F&I Product Menu Presentation - Maximizing Product Penetration & PVR - 2026 Guide

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

A 20-point improvement in VSC penetration, from 40% to 60%, adds more than $400 to your per-vehicle retail average. Over 100 monthly deals, that's $40,000 in additional monthly gross profit. The difference between average F&I managers and top performers isn't product knowledge or luck. It's menu presentation skill.

The best F&I managers don't sell products. They present protection solutions through consultative conversations that help customers make informed decisions. They understand that product penetration and customer satisfaction aren't competing goals, they're complementary when you present value correctly.

This isn't about manipulation tactics or pressure closes. It's about systematic presentation frameworks, needs-based questioning, value positioning, and professional service that customers appreciate.

Menu Presentation Philosophy

Your approach to menu presentation determines everything that follows. The consultative vs. transactional distinction matters. Transactional F&I managers rush through product menus trying to close before customers object. They present features, state prices, and push for decisions. This generates mediocre penetration and poor customer satisfaction.

Consultative F&I managers take a different approach. They ask questions about how customers use vehicles, what concerns them about ownership costs, and what protection they value. They educate rather than manipulate. They position products as solutions to customer-expressed needs.

Needs-based selling starts with discovery. "How long do you typically keep your vehicles?" "What's your budget for unexpected repairs?" "Have you had warranty claims in the past?" These questions reveal customer priorities and risk tolerance, which inform your product recommendations.

Education over manipulation builds trust. Customers appreciate F&I managers who explain what products do, show real repair cost examples, and acknowledge when products might not fit their situation. Transparency differentiates you from managers who use confusion as a sales tactic.

Long-term customer value thinking changes your perspective. A customer who buys GAP and VSC today but feels pressured might give you a bad CSI score and never return. A customer who buys only GAP but appreciates your professional presentation might buy 10 vehicles over 20 years and refer friends. Play the long game.

Compliance through transparency is simpler than compliance through legalistic disclosure. Present products clearly. Explain costs separately. Show payment impacts honestly. When customers understand what they're buying and why, compliance documentation becomes a formality rather than a legal shield.

Pre-Presentation Preparation

The menu presentation starts before the customer enters your office. Customer profile review gives you context. Look at the credit application. Are they a high-mileage driver? That increases VSC value. Do they have tight DTI (debt-to-income)? They might be payment-sensitive. Is this their first luxury vehicle? They might not understand maintenance costs. Deal structure understanding shows you what room you have. What's the agreed payment? What's the maximum payment they qualified for? If there's a $75/month gap, you can add products without exceeding their budget. If they maxed out their payment to buy the vehicle, you have less room. Understanding the desking deal structure sets you up for success.

Payment room availability is critical. The sales team should structure deals leaving payment room for F&I. If a customer qualifies for $650/month but agreed to $595, you have $55/month to work with. A $2,500 VSC at 72 months adds about $38/month. A $795 GAP policy adds $12/month. That fits within the budget.

Pre-selling status from sales team tells you if groundwork was laid. Did the sales consultant mention protection products? Did they warm the customer up to the idea? Or did they promise "no other products, just sign and go"? Knowing this prevents surprises.

The Welcome and Transition

First impressions set the tone for the entire presentation. Congratulations on purchase establishes positive momentum. "Congratulations on your new Silverado! I saw you went with the LTZ package, great choice." This reinforces their buying decision and creates enthusiasm.

Role explanation clarifies your purpose. Don't assume customers understand what you do. "My job is to finalize your payment options and show you some protection products that many customers find valuable. I'll explain what's available, you decide what makes sense."

Setting time expectations prevents frustration. "This usually takes about 45 minutes. I'll review your financing, show you a few protection options, and get your paperwork completed." Now they're not surprised when it takes longer than five minutes.

Building on sales relationship connects you to the positive experience. "Josh mentioned you're planning to use this for towing your boat. That's actually relevant to some of the protection products I'll show you." This shows continuity and attention to their needs, building on the automotive sales process foundation.

Menu Technology and Display

How you present products affects how customers perceive them. Electronic menu systems vs. paper is now standard at most stores. Electronic menus from providers like Route One or DealerTrack offer visual comparison, payment-based presentation, and compliance documentation. According to Cox Automotive research, maximized menu selling through electronic presentations helps dealerships achieve higher per-vehicle revenue. They're more professional than paper four-squares.

Payment-based presentation works better than price-based for most customers. Instead of saying "this VSC costs $2,895," you show "adding this VSC changes your payment from $595 to $633." Customers think in monthly payments, not total prices.

Visual comparison advantages help customers evaluate options. Side-by-side comparisons showing coverage levels, deductibles, and payment impacts let customers see trade-offs clearly. "Here's basic coverage at $32/month, enhanced coverage at $39/month, and comprehensive coverage at $48/month."

Menu design best practices include clean layouts, clear terminology, and logical flow. Avoid cluttered screens with too many options. Present products sequentially. Use simple language instead of insurance jargon. Show total cost and payment impact for every product.

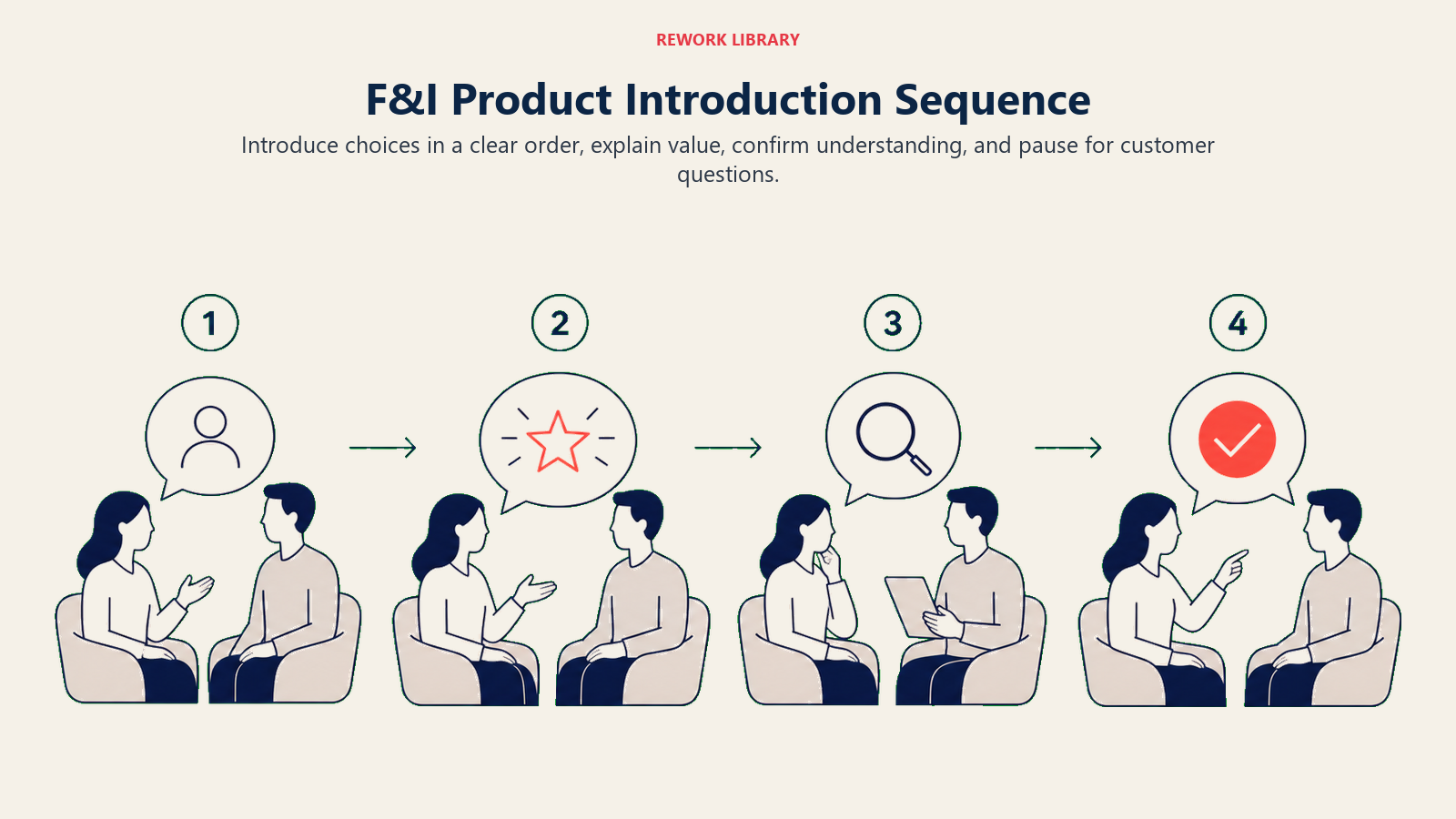

Product Introduction Sequence

The order you present products affects penetration rates. VSC/extended warranty first because it's your highest-value product and generates the most commission. Industry data shows service contract penetration rates average 40-46%, making VSC one of the most important F&I products. Start with the most important product while customer attention is highest. Position it as primary protection, not an add-on. Present VSC by addressing the risk: "Factory warranty covers you for three years or 36,000 miles. Most customers keep vehicles longer. A transmission replacement on this truck runs $5,500-6,500. The powertrain VSC extends your coverage to 100,000 miles for about $39 per month. That's your primary protection."

GAP insurance follows naturally after discussing financing. "You're financing $34,500 at 6.9% over 72 months. In the first few years, you'll owe more than the vehicle's worth. If it's totaled, your insurance pays current value, not what you owe. GAP covers that difference, about $12 per month."

Maintenance plans are easier to present after VSC and GAP because they're lower cost and have clear ROI. "Scheduled maintenance, oil changes, tire rotations, inspections, costs about $800-1,000 over three years if you pay retail. This plan pre-packages that for $695. You save money and guarantee you keep up with maintenance." Industry data shows prepaid maintenance penetration averaging 12-17%.

Ancillary products like tire & wheel protection, key replacement, or appearance protection come last. These are the "nice to have" products after primary protection is addressed. Present them quickly and move to close if the customer isn't interested.

Add-on payment increments should be presented cumulatively. "Your base payment is $595. Adding the VSC brings it to $633. GAP makes it $645. And the maintenance plan brings the total to $660. You're still well within your qualified maximum of $700."

Value Presentation Techniques

How you frame value determines whether customers buy. Risk positioning with real repair cost examples makes protection tangible. Don't just say "covers repairs." Say "the turbocharger on this engine costs $2,800 to replace. The infotainment system is $1,900. The transmission is $6,500. Any one of those repairs costs more than this entire VSC."

Peace of mind messaging addresses emotional needs. "I can't predict what will break or when. But I can tell you that most customers who decline coverage and then have a major repair wish they'd made a different choice. This eliminates that worry."

Payment vs. out-of-pocket cost framing makes products seem more affordable. A $2,500 VSC sounds expensive. But "$38 per month for 5 years of protection" sounds reasonable. Frame everything in monthly payment impact.

Social proof and testimonials build credibility. "About 60% of our customers choose VSC coverage. I had a customer last month whose turbo failed at 48,000 miles, $3,200 repair fully covered. She was grateful she bought the coverage."

Handling Payment Objections

"I can't afford it" is the most common objection. Address it systematically. Term extension options create payment room. "Your 72-month loan is $595/month. If we extended to 78 months, that's $558. That creates $37/month we could use for VSC while keeping you at your target payment." This works if the customer isn't already at maximum term. Understanding finance source management helps optimize terms. Product reduction strategies offer alternatives. "If the comprehensive coverage doesn't fit your budget, here's powertrain-only coverage that's $24/month instead of $48. You're still protecting the most expensive repairs."

Remove and reconsider approach handles resistance without killing the sale. "No problem, we'll skip the VSC for now. You can always add it later before factory warranty expires, though the price will be higher then." This plants the seed that declining is a short-term decision.

Alternative coverage levels let customers step down instead of walking away. "The 100,000-mile plan might not fit right now. Here's the 60,000-mile option at $28/month instead of $48. Still gives you several years of protection."

The Close

Getting to signature requires clear direction and confidence. Assumptive close positions products as the default choice. "Which coverage level works best for you, comprehensive or powertrain?" This assumes they're buying, the question is just which option.

Alternative choice close is a variation. "Do you want the $500 deductible or zero deductible on your VSC?" Either answer moves toward purchase.

Summary of coverages selected creates commitment. "Perfect. So we're doing the comprehensive VSC with $100 deductible, GAP coverage, and the maintenance plan. That brings your payment to $648. Let me get your paperwork ready."

Addressing final concerns handles last-minute hesitation. If they pause, ask directly: "You seem uncertain. What concerns you?" Sometimes it's payment, sometimes it's value, sometimes it's decision fatigue. Address the specific concern rather than guessing.

Post-Menu Follow-Up

The transaction doesn't end at signature. Coverage explanation and documentation ensures understanding. "You've got VSC coverage through 100,000 miles with a $100 deductible. Here's your coverage document and claim phone number. Keep this in your glove box." Claim process overview prevents future frustration. "If you need warranty service, call the claims number first to verify the repair is covered and get authorization. Then take it to any licensed shop. You pay the deductible, the claim covers the rest."

Setting service expectations builds dealership loyalty. "Your maintenance plan covers all scheduled service here at our dealership. We'll send you appointment reminders when you're due. This plan also gets you service loaners and priority scheduling."

Cancellation disclosure (as required by law) must be clear. "Most products have a 30-60 day full-refund period if you change your mind. After that, cancellation is pro-rated. I'd rather you keep the coverage because I believe it's valuable, but I want you to know you have options." Follow compliance best practices for all disclosures.

The best F&I managers run $2,200-2,800 PVR with 75%+ CSI scores. That's not contradictory, it's complementary. Customers appreciate professional service, clear explanations, and valuable products presented without pressure. Master the consultative presentation approach, understand your products deeply, and position value effectively. The results follow: higher penetration, stronger PVR, better customer satisfaction, and a sustainable F&I business model that generates profit for years.