must show cash price option prominently, not buried in fine print.

Present payment options at various financing terms AND cash purchase option. Failure to show cash pricing clearly violates federal disclosure requirements.

Optional Product Clear Indication:

Every F&I product must be clearly disclosed as optional. Use explicit language:

- "The following products are optional and not required to obtain financing."

- "You may purchase any of these products separately or decline all coverage."

Ambiguous presentation suggesting products are required violates consumer protection laws.

Payment Impact Transparency:

Show clear payment impact for each product or package:

- Base payment without products

- Payment with each product added

- Total payment with selected package

Don't hide payment increases or present only "fully loaded" payment. Transparency is required and prevents complaints.

Multiple Payment Options Presentation:

Display financing options at various terms (48, 60, 72 months, etc.). This demonstrates you're not steering customers toward specific financing structure to maximize dealer profit.

Regulators view single-term presentation as potentially deceptive practice designed to hide financing cost.

Menu Template Approval Process:

Don't create custom menus without legal review. Use approved templates from:

- Menu software providers (who consult compliance attorneys)

- Legal counsel specializing in automotive retail

- Industry compliance consultants

Update menus when regulations change. Out-of-date menus create compliance liability even if they were compliant when designed.

Rate and Reserve Compliance - Avoiding Rate Discrimination

Dealer reserve (rate markup) creates the highest compliance risk in FF&I operationsI operations. Discriminatory rate practices trigger ECOA violations, federal consent orders, and million-dollar settlements.

Objective Credit Scoring Application:

Use objective credit scoring criteria for rate decisions. Document your rate structure:

- Tier 1 credit (720+ score): buy rate to buy rate + 1%

- Tier 2 credit (680-719): buy rate + 1% to + 2%

- Tier 3 credit (640-679): buy rate + 2% to + 3%

- Below 640: case-by-case evaluation

Objective criteria defend against discrimination claims. "I gave them that rate because they seemed flaky" won't fly. "I gave them that rate based on credit tier and loan term per our written policy" creates defensible position.

Rate Markup Consistency and Policy:

Document your rate markup policy in writing. Include:

- Maximum markup by credit tier

- Approval requirements for markups exceeding normal range

- Manager oversight of rate decisions

- Justification documentation for rate variations

Consistency matters. If one customer gets 1% markup on 720 credit score while another gets 2.5% markup on 720 score, you need documented justification for the difference.

Disparate Impact Monitoring:

ECOA violations occur even without discriminatory intent. If your rate practices result in higher average rates for protected classes, you've created disparate impact.

Monitor rate data:

- Average rate by credit tier

- Average markup by demographics (where legally collectible)

- Rate distribution across customer profiles

If data shows disparate impact, adjust practices immediately. Federal agencies use statistical analysis to identify problematic patterns.

Reserve Documentation and Justification:

Document justification for all rate markups:

- Credit tier supporting rate decision

- Loan term affecting markup

- Special circumstances (if any)

- Manager approval for above-standard markups

Documentation protects against discrimination claims and demonstrates consistent application of objective criteria.

Rate Disclosure to Customer (State-Dependent):

Some states require rate disclosure showing buy rate vs. contract rate. Others don't. Know your state requirement.

When disclosure is required, don't fight it. Explain dealer participation clearly: "Your approved buy rate is 6.5%. We're offering 7.5%. The difference represents dealer participation and covers transaction processing costs."

Transparency builds trust. Hiding rate structure invites suspicion and complaints.

Product Sale Compliance - Proper Procedures

F&I product sales face specific compliance requirements. Improper procedures trigger consumer complaints, regulatory action, and lawsuit vulnerability.

Voluntary Purchase Confirmation:

Products must be voluntary. Obtain clear confirmation:

- "I understand these products are optional and not required to obtain financing."

- Signature acknowledging voluntary purchase

Don't use language suggesting products are required, strongly recommended by lender, or necessary for approval. Optional means optional.

Coverage Terms Clear Explanation:

Explain product coverage clearly before purchase:

- What's covered and what's excluded

- Coverage term and mileage limitations

- Deductible requirements (if any)

- Claim process and administrator contact

"Sign here" without explanation violates ethical standards and invites complaints that customers didn't understand what they purchased.

Cancellation and Refund Disclosure:

Provide written disclosure of cancellation terms:

- Cancellation notice requirements

- Refund calculation method (pro-rated, flat, etc.)

- Claims impact on refund amount

- Administrator contact for cancellation

Some customers will cancel. Make the process clear upfront to avoid complaints about "hidden" cancellation restrictions.

Duplicate Coverage Prohibition:

Never sell coverage duplicating existing protection:

- Don't sell GAP if customer already has it through lender or insurance

- Don't sell maintenance plan duplicating manufacturer coverage

- Don't sell VSC overlapping with remaining factory warranty (unless disclosed as extension)

Ask explicitly: "Do you currently have GAP coverage through your insurance or existing loan?" If yes, don't sell duplicate.

Product-Specific State Regulations:

VSC, GAP, and other products face state-specific requirements:

- Some states regulate VSC as insurance (requiring insurance licenses)

- Some states require specific GAP disclosures

- Some states mandate particular cancellation terms

Use state-compliant forms and disclosures for each product. National templates may not satisfy state requirements.

Documentation Best Practices - Protection Through Paperwork

Complete, accurate documentation protects against disputes, lawsuits, and regulatory actions. Incomplete documentation destroys defensibility in legal proceedings.

Complete Buyer's Order:

Buyer's order is your master transaction document. Must include:

- Complete vehicle description and VIN

- Accurate pricing (vehicle, fees, taxes, products)

- Trade-in allowance and payoff

- Down payment and payment method

- Customer and co-buyer information

- Signatures acknowledging accuracy

Incomplete buyers orders create contract disputes and unwinding liability.

All Required Signatures Obtained:

Every document requires proper signatures:

- Buyer and co-buyer (where applicable)

- Guarantor signatures (if used)

- F&I manager counter-signature (where required)

- Date all signatures

Missing signatures void agreements or create enforceability issues. Check every signature line before customer leaves.

Legible and Accurate Information:

Documents must be legible. Illegible contracts create disputes about terms. Ensure:

- Typed information whenever possible

- Clear handwriting if manual entry required

- No cross-outs or white-out (void and reprint instead)

- Accurate information (verify VIN, customer name, amounts)

Sloppy documentation creates problems during audits and disputes.

Proper Form Sequencing:

Present documents in logical sequence:

- Credit application and privacy notice first

- Financing disclosures before contract signing

- Contract and security agreement

- Product agreements after contract

- Final delivery checklist

Proper sequencing demonstrates compliance with disclosure timing requirements and improves customer understanding.

Electronic Signature Compliance:

Electronic signatures (e-signatures) are legally binding under ESIGN Act when properly implemented:

- Customer must consent to electronic process

- Identity authentication required

- Electronic records must be retainable

- Provide paper copies if requested

Use reputable e-signature platforms designed for automotive retail. Don't improvise electronic signing processes.

Document Retention Policy (7+ Years):

Implement systematic retention:

- 7 years minimum for all transaction documents

- 10+ years in states requiring longer retention

- Organized filing system (physical or digital)

- Backup for digital records

- Secure destruction after retention period expires

When audits or lawsuits emerge years later, complete documentation protects you. Missing documents destroy defensibility.

Training and Certification - Staff Competency

Compliance failures usually stem from inadequate training, not intentional violations. Systematic training prevents problems before they occur.

Initial F&I Training Requirements:

New F&I managers need comprehensive training before handling transactions:

- Federal compliance requirements (ECOA, FCRA, TILA, Red Flags, GLBA)

- State-specific regulations

- Product knowledge and disclosure requirements

- Menu presentation compliance

- Rate and reserve policies

- Documentation procedures

Minimum 40 hours of initial training before independent transaction handling. Use industry training programs (JM&A, Reahard & Associates, NCM, F&I Training Solutions).

Ongoing Compliance Education:

Regulations change. Products change. Staff knowledge must stay current:

- Quarterly compliance updates (regulatory changes)

- Annual comprehensive compliance review

- Product training when new offerings added

- Remedial training when deficiencies identified

Document all training. Regulatory investigations ask: "What training did this employee receive?" If answer is "none since hire 5 years ago," you've demonstrated negligence.

Role-Playing and Scenario Training:

Classroom compliance training isn't enough. Practice real scenarios:

- Handling discrimination complaints

- Responding to credit denials properly

- Explaining product disclosures clearly

- Dealing with challenging customers

- Recognizing red flags of identity theft

Role-playing reveals knowledge gaps before they create real-world problems.

State Certification Maintenance:

If your state requires F&I licensing, maintain certifications:

- Complete continuing education requirements

- Renew licenses before expiration

- Track certification status for all F&I staff

- Budget for licensing and education costs

Lapsed licenses create compliance violations even if employee did nothing else wrong.

Manufacturer Program Training:

Captive finance companies provide training on their programs, requirements, and compliance expectations. Attend manufacturer training:

- Understand specific lender requirements

- Learn about lender audit criteria

- Access lender compliance resources

- Build relationships with lender representatives

Manufacturer audits are easier when you understand their specific requirements upfront.

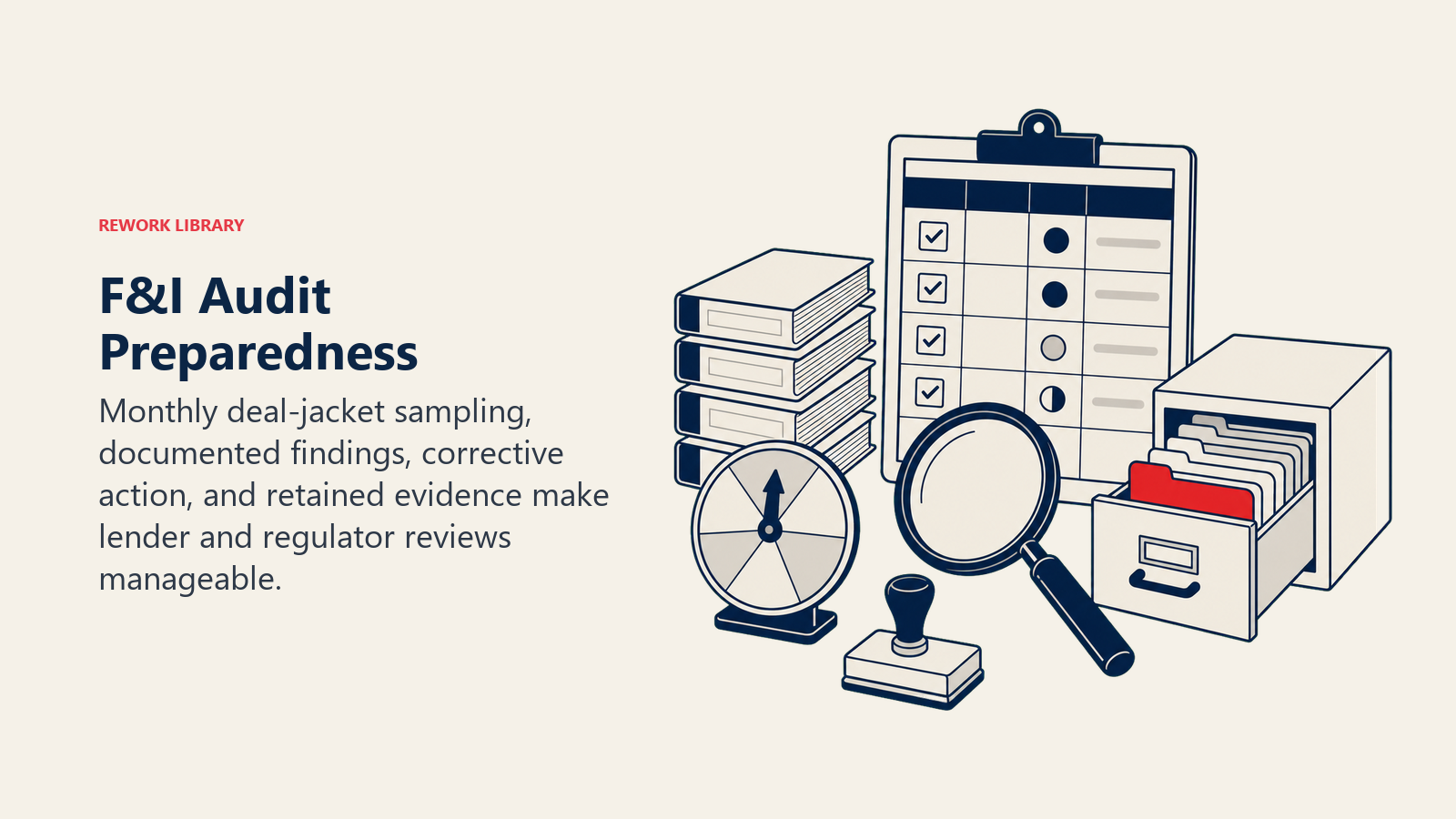

Audit Preparedness - Internal and External Reviews

Audits are inevitable. Lenders audit contracts. Manufacturers audit captive finance deals. State regulators conduct investigations. The question isn't if you'll be audited, but when, and whether you'll pass.

Monthly Deal Jacket Audits:

Don't wait for external audits to find problems. Implement internal monthly audits:

- Randomly select 10-15 deal jackets

- Review for documentation completeness

- Verify signature requirements met

- Check disclosure compliance

- Confirm rate and product pricing accuracy

- Document findings and corrective actions

Monthly audits identify deficiencies early, allowing corrective training before patterns develop.

Compliance Checklist Per Deal:

Create transaction checklists used on every deal:

- Credit application complete and signed

- Privacy notice provided

- Credit authorization obtained

- Adverse action notice provided (if applicable)

- Federal credit disclosures complete

- Contract terms match disclosures

- Product disclosures provided

- All product agreements signed

- Cancellation terms disclosed

- Copy of documents provided to customer

Physical or digital checklist ensures consistent compliance execution.

Lender Audit Response Procedures:

When lenders audit contracts, respond promptly:

- Provide requested documentation within specified timeframe

- Correct deficiencies identified

- Implement training to prevent recurrence

- Track audit findings over time

Repeated audit deficiencies trigger lender attention and possible termination of financing relationship.

Manufacturer Audits (Captive Finance):

Manufacturer captive finance arms conduct regular dealer audits verifying compliance with their specific programs:

- Program eligibility verification

- Documentation requirements

- Rate and reserve compliance

- Product penetration monitoring

Pass manufacturer audits to maintain access to captive financing (often your best financing source).

State Regulatory Audits:

State regulatory audits are less frequent but more serious. Triggered by:

- Consumer complaints

- Random selection

- Industry sweep examinations

- Regulatory concern about specific practices

Respond cooperatively. Provide requested information completely. Address findings immediately. Regulatory audits can result in fines, license suspension, or enforcement actions.

Common Audit Findings and Prevention:

Most audit findings fall into predictable categories:

- Missing signatures (prevention: checklist per deal)

- Incomplete disclosures (prevention: use approved forms)

- Inconsistent rate markups (prevention: written policy and oversight)

- Product documentation gaps (prevention: product-specific checklist)

- Record retention failures (prevention: systematic filing and retention)

Address common problems systematically and audit findings decrease dramatically.

Creating Compliance Culture - Beyond Checkboxes

True compliance isn't about checking boxes. It's about organizational culture where ethical behavior and regulatory adherence are expected, rewarded, and enforced.

Management Commitment to Compliance:

Compliance culture starts with dealer principal and general manager. When leadership treats compliance as bureaucratic annoyance rather than business fundamental, staff follows suit.

Demonstrate commitment:

- Invest in compliance training and resources

- Attend compliance seminars yourself

- Review compliance metrics monthly

- Hold managers accountable for department compliance

- Celebrate strong compliance performance

Staff watches leadership. If GM takes compliance seriously, F&I managers will too.

Consequences for Violations:

Establish clear consequences for compliance violations:

- First offense: remedial training and warning

- Second offense: written reprimand and performance plan

- Third offense: suspension or termination

Don't tolerate repeated violations. One bad F&I manager can create million-dollar liability.

Incentive Structure That Doesn't Encourage Cutting Corners:

F&I compensation structures sometimes encourage violations. If manager gets paid large bonuses for rate reserve but faces no penalty for discrimination complaints, you've incentivized problematic behavior.

Balance incentives:

- Commission for PVR (rewards productivity)

- Compliance bonuses (rewards clean audits)

- Penalties for compliance failures (discourages shortcuts)

- Customer satisfaction metrics (encourages ethical treatment)

Customer Complaint Resolution:

Handle complaints quickly and fairly:

- Designate complaint response person

- Respond to complaints within 48 hours

- Investigate thoroughly

- Resolve fairly (even if costly)

- Document complaint and resolution

One unresolved complaint can spiral into regulatory investigation, lawsuit, or reputation damage. Spend the money to resolve complaints when justified.

Continuous Improvement Mindset:

Compliance isn't static. Regulations change. Court decisions create new interpretations. Industry best practices evolve.

Stay current:

- Subscribe to compliance publications

- Join dealer associations with compliance resources

- Attend annual compliance seminars

- Review and update procedures annually

- Learn from other dealers' mistakes

Continuous improvement prevents compliance failures before they occur.

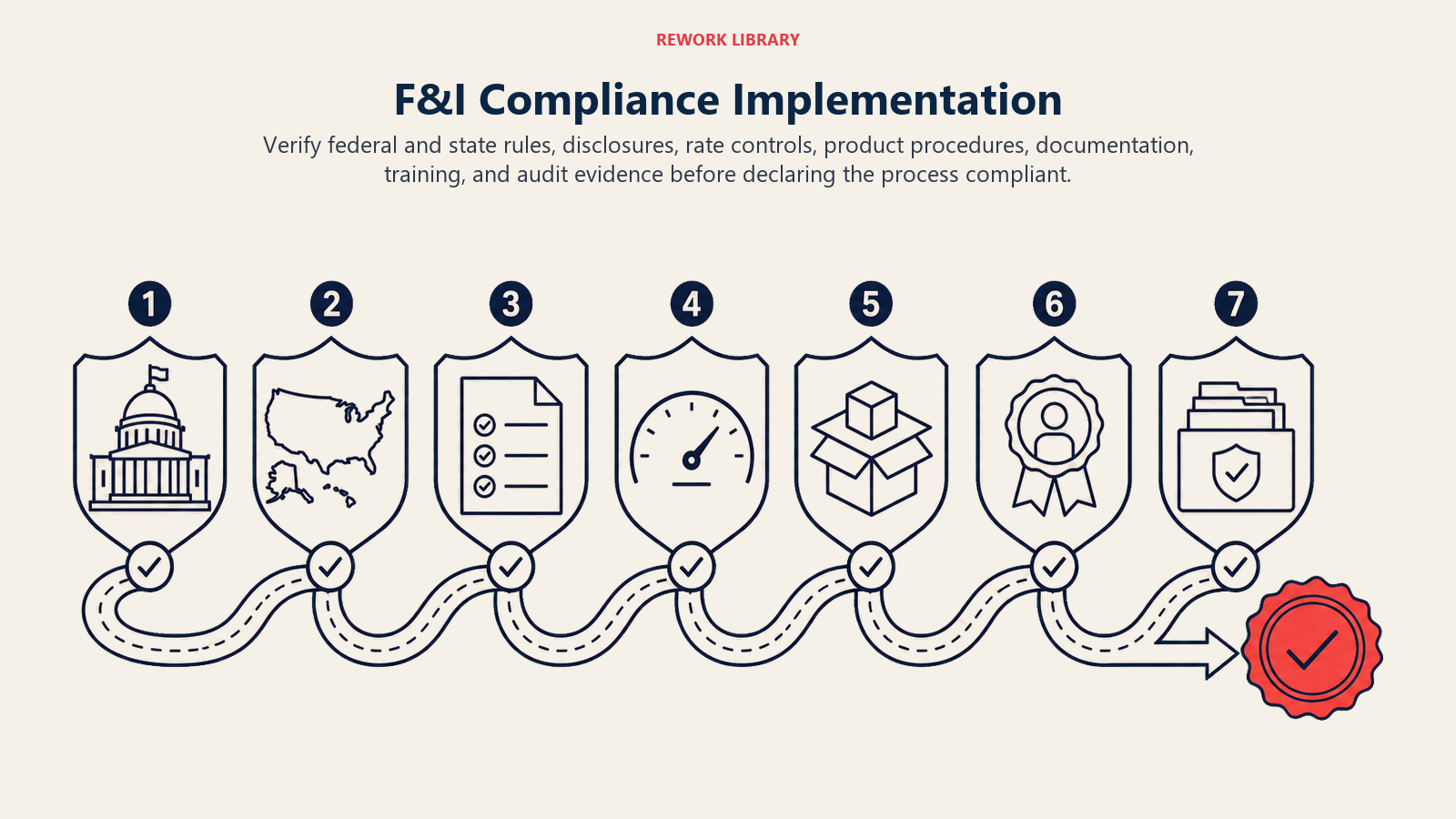

F&I Compliance Implementation Checklist

Federal Compliance Verification:

- ECOA anti-discrimination policy documented

- FCRA credit procedures and adverse action process defined

- TILA disclosure forms current and properly used

- Red Flags identity theft program documented

- Safeguards Rule data security measures implemented

- GLBA privacy notices provided on all transactions

State Compliance Verification:

- F&I licensing requirements identified and met

- State rate/reserve limitations documented and enforced

- State product disclosure requirements satisfied

- Cancellation rights policies match state requirements

- Record retention meets state minimum requirements

Menu Compliance:

- Full product disclosure on all menu presentations

- Cash price clearly disclosed

- Optional nature of products explicitly stated

- Payment impact shown transparently

- Multiple financing term options presented

- Menu template legally reviewed and approved

Rate and Reserve Compliance:

- Written rate markup policy exists

- Objective credit criteria documented

- Manager oversight process for rate decisions

- Rate markup consistency monitored

- Disparate impact analysis conducted periodically

Documentation Standards:

- Complete buyer's order on all deals

- All required signatures obtained

- Information legible and accurate

- Proper document sequencing followed

- E-signature compliance (if used)

- 7+ year retention policy implemented

Training Program:

- Initial F&I training for new managers (40+ hours)

- Quarterly compliance updates

- Annual comprehensive review

- Role-playing and scenario practice

- State certification maintenance tracked

- Training documentation maintained

Audit Preparedness:

- Monthly internal deal jacket audits

- Per-deal compliance checklist

- Lender audit response procedures

- Regulatory audit cooperation plan

- Common findings prevention measures

- Audit finding tracking over time

Compliance Culture Elements:

- Leadership commitment demonstrated

- Violation consequences clearly defined

- Balanced incentive structure

- Complaint resolution process

- Continuous improvement practices

- Regular compliance metric review

F&I compliance isn't the enemy of profitability. It's the foundation for sustainable backend revenue. The dealers facing lawsuits, consent orders, and regulatory penalties? They're the ones who treated compliance as optional or bureaucratic waste.

The top-performing F&I departments? They achieve high PVR through ethical practices, consistent procedures, comprehensive training, and systematic documentation. They pass audits easily because they operate compliant processes every day, not scramble when auditors arrive.

Build compliance into your F&I operations from day one. Train thoroughly. Document completely. Monitor consistently. Audit internally. And create culture where ethical behavior and regulatory adherence are expected standards, not optional goals.

That's how you protect your dealership from legal exposure while building sustainable F&I profitability. It's not complicated. It just requires commitment, systems, and consistent execution.

Commit: write your F&I compliance policies. Implement systematic procedures. Train your people thoroughly. Execute consistently on every transaction. The alternative, hoping compliance problems don't happen, eventually results in the lawsuit, regulatory action, or reputation damage that costs far more than prevention would have.

External Resources

- NADA Compliance Resources - Comprehensive dealer compliance guidance including F&I regulations

- FTC Safeguards Rule for Auto Dealers - NADA resource on FTC data security requirements

- FTC CARS Rule Compliance - Federal Trade Commission guidance on auto dealer F&I disclosure requirements

- CFPB Auto Finance Supervision - Recent supervisory findings and enforcement priorities

- Dealer Compliance Strategies 2025 - PNI HCM - Key compliance strategies for modern automotive dealerships

Senior Implementation Consultant

On this page

- Federal Compliance Framework - Core Regulations

- State-Specific Regulations - Varying Requirements

- Menu Compliance - Presentation Requirements

- Rate and Reserve Compliance - Avoiding Rate Discrimination

- Product Sale Compliance - Proper Procedures

- Documentation Best Practices - Protection Through Paperwork

- Training and Certification - Staff Competency

- Audit Preparedness - Internal and External Reviews

- Creating Compliance Culture - Beyond Checkboxes

- F&I Compliance Implementation Checklist

- External Resources