Partner vs Employee Model: Choosing the Right Ownership and Compensation Structure

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

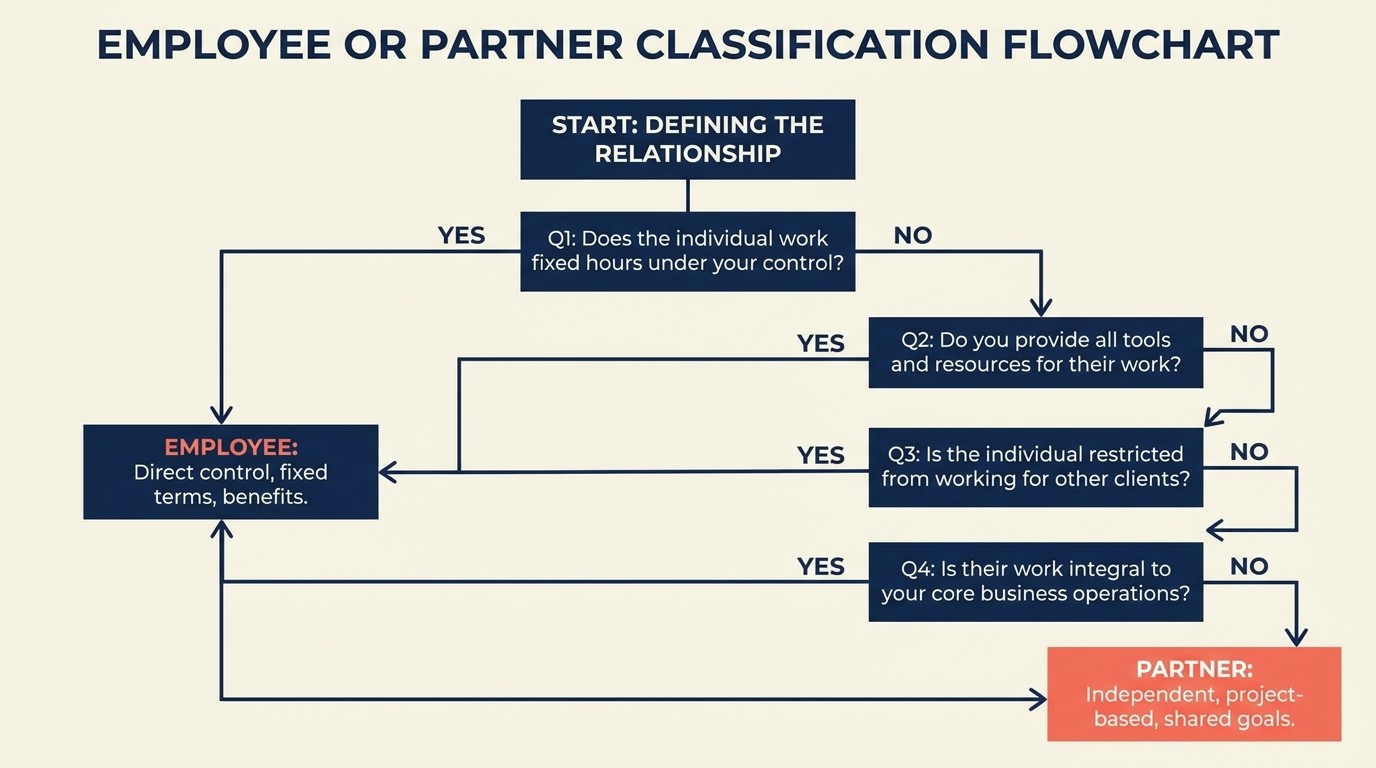

The partner vs employee model is the choice between giving people ownership equity in the firm or keeping them as salaried staff. The employee model, used by large firms like BCG and Accenture for most of their workforce, scales fast with simple, centralized pay. The partner model aligns incentives through profit sharing and equity, but adds governance, capital, and succession complexity. Most firms end up using a hybrid of the two.

Every professional services firm eventually faces this question: should we make people partners or keep them as employees? It seems like a binary choice, but the reality is messier. Your compensation structure shapes everything - how people make decisions, how they collaborate, what they prioritize, and whether they stick around for the long haul.

Get this wrong and you'll watch talented people leave for competitors, see politics overtake performance, or discover that nobody thinks beyond their next paycheck. Get it right and you build a firm where smart people align their interests with yours, where succession happens naturally, and where the value you create compounds over decades.

This guide walks through both models, the variations between them, and how to figure out what fits your firm. No universal right answer exists - just trade-offs that matter differently depending on where you are and where you're headed.

The ownership dilemma

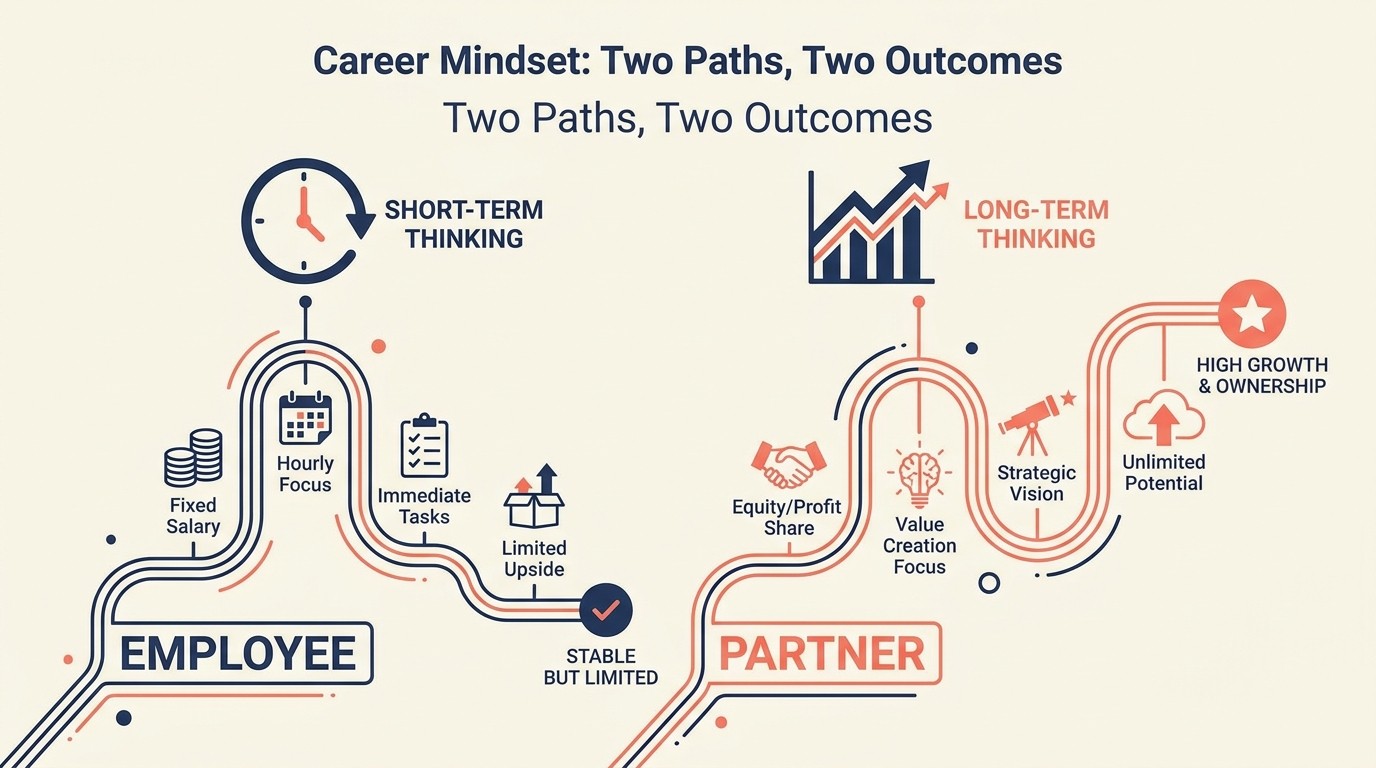

Here's what most firm leaders miss: the structure you choose drives behavior more than your values statement ever will. Put someone on a W-2 salary with no equity stake, and they'll optimize for different things than someone who owns 5% of the firm.

The employee model keeps things simple. Clear hierarchy, predictable compensation, minimal governance complexity. People show up, do great work, get paid well, and go home. But you're capped on upside - the best performers will eventually ask "why am I building someone else's equity?" Your talent development program must address this ceiling or you'll lose your best people.

The partner model aligns incentives. When people own a piece of the firm, they think like owners. They care about margins, client relationships, and long-term reputation. But you're introducing complexity - profit splits, capital requirements, governance fights, and the reality that not everyone should be an owner just because they've been around for seven years.

The hidden cost of getting this wrong isn't just losing people. It's cultural drift. Employee firms struggle to get people to care about profitability. Partnership firms struggle with partners who protect their book of business instead of collaborating. Both can work, but only if you design the structure intentionally.

The employee model deep dive

In the employee model, everyone's on payroll. Partners or principals might own equity, but most people - even senior ones - are W-2 employees with salary, bonus, and benefits. Think of how BCG or Accenture operates for most of their workforce.

The core economics are straightforward: base salary covers living expenses, bonus rewards performance, equity (if any) is granted not bought. People aren't writing checks to join the firm or taking distributions tied to profitability.

When the employee model works best:

If you're building a firm that needs to scale quickly, the employee model makes sense. You can hire 50 consultants without worrying about 50 new partners voting on firm direction. Decision-making stays centralized, which matters when you're moving fast.

If your service is productized or process-driven, employees work better than partners. Implementation consulting, tax preparation, compliance work - these benefit from consistency more than individual entrepreneurship. You want people following a methodology, not inventing their own.

If you plan to sell the firm or raise outside capital, keeping most people as employees simplifies cap tables and decision rights. Investors don't want to negotiate with 30 partners; they want to deal with founders or a small leadership team.

The advantages:

Simplicity wins here. Onboarding is faster - sign an offer letter, start working. Offboarding is cleaner - no equity buybacks or profit clawbacks. Compensation is transparent and comparable to market rates.

Flexibility matters too. You can adjust team size quickly without worrying about dilution or partner votes. Need to hire five more associates? Go ahead. Market shifts and you need to trim? Harder emotionally, but legally straightforward.

Cash flow is easier to manage. You're not doing quarterly distributions or managing partner capital accounts. Payroll comes out, profits stay in the firm to reinvest or pay out as owner dividends.

The limitations:

Retention becomes your biggest problem. Top performers hit a ceiling and realize they're building equity for someone else. The best ones leave to start their own firms or join competitors offering partnership.

You'll see less ownership mentality. When people don't own equity, they don't sweat margins the same way. They'll take clients out to expensive dinners on the firm's dime without thinking twice. They won't push back on scope creep because profitability isn't their problem.

Succession planning gets tricky. If you're a founder-led firm with employees, who takes over when you're ready to step back? You either sell to an outsider or you're suddenly creating partners out of employees - which is a jarring transition.

Typical roles that stay employee:

Junior and mid-level consultants, analysts, project managers, associates. These people are learning the craft and building skills. Employee status makes sense.

Specialists who don't want ownership responsibilities. A senior data scientist who loves the technical work but hates business development? Keep them as a well-paid employee. Not everyone wants to be an owner.

Support and operational roles. Finance, HR, marketing, IT - these typically stay employee roles even in partnership firms unless they're at the most senior level.

The partner model deep dive

The partner model means people buy in (literally or through vested equity) and own a piece of the firm. They're not just highly paid employees; they have skin in the game. Law firms, accounting firms, and boutique consultancies run this way.

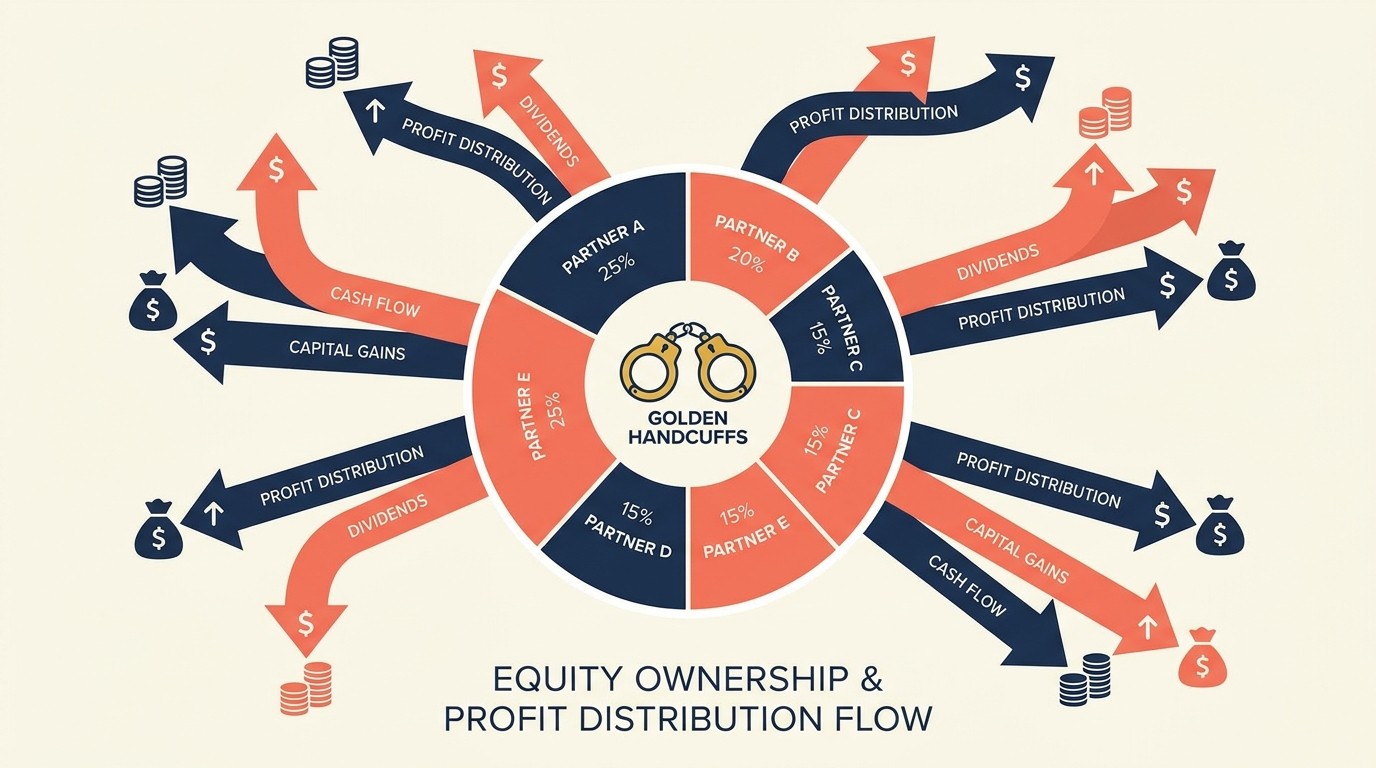

Partners share in profits, participate in governance, and bear some level of risk. If the firm has a bad year, partner compensation drops. If it's a great year, they make significantly more than they would as employees.

When the partner model works best:

If your business depends on relationships and reputation, partnerships work. When clients hire you because of specific people, those people should be owners. Otherwise they'll take the relationships with them when they leave.

If you need long-term thinking, ownership changes behavior. Partners care about five-year client relationships, not just this quarter's revenue. They invest in junior talent development because they'll benefit from leverage over time.

If you want to build a multi-generational firm, partnership provides the succession mechanism. Older partners gradually sell to younger partners, transferring ownership and client relationships in a structured way.

The advantages:

Alignment is the big win. When someone owns 3% of the firm, they care deeply about firm profitability, reputation, and growth. They'll work late to save a client relationship because it's their equity at risk.

Retention improves dramatically. The path to partnership creates a clear career track that keeps talented people around. Once they make partner, golden handcuffs kick in through equity value and unvested ownership.

Distributed decision-making can be a strength. Partners bring different client perspectives and market insights. If you're genuinely collaborative, partner governance produces better strategy than one founder calling all shots.

The complexities:

Governance becomes real work. Partner meetings, compensation committees, voting on major decisions - this takes time. And the more partners you have, the harder consensus becomes.

Not all partners are equal, but treating them differently causes tension. The rainmaker who bills $5M wants more than the service delivery partner who bills $1M. Figuring out fair splits without destroying collaboration is an art.

Bad partner decisions are expensive. Once someone makes partner, removing them is legally and emotionally brutal. And underperforming partners drain profitability while collecting distributions they haven't earned.

Capital requirements create barriers. If partnership requires a $200K buy-in, you're excluding people who don't have that cash, which might screen out talented people from non-wealthy backgrounds.

Partnership variations:

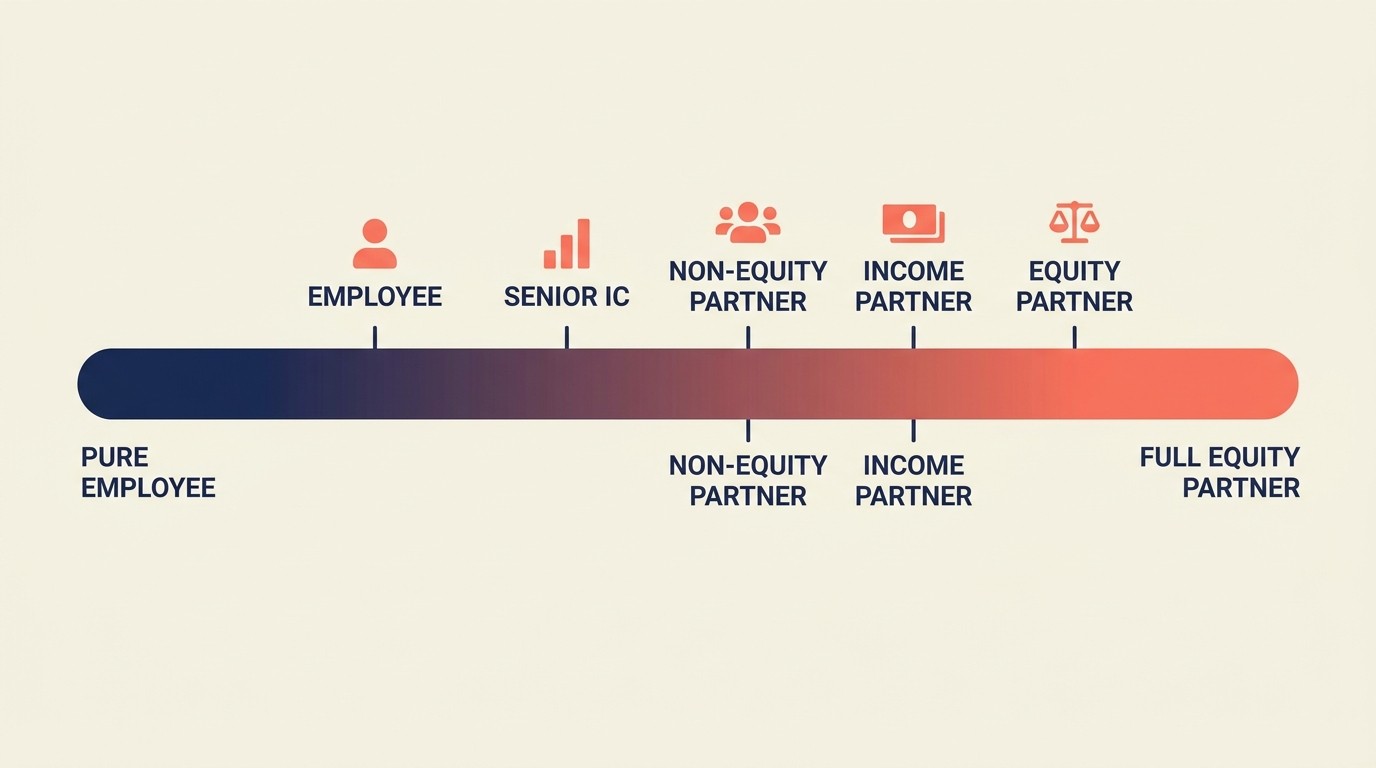

Not all partnerships are the same structure. You've got equity partners who own actual shares, income partners who share in profits but have no voting rights, and junior partners who get a title but minimal economics.

Two-tier partnerships are common: senior partners with full voting and equity rights, junior partners with limited economic participation. This gives you progression within the partnership track.

Some firms run non-equity partnerships where "partners" are really senior employees with better titles and profit-sharing bonuses but no actual ownership. This can feel like a bait-and-switch if not communicated clearly.

Partnership structure options

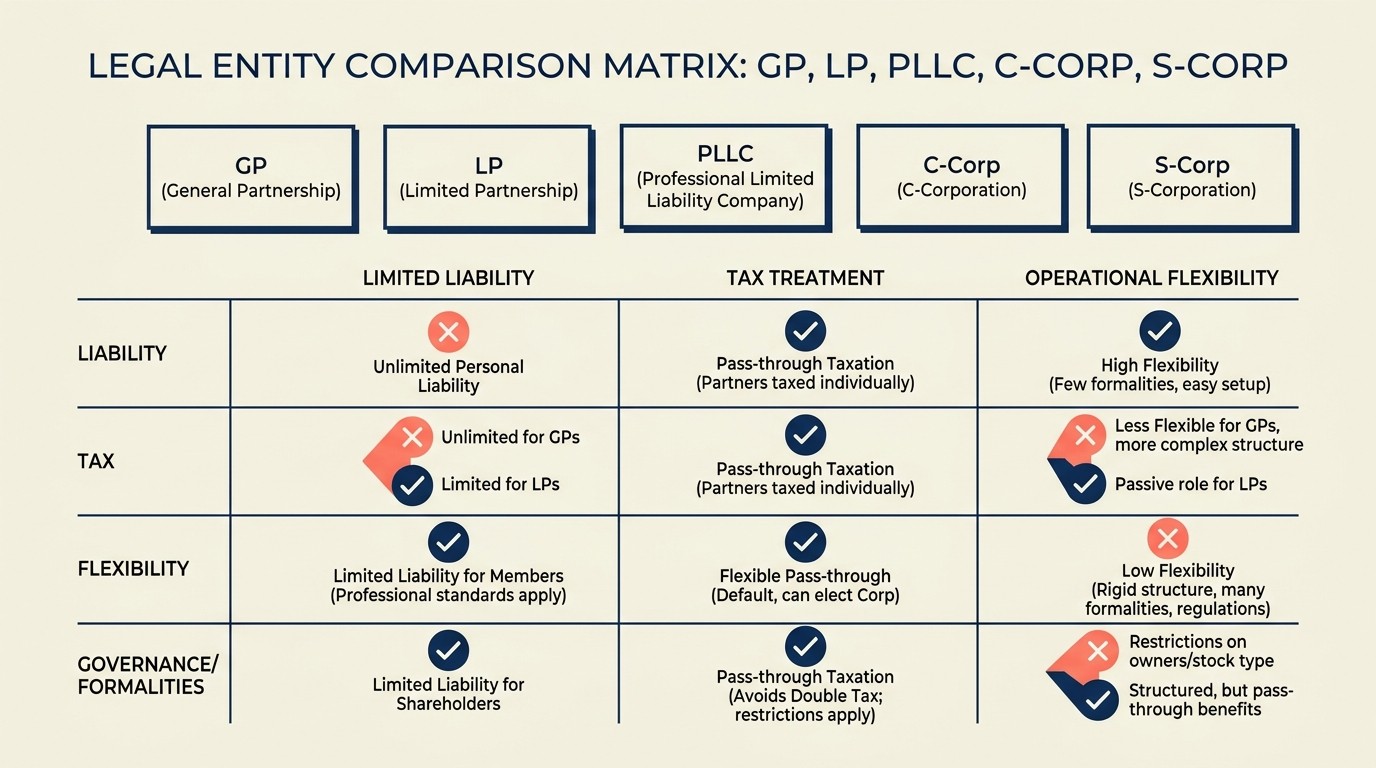

The legal entity you choose matters because it affects taxes, liability, and governance. Here's what actually gets used.

General Partnership (GP):

Everyone's a general partner with equal voting rights and unlimited liability. Rare today because unlimited liability is terrifying - if the firm gets sued, partners' personal assets are at risk.

Only makes sense for tiny firms (2-3 people) with very low liability risk. Even then, most people choose something safer.

Limited Partnership (LP):

You have general partners who run the firm and bear liability, plus limited partners who invest capital but don't manage the business. This was popular for investment firms but less common in professional services.

The distinction between GP and LP classes creates complexity most service firms don't need.

Professional LLC (PLLC):

This is the most common modern structure. Partners get liability protection (your personal house isn't at risk if the firm gets sued), pass-through taxation (profits flow to partners' personal returns), and flexible operating agreements.

You can structure profit splits, voting rights, and capital requirements however you want in the operating agreement. This flexibility is why most law firms, consultancies, and accounting firms use PLLCs or similar entities.

C-Corporation with equity:

If you plan to raise outside investment or eventually sell to a strategic buyer, C-corp makes sense. You issue shares to partners and employees, just like a startup.

The downside is double taxation - the corporation pays taxes on profits, then shareholders pay taxes on dividends. Only worth it if the exit or investment advantages outweigh the tax hit.

S-Corporation structures:

S-corps give you liability protection and pass-through taxation without the double-tax problem of C-corps. Profits flow through to shareholders' personal returns.

The catch: you're limited to 100 shareholders (fine for most firms) and only one class of stock (which limits your flexibility on different partner classes).

Hybrid and multi-tier models:

Many firms combine structures. The main firm might be a PLLC for partners, with a separate C-corp holding company for non-partner equity grants. Or you have a management company (PLLC) that owns operating entities (LLCs).

The more complex your structure, the more legal and accounting fees you'll pay. Only go multi-tier if you have a specific reason - geographic expansion, different service lines with different economics, or sophisticated tax planning.

Equity models and vesting

Equity without structure is chaos. You need clear rules on how people earn ownership, what happens when they leave, and how value gets created and distributed.

Ownership vs equity stakes:

Real equity means you own a percentage of the firm and have rights to vote, receive distributions, and sell your stake. Phantom equity or profit interests give you economic upside without actual ownership - you get paid like an owner but don't vote or have the same legal rights.

Phantom equity is simpler administratively but feels less real. People want actual ownership if they're making a long-term commitment.

Vesting schedules and cliffs:

Don't give equity all at once. Standard vesting is four years with a one-year cliff. You earn 25% after year one, then monthly or quarterly vesting for the remaining 75%. This protects the firm if someone leaves early.

For partners, vesting might be longer - six to ten years - because you want long-term commitment. Fast vesting creates churn as people hit 100% and immediately start looking for exits.

Cliff periods are critical. If someone leaves in month eleven, they get nothing. This discourages people from joining, extracting knowledge, and leaving quickly.

Buy-in requirements:

Requiring partners to buy in (invest their own capital) creates stronger alignment. If you write a $150K check to buy 3% of the firm, you're damn sure going to care about profitability.

Buy-ins can be cash upfront, financed through future distributions, or earned through sweat equity over time. Cash creates immediate commitment; earn-in over time is easier to access but less psychologically binding.

The amount matters. Too low and it's not meaningful. Too high and you exclude people who don't have wealth. Many firms set buy-in at 1-2x expected first-year partner compensation.

Buy-out formulas and valuation:

What happens when a partner leaves, retires, or dies? You need a formula that determines what their equity is worth and how the firm buys it back.

Common approaches: book value (assets minus liabilities, usually very low for service firms), multiple of revenue or EBITDA, or fixed formula based on trailing partner distributions.

Most partnerships use something like "3x average distributions over the last three years" or "1.5x revenue attributable to the partner." The goal is fairness without creating financial strain on remaining partners.

Avoid letting departed partners stay on cap table forever. Buy them out over 3-5 years so you're not sending checks to people who left a decade ago.

Dilution and refresh strategies:

As you add new partners, existing partners get diluted unless the firm grows. If you're 10 partners with 10% each and you add two more, everyone drops to 8.3% (assuming equal splits).

Refresh grants solve this. High performers get additional equity grants every few years to offset dilution. This keeps compensation competitive and rewards continued performance.

Some firms maintain an equity pool (like startups do for employee options). The pool is reserved for future partners, and as people join, they draw from the pool rather than diluting existing partners directly.

Compensation models for revenue generators

How you pay people shapes what they prioritize. Different models create different incentives.

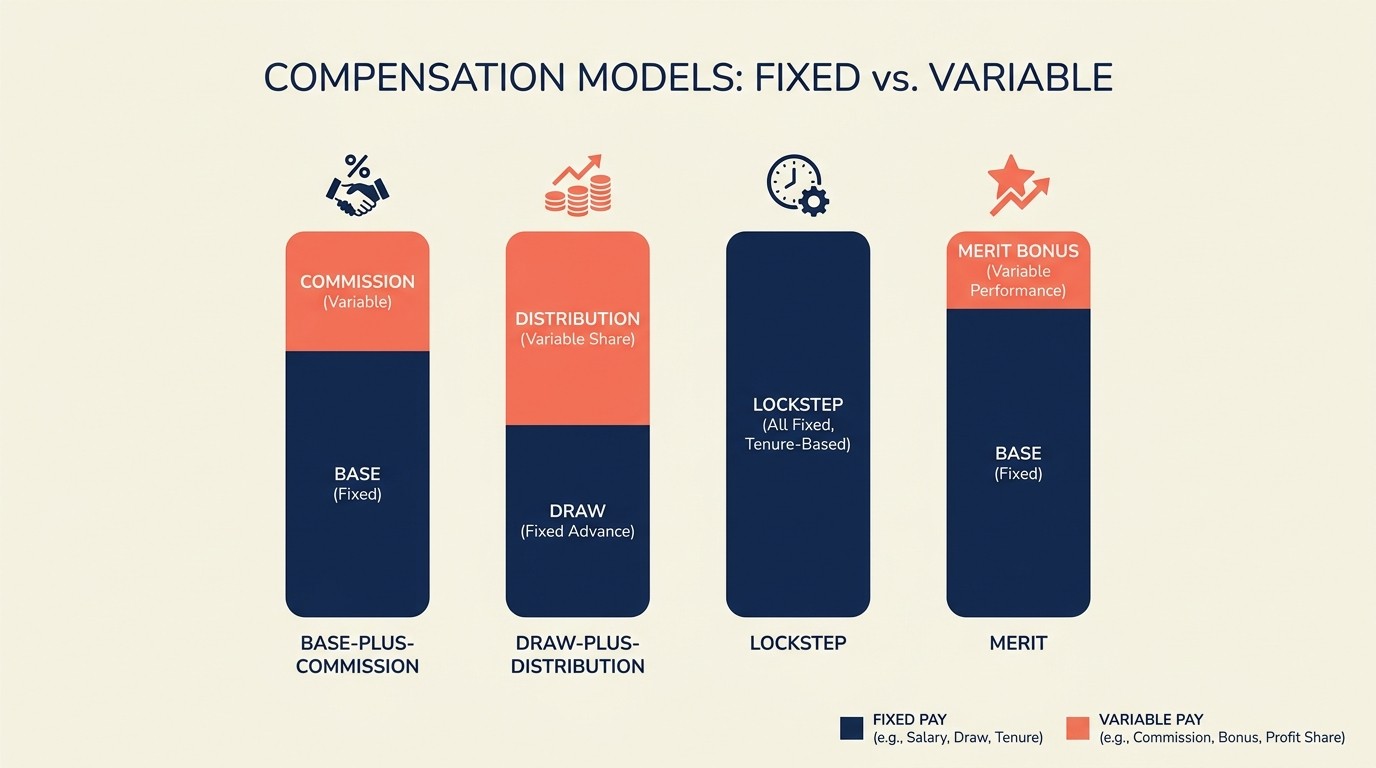

Base salary + commission:

This works like traditional sales. You get a base salary to cover living expenses, then commission on revenue you generate. Common in smaller consultancies and agencies.

Typical splits: 60% base, 40% commission at full productivity. Commissions might be 15-25% of revenue you bring in or 30-50% of gross margin.

The upside: revenue generators are directly rewarded for bringing in business. The downside: people optimize for their own book and resist collaboration. Why help a colleague win a deal if you don't get credit?

Draw + distribution models:

Common in law firms. Partners take a monthly draw (basically a salary) and then receive annual or quarterly distributions based on firm profitability and their ownership percentage.

The draw covers living expenses and smooths cash flow. Distributions are the real compensation - this is where you make serious money in profitable years.

Distribution splits can be equal (everyone gets the same % regardless of contribution) or tiered based on seniority, origination credit, or performance.

Lockstep advancement models:

Traditional law firm approach. Compensation increases in lockstep with years of tenure. A fifth-year partner makes X, a tenth-year partner makes Y, regardless of individual performance.

Lockstep promotes collaboration and long-term thinking. People share credit because everyone benefits from firm success. But it also rewards tenure over performance, which frustrates high achievers and protects underperformers.

Very few firms run pure lockstep anymore. Most have shifted to modified lockstep with performance adjustments.

Merit and performance-based models:

The opposite of lockstep - you're paid based on what you produce. Metrics include revenue originated, hours billed, client relationships managed, and subjective performance reviews.

Eat-what-you-kill is the extreme version: you keep a high percentage of what you bring in and bill, with a smaller portion going to firm overhead. This maximizes individual incentive but destroys collaboration.

Modified merit systems balance individual performance with firm contribution. You're rewarded for your book of business but also for mentoring junior staff, serving on committees, and building firm capabilities.

Clawback provisions:

What if a partner leaves and takes clients with them? Or what if their deals fall apart after they collect their commission? Clawback provisions let the firm recover compensation.

Typical clawback triggers: client leaves within 12 months of partner departure, revenue was fraudulently reported, or quality issues emerge after payment.

Clawbacks are controversial but necessary when you're paying significant upfront compensation based on future value delivery.

The economics of partnership

Understanding the financial mechanics helps you see why partnership works (or doesn't) for different firms.

Partnership equity value creation:

Service firm equity value comes from three sources: client relationships (recurring revenue streams), intellectual property (methodologies, frameworks, tools), and talent bench (ability to deliver without founder dependency).

For most service firms, 70% of value is in client relationships. That's why partner transitions matter so much - if the relationships walk out the door, equity value drops.

Building equity value means developing client relationships that transcend individual partners, creating IP that differentiates you, and building a talent pipeline that reduces key-person risk.

Profit splitting mechanisms:

Equal splits are simplest but rare. Most firms use formulas that consider origination credit (who brought in the client), execution credit (who did the work), and firm contribution (committee work, recruiting, etc.).

A common model: 40% origination, 40% execution, 20% firm contribution. This rewards business development and delivery while still valuing citizenship.

Subjective splits give a compensation committee discretion to adjust based on qualitative factors. More flexible but also more political.

Tax implications by structure:

Partnership/PLLC: Pass-through taxation. Firm profit flows to partners' personal returns. You're taxed as ordinary income at your personal rate. You also pay self-employment tax on earnings.

C-corp: Double taxation. Firm pays corporate tax on profits, then you pay personal tax on dividends. But you can defer taxation by keeping earnings in the corp.

S-corp: Pass-through without self-employment tax on distributions (only on salary portion). This saves ~15% on taxes but limits flexibility on equity classes.

Get tax advice specific to your situation. The difference between structures can be $50K+ per year per partner.

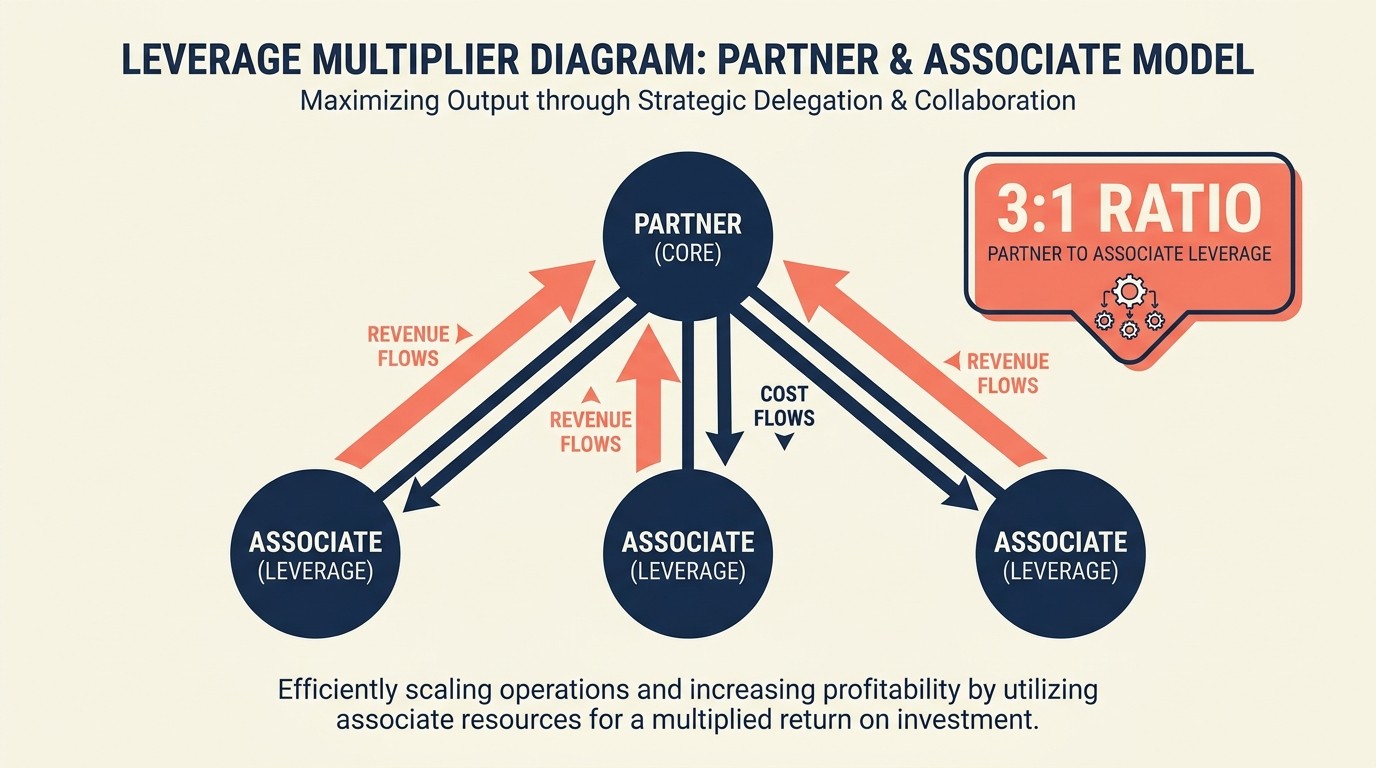

Leverage and multiplier effects:

Partner economics improve dramatically with leverage - the ratio of junior staff to partners. If you're a solo partner billing $500K annually, you keep all the profit but you're limited by your own capacity.

Add two associates at $150K loaded cost each who bill $300K each. You're now generating $1.1M in revenue with $300K in associate costs. Your economics just improved by $400K.

At 3:1 leverage (three associates per partner), math gets really attractive. This is why consulting firms obsess over utilization and leverage ratios. It's how partners make $500K-$2M+ instead of just high six figures. See leverage model optimization for detailed guidance on structuring this effectively.

Human dynamics and culture implications

Structure shapes culture more than vision statements do.

How ownership changes decision-making:

Employees think quarter to quarter. Partners think year to year or decade to decade. When you own equity that vests over six years, you care deeply about decisions that compound over time.

Ownership also changes risk tolerance. Employees prefer stability - consistent salary, low drama. Partners accept volatility because upside matters more. This affects everything from client selection to expansion decisions.

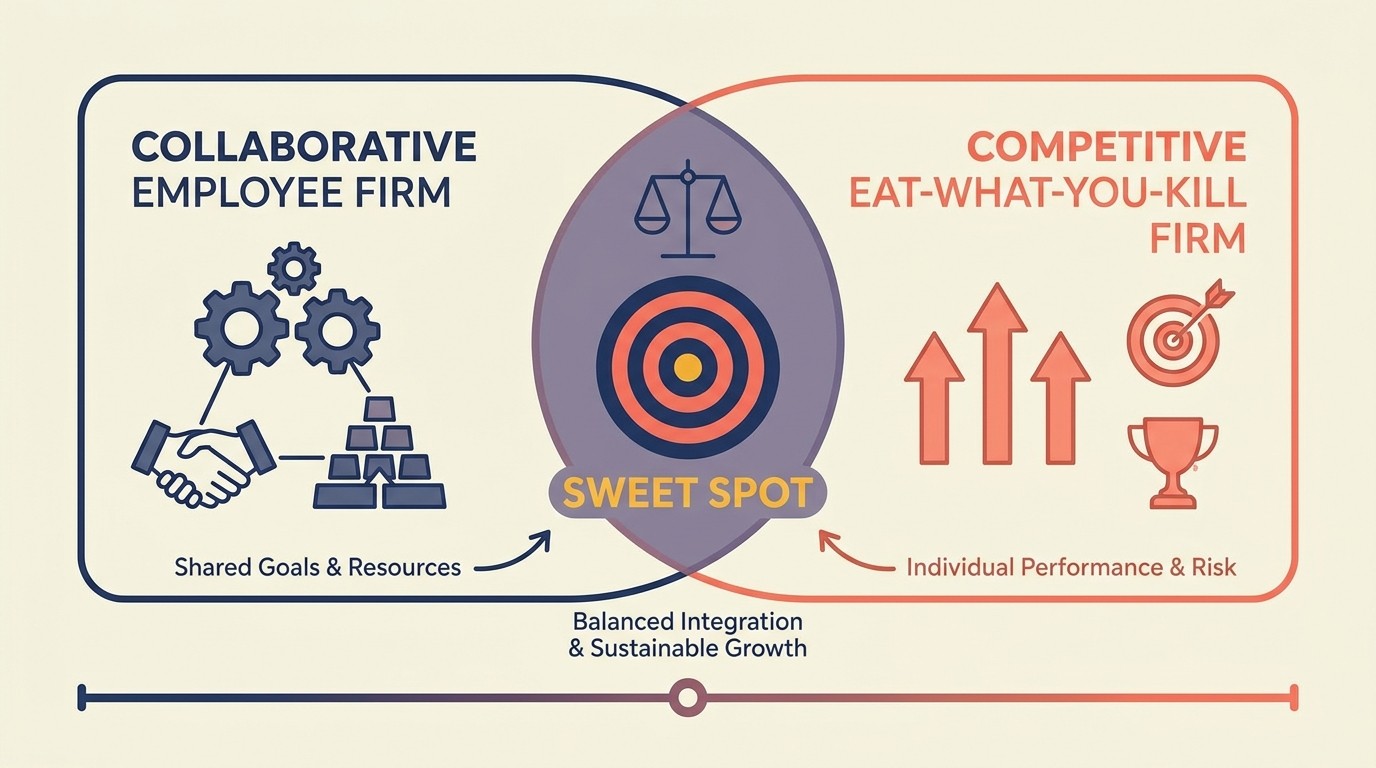

Collaboration vs competition dynamics:

Pure employee firms see less internal competition. People are collaborative because there's no zero-sum compensation fight. But you also get less entrepreneurial drive.

Eat-what-you-kill partnerships create fierce competition. Partners guard their clients, resist cross-selling, and fight over origination credit. This maximizes individual effort but fractures firm culture.

The sweet spot is modified partnership where compensation balances individual performance with firm contribution. You're rewarded for your book but also for helping others succeed.

Long-term vs short-term thinking:

Employees optimize for this year's bonus. Partners optimize for equity value creation over five to ten years. This shows up in client selection (partners avoid one-time projects, prefer retainers), talent development (partners invest in mentoring), and reinvestment (partners accept lower distributions to fund growth).

If your strategy requires long-term investments, partner structure helps. If you need to maximize short-term cash, employee structure might fit better.

Meritocracy vs seniority tensions:

Every firm claims to be a meritocracy, but partnership introduces seniority bias. The partner who joined 15 years ago often expects more compensation than the new partner, even if the new partner is outperforming them.

Pure meritocracy says pay for current performance. Pure seniority says reward tenure. Most firms blend both - base compensation on seniority, performance adjustments on top.

Tension emerges when high-performing junior partners see senior partners coasting at higher compensation. If you don't address it, the high performers leave.

Partner track and progression paths

Unclear paths to partnership destroy retention. You need transparent criteria and realistic timelines.

Clear vs ambiguous partnership tracks:

Best firms publish partnership criteria: revenue origination targets, client relationship depth, leadership contributions, technical expertise. This gives ambitious people a roadmap.

Ambiguous tracks ("we'll know it when we see it") create politics and favoritism. People guess at what matters, try to game the system, or get frustrated and leave.

Clarity doesn't mean guarantees - you can say "these are the criteria, but partnership isn't automatic." That's fair. What's not fair is having secret criteria that change year to year.

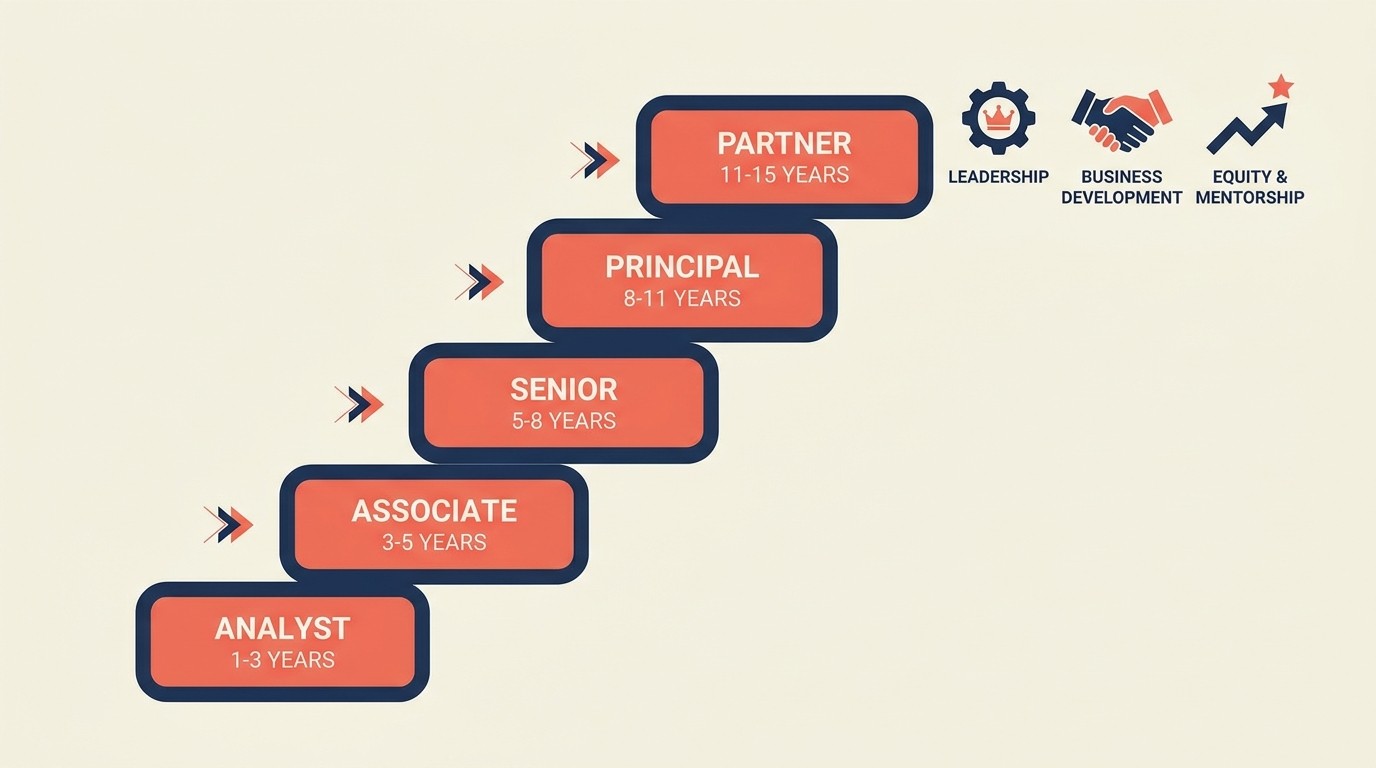

Time to partnership (typical 7-15 years):

Consulting firms: 7-10 years from analyst to partner. Law firms: 8-12 years from associate to partner. Accounting firms: 10-15 years.

Faster tracks (5-6 years) are possible but risky. People might not be ready for ownership responsibility. Slower tracks (15+) lose people to competitors who'll make them partner sooner.

The right timeline depends on complexity of the work and how long it takes to develop client relationships. Strategy consulting can move faster than tax accounting because relationship depth matters less.

Requirements and expectations:

Typical partnership requirements: consistent revenue generation ($1M-$3M depending on firm), strong client relationships (3-5 major clients who trust you), leadership capability (can you manage a team?), and cultural fit (do people want you as a partner?).

Some firms require you to bring a specific client or amount of business as your "entry ticket." Others promote based on potential and expect you to build your book as a partner.

Non-revenue requirements matter too: mentoring junior staff, contributing to thought leadership, serving on firm committees. You're joining the ownership team, not just getting a pay bump.

Denial management and transitions:

Not everyone makes partner, and that's okay - if you handle it professionally. The worst thing you can do is string someone along for years then deny partnership without explanation.

Up-or-out policies are brutal but clear. If you're not making partner after 10 years, you need to leave. This creates urgency and opens room for new talent. But it's harsh on people who are excellent individual contributors who don't want ownership.

Senior non-partner roles (principal, director, of counsel) give people a place to land if they're valuable but not partner material. This preserves talent without diluting partnership.

Hybrid and alternative models

Most firms don't fit neatly into "all employees" or "all partners." You need graduated structures.

Of Counsel arrangements:

Common in law firms. Of Counsel are experienced lawyers who work independently but affiliate with the firm. They're not employees or partners - more like contractors with close relationships.

This works for semi-retired partners who want to step back, specialists who bring niche expertise, or rainmakers who bring clients but don't want operational responsibility.

Equity partner vs senior associate hybrids:

Not everyone who deserves ownership responsibility wants full economic risk. Non-equity partners get the title and participate in decisions but don't have capital requirements or full profit exposure.

This can be a stepping stone to full equity partnership or a permanent role for people who contribute strategically but don't originate revenue.

Senior manager tiers:

Create senior IC (individual contributor) tracks for people who are exceptional at delivery but don't want ownership. Senior managers, principals, directors - these roles pay well and carry status without partnership obligations.

This prevents forcing great doers into owner roles they don't want. Not everyone should be a partner.

Multi-tiered partnership:

Junior partners own 1-3%, senior partners own 5-10%, founding partners own 15-25%. This reflects contribution and seniority while still giving newer partners real ownership.

Multi-tier creates progression within partnership. You can promote someone to junior partner at year 8, senior partner at year 15, based on continued performance.

Client-based equity models:

Some firms grant equity based on specific client relationships. If you own the relationship with a $5M client, you get equity tied to that client's revenue.

This aligns incentives perfectly but creates complexity if clients leave or relationships transition. And it discourages collaboration on client teams.

Governance and decision-making

Partnership without governance is chaos. You need structure for how decisions get made.

Partnership agreements essentials:

Your partnership agreement is the constitution. It should cover: equity ownership and vesting, profit distribution formulas, voting rights and thresholds, buy-in and buy-out terms, departure and retirement processes, and dispute resolution.

Don't use a generic template. Get a lawyer who specializes in professional services partnerships to draft it properly. This document prevents 90% of future conflicts.

Update it regularly. Your partnership agreement at five partners won't work at 50. Build in mechanisms for amendments (usually requiring 2/3 or 75% partner vote).

Partner meetings and cadence:

Monthly partner meetings for operational updates, quarterly for financial reviews and strategic discussions, annual for compensation decisions and major strategy.

Keep operational meetings efficient - updates, quick decisions, client issues. Save the heavy strategic debates for quarterly offsites where you have time to think deeply.

Document decisions. Memory is selective, especially around compensation and equity discussions.

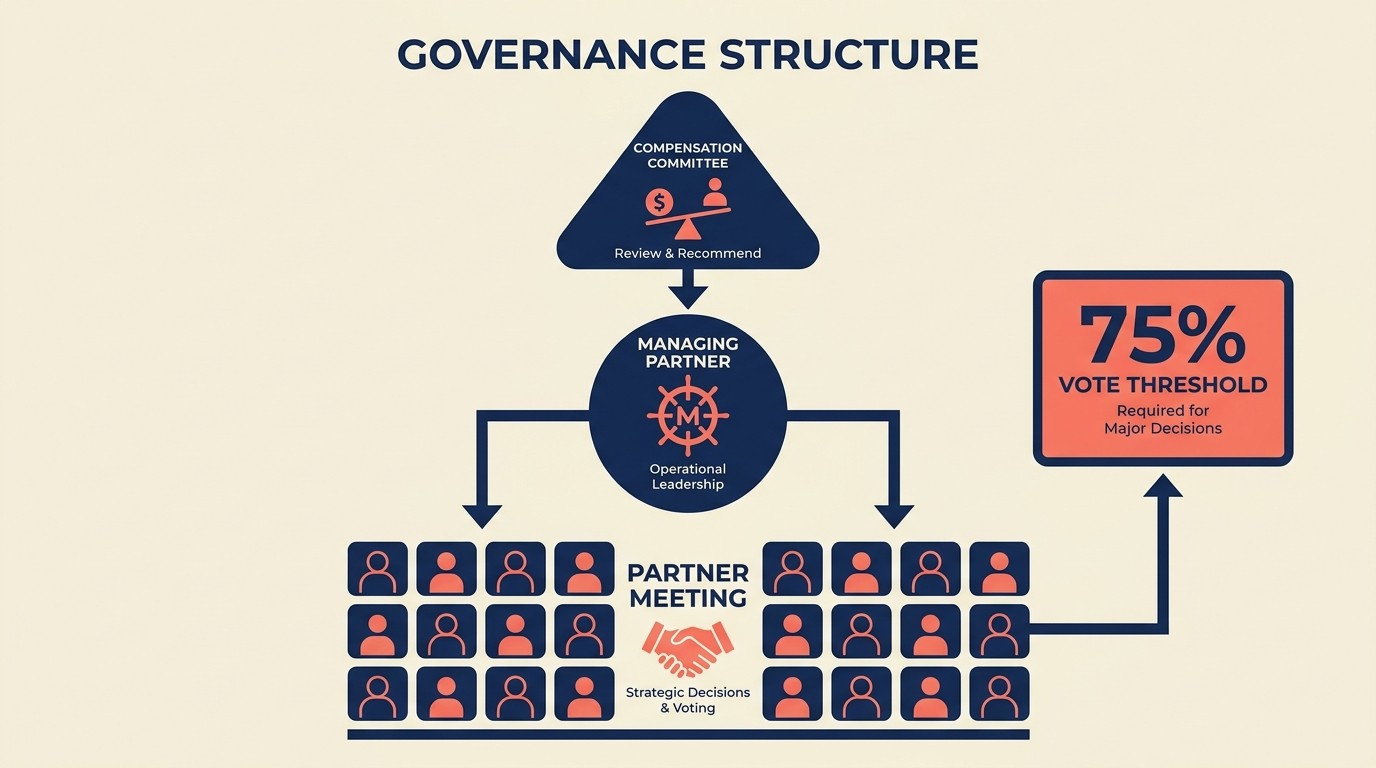

Managing partner role:

Someone has to run the firm day-to-day. The managing partner is CEO - they make operational calls, represent the firm externally, and drive execution of partner decisions.

Managing partners can be elected (democratic but political) or appointed by founders (faster but less buy-in). Term limits (3-5 years) prevent entrenchment and let people rotate back to client work.

Compensate managing partners for the role. They're sacrificing billable time to run the firm. Either give them additional equity or a stipend.

Compensation committee function:

Don't let all partners vote on each other's compensation - it's too political. A compensation committee (3-5 partners) reviews performance and makes recommendations.

Rotate committee membership every 2-3 years to prevent power concentration. Include a mix of senior and junior partners to balance perspectives.

The committee should use objective criteria when possible (revenue targets, client satisfaction scores) and document subjective decisions carefully.

Dispute resolution mechanisms:

Partners will disagree. Your agreement should specify how disputes get resolved: mediation first, then arbitration if needed. Avoid litigation between partners - it destroys the firm.

For minor disagreements, managing partner mediates. For major issues (partner removal, buy-out disputes), bring in outside mediator or arbitrator.

Build in forced resolution timelines. Disputes can't drag on for months while the firm suffers.

The transition decision: employee to partner

Promoting someone to partner is a one-way door. Get it right.

Evaluation criteria for partnership:

Financial contribution: Are they generating enough revenue to justify partner economics? Client relationships: Do clients trust them independently? Leadership: Can they develop talent and lead teams? Cultural fit: Do current partners want them as peers? Strategic value: Do they bring capabilities the firm needs?

All five need to be yes. Revenue alone isn't enough if they're toxic to culture. Great culture fit isn't enough if they can't bring in business.

Formal promotion process:

Set annual promotion cycles (usually end of year or mid-year). This prevents ad-hoc decisions and creates fairness.

Candidates submit partnership applications or are nominated by current partners. The compensation/partnership committee reviews against criteria. Finalist candidates interview with existing partners. Final vote requires supermajority (usually 75-80%).

High bar is good. If you're unsure, wait a year. Promoting the wrong person is much more expensive than making someone wait 12 more months.

Onboarding new partners:

Becoming a partner changes everything. Provide real onboarding: how profit distribution works, governance processes, partner responsibilities, client transition expectations.

Many firms assign a mentor partner to new partners for the first year. This helps them navigate the transition from "doing great work" to "owning the firm."

Set explicit expectations for year one: how much revenue they should originate, what committees they should join, how they should develop their role.

Communication strategy:

Announce new partners firm-wide, but explain the decision thoughtfully. This helps people understand partnership criteria and shows transparency.

If someone expected promotion and didn't get it, have a direct conversation. Explain gaps and what they need to develop. Either they improve and make it next year, or they understand it's not happening and can make their own decisions.

Partner buy-in and capital requirements

Skin in the game matters. But structure it fairly.

Capital contribution amounts:

Typical buy-in is 1-2x expected first-year partner compensation. If new partners make $250K, buy-in might be $250K-$500K.

This should feel significant but not impossible. Too low and it doesn't create real commitment. Too high and you exclude talented people without existing wealth.

Consider the firm's capital needs. If you're asset-light (consulting), you don't need much capital. If you have significant equipment or real estate (architecture firm), you might need more.

Buy-in from profits vs outside capital:

Let people buy in from future distributions over 3-5 years. They commit to contribute X% of their distributions until they've paid their buy-in amount.

This makes partnership accessible to people who don't have $300K sitting around. And it creates automatic retention - if you leave before fully buying in, you forfeit some equity.

Requiring outside capital (write a check or get a loan) creates stronger immediate commitment but screens out people based on wealth rather than merit.

Partner loans and financing:

Some firms provide loans to partners for buy-in, repaid through distributions. This keeps equity accessible while still requiring cash commitment.

Partner loans should be market rate (don't give free money) and recourse (if they leave, they owe the balance). This protects the firm if someone quits before repaying.

External financing (bank loans for partner buy-in) requires personal guarantees. Make sure candidates understand what they're signing up for.

Return on capital expectations:

If partners are putting in $250K, what return should they expect? Service firms typically return 20-40% annually on partner capital through distributions.

Lower returns (sub-15%) and you should reconsider requiring capital - you're just creating a barrier without meaningful return. Higher returns (50%+) are unusual but possible in extremely profitable boutiques.

Be clear about this upfront. If you tell someone "invest $300K for 3% equity" they need to understand profit expectations.

Partner retirement and exit planning

People will leave eventually. Plan for it.

Equity buy-back formulas:

Common approaches: 3x average annual distributions over last three years, 1.5-2x revenue attributable to the partner, book value plus goodwill multiple, or fixed schedule based on years of service.

The formula should be fair to both sides - not so high that the firm can't afford it, not so low that departing partners feel cheated.

Include payment terms: usually 3-5 years in installments. This spreads the cash flow burden and protects the firm if clients leave with the partner.

Transition periods and handoff:

Require 6-12 months notice for retirement. This gives time to transition clients and knowledge.

During transition, retiring partners work reduced hours but stay involved to introduce successors and ensure continuity.

Some firms keep retired partners on "of counsel" status for 1-2 years post-retirement. They're available for client questions but not actively working. This smooths the transition.

Partner succession planning:

Don't wait until someone announces retirement to plan succession. Identify critical client relationships and start transitioning them 2-3 years before expected retirement.

Bring junior partners into client meetings, gradually shift relationship ownership, and make sure clients are comfortable before the transition happens.

Succession should be a 3-5 year process, not a crisis when someone turns 65.

Legacy and retirement benefits:

Some firms provide retirement benefits beyond equity buyout: healthcare coverage, office space, continued education stipends. This rewards long service and maintains alumni relationships.

Others cut clean: buy out equity, wish them well, no ongoing relationship. Both approaches work, but be consistent.

Legal and tax implications

Get professional advice here. These decisions have big consequences.

Choice of entity impacts:

PLLC/Partnership: Pass-through taxation, flexible governance, professional liability protection. Best for most service firms.

C-Corp: Double taxation, but easier to raise capital or sell. Better if you're building toward exit.

S-Corp: Pass-through taxation, self-employment tax savings, but limited to one class of stock. Good for smaller firms with simple structures.

The entity choice affects everything: how you file taxes, how easy it is to add/remove partners, what liability exposure exists.

Partnership agreement essentials:

Already covered this in governance section, but worth emphasizing: spend $10K-$25K on a good partnership attorney to draft this properly. Cheap templates create expensive problems.

Tax optimization strategies:

Partners can reduce tax burden through: allocating income between salary and distributions (affects self-employment tax), timing distributions to manage tax brackets, investing in firm assets that create depreciation, structuring expenses properly.

Work with a CPA who specializes in partnership taxation. Small optimizations compound to six-figure savings over time.

Buy-sell agreements:

What happens if a partner dies, becomes disabled, or wants to sell their equity? Buy-sell agreements create forced transactions at predetermined valuations.

Typical triggers: death (firm buys at book value), disability (firm buys after 12 months), voluntary departure (formula-based buyout), involuntary removal (discounted buyout).

Fund buy-sell agreements with life insurance on partners. If a partner dies, insurance pays the buyout so remaining partners don't have to come up with cash.

Industry-specific models

Different professional services use different approaches. Here's what actually works in each.

Law firms (lockstep vs eat-what-you-kill):

Traditional law firms used lockstep - compensation based purely on seniority. This encouraged collaboration and long-term thinking but frustrated top performers.

Modern trend is modified merit - base compensation on seniority, adjustments for performance. Or full eat-what-you-kill where you keep a high percentage of what you originate and bill.

Eat-what-you-kill maximizes individual incentive but destroys collaboration. You end up with a collection of solo practitioners sharing overhead, not a real firm.

Consulting firms (pyramid leverage):

Consulting economics depend on leverage. Partners need 3-6 junior consultants working under them to hit target economics.

This drives up-or-out cultures. You need constant influx of junior talent and regular graduation of people who don't make partner.

Partner compensation often includes origination credit (who brought in the work) and execution credit (who managed delivery), creating incentive to both sell and deliver.

Accounting firms (partner classes):

Accounting firms often have multiple partner tiers: equity partners who own the firm, income partners who share in profits but don't have equity, and senior managers on partner track.

Progression is slower than consulting (10-15 years vs 7-10) because technical depth and client relationships take longer to build.

Partner buy-ins tend to be higher because accounting firms have more assets (lease commitments, equipment, working capital).

Marketing agencies (creative vs operator partners):

Agencies struggle with balancing creative talent and business operators. The brilliant creative director brings the work and client relationships. The COO makes the firm run efficiently.

Some agencies split equity 50/50 between creative and business partners. Others weight toward revenue generators. Both can work if expectations are clear.

Agency partnerships also deal with personal brands - clients often hire "the agency that David works at" not the agency itself. Structuring this is tricky.

Architecture and engineering firms:

These firms have significant capital requirements (software, equipment, insurance) so partner buy-ins tend to be higher.

Long project timelines (2-5 years) make annual compensation adjustments harder. Partners might need to wait years to see the profit from projects they originate.

Principal vs partner distinction is common - principals are senior technical leaders, partners are owners. This separates technical excellence from ownership responsibility.

Decision framework: which model for your firm

Here's how to actually make this choice.

Firm maturity assessment:

Early stage (0-3 years, <10 people): Stay simple. Founders own everything, everyone else is employee. Add complexity only when needed.

Growth stage (3-7 years, 10-50 people): Introduce partnership track. Your first senior hires are hitting the point where they need ownership or they'll leave.

Mature stage (7+ years, 50+ people): You should have a clear partnership model by now, with multiple partner cohorts and proven progression paths.

Key decision criteria:

Do you need to retain top performers long-term? → Partnership creates golden handcuffs.

Are you building a firm to sell? → Keep most people as employees, limited equity.

Does your business depend on individual relationships? → Partnership aligns incentives.

Do you need centralized decision-making? → Employee model is simpler.

Will you need outside capital? → Employee model or corporation with limited partners.

Quick assessment questions:

If your best performer left tomorrow and took clients with them, would your firm be severely damaged? If yes, you need partnership to retain them.

Can you afford to pay market-rate salaries plus benefits to retain top talent without offering equity? If yes, employee model can work. If no, equity is cheaper than cash.

Do you want to run this firm forever, or sell it in 5-10 years? Forever = partnership makes sense. Sell = keep equity tight.

Are you willing to share governance and accept slower decision-making? If yes, partnership. If no, employee model retains control.

Strategic fit evaluation:

Your compensation model should fit your business model. If you're selling standardized services at scale, employee model works. If you're selling custom expertise and relationships, partnership works.

Don't copy what your competitor does. Copy what works for firms with similar economics and strategy to yours.

Common mistakes and pitfalls

Learn from others' expensive errors.

Vague partnership tracks:

"Work hard and maybe someday you'll make partner" is not a track. People need clear criteria and realistic timelines. Vagueness creates politics and frustration.

Fix: Publish partnership criteria. Tell people exactly what's required and what the typical timeline is.

Equity without responsibility:

Giving someone partnership title and equity but no expectation that they'll originate business or lead teams. This creates deadweight.

Fix: Partnership should come with explicit responsibilities. If you're a partner, you're expected to bring in $2M annually, develop three junior staff, and serve on a committee.

Compensation disputes:

Partners fighting over origination credit, execution credit, and who deserves what share. This destroys culture and wastes time.

Fix: Establish clear formulas documented in partnership agreement. Have compensation committee make final calls. No arguing.

Under-performing partner retention:

The partner who made sense 10 years ago but hasn't been productive in five years. They still collect full distributions because nobody wants the confrontation.

Fix: Build in performance reviews for partners. Create graceful exits: transition to of counsel status, reduced equity, retirement packages. Don't let underperformers drain the firm.

Founder control issues:

Founders who create partnership structure but then veto every decision because "it's still my firm." This makes partnership meaningless.

Fix: If you're creating real partnership, you're giving up control. If you want control, stay employee model. Don't do fake partnership.

Implementation roadmap

Here's how to actually make this change if you're transitioning models.

Phase 1: Assessment (Month 1-2)

Analyze current state: who's here, what they make, what they contribute, where gaps exist. Review financials to understand if you can afford the model you want. Talk to advisors (attorney, accountant, business consultant) about options. Research what competitors and similar firms do.

Phase 2: Design (Month 2-4)

Choose entity structure. Draft partnership agreement (with attorney). Build compensation formulas and partnership criteria. Create financial projections showing how economics work. Design progression paths and timelines. Get buy-in from founders or existing leadership.

Phase 3: Rollout (Month 4-6)

Communicate the model firm-wide: why you're doing this, what it means, who's affected. Hold individual conversations with key people who'll be affected. Finalize legal documents and file necessary changes. Announce first partner promotions (if applicable). Train people on how the model works.

Phase 4: Optimization (Month 6+)

Collect feedback quarterly. Track metrics: retention rates, compensation satisfaction, recruiting success. Adjust formulas based on what's working and what's not. Annual reviews of partnership agreement to handle edge cases you didn't anticipate.

Expect a bumpy first year. You won't get everything right immediately. The key is creating a fair structure with clear rules, then iterating based on experience.

Frequently Asked Questions

What is the difference between a partner and an employee at a firm?

An employee is paid a salary and bonus and does not own a stake in the firm. A partner buys in or earns equity, shares in firm profits through distributions, participates in governance, and bears some downside risk if the firm has a bad year. Partners think like owners; employees optimize for compensation and stability.

Why do firms like BCG keep most staff as employees?

Large consulting firms keep most of their workforce on salary so they can scale quickly, centralize decision-making, and standardize delivery. Hiring 50 consultants as employees does not add 50 partners voting on firm direction, which keeps governance simple and protects the firm's ability to move fast and to sell or raise capital later.

When should a firm switch from employees to partners?

Most firms introduce a partnership track in the growth stage, roughly 3 to 7 years in with 10 to 50 people, when senior performers hit a ceiling and start asking why they are building someone else's equity. If losing a top performer with their clients would severely damage the firm, partnership is usually the tool that retains them.

What are the main partnership structures?

Common options include a Professional LLC (PLLC) for pass-through taxation and liability protection, S-corp or C-corp structures when an exit or outside capital is likely, and multi-tier partnerships where junior, senior, and founding partners hold different ownership percentages. Many firms also use non-equity or income partners as a stepping stone.

How long does it take to make partner?

Time to partner typically runs 7 to 10 years in consulting, 8 to 12 years in law, and 10 to 15 years in accounting. The timeline depends on how long it takes to build client relationships and technical depth, and on whether the firm publishes clear partnership criteria.

Where to go from here

Your compensation and ownership structure is never "done." It evolves as your firm grows, as markets change, and as you learn what works.

Start by getting clear on what you're optimizing for: retention, decision speed, exit value, cultural fit, or something else. There's no universally right answer, but there is a right answer for your situation.

Talk to other firm leaders in your industry. Ask what's working for them, what they'd change, and what mistakes they made. Most people are surprisingly open about this because we've all struggled with the same questions.

If you want to go deeper on specific aspects of firm operations:

- Professional Services Growth Model - The overall economic framework

- Professional Services Metrics - How to measure what matters

- Utilization & Capacity Planning - Getting leverage right

- Billable Hour vs Value-Based Pricing - Pricing strategy that affects compensation

The firms that get compensation right don't necessarily pay the most. They create structures where talented people see a clear path to building wealth alongside the firm. That alignment drives everything else.

Senior Operations & Growth Strategist

On this page

- The ownership dilemma

- The employee model deep dive

- The partner model deep dive

- Partnership structure options

- Equity models and vesting

- Compensation models for revenue generators

- The economics of partnership

- Human dynamics and culture implications

- Partner track and progression paths

- Hybrid and alternative models

- Governance and decision-making

- The transition decision: employee to partner

- Partner buy-in and capital requirements

- Partner retirement and exit planning

- Legal and tax implications

- Industry-specific models

- Decision framework: which model for your firm

- Common mistakes and pitfalls

- Implementation roadmap

- Frequently Asked Questions

- Where to go from here