Strategic Fundraising Guide: How Leaders Build and Sustain Investor Relationships

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Most founders think about fundraising as a specific activity they do periodically: prepare a deck, contact investors, run a process, close a round. This framing is understandable but costly. The leaders who raise successfully, consistently, and on favorable terms think about fundraising differently: as an ongoing relationship-building discipline that happens to culminate in capital transactions.

The round that closes in June was made possible by conversations in January, introductions in October, and credibility built through a year of demonstrated execution. The investor who leads your Series B may have first encountered your company as a Series A observer. The terms you get on your next round are shaped in part by how you managed your current investors throughout the previous one.

This guide addresses fundraising as a leadership discipline, not just a tactical process.

What Investors Are Actually Evaluating

Understanding investor decision-making is the starting point for strategic fundraising. Most investment memos focus on market size, business model, financial metrics, and team quality. But the actual decision is rarely as linear as the memo suggests.

The narrative test. Investors are pattern-matching against a mental model of what great companies look like at a given stage. Your job is to demonstrate that you fit (or credibly challenge) that pattern. The narrative of your business needs to be coherent: why this market, why now, why this team, why is this solution better than what exists? If the narrative breaks down under questioning, conviction does not emerge.

The founder-market fit test. Before evaluating market size or financial projections, investors ask: does this team have an inherent advantage in this market? It might come from domain expertise, a proprietary customer relationship, an insight into customer behavior that others have missed, or a technical capability that is genuinely differentiating. Teams that could have been assembled to attack any attractive market carry less conviction than teams with a specific, credible reason to win in this one.

The momentum signal. Investors respond to trajectory more than absolute metrics. A business that is growing 20% month-over-month with a small base is more attractive than a business that has plateaued at a larger base. The corollary: fundraising is harder when metrics are flat or declining, and much easier when the trajectory is clear and up. Timing your fundraising process to coincide with periods of strong momentum is a significant tactical advantage.

The reference check network. Investors talk to each other and to people who know your team. Your reputation among customers, past employers, former investors, and the broader entrepreneurial ecosystem matters. Founders who treat every professional interaction as a potential reference point are practicing strategic fundraising even when they are not in a formal process.

Round Types and Their Strategic Logic

Different types of capital serve different purposes. Choosing the right type at the right stage is part of strategy, not just financing.

Pre-seed and seed capital is appropriate for validating core assumptions before you have a repeatable business. The goal is to get enough information to know whether the business is worth building, and to build a foundation of customer evidence that makes subsequent fundraising credible. Seed investors are tolerating higher uncertainty and are compensated with lower valuations. The right investors at this stage provide not just capital but relevant networks, market knowledge, and credibility with subsequent investors.

Series A is typically the first institutional capital of scale. It comes after you have demonstrated product-market fit (customers who use the product, get value from it, and would miss it if it went away) but before you have a fully proven scalable go-to-market. Series A investors are evaluating whether the business can scale, not just whether it can work. The key metrics vary by sector but typically include retention (does the product hold customers?), unit economics (does the business model work at the unit level?), and growth rate.

Series B and beyond is capital to scale what is already working. Investors at these stages are doing financial analysis that looks more like traditional private equity diligence: market sizing, competitive positioning, management depth, financial model integrity, and go-to-market efficiency. The storytelling component shrinks relative to the financial analysis component.

Debt and revenue-based financing are non-dilutive alternatives that are appropriate for businesses with predictable revenue and a clear use of proceeds that generates a return higher than the cost of the debt. These instruments are increasingly available to software and subscription businesses and can be a better choice than equity when the company can deploy capital at a rate that makes dilution expensive.

Strategic investment from corporate investors (large companies investing in their ecosystem) is neither pure financial capital nor pure strategic benefit. It comes with relationship complexity, potential conflicts of interest, and term structures that can complicate future fundraising. Strategic investors can open commercial relationships and market access that financial investors cannot. They can also create significant constraints on future financing and M&A options if terms are not carefully negotiated.

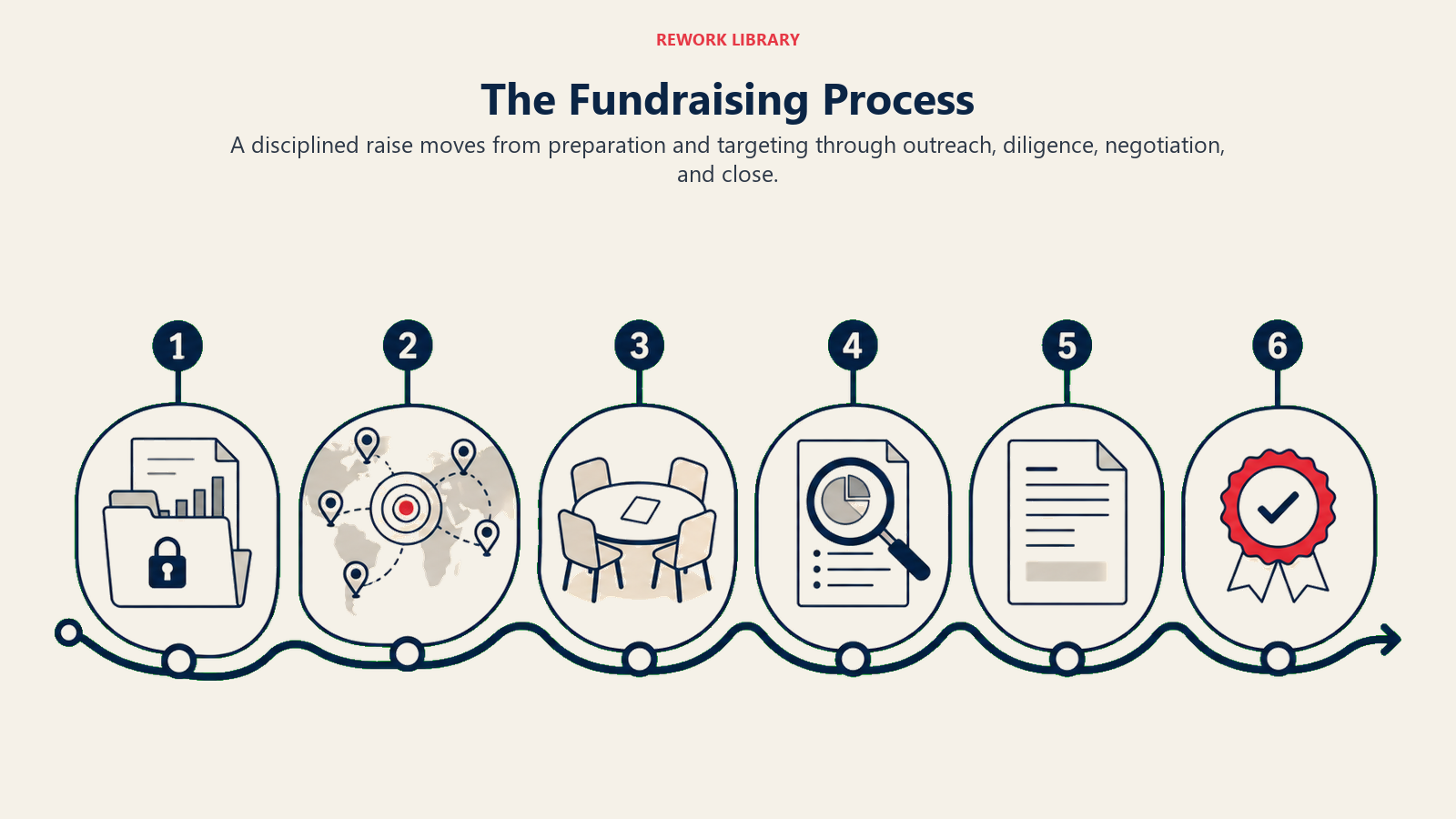

The Fundraising Process

A well-run fundraising process is not passive. It is designed to create information flow and dynamics that favor the company.

Establish your target list. Research investors who are genuinely active in your stage and sector. The right investor for a seed-stage healthcare company is different from the right investor for a Series B enterprise software company. An investor who does not have conviction in your market will not champion the deal internally regardless of how well the pitch goes.

Develop warm introduction paths. Cold outreach to investors works rarely. Warm introductions, through portfolio founders, mutual contacts, or investors who know you from prior interactions, work much more often. Building your network of people who can make credible introductions is a long-term discipline, not something you can manufacture during a process.

Run a compressed, parallel process. The worst fundraising process is a series of sequential conversations over many months where momentum dissipates between meetings and no single investor feels urgency. A better structure runs parallel conversations with multiple firms on a compressed timeline, so that interest from one investor is visible to others and decisions are made with information about alternatives.

Control the information flow. During a process, every piece of information you share shapes how investors evaluate the business. Share what demonstrates your strengths and validates your narrative. Be honest about challenges (investors are sophisticated and will discover them eventually), but be thoughtful about the timing and framing of information that requires context to interpret correctly.

Manage the close, not just the pitch. Many fundraising processes break down not because investors lacked conviction but because the mechanics of closing a term sheet, conducting diligence, and completing legal documentation created delays that eroded momentum. Experienced founders have a lawyer who specializes in venture transactions, model documents ready to send, and a clear understanding of what diligence will look like so it does not become a discovery process.

What to Negotiate

Term sheet negotiation is not just about the headline valuation. Many terms have consequences that outlast the round itself.

Liquidation preferences. The order and multiplier at which investors are paid ahead of common shareholders in a sale or liquidation. Standard terms (1x non-participating preference) are reasonable. Participating preferences, or multiples above 1x, can significantly reduce founder and employee proceeds in outcomes that would otherwise be good.

Board composition. Each institutional round typically results in the investor taking a board seat. Board composition determines governance: who can hire and fire the CEO, what decisions require board approval, who controls the company in a distressed scenario. Founders who give up board control early often find it difficult to recover in subsequent rounds when they need more capital.

Anti-dilution provisions. These protect investors against future financing rounds at lower valuations. Full ratchet anti-dilution is very investor-favorable and can be extremely painful in a down round. Broad-based weighted average anti-dilution is standard and more balanced.

Information rights and pro-rata rights. Major investors typically receive the right to participate in future rounds to maintain their ownership percentage. This is generally acceptable but can constrain your flexibility in future rounds if your early investor base is large or includes parties whose continued participation is complex.

Managing Existing Investors

Fundraising does not end when the round closes. Managing existing investors well is a strategic discipline that directly affects future fundraising.

Consistent, honest communication. Regular investor updates (monthly or quarterly) that acknowledge challenges alongside progress build trust over time. Investors who are surprised by bad news at a board meeting are more difficult to work with than investors who knew about the challenge in advance and have had time to process it.

Leverage networks actively. Investors have networks. Most are willing to make introductions to customers, potential hires, or subsequent investors if you ask specifically. Vague requests for "help" produce little. Specific requests ("I am looking for an introduction to the Chief Revenue Officer of companies in the X category who have 50-200 person sales teams") produce useful connections.

Be direct about what you need. If a subsequent fundraising round is coming, your existing investors are among the first who should know. They have information rights and an economic interest in the company's success. Keeping them closely informed about where the business is heading and what the capital needs are allows them to prepare to participate or to make introductions that accelerate the process.

Key Facts

- Most fundraising failures are timing failures, not quality failures. A strong business fundraising into a weak market environment or against a deteriorating macro backdrop will struggle regardless of fundamental quality. Understanding the market environment before launching a process and timing accordingly can make a significant difference.

- The first term sheet changes the process dynamics entirely. A process without term sheets is a process looking for conviction. Once a credible investor commits, others can respond to the offer rather than forming independent conviction from scratch. Getting to the first term sheet is the critical milestone.

- Reference checks are bilateral. You can and should reference-check investors before accepting their capital. Investors who have been difficult board members, who have pushed founders out of companies, or who have behaved badly in distressed situations leave trails. Talk to founders at their portfolio companies before closing.

Frequently Asked Questions about Strategic Fundraising Guide

When is the right time to raise external capital?

The right time is when you have enough evidence to make a credible case for the investment, when you have a specific and defensible use of proceeds, and when the market environment is favorable. Fundraising when you are running out of money is the worst time because it eliminates your negotiating leverage and signals distress. The general guidance is to start a fundraising process with 12-18 months of runway so you can afford to be selective.

How much should you raise?

Raise enough to reach the next meaningful inflection point in your business: the milestone that will make the subsequent round easier. Raising too little and running out of runway before that milestone is a common failure. Raising too much at too high a valuation creates pressure to grow into the valuation that can distort decision-making. The heuristic most operators use is: raise 18-24 months of runway at the capital efficiency you expect to achieve.

Should founders care about which investor they take money from?

Yes, significantly. Investors with deep domain expertise, active portfolio networks, and a track record of constructive board participation create more value than those who provide capital without those attributes. Investors who are not aligned with your vision, who micromanage, or who have different risk tolerances can create significant friction. The relationship with a lead investor typically lasts five to ten years. It deserves as much due diligence as any other long-term business partnership.

What is the biggest mistake founders make in fundraising?

Underestimating how long it takes and starting too late. Fundraising processes that feel like they should take two months often take five. If you start when you need the money, you are already in trouble.

Related Reading