Service Line Strategy: Building a Profitable Professional Services Portfolio

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Seventy percent of professional services firms report having at least one service line that fails to generate acceptable returns. Partners champion services based on personal expertise rather than market demand. Firms add capabilities opportunistically when clients request them, then struggle to build repeatable offerings. Resources spread across too many services, preventing the depth required for true differentiation. The result: service portfolios that look comprehensive on paper but deliver mediocre profitability and weak competitive positioning.

Successful firms treat service lines as strategic portfolio assets requiring deliberate development, rigorous performance management, and disciplined investment allocation. They make data-driven decisions about which services to grow, maintain, or sunset. They understand the economics of each service line and allocate resources accordingly. They build specialized capabilities that create real competitive advantages rather than claiming generic expertise across every possible service.

Service line strategy transforms professional services firms from generalists competing on relationships into specialists competing on demonstrable capability. This allows premium pricing and higher margins while building sustainable market positions.

Understanding Service Line Architecture

Service line strategy begins with clear definitions that many firms lack. Service lines represent major capability areas that address distinct client problems, typically aligned with specific industries, functional areas, or business challenges. Strategy consulting, technology implementation, organizational transformation: these represent service lines with separate market positioning, delivery methodologies, and economic profiles. Service offerings nest within service lines as specific solutions or delivery approaches. A strategy consulting service line might include offerings like market entry strategy, M&A advisory, digital transformation strategy, or operational improvement. These offerings share common methodologies, talent profiles, and go-to-market approaches while addressing different client situations.

The distinction matters because firms manage service lines and service offerings differently. Service line decisions involve portfolio-level strategy: market positioning, capability investment, talent development, and resource allocation. Service offering decisions focus on solution design, pricing models, delivery efficiency, and client targeting within established service line capabilities.

Portfolio architecture organizes these elements into coherent structures. Some firms organize by industry verticals (healthcare services, financial services, technology sector) with functional offerings within each vertical. Others structure by functional horizontals (finance transformation, operations excellence, technology) serving multiple industries. Matrix approaches combine both dimensions, though implementation complexity increases substantially.

The architectural choice depends on how clients buy services, where competitive differentiation exists, and how talent develops expertise most effectively. Industry-focused architectures work when sector expertise drives buying decisions and regulatory or operational requirements vary substantially by industry. Functional architectures succeed when methodology and process expertise matter more than industry context.

Understanding overall professional services business models provides context for service line portfolio decisions within firm strategy.

Most firms evolve through architectural stages as they grow. Small firms start with founder expertise driving opportunistic service additions. Mid-size firms formalize service lines around proven capabilities. Large firms develop sophisticated portfolio management balancing industry and functional dimensions. Your architecture should reflect current market position and organizational capability, not aspirational complexity.

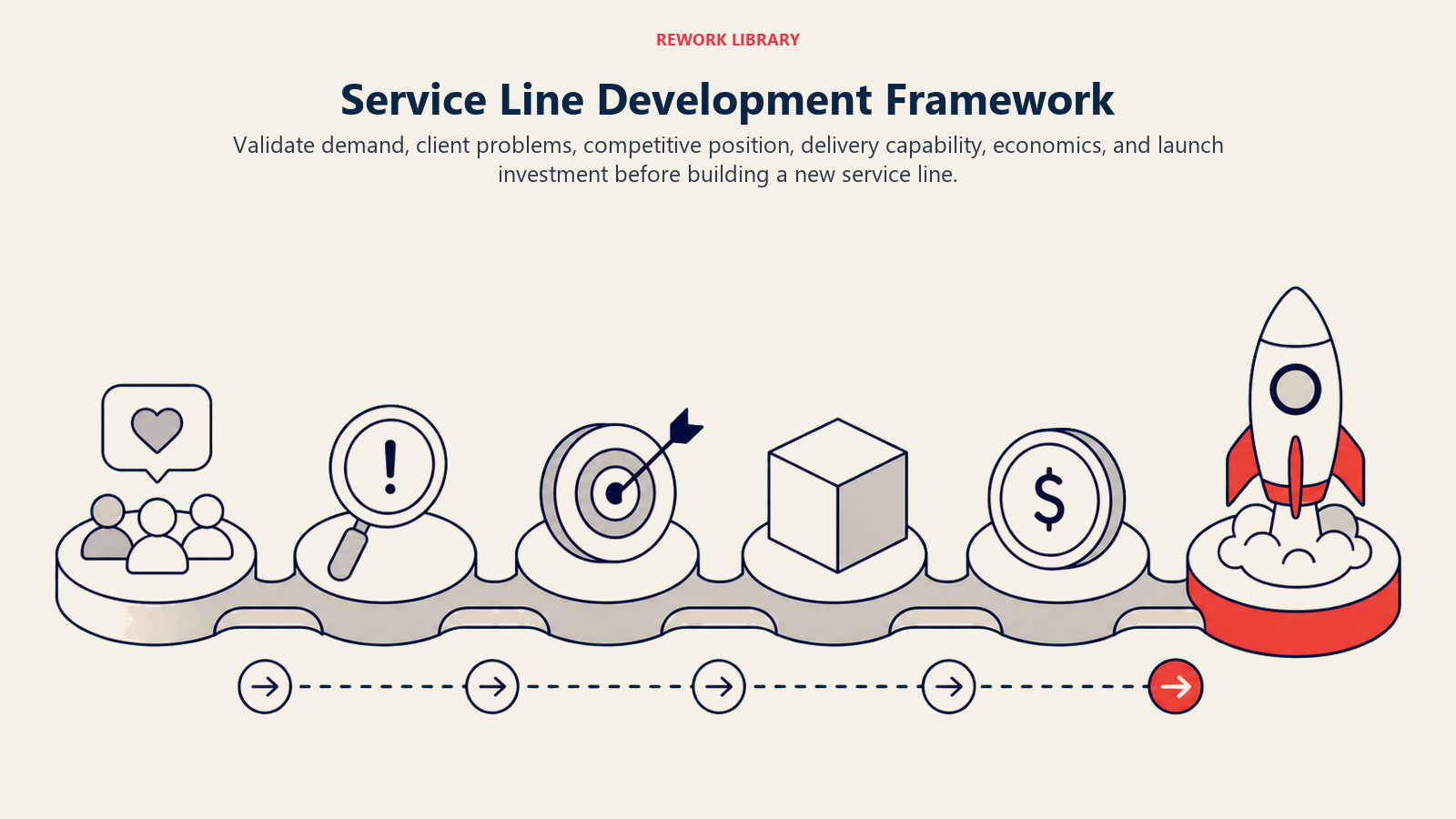

Service Line Development Framework

Developing new service lines requires systematic evaluation rather than opportunistic expansion. Market demand assessment examines whether sufficient client need exists to support dedicated service line investment. This goes beyond "clients are asking for this" to analyzing total addressable market size, growth trajectory, buying patterns, typical project sizes, and competitive intensity. Quantitative demand signals include frequency of client requests for specific capabilities, size of contracts competitors win in this space, industry analyst reports sizing market segments, and job posting trends indicating talent demand. Qualitative signals emerge from client interviews exploring unmet needs, win-loss analysis showing capability gaps, and partnership discussions revealing adjacent opportunities. Capability gap analysis compares current firm capabilities against requirements for credible market entry. Technology implementation services require different talent profiles, delivery methodologies, partnership ecosystems, and intellectual property than strategic advisory. Honest capability assessment prevents firms from pursuing opportunities where they lack foundation for competitive differentiation.

Gap analysis examines technical skills availability within current workforce, methodology and IP development required, technology platform or tools needed, industry credentials or certifications necessary, and reference clients in target segment. Large gaps don't necessarily prevent entry but require realistic investment planning and timeline expectations.

Investment requirements translate capability gaps into resource commitments. New service lines typically require 18-24 months before generating acceptable returns. Initial investments include hiring specialized talent, developing methodologies and IP, creating marketing materials and case studies, training delivery teams, and funding pilot projects at reduced margins to build experience.

Most firms underestimate total investment by focusing only on direct hiring costs while ignoring opportunity costs of partner time, business development expenses, and margin dilution during the ramp period. Realistic investment models project cash requirements and timeline to profitability, preventing premature abandonment when services don't generate immediate returns. Tracking these investments through professional services metrics ensures accountability.

Pilot and validation approaches test service line viability before full-scale investment. Controlled pilots with friendly clients validate delivery capability and refine offerings. Limited market tests assess demand and pricing sensitivity. Partnership arrangements provide interim capabilities while building internal expertise. These staged approaches reduce risk while generating learning that informs scaling decisions.

Connecting service line development to capability development strategies ensures firms build sustainable competitive advantages rather than superficial capabilities.

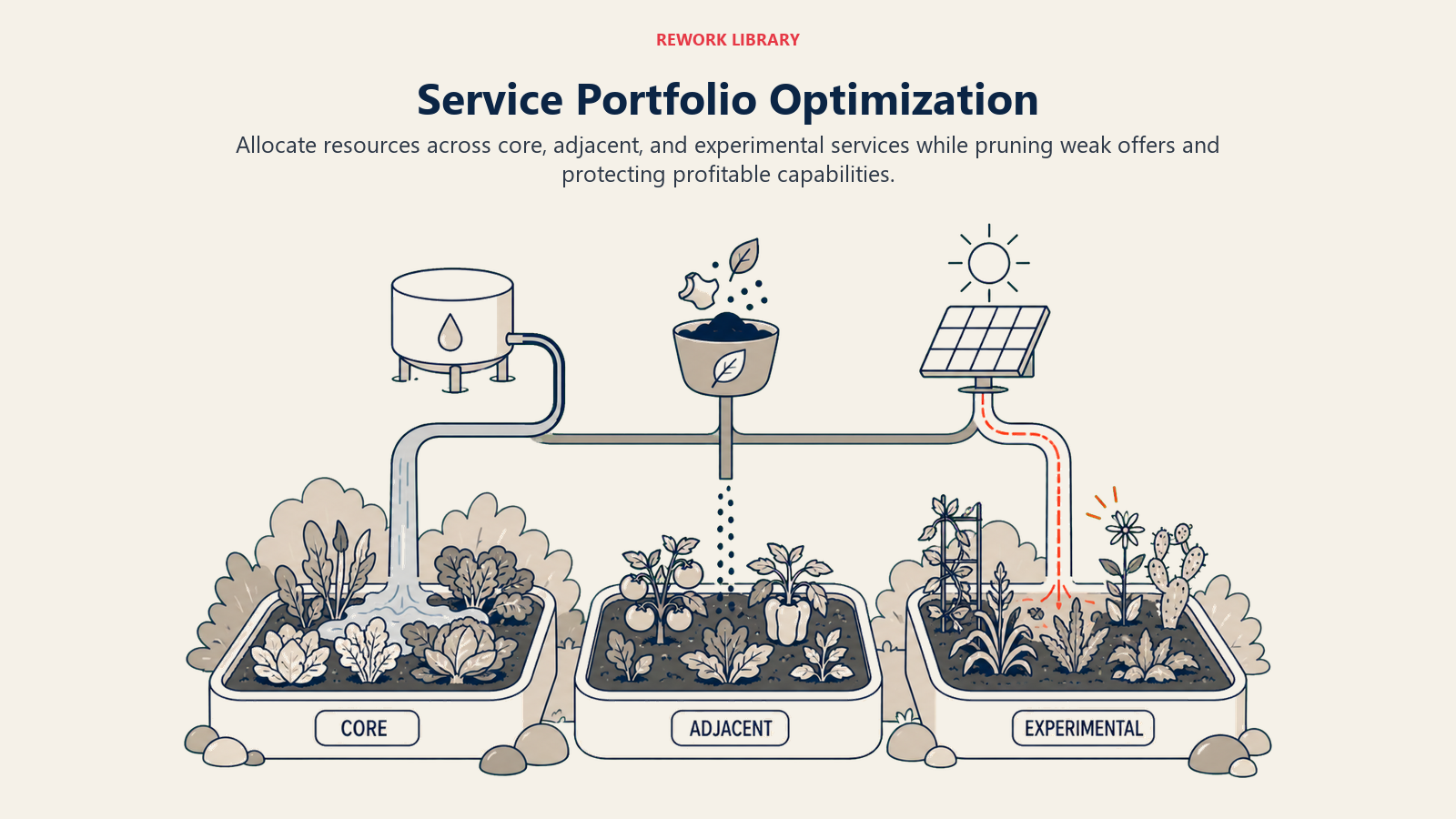

Portfolio Optimization Principles

Service line portfolios require active management to maintain health and profitability. The 70-20-10 rule provides a framework for balanced portfolio allocation: 70% of resources should support core services generating current revenue and profit, 20% should develop growth services with proven demand but requiring capability building, and 10% should explore emerging services testing new market opportunities. Firms violating this balance in either direction create problems. Conservative portfolios overweighting core services miss market evolution and competitive threats. Aggressive portfolios overweighting growth and emerging services undermine profitability and execution quality. The exact ratios vary by firm strategy and market position, but the principle of balanced investment across portfolio lifecycle stages remains constant. Core services form the revenue and margin foundation. These services demonstrate strong client demand with healthy pipeline, proven delivery capability with repeatable methodologies, talent depth that allows scale, and acceptable margins with clear path to premium pricing. Core services deserve continued investment to maintain competitiveness, but disproportionate resource allocation to mature services indicates portfolio stagnation.

Growth services represent expansion opportunities with momentum but incomplete development. Characteristics include demonstrated client interest with initial projects completed, capability gaps being actively addressed through hiring or partnerships, competitive positioning showing potential differentiation, and investment required to scale delivery and go-to-market. Growth services become core services or get relegated to emerging status based on performance over 12-18 month evaluation periods.

Emerging services test new opportunities with high uncertainty. These experimental services explore adjacent markets, new delivery models, or innovative solutions. Most emerging services fail to achieve scale, but successful ones provide future growth engines. Firms should pursue emerging services, but limited investment and clear success criteria prevent resource drain on unproven concepts.

Profitability analysis by service line reveals performance variation hidden in firm-wide averages. Contribution margin analysis allocating direct costs to service lines shows which services subsidize others. Firms commonly discover their largest service line by revenue ranks middle-of-pack on profitability, while smaller specialized services generate superior margins.

Understanding revenue streams in professional services helps optimize portfolio mix and pricing across service lines.

This analysis should include direct labor costs including utilization assumptions, direct project costs for delivery, allocated overhead based on reasonable driver metrics, and business development costs by service line. Activity-based costing provides more accurate profitability pictures than simple revenue allocation.

Sunset criteria establish standards for eliminating underperforming services. Clear criteria prevent emotional attachment to services draining resources without generating returns. Sunset triggers typically include consistent underperformance against margin targets for 18+ months, declining client demand with shrinking pipeline, inability to attract or retain qualified talent, or strategic misalignment with firm direction.

Client transition planning and timeline transparency preserve relationships during service discontinuation. Firms should provide adequate notice, recommend alternative providers when appropriate, and complete in-flight projects professionally. Poor sunset execution damages client relationships and firm reputation beyond the discontinued service.

Market Positioning Strategy

Service line positioning determines competitive basis and influences every aspect of go-to-market strategy. Horizontal positioning positions services across multiple industries based on functional expertise: finance transformation serves healthcare, manufacturing, retail equally. This approach maximizes addressable market and talent utilization but faces intense competition from other horizontal providers. Vertical positioning concentrates on industry-specific expertise. Healthcare consulting serves only healthcare organizations. This specialization creates deep domain knowledge, industry-specific methodologies, and stronger client relationships, but limits addressable market and creates talent development constraints within narrow expertise domains. The horizontal-vertical decision involves fundamental tradeoffs. Horizontal approaches scale more easily, support broader talent deployment, and avoid industry cycle exposure. Vertical approaches command premium pricing, generate stronger client loyalty, and create defensible competitive positions. Most large firms pursue hybrid models with some horizontal platforms and selected vertical specializations.

Specialization depth versus breadth creates a second positioning dimension. Deep specialists focus intensely on narrow problem domains (post-merger integration, supply chain optimization, cloud migration) building exceptional expertise within limited scope. Broad generalists cover wide capability ranges with less depth in any specific area.

Deep specialization allows premium pricing based on expertise, accelerated delivery through repeatable methodologies, lower risk profiles from proven approaches, and strong competitive differentiation. However, market size limits growth potential, talent development narrows, and demand fluctuations create utilization challenges.

Broad positioning provides larger addressable markets, flexibility in talent deployment, resilience against demand shifts, and relationship expansion within existing clients. But it also means intense competition from other generalists, difficulty demonstrating differentiation, pressure on pricing, and challenge building deep expertise.

Competitive differentiation factors determine positioning sustainability. Methodology differentiation based on proprietary approaches, frameworks, or tools creates defendable advantages when truly distinctive. Many firms claim unique methodologies that differ only cosmetically from standard approaches. Clients recognize this quickly.

Technology differentiation using proprietary platforms, data analytics capabilities, or implementation tools works when technology provides measurable value. Simply using common tools doesn't differentiate. Industry credentials including certifications, partnerships, or regulatory expertise create barriers in regulated industries but offer less protection in others.

Connecting positioning decisions to pricing strategies ensures market positioning supports desired pricing and margin objectives.

Talent brand as employer of choice for specialized expertise attracts better practitioners, allowing superior delivery that reinforces market position. This virtuous cycle (specialized positioning attracts specialized talent, which drives differentiated delivery, creating stronger market position) builds sustainable competitive advantage over time.

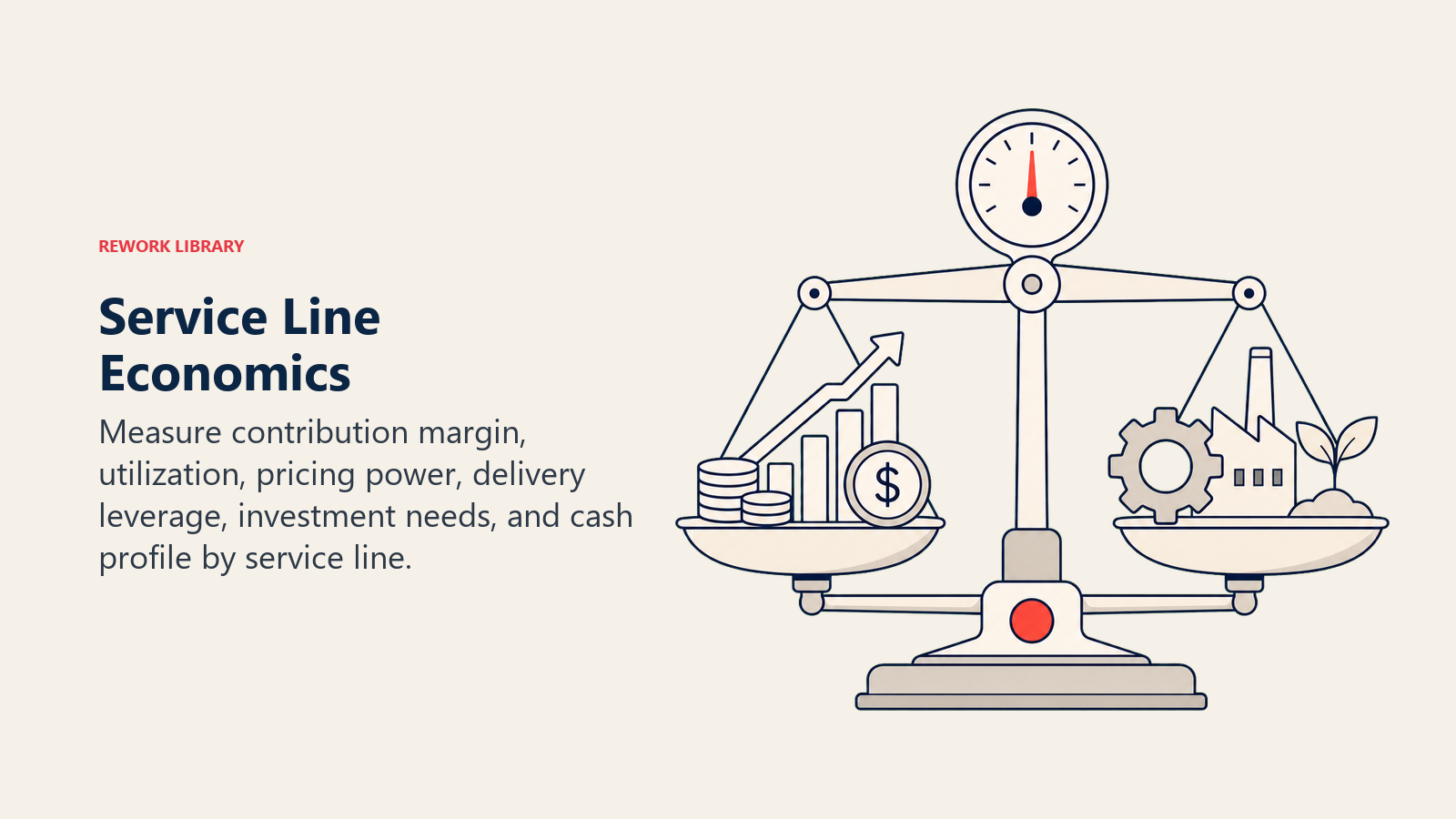

Service Line Economics

Understanding service line economics supports data-driven portfolio decisions and performance management. Contribution margin analysis allocates revenue and costs to service lines, revealing profitability variation. Standard analysis includes revenue from projects, direct labor costs based on actual utilization, project delivery costs, and allocated overhead using reasonable drivers. Utilization patterns vary substantially by service line based on delivery model, project duration, and talent seniority. Implementation services often achieve 70-80% billable utilization through longer-term staffing. Strategy consulting typically runs 50-60% billable given shorter engagements, business development intensity, and knowledge development requirements. Target utilization rates should reflect service line characteristics rather than firm-wide averages. Services requiring significant IP development, intensive business development, or senior practitioner involvement justify lower targets. High-volume implementation services demand higher utilization to achieve margin objectives. Mismatched targets create either quality problems from over-utilization or profitability issues from under-utilization. Understanding utilization and capacity planning at the service line level is essential.

Price positioning strategy determines where services price relative to market alternatives. Premium positioning requires demonstrable differentiation through specialized expertise, proven methodologies reducing client risk, superior talent, proprietary tools or IP, or industry credentials. Without real differentiation, premium pricing fails in competitive processes.

Market positioning prices at prevailing rates, competing on relationship strength, execution quality, cultural fit, or convenience factors. This positioning works for firms with strong client relationships or execution reputations but limited differentiating capabilities. Margins depend on operational efficiency rather than pricing power. Understanding billable hour vs value-based pricing tradeoffs informs this positioning choice.

Value positioning prices below market to capture share through newer service lines building market presence, volume-oriented growth strategies, or competitive displacement approaches. Temporary value positioning during service line establishment makes sense, but sustained below-market pricing indicates lack of competitive differentiation requiring strategic adjustment.

Cross-sell and upsell potential varies by service line based on natural client relationship expansion paths. Diagnostic services create opportunities for implementation projects. Implementation projects reveal additional opportunities. Advisory relationships expose broader organizational challenges. Service lines that support expansion should factor downstream revenue into economic analysis.

Understanding cross-sell strategy and upsell approaches maximizes multi-service relationship value.

Client economics by service line (acquisition cost, average project size, relationship duration, and expansion rates) inform portfolio investment decisions. Services with high acquisition costs need larger project values or strong expansion potential to generate acceptable returns. Services with efficient acquisition should capture appropriate credit in portfolio analysis even if individual project margins appear lower. Developing a client qualification framework ensures you pursue the right opportunities within each service line.

Capability Building for Service Lines

Service line capabilities extend beyond individual consultant expertise to organizational assets supporting scalable delivery. Skills development creates talent pools with required technical expertise, industry knowledge, and delivery experience. This involves hiring experienced practitioners, developing training programs building specific capabilities, creating career paths encouraging specialization, and maintaining communities of practice sharing knowledge. Firms underinvest in structured skill development, relying on on-the-job learning that produces inconsistent results. Systematic capability building accelerates talent development, reduces delivery risk, and produces quality consistency that differentiates firms in client perception. A formal talent development program makes this systematic rather than accidental.

Intellectual property development transforms individual expertise into organizational assets through documented methodologies describing proven approaches, frameworks organizing thinking about common challenges, tools automating analysis or delivery components, templates accelerating common deliverable production, and case studies demonstrating successful applications.

Well-developed IP allows faster delivery with lower cost structures, reduced variability in quality and outcomes, accelerated new consultant onboarding, and stronger differentiation in competitive situations. IP development requires dedicated investment that firms struggle to justify under utilization pressure, but pays long-term dividends in competitive positioning and margin improvement.

Technology and tools vary in importance by service line. Data analytics services require sophisticated analysis platforms. Technology implementation needs project management and configuration tools. Strategy consulting may need only standard productivity software. Tool investment should reflect client expectations and competitive norms in specific service markets.

Partner ecosystem development provides capabilities firms can't or shouldn't build internally. Technology partnerships provide specialized tools or platforms. Delivery partnerships offer specialized skills or capacity expansion. Referral partnerships generate qualified opportunities. Strategic partnerships combine resources for large opportunities.

Effective partnerships require clear value exchange benefiting both parties, documented responsibilities and expectations, regular performance reviews, and structured communication. Many firms accumulate dormant partnerships that generate more administrative overhead than value. Regular portfolio reviews should sunset inactive partnerships while deepening relationships with productive partners.

Connecting capability building to go-to-market strategy ensures capability investments support market-facing priorities and revenue generation.

Service Line Governance

Service line governance establishes accountability and performance management that drives portfolio optimization. P&L ownership assigns specific leaders responsibility for service line financial performance including revenue targets and pipeline development, margin objectives and cost management, capability investment and talent development, and market positioning and competitive strategy. Clear ownership prevents the diffused accountability common in professional services where everyone feels responsible for everything while no one holds real accountability for service line results. P&L owners should have authority matching responsibility: ability to make hiring decisions, influence pricing and positioning, and allocate capability investment.

Resource allocation decisions distribute talent, investment capital, and partner time across competing service line priorities. Formal processes prevent ad hoc allocation based on latest client request or strongest internal advocate. Allocation frameworks consider strategic priority based on firm direction, economic performance including margins and growth, market opportunity size and trajectory, and competitive position strength.

Most firms over-allocate resources to established services with strong internal advocates while under-investing in growth services lacking political champions. Disciplined allocation processes counteract this bias by examining data alongside advocacy.

Performance dashboards track key metrics that support fact-based service line management. Standard dashboard elements include revenue and growth trends, pipeline value and conversion rates, utilization rates and capacity, margin performance versus targets, client satisfaction scores, win rates in competitive situations, and talent retention and satisfaction.

Dashboard design should allow quick health assessment while providing drill-down capability for deeper investigation. Monthly reviews identifying trends and emerging issues support proactive management rather than reactive crisis response.

Management rhythms establish regular review cadences at multiple timeframes. Weekly pipeline reviews track near-term opportunity progression. Monthly performance reviews examine current metrics against targets. Quarterly business reviews assess strategic health and market position. Annual portfolio reviews make service line investment and sunset decisions.

This multi-horizon approach balances short-term execution with longer-term strategic development. Firms focusing exclusively on short-term metrics underinvest in capability building. Those focusing only on strategy miss operational performance issues until they become serious problems.

Portfolio Expansion Strategies

Service line portfolio expansion follows several strategic approaches, each with distinct risk-return profiles and implementation requirements. Adjacent services build on existing capabilities to address related client problems. Finance transformation firms adding supply chain optimization, technology implementers offering change management, or strategy consultants providing interim executive services all represent adjacent expansion. Adjacent expansion benefits from existing client relationships and trust, related talent profiles that support redeployment, shared go-to-market infrastructure, and methodology overlap reducing development investment. However, adjacency doesn't guarantee client demand or competitive differentiation. Many adjacent expansions fail despite logical fit.

Acquisition versus build decisions determine development approach. Organic build offers full control over development direction, cultural alignment with existing organization, and margin preservation. However, it requires longer time to market and revenue, higher risk from uncertain product-market fit, and complete capability development burden.

Service line acquisitions provide immediate revenue and clients, proven market demand and delivery capability, experienced talent, and accelerated market entry. Challenges include integration complexity with different cultures and systems, premium prices for successful firms, and potential talent attrition post-acquisition.

Most firms default to organic build without seriously evaluating acquisition alternatives. Acquisitions make particular sense when speed to market creates competitive advantage, capability gap exceeds internal development capacity, talent acquisition proves difficult, or attractive targets exist at reasonable valuations.

Partnership models create capability access without full acquisition investment. Strategic partnerships combine resources for specific opportunities or markets. Delivery partnerships provide specialized skills complementing core capabilities. White-label partnerships offer services under your brand through third-party delivery. Referral partnerships exchange opportunity flow rather than delivery collaboration.

Successful partnerships require aligned incentives preventing conflict, clear role definition avoiding confusion, cultural compatibility that supports smooth collaboration, and regular performance assessment ensuring value delivery. Partnership agreements should address revenue and margin sharing, client ownership and relationship management, quality standards and accountability, and conflict resolution mechanisms.

Understanding market positioning ensures expansion services strengthen overall competitive position rather than diluting brand clarity.

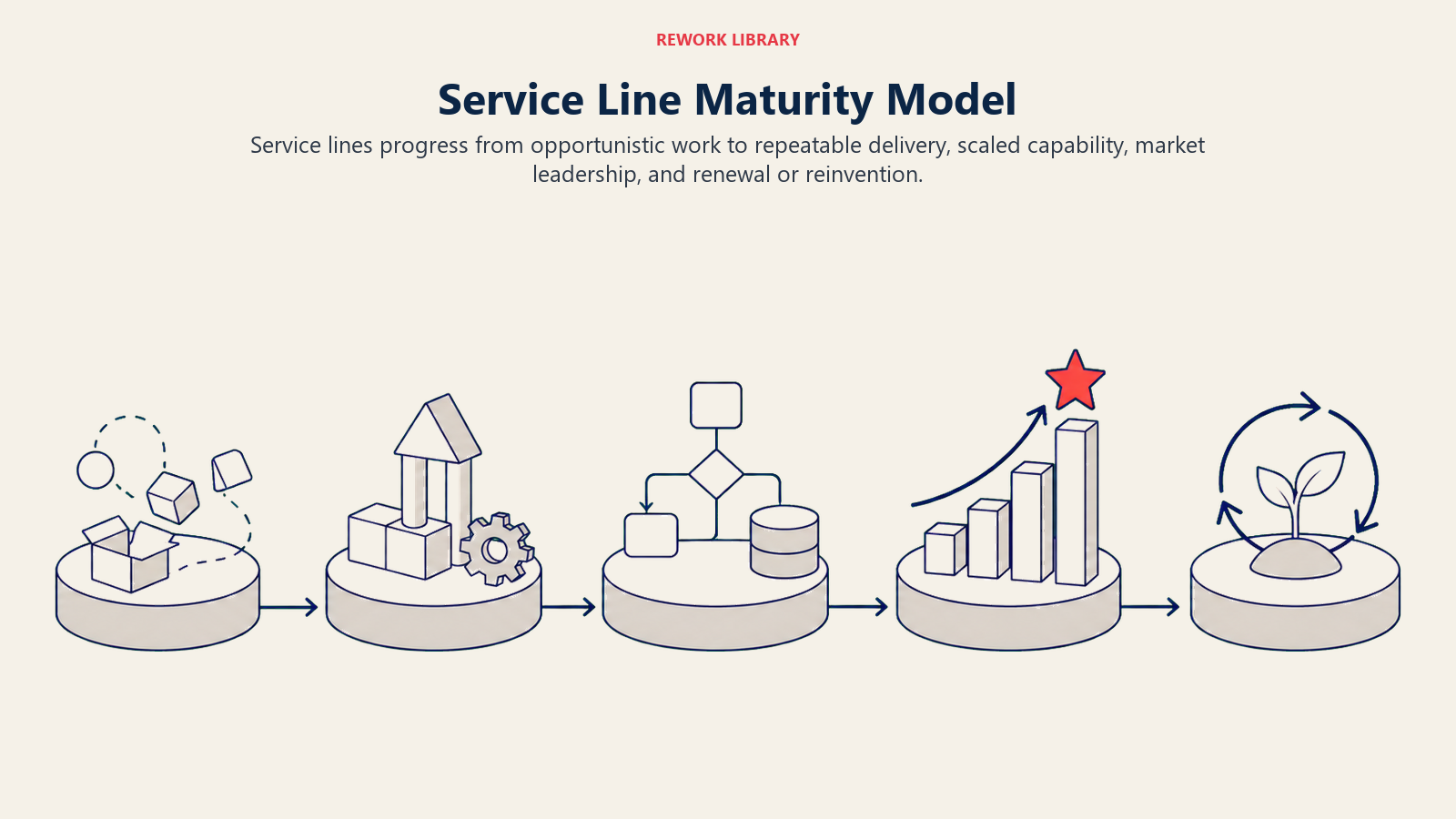

Service Line Maturity Model

Service lines evolve through maturity stages requiring different management approaches and investment levels. Opportunistic services emerge from individual client requests without systematic development. Characteristics include project-by-project delivery without repeatable methodology, no dedicated talent or formal expertise development, reactive marketing and business development, and highly variable quality and profitability. Many firms operate primarily at this maturity level, wondering why they struggle with profitability and differentiation. Opportunistic services work for testing market interest but can't support sustainable competitive position or acceptable margins at scale. Repeatable services develop systematic delivery approaches that produce consistent quality. These services feature documented methodologies guiding delivery, dedicated talent pools building expertise, proactive pipeline development and marketing, and predictable quality with managed risk profiles.

Moving from opportunistic to repeatable requires investment in methodology documentation and tools, talent development and hiring, marketing materials and case studies, and project management discipline. This transition represents the minimum threshold for credible competitive positioning.

Scalable services build organizational capability that supports growth without proportional resource increase. Characteristics include refined methodologies improving efficiency, developed IP and tools accelerating delivery, delivery models using varied skill levels, and strong talent development producing qualified practitioners.

Scalability drives margin expansion through improved efficiency while maintaining or improving quality. Services remaining at repeatable maturity often show flat or declining margins as volume increases because delivery doesn't become more efficient.

Differentiated services create distinctive market positioning based on demonstrated superiority. Markers include recognized expertise and thought leadership, proprietary methodology or technology, measurably superior outcomes for clients, and premium pricing power versus alternatives.

Differentiation requires sustained investment in IP and methodology development, talent attraction and development, market presence and thought leadership, and delivery innovation and improvement. Most services never reach this maturity level. Those that do command market-leading positions and margins.

Innovative services define new categories or fundamentally reshape delivery approaches. These leading-edge services address emerging client needs before broad market recognition, use new technologies or approaches in novel ways, create new business models or delivery methods, and generate intellectual property with licensing potential.

Innovation requires different talent profiles, higher risk tolerance, longer investment horizons, and different performance expectations than mature services. Few firms successfully maintain innovative services alongside scaled mature offerings because the management approaches and cultures conflict.

Understanding where each service line sits on this maturity model informs appropriate management approach, investment levels, and performance expectations. Managing mature services like innovative ones wastes resources. Managing innovative services like mature ones kills innovation through inappropriate performance pressure.

Performance Metrics for Service Lines

Service line performance requires multi-dimensional measurement capturing financial health, market position, delivery quality, and strategic trajectory. Revenue metrics (absolute revenue, growth rate, and revenue per client) establish basic scale and momentum. These should benchmark against initial projections and targets, market growth rates, and competitive performance when available.

Revenue alone can mask serious problems when growing unprofitably or in dying markets. Complementary metrics provide fuller pictures.

Margin performance (gross margin and contribution margin) reveals profitability after direct costs. These should trend toward or exceed firm-wide targets, with improvement trajectories for newer services. Persistent below-target margins indicate pricing problems from weak competitive position, delivery inefficiency requiring process improvement, or structural economic issues suggesting sunset consideration.

Win rate in competitive situations measures market competitiveness. Services winning 40-50% of competed opportunities demonstrate strong positioning. Below 30% suggests pricing or differentiation problems. Above 60% may indicate underpricing or weak competition. Win rate tracking over time reveals positioning strength trends.

Win-loss analysis examining why opportunities are won or lost provides richer insight than simple rates. Patterns in loss reasons (price, capability gaps, relationship strength, methodology differentiation) inform capability and positioning improvement priorities.

Client retention measures relationship strength and delivery quality. High retention rates above 90% indicate satisfied clients and strong positioning. Declining retention signals delivery problems, competitive threats, or changing client needs. Retention should factor relationship tenure because some client churn naturally occurs after specific projects complete.

Net Promoter Score or similar satisfaction metrics provide forward-looking indicators of retention and referral likelihood. These complement retention rates by identifying problems before they show up as client departures. Regular NPS collection allows trending and benchmarking across service lines revealing relative performance.

Pipeline metrics (pipeline value, pipeline coverage ratio, and conversion rates) predict future revenue and reveal business development health. Healthy pipelines maintain 3-4x coverage of quarterly revenue targets. Lower coverage ratios indicate business development problems. Declining conversion rates suggest qualification issues or competitive positioning weakness.

Understanding professional services metrics more broadly ensures service line measurement aligns with overall firm performance management.

Utilization and capacity metrics track talent deployment efficiency. Utilization should trend toward service line targets, with capacity planning preventing either chronic over-utilization harming quality or under-utilization destroying margins. Forward-looking capacity analysis supports proactive hiring or reduction decisions rather than reactive adjustments.

Making Service Line Strategy Work

Service line strategy provides the framework for building professional services firms that compete on demonstrable capability rather than relationships alone. The firms succeeding with portfolio approaches maintain discipline around service development, performance management, and resource allocation even when individual partners advocate for favorite services or opportunistic expansion.

Success requires cultural shifts in traditionally individualistic professional services environments. Moving from "we can do anything clients want" to "we focus on services where we deliver distinctive value" feels limiting to partners accustomed to full autonomy. But the constraint creates specialization, capability depth, and competitive positioning that generalist approaches can't match.

Data-driven decision making displaces seniority-based or relationship-driven resource allocation. Services demonstrate economic performance and strategic fit or face rationalization regardless of partner advocacy. This objectivity proves difficult in partnerships where consensus and accommodation often override business logic.

Investment patience lets services mature through developmental stages before demanding full financial performance. Most services require 18-24 months to reach acceptable profitability. Firms pulling investment prematurely when services don't generate immediate returns never develop new capabilities. Those maintaining investment discipline build portfolios that reduce dependence on mature services while positioning for evolving markets.

The strategic choice to manage service portfolios actively makes most sense for firms pursuing specialized positioning in chosen markets, premium pricing based on differentiated capabilities, scalable growth beyond founder expertise, and sustainable competitive advantage rather than relationship-dependent revenue.

For firms with these ambitions, service line strategy transforms professional services from personal consulting practices into scalable businesses that create value beyond individual relationships while building organizational capabilities that outlast any single practitioner.

Learn More

Senior Operations & Growth Strategist

On this page

- Understanding Service Line Architecture

- Service Line Development Framework

- Portfolio Optimization Principles

- Market Positioning Strategy

- Service Line Economics

- Capability Building for Service Lines

- Service Line Governance

- Portfolio Expansion Strategies

- Service Line Maturity Model

- Performance Metrics for Service Lines

- Making Service Line Strategy Work

- Learn More