Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

The difference between a $1,500 PVR and a $2,000 PVR doesn't sound dramatic until you do the math. For a dealership selling 120 vehicles per month, that $500 increase adds $60,000 to your monthly bottom line, $720,000 annually. That's real money, and it comes from products your customers actually need.

F&I Per Vehicle Retail is the single most important metric for measuring backend profitability. But most dealerships don't truly understand what drives it, how to benchmark it properly, or where the biggest improvement opportunities hide.

Understanding PVR Calculation

At its core, PVR is simple math: total backend gross profit divided by retail units delivered.

If your F&I department generated $180,000 in backend gross last month and you delivered 120 vehicles, your PVR is $1,500. That's your baseline. But the real insight comes from breaking this number down.

Total PVR tells you overall performance. Product-specific PVR shows you where money's being made or left on the table. Some dealerships track VSC PVR separately from GAP PVR, maintenance plan PVR, and ancillary product PVR. This granular view reveals which products need better penetration or pricing.

New vehicle PVR typically runs $200-400 lower than used vehicle PVR. Why? Used car buyers finance more often, need GAP insurance more urgently, and face higher maintenance concerns. If your new vehicle PVR is $1,400 and used is $1,800, that's normal. If the gap is wider than $600, something's wrong with your new vehicle F&I process.

Finance PVR excludes cash deals entirely. Since you can't sell finance reserve or most F&I products to cash buyers, tracking finance-only PVR gives you a cleaner picture of your FF&I managersI managers' true performance. A $2,200 finance PVR with 75% finance penetration is better than a $1,900 overall PVR.

Lease PVR runs lower because lease customers resist products that extend beyond their lease term. But you can still sell short-term maintenance plans, GAP, tire and wheel protection, and appearance packages. Don't skip the F&I process just because it's a lease.

What Actually Drives PVR

PVR is the sum of multiple revenue streams, each with its own profit potential.

Finance reserve comes from rate markup on indirect loans. If you secure a 5.9% rate from the lender and the customer accepts 7.9%, that 2-point spread generates reserve income. At typical reserve rates, that 2-point markup on a $30,000 loan for 72 months produces about $1,800 in reserve. That alone can represent 60-70% of your total PVR.

But finance reserve isn't guaranteed. Lenders cap reserve at 2-2.5 points depending on your state's regulations. Some states don't allow any markup at all. And if your sales team negotiates away payment room, you can't mark up the rate without blowing the payment structure.

VSC commission typically ranges from 40-50% of the selling price. Sell a $2,500 extended warranty, earn $1,000-1,250 in gross. With 50-60% penetration, VSC alone should contribute $500-750 to your PVR. If it doesn't, you're either not presenting effectively or your pricing is too low.

GAP insurance commission runs 60-80% of selling price. A $795 GAP policy nets you $476-636. With 70% penetration on financed vehicles, that's $333-445 per delivered unit. GAP has the highest commission rate of any F&I product, yet many dealers underperform here.

Maintenance plans vary wildly by brand and pricing structure. Factory plans pay 10-20% commission. Dealer-owned plans can generate 50-70% margin. A $1,500 maintenance plan at 50% margin contributes $750 to backend gross. At 40% penetration, that adds $300 to PVR.

Ancillary products include tire and wheel protection, theft protection, appearance protection, key replacement, and windshield protection. Each product adds $50-150 to PVR when presented properly. The problem is most FF&I managersI managers either ignore these products or bundle them poorly.

Documentation fees contribute to backend gross in many states. A $699 doc fee on every deal adds $699 to PVR if it's pure profit. But most states regulate doc fees, and many dealerships use doc fees to cover legitimate administrative costs rather than profit centers.

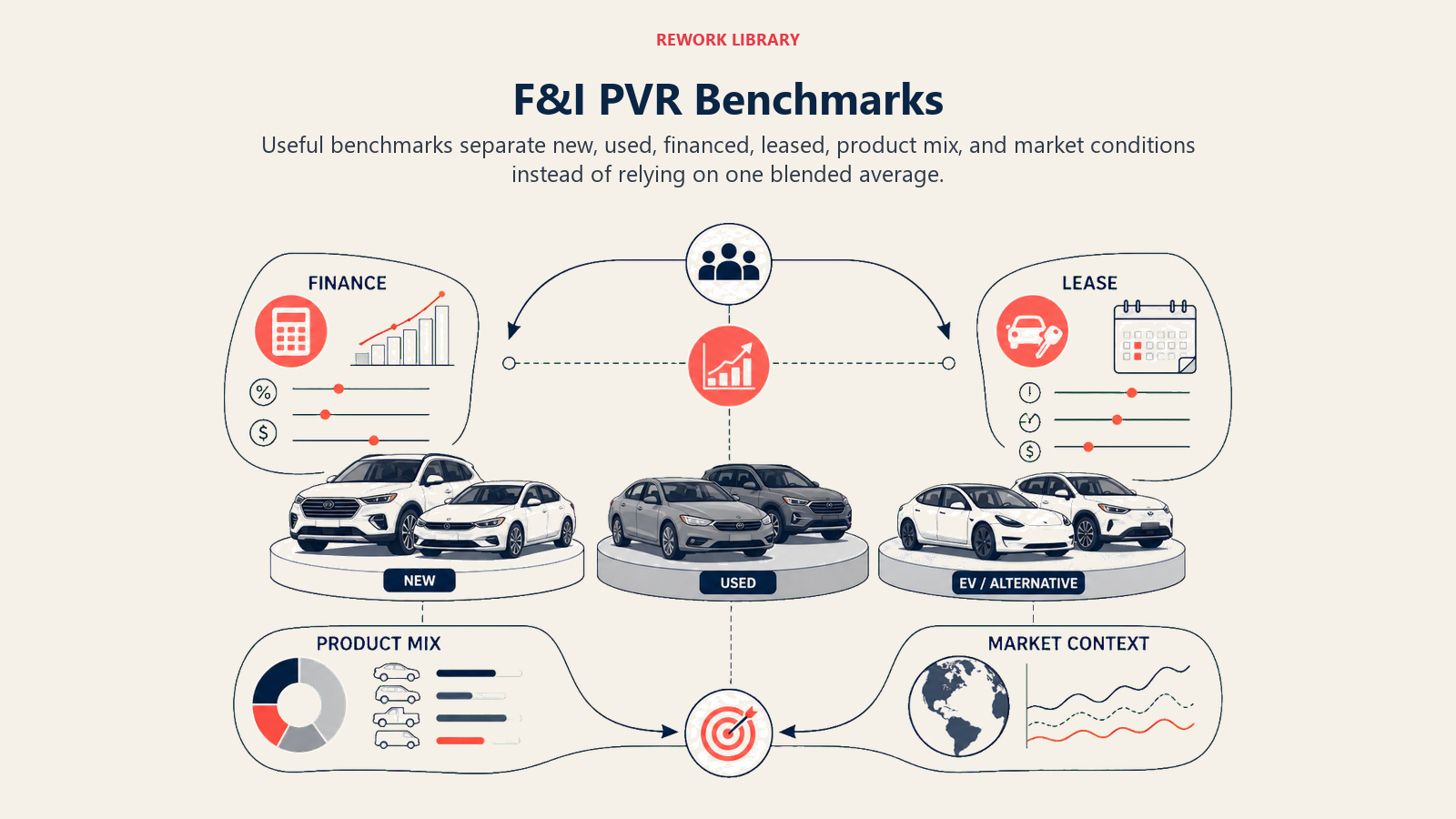

Industry Benchmarks That Actually Matter

NADA benchmarks provide guidance, but they lag current market conditions by 12-18 months. Use them as directional targets, not gospel.

New vehicle PVR for top-performing dealerships ranges from $1,400 to $1,800. That's total PVR including cash deals. If you're below $1,400, you've got serious work to do. Finance-only new PVR should hit $1,800-2,200.

Used vehicle PVR targets sit at $1,600-2,200 for total PVR, and $2,000-2,600 for finance-only deals. Used car buyers need F&I products more than new car buyers, so penetration rates should be higher across every category.

Elite performers push past $2,500 total PVR. According to recent industry data, publicly owned dealerships averaged $2,501 per vehicle in Q4 2024. These aren't shady dealers forcing products on customers. They're stores with exceptional product presentation, menu design, sales processes that leave payment room, and FF&I managersI managers who view themselves as consultants rather than salespeople.

Regional variations matter more than most dealers realize. California's rate markup restrictions crush finance reserve income, forcing dealers to rely more heavily on product penetration and pricing. Texas and Florida dealers enjoy more favorable finance reserve regulations. Adjust your benchmarks based on your state's regulatory environment.

Brand variations are real. Luxury brands support higher PVR through wealthier customers, better credit profiles, and higher average transaction prices. A BMW store should target $2,200+ PVR. A Nissan store might target $1,600. That doesn't make one better than the other, it reflects different customer bases.

Penetration Rate Impact

Volume times average equals total revenue. The same math applies to PVR.

VSC penetration of 50% at $1,200 average selling price and 50% commission generates $600 per delivered unit. Increase penetration to 60%, keep average price the same, and you add $120 to PVR. That's the power of penetration improvement.

Most dealerships target 40-60% VSC penetration. Below 40%, you're leaving massive profit on the table. Above 60%, you're either exceptionally good or pushing too hard. The sweet spot is 50-55% with strong average pricing.

GAP penetration should hit 70-80% on financed deals. GAP is the easiest product to sell because the value proposition is obvious: if you total the vehicle, GAP pays off the negative equity. Yet many stores sit at 40-50% penetration. That gap represents $300-400 in lost PVR.

Maintenance plan penetration varies by brand. Factory plans on luxury brands can hit 50-60% because customers value convenience. Aftermarket maintenance plans on mass-market brands struggle to break 30% because customers don't see clear value. Price these plans aggressively and emphasize dealer service relationship benefits.

Ancillary products rarely exceed 30% penetration individually, but collectively they matter. If you sell tire and wheel at 25%, appearance protection at 20%, and key replacement at 15%, those three products at $600 average commission contribute $360 to PVR.

Calculate your penetration impact this way: Current penetration × current average price × commission rate = current PVR contribution. Then increase penetration by 10 percentage points and recalculate. That difference is your opportunity.

Product Pricing Strategy

Pricing is where most F&I directors fail. They either price too low chasing volume or price too high killing penetration.

Competitive pricing sounds smart until you realize you're competing against dealers who don't know their costs. Market pricing only makes sense when your market is rational. In F&I, it rarely is.

Cost-plus pricing gives you a foundation. If a VSC costs you $1,200, and you need 50% margin to hit your profitability goals, sell it for $2,400. Then test variations. Can you sell it for $2,600 without killing penetration? Try it. Does $2,200 boost penetration enough to offset lower margin? Test that too.

Menu design impacts pricing more than most dealers realize. A three-tier menu with good, better, best pricing anchors the customer on the middle option. Price the top tier 40% higher than middle and 80% higher than bottom. Most customers choose the middle, but 15-20% step up to the top tier when presented properly.

Term and coverage level influence pricing power. A 60-month VSC priced at $2,000 feels expensive. But the same $2,000 for 84 months and 120,000 miles feels like a bargain because you're framing it per-month over the coverage period.

Dealer-owned products give you pricing flexibility. You set costs, terms, and coverage. The downside is claims management and reserve requirements. Lender-backed products offer fixed costs and no claims risk, but limited pricing control. Most dealers use a mix, dealer products for maintenance and ancillary items, lender products for VSC and GAP.

F&I Manager Performance Tracking

Individual PVR accountability separates good F&I departments from great ones.

Set individual PVR goals based on each manager's experience level and deal mix. J.D. Power's research shows that customer satisfaction in the F&I office directly correlates with product penetration and profitability. A new F&I manager handling 60% used deals should target $1,600 PVR. An experienced manager with the same deal mix should hit $2,000+. Different goals for different people based on realistic expectations.

Product-specific penetration analysis reveals coaching opportunities. If one manager sells GAP at 85% penetration and another hits 45%, you've got a training issue. Sit with the low performer and diagnose the problem. Is it presentation? Objection handling? Menu design? Confidence?

Compensation structures tied to PVR drive behavior. A flat salary produces flat performance. Commission on backend gross aligns incentives with dealership profitability. But pure commission can create aggressive selling that damages CSI. A balanced approach, base salary plus commission with CSI guardrails, works best.

Performance improvement plans matter when managers consistently underperform. If your PVR target is $1,800 and someone's averaging $1,200 for three consecutive months, that's a performance issue requiring documentation and intervention. Either they improve through coaching and training, or they need a different role.

How Sales Process Impacts PVR

F&I profit starts in the sales tower, not the F&I office.

Sales managers who set payment expectations too low kill backend profit. When your sales manager quotes a payment based on zero down, max term, and minimum rate, there's no room for F&I products without blowing the payment. That $450 payment becomes $520 after adding VSC and GAP, and the customer walks.

Leaving payment room means quoting payments 10-15% higher than minimum. If your best payment is $450, quote $495. When the F&I manager adds products and the payment lands at $505, the customer accepts it because they expected $495. That $55 difference supports $2,000-2,500 in product sales.

Product value education before F&I builds receptivity. Sales consultants who mention "the F&I manager will explain protection options" create curiosity. Those who say "you'll need to sit through the F&I pitch" create resistance. Language matters.

Smooth handoffs to F&I preserve momentum. When the sales manager walks the customer to F&I, introduces them personally, and says something positive about the F&I manager, the customer enters with positive expectations. When they point down the hall and say "wait over there," you're starting from a deficit.

Deal structure determines F&I success. A deal with $5,000 down, 60-month term, and 6.9% rate leaves room for products. A deal with zero down, 84-month term, and 12.9% rate has no room. Structure deals for profit, not just approval.

Common PVR Killers

Most PVR problems come from preventable mistakes.

Aggressive discounting to close deals destroys backend profit. When your sales team gives away $2,000 in discount and then asks the F&I manager to "make it up on the back," you're setting up failure. You can't recover front-end losses with backend products consistently.

No payment room is the number one PVR killer. If every deal is structured at minimum payment, you can't add products without payment shock. This requires GM-level intervention because it's a sales department problem, not an F&I problem.

Poor product presentation skills cost $300-500 per deal. FF&I managersI managers who rush through menus, use jargon customers don't understand, or frame products as optional extras rather than essential protection leave money on every deal. Training fixes this.

Compliance-driven product removal happens when dealers panic over regulatory scrutiny. Yes, compliance matters. But removing profitable, legitimate products because you're afraid of regulators is an overreaction. Work with compliance experts to present products properly rather than eliminating them entirely.

Cash deals and bank direct finance bypass your F&I department completely. Customers who secure financing through their credit union don't sit with your F&I manager. You can't sell reserve, GAP, or most other products. Combat this by offering competitive rates and educating customers on product availability through dealer financing.

Rushed F&I processes kill penetration. When FF&I managersI managers feel pressure to "turn deals faster," they skip products or present them poorly. Yes, speed matters. But a 35-minute F&I process that generates $2,200 PVR beats a 20-minute process that generates $1,400.

PVR Improvement Roadmap

Systematic improvement requires a structured approach.

Start with current state assessment. Calculate PVR by F&I manager, new vs. used, finance vs. cash, and product category. Identify your biggest gaps. Is it VSC penetration? GAP pricing? Finance reserve? Ancillary products? You can't fix everything at once, so prioritize.

Set realistic goals by time period. If your current PVR is $1,400 and your target is $2,000, don't expect to get there in 30 days. Plan a 6-12 month improvement journey with quarterly milestones: $1,550 by Q2, $1,700 by Q3, $1,850 by Q4.

Training and skill development matter more than most dealers invest in. Send FF&I managersI managers to professional training. Role-play objections weekly. Record F&I presentations and review them together. Skills improve through deliberate practice, not osmosis.

Product portfolio optimization means evaluating which products to offer, at what price points, and through which providers. Drop products with low penetration and low profit. Add products your customers actually need. Negotiate better commission rates with providers based on volume.

Process improvements include menu redesign, payment quoting changes, sales-to-F&I handoff standardization, and deal structure discipline. These aren't F&I department issues, they're dealership-wide systems that require GM leadership.

Technology enablement through menu software, desking tools that show F&I payment impact, and reporting dashboards that track PVR in real-time creates visibility and accountability.

Ongoing tracking and accountability happen in daily F&I meetings reviewing yesterday's deals, weekly performance reviews comparing actuals to goals, and monthly deep dives into penetration rates by product and manager.

PVR improvement isn't a one-time project. It's a continuous discipline that separates elite dealerships from the rest.