Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

A 10-point improvement in approval rate, from 75% to 85%, doesn't sound dramatic until you do the math. For a dealership selling 100 vehicles monthly, that's 10 additional sold units. At $1,800 average front-end gross and $2,000 backend gross, you're looking at $38,000 in additional monthly profit. Over a year, that's $456,000.

Finance source management isn't about having relationships with lenders. It's about building and optimizing a lender network that maximizes approval rates, secures competitive buy rates, and generates maximum dealer reserve across the credit spectrum. This is a core function of the F&I department.

The best F&I directors treat lender relationships as strategic partnerships, not transactional arrangements. They understand which lenders to use for which credit profiles, how to position deals for approval, and how to leverage volume for better rates. This expertise translates directly to bottom-line profitability.

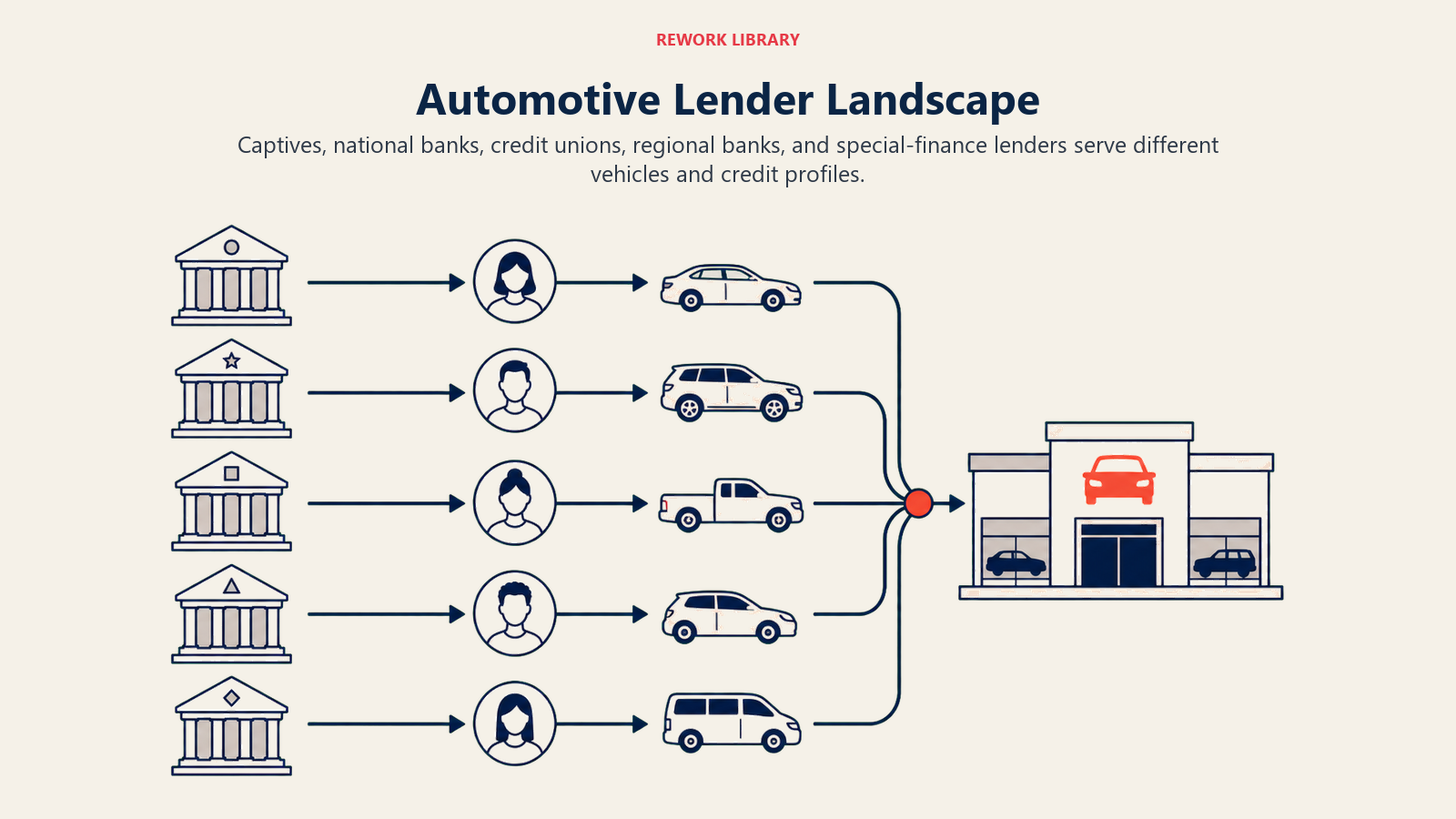

Finance Source Landscape

Understanding the different types of lenders and what they offer is the foundation of effective finance source management.

Captive finance companies are manufacturer-owned lenders like GM Financial, Toyota Financial Services, or Ford Credit. They exist primarily to support vehicle sales for their parent brands. Captives offer several advantages: higher approval rates on franchised brand vehicles, subvented (subsidized) interest rates on promotional programs, and manufacturer incentive qualification.

But captives have limitations. They're selective on credit quality, often requiring scores above 620-640. They focus primarily on new vehicle financing. And they may not offer competitive rates on used vehicles or competitor brands.

National banks and credit unions like Chase, Wells Fargo, Bank of America, or Navy Federal provide broad market coverage with competitive rates, especially for prime credit customers (720+ scores). They finance both new and used vehicles across all brands.

National lenders bring volume capacity and technology platforms that integrate smoothly with dealer systems. But they can be bureaucratic, with slower decision turnaround and less flexible underwriting than smaller lenders.

Regional banks operate in specific geographic areas and often provide more flexible underwriting than national lenders. They know local market conditions, they're more willing to work with marginal deals, and they provide relationship-based service.

Regional banks can be excellent partners for near-prime credit (660-719) and unique situations that don't fit standard underwriting boxes. But they have lower volume capacity and may not offer the best buy rates on prime credit deals.

Sub-prime lenders specialize in higher-risk credit profiles (typically scores below 660). Companies like Santander, Credit Acceptance, Westlake Financial, and AmeriCredit finance customers that captives and banks decline. They charge higher rates, require larger down payments, and impose stricter terms, but they approve deals other lenders won't touch. Understanding automotive lead management helps identify customers early in the process.

Sub-prime lenders generate higher dealer reserve (often 3-5% markup vs. 2% for prime lenders) due to higher risk. But they also have stricter documentation requirements and higher chargeback exposure.

Special finance companies go even deeper into sub-prime territory, financing customers with credit scores and approval rates below 600, bankruptcies, repossessions, or limited credit history. These lenders often require GPS tracking, starter interrupt devices, or additional collateral.

Special finance is a profit opportunity (reserve can exceed $3,000 per deal) but requires expertise. Poor execution leads to high default rates, repossessions, and chargeback losses.

Buy-here-pay-here (BHPH) as a last resort means the dealership itself finances the customer. You're both the seller and the lender. BHPH generates maximum profit potential but carries maximum risk: you're responsible for collections, repossessions, and credit losses.

Most franchised dealers avoid BHPH due to complexity and risk. It's more common in independent used car operations.

Building a Lender Network

Your lender portfolio needs strategic construction to cover all customer types and maximize approval rates.

Optimal number of lenders is typically 8-12 active lending sources. Fewer than eight and you're leaving gaps in credit coverage or losing competitive leverage. More than twelve and you're creating administrative burden without meaningful benefit.

Your portfolio should include 1-2 captive lenders (if franchised), 2-3 national banks or credit unions for prime credit, 1-2 regional banks for near-prime, 2-3 sub-prime lenders for higher-risk credit, and 1-2 special finance sources for deep sub-prime.

Coverage across credit spectrum ensures you can approve deals at every credit tier. Prime (720+), near-prime (660-719), sub-prime (600-659), and deep sub-prime (below 600) each require different lenders. Gaps in coverage mean declined deals and lost sales.

New vs. used vehicle specialization matters because some lenders only finance newer vehicles (less than 5 years old with under 60,000 miles). Others specialize in older used vehicles. Match your inventory mix to your lender capabilities.

Geographic considerations affect lender availability. Some lenders operate nationally. Others are regional or state-specific. If you're near state borders, ensure you have lenders licensed in all relevant states.

Relationship vs. transactional lenders is a strategic choice. Relationship lenders value your volume, provide relationship managers, and work marginal deals. Transactional lenders offer competitive rates but provide no special treatment. You need both types in your portfolio.

Lender Relationship Management

Building a lender network is step one. Managing those relationships for maximum value is step two.

Regular communication and visits strengthen relationships. The best F&I directors schedule quarterly meetings with key lender representatives. These meetings review volume trends, discuss problem deals, negotiate rate improvements, and identify new programs.

Face-to-face relationships matter. When a lender rep knows you personally, they're more likely to work a marginal deal or expedite a funding.

Volume commitment and performance gives you leverage. Lenders reward volume with better rates, faster decisions, and program access. If you're sending a lender 15-20 deals monthly, you have negotiating power. If you're sending two deals monthly, you're a transactional account.

Decision turnaround time expectations should be defined. Prime credit decisions should be instant or within 30 minutes. Near-prime decisions within 2-4 hours. Sub-prime decisions within 24 hours. If a lender consistently misses these timelines, communicate the issue or reduce submissions.

Program participation requirements from lenders often include training certifications, compliance standards, or technology integrations. Meet these requirements to maintain access to best rates and programs.

Dispute resolution procedures need to be established before you need them. What happens if you disagree with a vehicle valuation? How do you escalate a funding delay? Having clear escalation paths prevents small issues from becoming deal-killers.

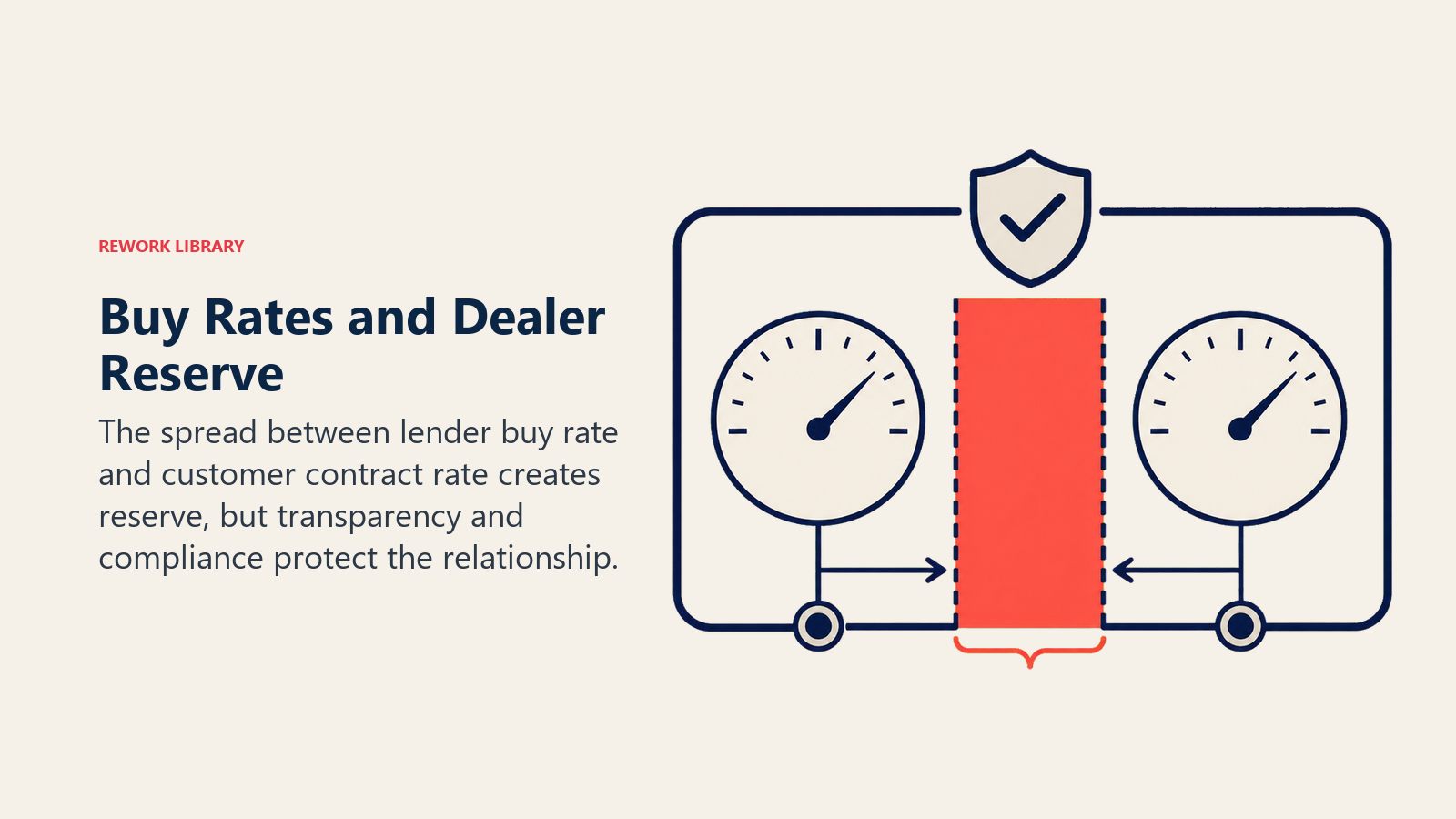

Buy Rates and Reserve

Understanding how dealer compensation works is essential to optimizing finance profitability.

How buy rates are determined depends on the customer's credit profile, loan-to-value ratio, term length, and lender's risk appetite. A 760 credit score with 20% down and 60-month term might qualify for a 5.5% buy rate. A 640 score with minimal down and 72-month term might get 9.9%.

Lenders send rate sheets showing buy rates by credit tier and term. F&I managers review these sheets to determine the best buy rate for each customer.

Rate markup and reserve maximums are regulated. Most states limit dealer markup to 2-2.5% above buy rate. Some states (California, Connecticut) have stricter limits. The CFPB issued guidance on indirect auto lending under ECOA to prevent discriminatory rate markups. Violating these limits creates legal liability and regulatory sanctions. Follow F&I compliance best practices carefully.

Reserve is calculated based on the markup and loan amount. A $30,000 loan marked up 2% over 72 months generates approximately $1,800-2,000 in dealer reserve.

Participating vs. non-participating lenders handle reserve differently. Participating lenders pay reserve upfront when the loan funds, subject to chargeback if the customer refinances or pays off early (typically within 90-180 days).

Non-participating lenders pay reserve over time as the customer makes payments. This reduces chargeback risk but delays revenue recognition.

Reserve holdback and chargeback policies vary by lender. Some lenders hold back a portion of reserve (10-20%) for 90 days to offset potential chargebacks. Others pay full reserve upfront but aggressively pursue chargebacks if customers refinance.

Understanding each lender's policy helps you project cash flow and avoid chargeback surprises.

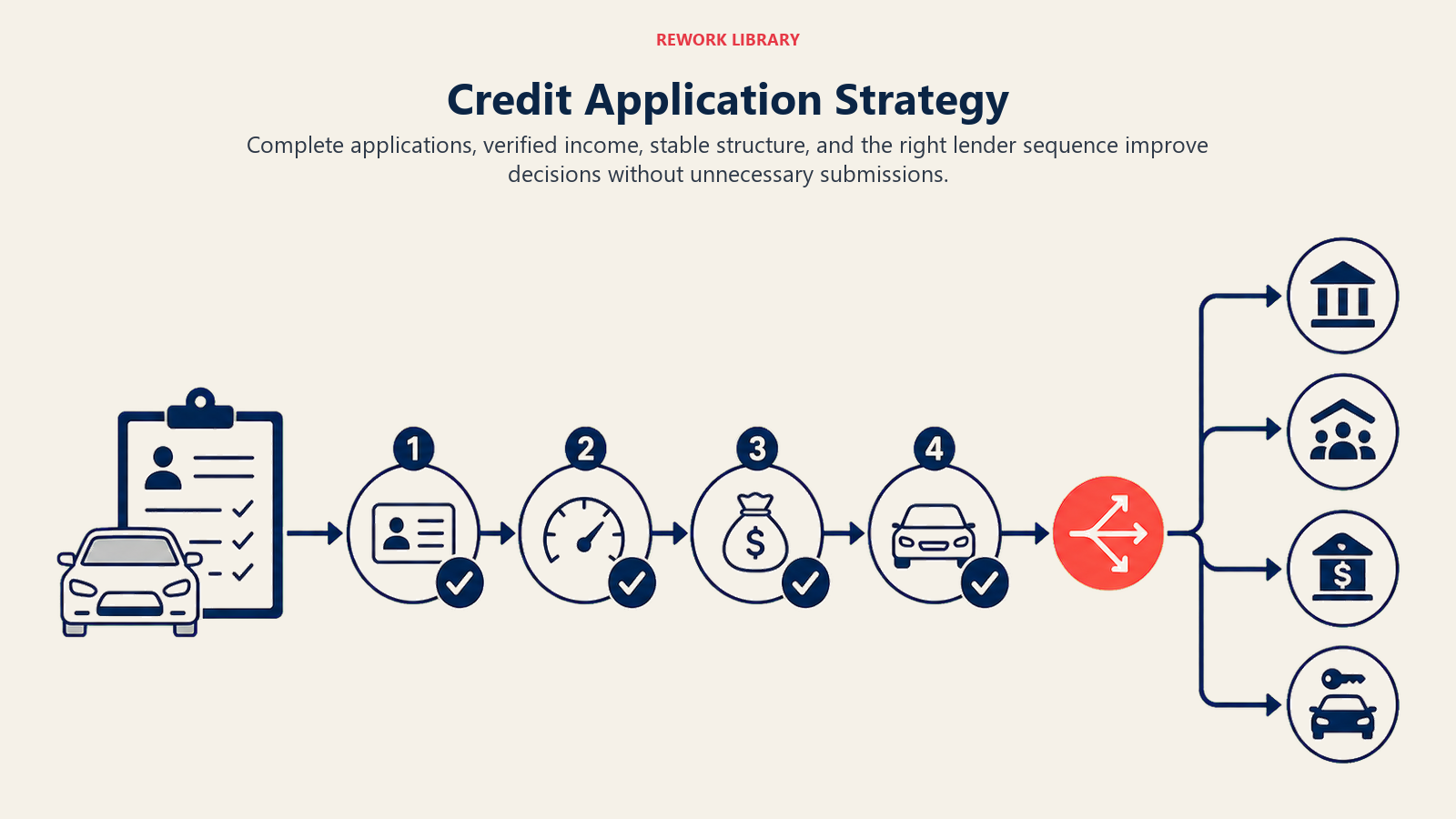

Credit Application Strategy

How you submit deals to lenders affects approval rates and reserve potential.

Credit score and tier determination should happen before you submit to lenders. Pull credit internally if possible. Know the score, the credit history, the payment-to-income ratio, and any derogatory marks.

This prevents wasted submissions and credit bureau inquiries. A 580 score won't get approved by a captive lender no matter how well you present it. Send it to the right lender first.

DTI (debt-to-income) considerations are critical for approval. Most lenders limit DTI to 40-50%, meaning monthly debt payments (including the new car payment) can't exceed 40-50% of gross monthly income. Understanding Equal Credit Opportunity Act requirements ensures you evaluate applications fairly and compliantly.

If a customer shows $6,000 monthly income and $2,000 in existing debt payments, they can qualify for about $400-600 in new car payment depending on lender. Knowing this before you submit prevents declined deals.

LTV (loan-to-value) requirements limit how much lenders will finance relative to vehicle value. Prime lenders might finance 120% LTV. Sub-prime lenders might limit to 110%. Special finance might require 90-100% LTV (meaning down payment is mandatory).

If you're trying to bury $5,000 negative equity on a $25,000 vehicle, you need a lender that accepts 120% LTV. Submitting to a lender with 110% maximum wastes time.

First vs. simultaneous submission is a tactical decision. Submitting to your best-rate lender first preserves the opportunity to submit elsewhere if declined. Simultaneous submission to multiple lenders generates multiple credit inquiries but speeds approval.

Best practice: submit to your highest-probability lender first. If declined, simultaneous submission to backup lenders.

Protecting credit bureau pulls is both customer service and compliance. Every credit inquiry impacts the customer's credit score slightly. Excessive inquiries can hurt approval chances. The Fair Credit Reporting Act regulates how dealerships access and use consumer credit information.

Shotgunning deals to 10 lenders hoping someone approves is lazy F&I work that damages customer credit. Submit strategically to lenders likely to approve based on credit profile.

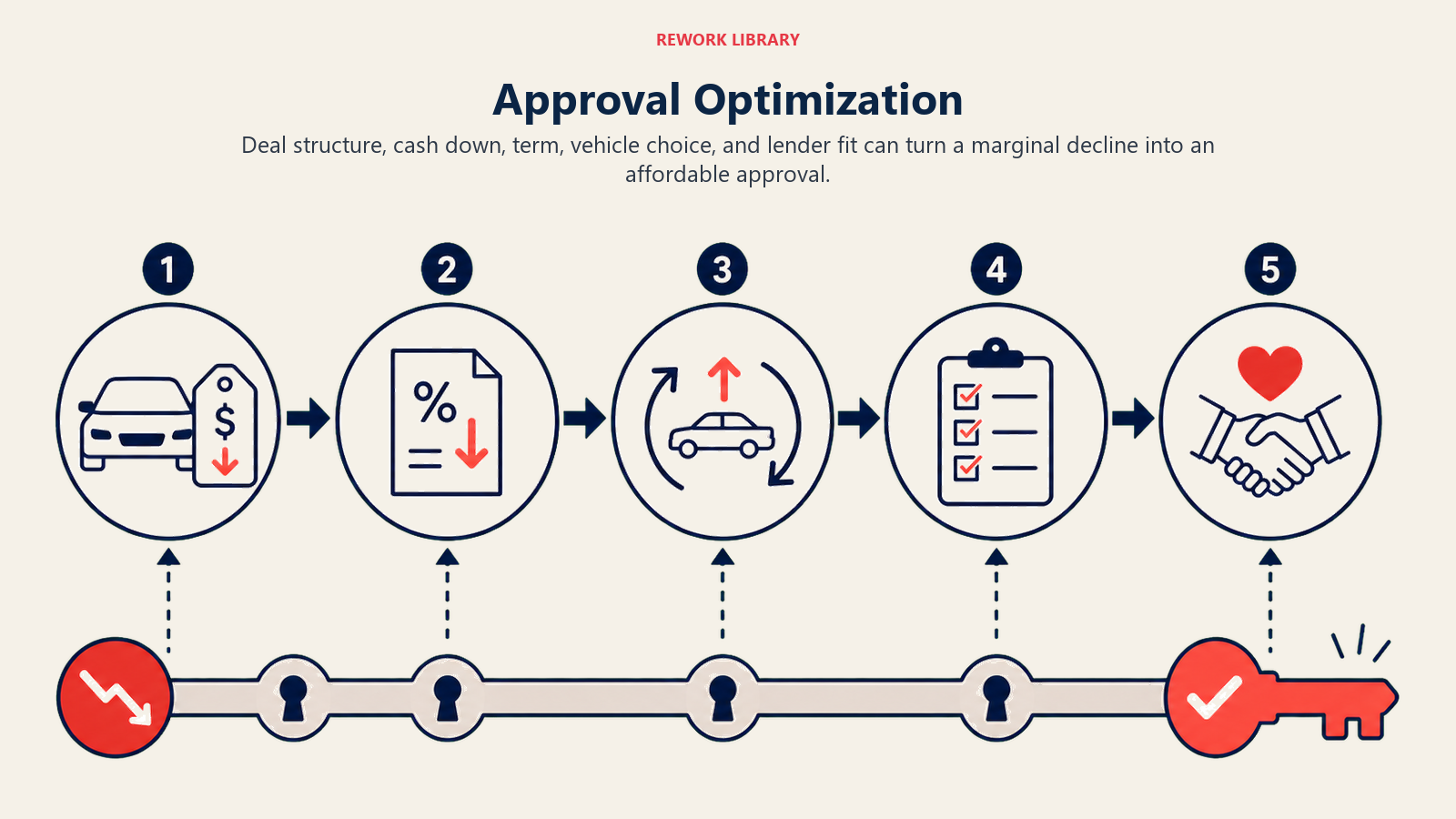

Approval Optimization

Small improvements in approval rate generate massive profitability improvements.

Application completeness and accuracy is foundational. Incomplete applications (missing employment info, wrong income figures, inaccurate addresses) trigger declines or delays. Double-check every field before submission.

Income verification strategies help marginal deals. Can the customer provide pay stubs? Bank statements? Tax returns? Lenders approve more deals when income is documented. Help customers gather this documentation quickly.

Down payment and trade equity positioning improves approval rates. A customer with $3,000 down or $4,000 trade equity has better approval odds than one with zero down. If a deal is borderline, ask for additional down payment. This is a key part of desking deal structure.

Co-buyer and co-signer utilization salvages declined deals. A customer with a 590 score might not qualify alone, but add a co-buyer with a 680 score and the deal gets approved. Know when to suggest co-buyer or co-signer options.

Stip (stipulation) management speeds funding. When a lender approves with stipulations (requirements like proof of income, proof of residence, or vehicle inspection), fulfill those stips immediately. Delayed stip fulfillment costs days and risks deal cancellation.

Special Finance Management

Sub-prime lending requires specialized expertise and processes.

Sub-prime lender relationships need extra attention. These lenders take higher risks, so they demand stronger documentation, clearer communication, and better performance. Deliver on your commitments and they'll approve more deals.

Documentation requirements (full stip packages) are extensive. Sub-prime lenders typically require proof of income (pay stubs or bank statements), proof of residence (utility bill or lease), proof of phone (cell phone bill), valid driver's license, proof of insurance, and references.

Having a stip checklist and gathering documents proactively speeds approvals.

GPS and starter interrupt devices are often required on deep sub-prime deals. These devices let lenders locate and disable the vehicle if payments stop. Some customers resist them. Position them as tools that enable approval: "This device is how the lender manages risk, which allows them to approve your application." Clear communication improves customer experience.

Higher reserve potential with higher risk is the trade-off. Sub-prime lenders often allow 3-5% markup vs. 2% for prime lenders. A $25,000 sub-prime loan at 4% markup generates $2,500-3,000 in reserve vs. $1,500 for a prime loan.

But that extra reserve comes with extra risk: higher chargeback rates due to early payoffs or defaults.

Collection support and repossession partnerships matter. Some sub-prime lenders provide collection support if customers miss payments. This protects you from chargeback while helping customers stay current. Understand what support your lenders offer.

Captive Finance Advantages

Manufacturer-owned lenders provide unique benefits worth understanding.

Subvented rates and special programs are the primary advantage. Manufacturers subsidize interest rates to move inventory. A retail rate of 6.5% might be subvented to 0.9%, 1.9%, or 2.9%. These low rates drive sales and generate customer savings.

The dealership doesn't earn reserve on subvented rates, but you earn volume bonuses and customer goodwill.

Approval rate advantages on franchised brands are significant. Toyota Financial Services approves Toyota buyers at higher rates than generic lenders because the captive understands residual values, customer loyalty, and brand-specific risk profiles.

Lease support and residual positioning comes from captives. They set residual values (projected end-of-lease vehicle value) that make lease payments competitive. Strong residuals enable lower lease payments, which drives lease penetration. Track this as part of dealership revenue streams.

Manufacturer incentive qualifications sometimes require captive financing. A $2,000 customer cash incentive might require financing through the captive. This creates additional motivation to use captive lenders when available.

Finance Source Performance Tracking

You can't optimize what you don't measure. Track lender performance systematically.

Approval rates by lender show you which lenders approve the highest percentage of submissions. Target: 75-85% approval rate per lender. Below 60% means you're submitting wrong deals to that lender. Above 90% might mean you're under-utilizing them.

Average buy rate by tier reveals which lenders offer best rates. If Bank A consistently offers 5.9% on 720+ credit while Bank B offers 6.4%, you should favor Bank A for prime credit.

Reserve per deal by source shows profitability. Lender C might approve 80% of deals but generate $1,200 average reserve. Lender D approves 85% and generates $1,600 average reserve. Lender D is more valuable.

Decision turnaround time affects customer experience and close rates. Lenders that consistently take 4+ hours for decisions cost you sales because customers get tired of waiting. Track this and address slow performers.

Chargeback rates indicate whether you're selling deals that don't stick. If Lender E has 18% chargeback rate while others average 8%, either you're submitting wrong deals to them or their customer risk profile is poor. Either way, it's costing you money.

Finance source management is the backbone of F&I profitability. Build a diverse lender network covering all credit tiers. Cultivate relationships through volume, communication, and performance. Submit deals strategically to maximize approval rates and reserve. Track performance religiously and optimize continuously. Do this well and you'll approve more deals, generate more reserve, and deliver better customer financing experiences, all of which drive sustainable dealership profitability.