Digital F&I Process - Remote & Hybrid Finance Office Solutions

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Consumer research consistently shows 60% of car buyers prefer completing F&I remotely rather than sitting in the finance office. They want convenience. They want speed. They want to complete paperwork from home in comfortable clothes, not in a dealership at 8 PM after three hours of negotiation.

But here's the challenge: F&I managers who master in-person menu presentation, relationship building, and objection handling often struggle to maintain penetration rates in remote environments. Average dealers see product penetration drop 15-25% when transitioning to digital F&I. Backend PVR falls. Commission checks shrink. And dealers wonder if digital convenience is worth the profit sacrifice.

It doesn't have to be this way. Top-performing digital F&I operations maintain, and sometimes exceed, in-store penetration rates. The difference? They don't simply move their in-person process to Zoom calls. They redesign F&I workflow specifically for digital environments, leverage technology effectively, prepare customers through pre-selling, and create engagement strategies that work remotely.

This guide provides the complete digital F&I framework covering implementation models, technology requirements, remote presentation strategies, compliance considerations, product penetration techniques, delivery coordination, and customer experience optimization.

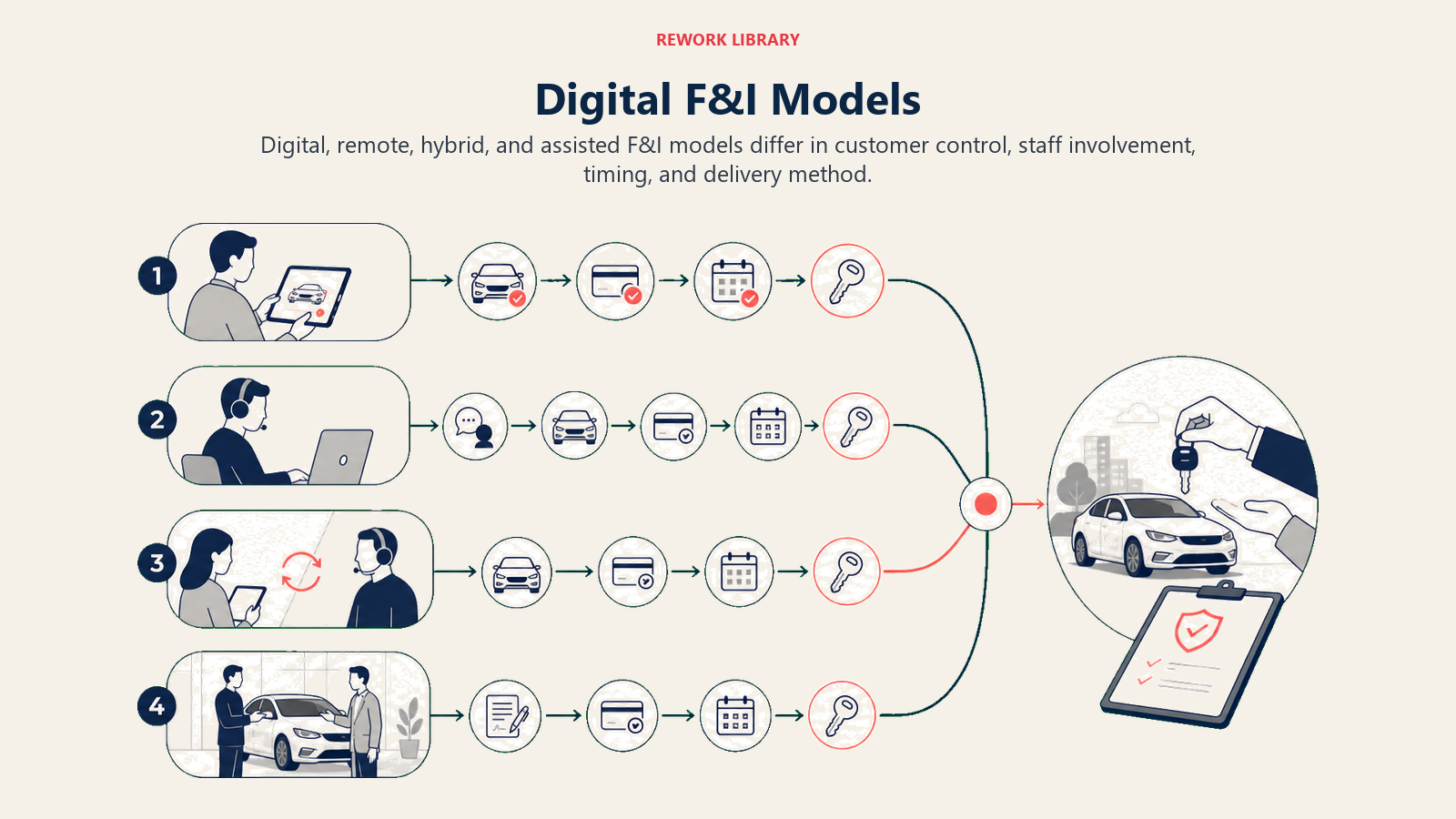

Digital F&I Models - Implementation Options

"Digital F&I" isn't one thing. Multiple models exist, each with different benefits, challenges, and customer experience implications.

Full Remote/At-Home F&I:

Customer completes entire F&I process from home via video call or digital menu. Never visits dealership for financing or product presentation. F&I manager conducts menu presentation remotely, processes documents electronically, and coordinates delivery separately.

Benefits:

- Maximum customer convenience

- Enables true home delivery

- Reduces dealership visit time to zero for F&I

- Appeals to busy professionals and reluctant showroom visitors

Challenges:

- Product penetration typically drops without preparation

- Requires robust technology platform

- Compliance verification more difficult

- Personal connection harder to establish

- "I'll think about it" increases

Best for: High-income customers, repeat buyers, referral customers, markets with long dealership drive times.

Hybrid (Menu Remote, Signature In-Store):

Customer reviews F&I menu and makes product selections remotely via digital platform. Then visits dealership briefly to sign documents, complete delivery, and take possession.

Benefits:

- Customer reviews menu at their own pace (reduces pressure perception)

- Shortens dealership visit time significantly

- F&I manager available for questions but customer controls timing

- Maintains some in-person touchpoint for relationship building

Challenges:

- Still requires dealership visit (not true home delivery)

- Time gap between menu review and signature creates "think about it" window

- F&I manager can't respond to objections in real-time during menu review

- Some customers complete menu review superficially

Best for: Customers valuing convenience but accepting dealership visit, transitions toward full remote, dealers testing digital F&I.

In-Store with Digital Tools:

Traditional in-person F&I office experience enhanced with digital menu presentation, e-signature, and streamlined document management. Customer sits with F&I manager but technology accelerates process.

Benefits:

- Maintains personal interaction and relationship building

- Digital tools speed up paperwork (no printing, manual signatures, scanning)

- F&I manager maintains full objection handling capability

- Easiest transition from traditional process

Challenges:

- Doesn't reduce dealership visit time significantly

- Misses customer convenience preference for remote process

- Requires F&I office space and scheduling

Best for: Traditional customers, complex credit situations, dealers prioritizing penetration over convenience, smooth digital transition.

Delivery with Mobile F&I:

F&I manager travels to customer location (home, office) with mobile technology to conduct menu presentation and complete documents on-site during delivery.

Benefits:

- Combines home delivery convenience with in-person presentation

- Maintains personal interaction for relationship building

- F&I manager controls presentation environment

- Premium service experience

Challenges:

- Requires mobile technology investment

- F&I manager time per deal increases significantly

- Scheduling complexity

- Manager travel time reduces daily deal capacity

- Works only in limited service radius

Best for: Luxury dealerships, high-transaction-value deals, VIP customers, dealerships differentiating through white-glove service.

Choosing the Right Model:

Selection depends on:

- Customer demographic: Tech-savvy millennials want full remote. Older customers prefer in-person.

- Market geography: Rural markets with 1-hour drive times benefit more from remote F&I than urban markets.

- Transaction type: Repeat buyers accept remote more than first-time buyers.

- Dealership brand positioning: Luxury brands should consider mobile F&I. Value brands focus on efficiency.

- F&I manager capability: Remote selling requires different skill set than in-person.

Many successful dealers offer multiple options: full remote for customers requesting it, hybrid as default, in-store for those preferring traditional experience.

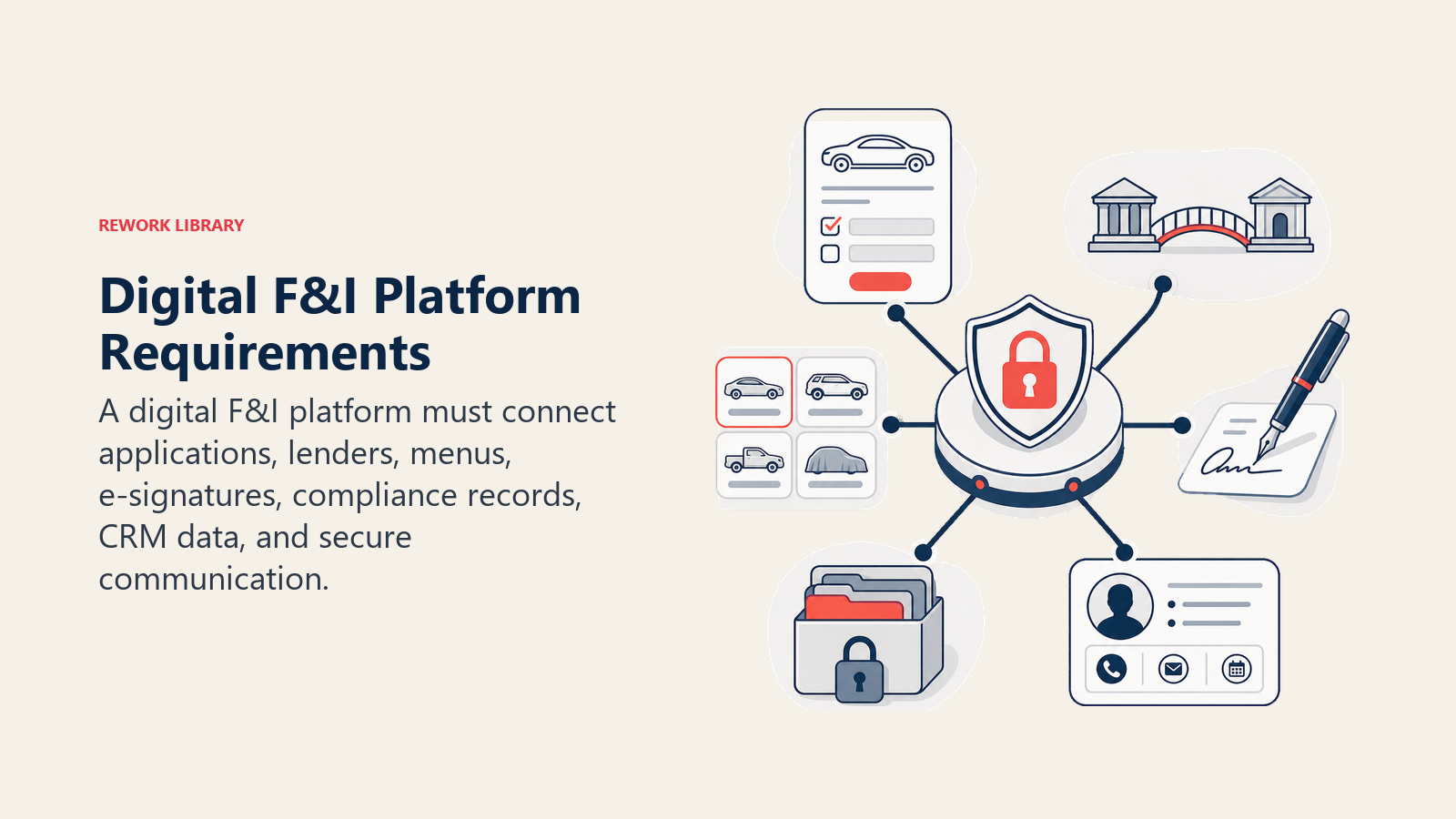

Technology Platform Requirements - Core Capabilities

Digital F&I effectiveness depends on technology. Poor platforms create frustration, compliance gaps, and product penetration loss. Robust platforms enable smooth workflow and strong performance.

Electronic Menu Presentation:

Digital menu software must provide:

- Visual product comparison (like in-person menus)

- Interactive selection (customer clicks products to add/remove)

- Real-time payment calculation as products are added

- Mobile-responsive design (works on phones, tablets, computers)

- Integration with DMS for accurate vehicle and pricing data

Platforms like RouteOne, DealerSocket, DealerTrack, F&I Express, Authenticom provide menu presentation capability. Evaluate user experience from customer perspective, confusing interfaces kill penetration.

E-Signature and Digital Contracting:

Electronic signature must satisfy ESIGN Act requirements:

- Customer consent to electronic process

- Identity authentication

- Tamper-evident contract storage

- Audit trail showing who signed what and when

- Ability to provide paper copies if requested

DocuSign, Adobe Sign, and automotive-specific platforms (RouteOne e-Contracting, etc.) handle this. Don't improvise e-signature processes with generic tools.

Lender Portal Integration:

Submit deals to lenders electronically, receive approvals, and transmit documents:

- Direct integration with major lenders (RouteOne, DealerTrack, etc.)

- Credit application pre-fill from DMS

- Real-time status updates

- Stip tracking and fulfillment

- Funding confirmation and wire transfer notification

Manual lender communication kills digital F&I efficiency. Integration is essential.

CRM and DMS Integration:

Digital F&I platforms should integrate with your dealership management system:

- Pull customer information (no duplicate data entry)

- Import deal structure from sales

- Update finance status in CRM for customer communication

- Push completed deal into DMS for accounting and registration

- Maintain single source of truth across systems

Disconnected systems create manual work, data errors, and customer frustration.

Video Conferencing Capability:

For remote FF&I presentationI presentation, you need reliable video:

- Zoom, Microsoft Teams, or Google Meet for general use

- Automotive-specific platforms with integrated video and menu

- Screen sharing for walking through menu together

- Recording capability for compliance documentation

- Mobile-friendly for customers without computers

Video quality matters. Dropped calls and choppy audio destroy presentation flow and customer confidence.

Document Management and Storage:

Store and retrieve documents efficiently:

- Electronic contract storage

- Compliance document archival

- Easy retrieval for lender requests or audits

- Secure access controls

- Backup and redundancy

Cloud-based document management (Box, Google Drive, automotive-specific platforms) enables remote access while maintaining security.

Remote Menu Presentation - Virtual Selling Strategies

Conducting effective F&I menu presentations remotely requires different techniques than in-person. What works face-to-face doesn't always translate to video calls.

Video Call vs. Screen Sharing:

Two primary approaches:

Video call with live interaction: F&I manager and customer both visible on camera, having conversation while manager shares screen showing menu. This maintains personal connection and allows manager to read body language and engagement.

Screen sharing with voice: Manager shares screen and walks through menu while talking (video off or minimized). This focuses customer attention on menu but loses personal connection.

Best practice: Start with video to build rapport, then shift to screen sharing for menu presentation while maintaining small video thumbnail. This balances personal connection with focused menu review.

Maintaining Engagement Remotely:

Remote presentations face engagement challenges:

- Customer distractions (kids, pets, other people)

- Multitasking (customer checking phone, email during call)

- Technical difficulties reducing focus

- Lack of physical presence allowing mental checkout

Maintain engagement:

- Confirm environment: "Are you in a quiet place where we can focus for 15-20 minutes?"

- Interactive questions: Don't lecture. Ask questions frequently. "How long are you planning to keep this vehicle?"

- Pause for responses: Let customer talk. Don't fill silence with more talking.

- Name usage: Use customer's name throughout conversation.

- Energy level: Bring higher energy than in-person. Video flattens affect, requiring compensation.

Product Demonstration Techniques:

Without physical presence, product demonstration requires creativity:

- Share warranty examples: Screen share service RO showing expensive repair. "This $4,200 transmission repair is exactly what VSC would cover."

- Use vehicle photos: Show customer's specific vehicle, highlighting features protected by coverage.

- Calculation tools: Live calculate GAP exposure showing actual numbers for their deal.

- Video content: Short product explanation videos (30-60 seconds) demonstrating coverage value.

Visual demonstration beats verbal explanation in remote settings where attention is fragile.

Handling Technical Difficulties:

Technology fails. Plan ahead:

- Test customer connection: Start call 5 minutes early to troubleshoot.

- Backup communication: Get customer's phone number before video call in case you need to pivot to phone.

- Simplified access: Use simple join links (Zoom meeting ID, etc.), not complex software installations.

- Support availability: Have someone available to help customers with technical issues.

- Patience and flexibility: If video won't work, shift to voice call with emailed menu review.

Technical frustration kills deal engagement. Handle it smoothly.

Time Management in Remote Environment:

Remote F&I takes longer than in-person due to:

- Technical setup time

- Reduced ability to "control" pace

- Customer distractions requiring refocus

- Explanation time without visual cues

Budget 30-40 minutes for remote F&I vs. 20-30 minutes in-person. Don't rush. Rushing increases resistance and decreases penetration.

Compliance in Digital Environment - Meeting Requirements

Digital F&I must satisfy identical compliance requirements as in-person transactions. Remote delivery doesn't create compliance exceptions.

E-Signature Legal Validity (ESIGN Act):

ESIGN Act establishes electronic signatures as legally equivalent to handwritten signatures when:

- Customer consents to electronic process

- System provides electronic record copy

- Signatures are attributable to specific person

- Records are accurate and accessible

Use compliant e-signature platforms. Don't email PDFs and accept email reply as "signature."

Product Disclosure Verification:

Ensure customer actually reads disclosures:

- Require clicking "I have read and understand" checkboxes

- Use attestation language: "I acknowledge these products are optional"

- Record video call where you verbally explain key disclosures

- Send disclosure documents separately for review before signing

- Confirm verbally during call: "Do you understand these products are optional?"

"Customer didn't read it" won't defend against complaints. Build verification into process.

Voluntary Purchase Confirmation:

Remote environment creates higher risk of customer claiming pressure or misunderstanding. Document voluntary nature explicitly:

- Written attestation: "I voluntarily choose to purchase these products"

- Verbal confirmation during call: "You're choosing to add these products, correct?"

- Clear opt-out process: "You can remove any of these products before finalizing"

- Recording preservation showing customer understanding

Over-document voluntary nature in remote transactions.

Identity Verification (Red Flags):

Identity theft risk increases in remote transactions. Strengthen verification:

- Government-issued ID photo upload and verification

- Video call visual verification of customer

- Credit report information cross-check against application

- Confirmation call to phone number on credit application

- Address verification against credit bureau data

Don't skip identity verification because it's "inconvenient" remotely. Fraud losses exceed convenience costs.

Adverse Action Delivery:

Electronic adverse action notice delivery satisfies FCRA when:

- Customer consents to electronic delivery

- Email delivery confirmation received

- Physical mailing if electronic delivery fails

- Content identical to paper adverse action notice

Track delivery confirmation. If customer doesn't receive email, physical mail is required.

Record Retention for Digital Documents:

Same retention requirements apply: 7+ years. Ensure:

- Cloud storage with redundancy and backup

- Organized filing system for electronic records

- Audit trail showing document creation, signing, and storage

- Access controls limiting who can view customer data

- Regular backup verification

Digital records are easier to lose than paper if backup systems fail. Test your disaster recovery.

Finance Application and Approval - Remote Processing

Credit application and lender approval processes adapt to remote environment.

Digital Credit Application:

Customer completes credit application electronically:

- Web form or mobile app input

- Auto-fill from DMS where available

- Required field validation (prevents incomplete applications)

- Privacy notice presentation and acknowledgment

- Electronic signature on completed application

Pre-fill applications when possible. Every field customer must manually complete reduces completion rate.

Income and Identity Verification:

Lenders require verification documentation:

- Pay stubs (photo upload or PDF)

- Bank statements (PDF download)

- Driver's license (photo both sides)

- Proof of insurance

- Residence verification (utility bill, lease, etc.)

Enable easy upload via mobile app or email. Complicated document submission kills deal momentum.

Lender Submission and Approval:

Submit to multiple lenders through integrated platform:

- RouteOne, DealerTrack, or direct lender portals

- Parallel submission to multiple sources

- Real-time status tracking

- Automated stip requests sent to customer

- Approval notification via email/text

Keep customer informed throughout process. Silence creates anxiety and deal-killing doubt.

Rate Shop and Approval Communication:

When multiple approvals are received, communicate options clearly:

- Email summary showing rate, term, payment for each option

- Video call to discuss options if customer prefers

- Clear recommendation with justification

- Selection deadline (avoiding indefinite "I'll think about it")

Don't surprise customers with rates or terms significantly different from expectations set earlier.

Stip Collection and Processing:

Stipulations (additional documentation requirements) slow deals. Streamline collection:

- Text message with direct upload link

- Clear explanation of what's needed and why

- Deadline for submission

- Follow-up if customer doesn't respond within 24 hours

- Re-submit to lender immediately upon receipt

Stip delays kill deals. Aggressive follow-up maintains momentum.

Product Penetration Challenges - Maintaining PVR

Digital F&I environments create penetration challenges. Anticipate and address them systematically.

Engagement Difficulty in Remote Setting:

Customer attention is divided remotely. They're home, comfortable, and easily distracted. Counter this:

- Schedule dedicated time: "I'll call at 6 PM when you're available to focus for 20 minutes."

- Request distraction-free environment: "Can you find a quiet spot without interruptions?"

- Engage actively: Ask questions frequently, don't monologue.

- Use visuals: Share screen with compelling images, not walls of text.

Passive presentation fails remotely. Active engagement succeeds.

"I'll Think About It" Increase:

Remote customers can defer decisions easily. In-person presence creates natural decision point. Remote calls? Customer can end call and "think about it" indefinitely.

Counter this:

- Create urgency: "Coverage must be added before first payment. Once the loan starts, we can't modify it."

- Time-limit offers: "This pricing is locked in today. Tomorrow I'll need to re-quote."

- Immediate decision request: "Let's make a decision today while we're reviewing everything together."

- Show opportunity cost: "Waiting to decide means delaying delivery. Let's finalize so you can take possession tomorrow."

Don't accept "I'll think about it" without attempt to close.

Product Value Demonstration Limitations:

In-person, you can show service ROs, flip through VSC contracts, demonstrate coverage benefits physically. Remotely, everything is verbal or screen-shared documents. Less tangible feels less valuable.

Compensate:

- Specific examples with numbers: "Last week a customer had $3,800 transmission repair covered by VSC."

- Show actual documents: Screen share service invoices, coverage contracts, claim examples.

- Use customer's vehicle: "Your specific model has known issues with X component. Coverage addresses this directly."

- Payment focus: Make abstract coverage tangible through minimal monthly payment impact.

Remote value demonstration requires extra preparation and compelling evidence.

Strategies to Maintain Penetration:

Tactical approaches to preserve product sales:

- Package presentation: Show complete protection package as default, not individual products.

- Pre-selling by sales: Sales staff introduces F&I products during vehicle presentation.

- Default opt-out framing: "Your package includes these protections. Do you want to remove any?"

- Multiple touchpoints: Email menu before call so customer reviews in advance.

- Persistent follow-up: If customer defers decision, follow up daily until closed or rejected.

Pre-Selling Importance Increases:

In-person F&I managers can overcome lack of pre-selling. Remote F&I managers can't. Pre-selling becomes essential:

Sales staff language: "Your service coverage is included for five years, so you won't have any repair costs. That's already factored into the deal."

Customer arrives at F&I expecting coverage, not hearing about it for the first time. Acceptance increases dramatically.

Deal Delivery Options - Completing the Transaction

Digital F&I separates financing from physical delivery. Multiple delivery models exist.

At-Home Delivery with Signatures:

Vehicle delivered to customer location with F&I documents signed during delivery:

- Driver delivers vehicle

- Brings printed documents requiring physical signature (if any remain)

- Collects down payment, trade-in, keys

- Provides delivery orientation

Works best when e-signature handles most documents and only 1-2 require physical signature.

Customer Pick-Up After Remote F&I:

Customer completes F&I remotely, then visits dealership briefly to pick up vehicle:

- F&I completed in advance (all signatures electronic)

- Pick-up visit is 10-15 minutes (keys, orientation, leave)

- No waiting in dealership

- No prolonged F&I office time

This hybrid approach provides convenience while maintaining some in-person touchpoint.

Mobile Notary for State Requirements:

Some states require notarized signatures on specific documents. Mobile notary enables home delivery:

- Schedule mobile notary to customer location

- Notary witnesses required signatures

- Dealership pays notary fee ($75-$150 typically)

- Enables complete remote transaction in notary-required states

Cost is easily absorbed in deal structure or charged as delivery fee.

Trade-In Pick-Up Coordination:

When customer has trade-in but delivery is remote:

- Option 1: Customer drives trade to dealership during pick-up

- Option 2: Dealership picks up trade from customer location

- Option 3: Customer keeps trade until first payment due (if payoff not critical)

Option 2 (dealership pick-up) provides best customer experience but requires logistics coordination.

Payment Collection Methods:

Collect down payment and fees remotely:

- ACH transfer: Customer initiates bank transfer (free, 2-3 day delay)

- Wire transfer: Customer sends wire (immediate, $25-$50 fee)

- Credit card processing: Customer pays via secure payment link (immediate, 2-3% fee)

- Check by mail: Traditional but slow

- Physical check during delivery: Simplest for home delivery

Provide multiple options matching customer preference and timeline urgency.

Customer Experience Optimization - Digital Satisfaction

Digital F&I customer satisfaction determines referrals, reviews, and repeat business.

Scheduling Convenience:

Offer flexible scheduling:

- Evening availability (6-9 PM after work)

- Weekend options

- 24-hour advance notice minimum (customer can schedule online)

- Confirmation reminders (text/email)

Customers choose digital F&I for convenience. Inconvenient scheduling defeats the purpose.

Process Transparency and Expectations:

Set clear expectations upfront:

- How long will F&I call take? (30 minutes)

- What documents will be needed? (license, insurance, pay stub)

- What decisions will be made? (product selection, finalization)

- When will delivery occur? (24-48 hours after completion)

Mystery creates anxiety. Transparency creates confidence.

Technical Support Availability:

Provide easy access to help:

- Pre-call tech check (test video, audio, connection)

- Help phone number if customer has trouble joining call

- IT support for platform issues

- Patience when things don't work smoothly

Technical frustration destroys experience. Smooth support recovers situations.

Personal Touch Maintenance:

Don't let digital process feel impersonal:

- Use customer's name frequently

- Reference previous conversations or relationship history

- Show enthusiasm about their vehicle choice

- Personalize recommendations to their situation

- Follow up after delivery asking about experience

Technology enables efficiency. Personal interaction creates loyalty.

Follow-Up and Support:

Post-delivery contact ensures satisfaction:

- Email day after delivery confirming satisfaction

- Phone call at one week checking in

- Provide direct contact for questions or concerns

- Service appointment reminder

- Request Google review if experience was positive

Follow-up differentiates great dealerships from mediocre ones.

Implementation Roadmap - Transitioning to Digital

Moving from traditional F&I to digital requires systematic approach.

Technology Platform Selection:

Evaluate platforms on:

- Customer user experience (test from customer perspective)

- Integration with your DMS and lender network

- Compliance features and audit trail

- Cost structure (monthly fee, per-transaction, etc.)

- Training and support provided by vendor

- References from similar dealerships

Don't choose based on price alone. Poor platform creates customer frustration and penetration loss costing far more than premium platform fees.

Process Design and Workflow:

Map out complete digital F&I workflow:

- How does customer enter process? (BDC schedules call, customer self-schedules, etc.)

- What happens between deal structure and F&I call?

- How is menu presented and products explained?

- What documents require signature and in what sequence?

- How is delivery coordinated?

- What follow-up occurs post-delivery?

Document every step. Undefined processes create confusion and mistakes.

Staff Training and Change Management:

F&I managers need training on:

- Platform technology usage

- Remote presentation techniques

- Video call best practices

- E-signature and compliance in digital environment

- Customer objection handling remotely

- Troubleshooting technical issues

Minimum 20 hours platform training plus role-playing remote scenarios before going live.

Change management matters: some F&I managers resist digital process because they fear penetration loss and commission decline. Address concerns, provide support, and reward early adopters.

Pilot Program and Iteration:

Don't launch full digital F&I across entire dealership immediately. Run pilot:

- Start with one F&I manager (choose digitally-comfortable person)

- Offer digital option to select customers (tech-savvy, repeat buyers)

- Run 25-50 deals through process

- Collect customer feedback

- Identify friction points and process gaps

- Refine workflow based on learning

- Expand gradually once process is smooth

Pilot prevents disasters and identifies issues before full rollout.

Measuring Success Metrics:

Track performance compared to traditional F&I:

- Product penetration rate by product

- Backend PVR per unit

- Customer satisfaction scores

- Time from deal to delivery

- Deal fall-out rate during F&I process

- Technology issue frequency

If digital F&I shows significantly worse performance, diagnose why and address root causes (training, technology, process design).

Digital F&I Implementation Checklist

Model Selection:

- Customer demographic and preferences analyzed

- Market geography considerations evaluated

- Digital F&I model chosen (full remote, hybrid, mobile, enhanced in-store)

- Fallback options defined for customers preferring alternatives

Technology Platform:

- Platform selection based on user experience, integration, compliance

- DMS and lender portal integration confirmed

- E-signature capability verified ESIGN Act compliant

- Video conferencing solution selected

- Document management system established

- Mobile functionality tested

Remote Presentation Capability:

- F&I managers trained on video call engagement

- Screen sharing and menu presentation practiced

- Product demonstration materials prepared (ROs, examples, calculations)

- Technical difficulty protocols established

- Pre-call customer tech check process defined

Compliance Verification:

- E-signature compliance confirmed

- Product disclosure delivery verified

- Voluntary purchase confirmation documented

- Identity verification strengthened for remote

- Adverse action electronic delivery enabled

- Digital record retention system implemented

Product Penetration Strategy:

- Pre-selling approach coordinated with sales team

- Package presentation designed for digital menu

- Value demonstration materials created

- Objection response scripts adapted for remote

- Urgency creation techniques identified

- Follow-up persistence process defined

Delivery Coordination:

- Home delivery logistics established (if offering)

- Pick-up process streamlined

- Mobile notary service identified (if required)

- Trade-in pick-up options defined

- Payment collection methods enabled

Customer Experience Elements:

- Flexible scheduling system implemented

- Process expectations communication created

- Technical support availability established

- Personal touch techniques trained

- Post-delivery follow-up automated

Pilot and Launch:

- One F&I manager selected for pilot

- Customer selection criteria for pilot defined

- 25-50 deal pilot target set

- Customer feedback collection planned

- Performance metrics tracking established

- Iteration process before full rollout defined

Digital F&I represents the future of automotive finance operations. Consumer preference for remote convenience isn't reversing. The question isn't whether to offer digital F&I, but how to implement it effectively without destroying backend profitability.

The answer lies in strategic approach: choose the right model for your market, invest in robust technology, train staff thoroughly on remote presentation techniques, strengthen compliance verification, pre-sell aggressively, maintain engagement during remote calls, and optimize customer experience relentlessly.

Dealers who nail digital F&I gain competitive advantage. They offer convenience customers demand while maintaining, and sometimes improving, product penetration rates. They expand their geographic reach (no longer limited to customers willing to visit showroom). They reduce dealership facility costs. And they build reputation as modern, customer-focused operations.

Dealers who ignore digital F&I or implement it poorly? They watch market share erode to competitors offering better customer experience. Their F&I PVR drops as cherry-picking customers choose minimal coverage online. And they earn reputation as old-school operations resistant to customer preference.

The choice is clear. Implement digital F&I strategically, measure performance rigorously, iterate based on learning, and deliver both convenience and profitability. That's the path forward in modern automotive retail.

External Resources

- Cox Automotive Digital F&I Transformation 2026 - Latest innovations in digital finance and remote F&I processes

- Dealertrack F&I Solutions - Industry-leading digital F&I platform capabilities

- Cox Automotive: Transforming F&I for eCommerce - Strategic guidance on digital F&I implementation

- Top Automotive Retail Trends 2026 - Cox Automotive - Industry trends including digital finance adoption

Senior Implementation Consultant

On this page

- Digital F&I Models - Implementation Options

- Technology Platform Requirements - Core Capabilities

- Remote Menu Presentation - Virtual Selling Strategies

- Compliance in Digital Environment - Meeting Requirements

- Finance Application and Approval - Remote Processing

- Product Penetration Challenges - Maintaining PVR

- Deal Delivery Options - Completing the Transaction

- Customer Experience Optimization - Digital Satisfaction

- Implementation Roadmap - Transitioning to Digital

- Digital F&I Implementation Checklist

- External Resources