Contrarian Strategy: How Leaders Win by Disagreeing with Consensus

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Contrarian strategy is the discipline of making decisions that differ from industry consensus because you have identified where that consensus is wrong. It is not stubbornness or reflexive disagreement. It is a systematic approach to finding strategic opportunities that others have systematically missed.

What is contrarian strategy?

Most organizations compete on the same assumptions. They watch the same analysts, attend the same conferences, and read the same competitive intelligence reports. When the industry converges on a belief ("customers want X," "this segment is saturated," "that technology is not ready"), most leaders act on it. The result is a crowded center: lots of companies doing similar things, competing on price and execution rather than insight.

Contrarian strategy is the practice of asking, "Where is this consensus wrong, and what would it mean if we acted on the correct view?" The leaders who do this well are not iconoclasts. They are disciplined reasoners who understand how consensus forms, why it is often reliable, and when it breaks down.

The key distinction is between contrarian posture and contrarian analysis. A leader who reflexively avoids popular positions is not practicing contrarian strategy. They are just being difficult. A leader who builds a systematic process for stress-testing prevailing assumptions and identifying where market evidence does not actually support consensus beliefs is doing the real work.

Key Facts

Research on strategic decision-making consistently finds that organizations that pursue differentiated strategies outperform industry average returns over 10-year horizons, while cost-based parity strategies see margin compression as more competitors adopt similar approaches.

Studies of innovation in established industries find that the most disruptive entrants succeed not by having better technology, but by holding a different belief about customer behavior that incumbents had collectively dismissed or overlooked.

Analysis of venture-backed startups finds that the most successful outcomes disproportionately involve companies that were widely dismissed by domain experts at founding, suggesting that contrarian bets in venture are not noise but a consistent pattern among the highest returns.

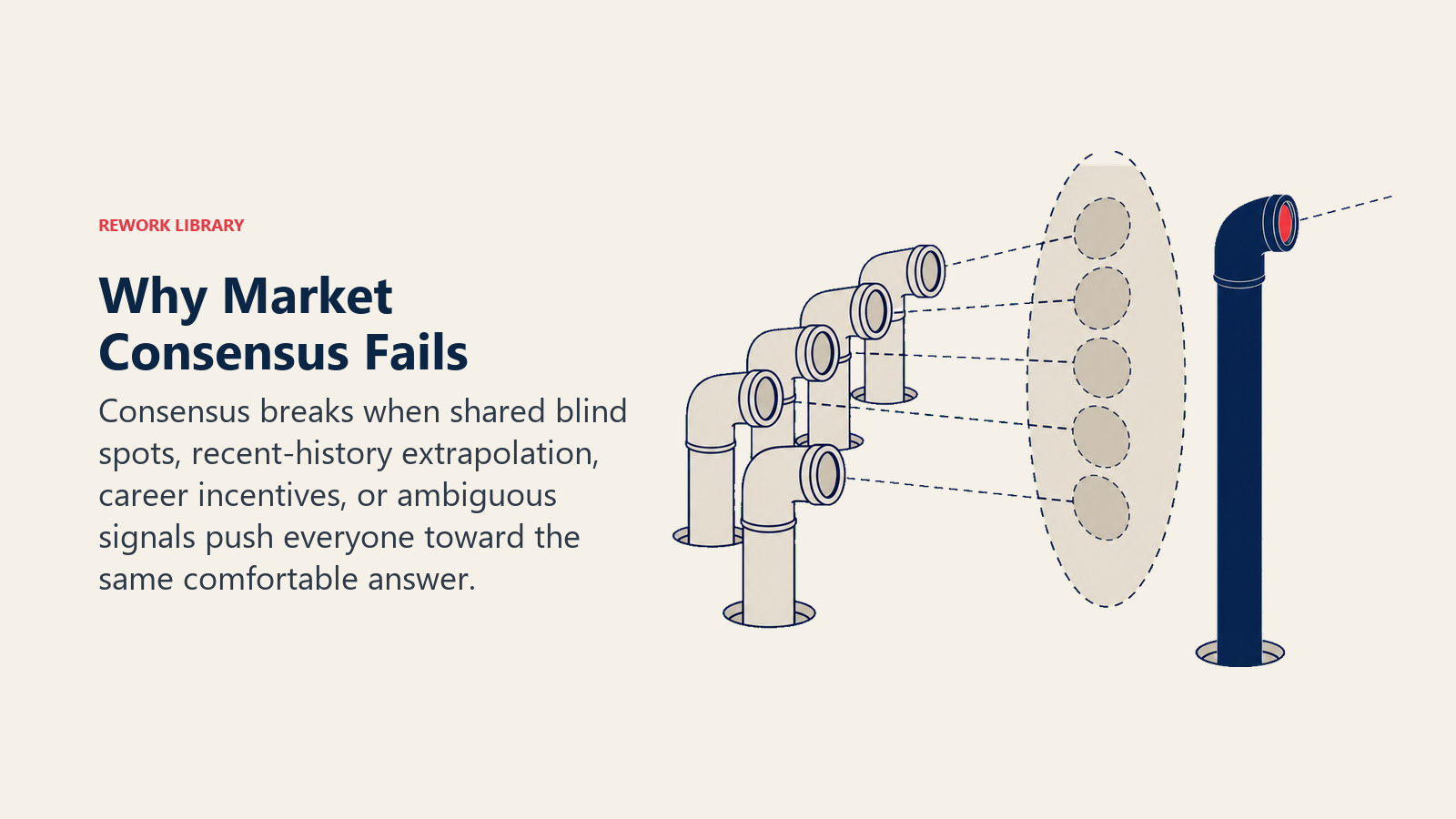

Where consensus goes wrong

Understanding when to trust consensus and when to question it is the central skill of contrarian strategy. Consensus is not always wrong. In fact, it is usually right. The cases where it breaks down follow predictable patterns.

Consensus formed from shared blind spots. When an entire industry recruits from the same talent pools, uses the same analytical frameworks, and rewards the same behaviors, it develops a systematic inability to see certain possibilities. The blind spot is invisible from inside the cluster. Leaders who bring genuine outside perspective (from a different industry, geography, or discipline) are more likely to spot the gap.

Consensus extrapolated from recent history. Markets tend to project the recent past forward. When a segment has been declining for five years, consensus assumes it will keep declining. When a technology has been "almost ready" for a decade, consensus assumes it will never be ready. Both assumptions get violated with regularity. Contrarian analysis asks: what would have to be true for the trend to reverse, and is that now more likely than it was?

Consensus optimized for current incentives. Analysts, consultants, and executives all have career incentives that shape their strategic recommendations. Recommending a contrarian position is professionally risky if it turns out to be wrong. Recommending the consensus position is professionally safe even if it turns out to be wrong, because everyone failed together. This incentive structure systematically pushes consensus toward the center.

Consensus where the signal is ambiguous. Markets produce noisy data. When the evidence genuinely does not point clearly in one direction, consensus fills the gap with comfortable assumptions. Contrarian leaders look for situations where data is being interpreted through a strong prior that is worth questioning.

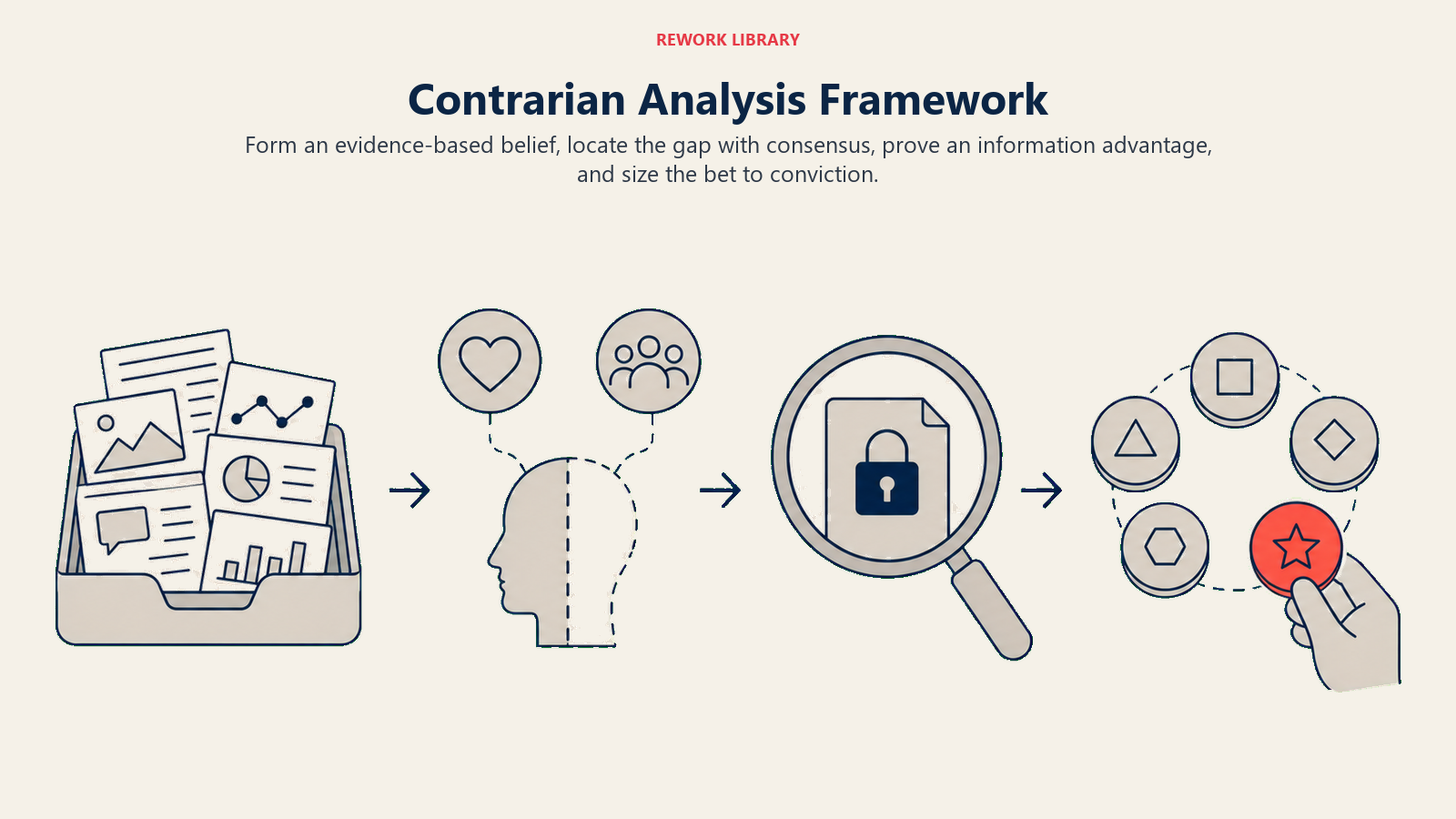

The components of contrarian analysis

Effective contrarian strategy is not about being skeptical of everything. It is about being disciplined in finding the specific situations where the market has mispriced an opportunity.

Form a belief about what is true. Start with first-principles analysis of what the data actually shows, separate from the interpretation that has been applied to it. What are customers actually doing, not what they say they want? What are the unit economics showing, separate from the revenue narrative? What is the operational data suggesting that the strategic narrative glosses over?

Identify where your belief differs from consensus. The gap between what you believe and what the market consensus believes is the potential source of strategic opportunity. If you believe a segment is structurally better positioned than consensus assumes, you are looking at a candidate for investment. If you believe a capability that competitors are building is overrated, you are identifying a place to redirect resources.

Assess your information advantage. Contrarian positions require a reason why you see something the market does not. The most durable reasons come from proprietary data (direct customer relationships, operational experience, or research that competitors lack), different analytical frameworks, or willingness to look at longer time horizons than market consensus normally rewards.

Size the bet appropriately to conviction. Not every contrarian view deserves a company-defining commitment. The discipline is to match the size of the bet to the strength of the evidence. Small bets on high-uncertainty contrarian hypotheses are often worth making as real options. Large bets should require a higher evidence bar and a clearer model of how you will be right and why the market will eventually recognize it.

Contrarian strategy in practice

| Situation | Consensus view | Contrarian question | What to investigate |

|---|---|---|---|

| Declining market | Category is mature, shrink to defend margins | Who is still growing in this market and why? | Segment-level data, customer churn drivers |

| Overhyped technology | This will transform everything within 3 years | Where does the hype exceed demonstrated value? | Adoption curves, actual use cases in production |

| Underrated capability | This is a nice-to-have, not a competitive factor | What if this becomes a requirement in 2 years? | Customer priority shifts, regulatory trends |

| Competitive threat | This new entrant can't reach our customers | What if they don't need our distribution model? | Entrant's go-to-market approach, customer acquisition data |

| Talent assumption | The best people want X in an employer | Is this preference stable or cohort-specific? | Longitudinal survey data, hiring outcomes |

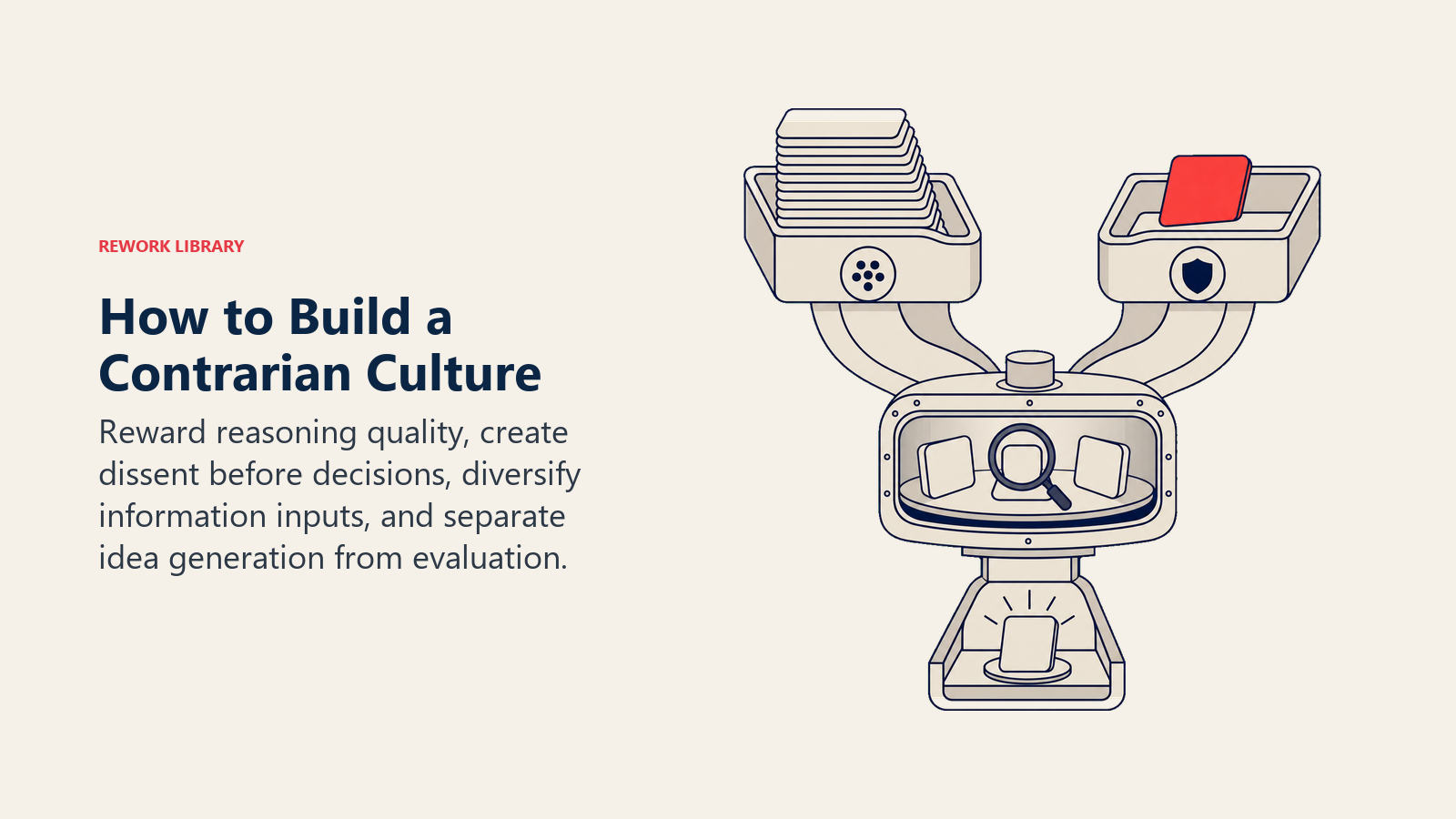

Building a contrarian culture

Individual contrarian insight is valuable. But building an organization that systematically generates contrarian analysis requires structural choices.

Reward the quality of reasoning, not just outcomes. Good contrarian bets fail sometimes. If leaders are only judged by outcomes, they will quickly learn to stop making contrarian bets. Organizations that want to generate contrarian insight need to evaluate decisions based on the quality of the analysis at the time it was made, not just whether it worked out.

Create space for dissent before decisions, not after. Most organizations produce conformity in the direction of whoever is senior. Pre-mortems, devil's advocate assignments, and red-teaming exercises force contrarian analysis into the decision process. Psychological safety is a prerequisite. If junior team members cannot challenge a senior leader's strategic assumptions without career risk, the organization will never surface the contrarian views that matter most.

Diversify information inputs deliberately. If everyone on the leadership team reads the same publications, attends the same conferences, and talks to the same advisors, the team will converge on consensus faster than any external analyst. Structural diversity in information diet, including sources from adjacent industries, academic research, and direct customer contact at all levels, slows convergence and surfaces alternative interpretations.

Separate idea generation from idea evaluation. The moment at which ideas are generated is different from the moment at which they should be evaluated. Organizations that criticize ideas at generation create pressure to propose only safe ideas. Separating the two processes allows contrarian hypotheses to surface before they have been pressure-tested and killed.

Risks and failure modes

Contrarian strategy has real failure modes that experienced leaders guard against.

Confusing contrarianism with correctness. Being different from consensus is not itself evidence of being right. Markets are often correct. The fact that an assumption is widely held is not a reason to dismiss it. Contrarian analysis requires positive evidence that the consensus is wrong, not just the observation that it exists.

Anchoring to a contrarian view too long. Conviction is necessary for contrarian strategy to pay off, but conviction needs to be responsive to new evidence. Leaders who develop a contrarian thesis and refuse to update it as market evidence comes in are not practicing contrarian strategy. They are practicing denial.

Taking contrarian positions publicly before the evidence is strong enough. There is an important difference between holding a contrarian hypothesis internally and staking the organization's public positioning on it. Premature public commitment narrows options and creates pressure to defend the position regardless of new information. The most effective contrarian strategy is often invisible to competitors until the position is already built.

Applying contrarian analysis to execution rather than strategy. Contrarian strategy applies to beliefs about markets, customers, and competitors. It does not apply to operational excellence. The counterintuitive pricing structure, the unconventional go-to-market approach, the overlooked customer segment: these are strategic contrarian bets. Doing performance management "contrarianism" or finance "contrarianism" is usually just an excuse for not running a tight operation.

How contrarian strategy connects to other frameworks

Contrarian strategy connects most directly to risk-based decision-making because every contrarian bet is fundamentally a bet that the market has mispriced risk in a specific situation. Understanding how to evaluate and size that bet requires a structured approach to uncertainty.

Strategic pivot timing is the execution question that follows a successful contrarian analysis: once you have identified that consensus is wrong and a different path is better, when and how do you make the move? Timing matters enormously. A correct contrarian view acted on too early loses money as competitors dismiss the approach. Acted on too late, it loses the advantage.

Platform strategy is one domain where contrarian analysis has historically produced the largest returns. Many platform businesses were built on the explicit belief that existing market leaders had fundamentally wrong models of how value would be created in their category.

Frequently Asked Questions about Contrarian Strategy

How do I know if my contrarian view is genuine analysis or just wishful thinking?

Genuine contrarian analysis starts with evidence that conflicts with consensus, not a desired conclusion. The test is whether you would update the position if specific evidence changed. If you cannot specify what evidence would make you wrong, you are not doing analysis. You are rationalizing.

Should contrarian strategy affect how I communicate with the board or investors?

Yes, but with care. Boards and investors operate in the same consensus ecosystem as everyone else. A contrarian strategic view requires more explanation, not less. You need to explain what the consensus is, why you believe it is wrong, and what evidence you have for your alternative view. This is harder than saying "we are aligned with industry direction," but it is the honest description of what a contrarian bet actually is.

How much of a portfolio should be contrarian bets vs consensus plays?

The answer depends on the business. Startups often need a high contrarian bet percentage because consensus-following in a new market usually means following incumbents with existing advantages. Established businesses with profitable core operations can afford to run a smaller percentage of their investment in contrarian bets. The exact mix matters less than making the distinction explicit: knowing which of your strategic choices are consensus-dependent and which are genuinely contrarian.

Is contrarian strategy the same as first-mover advantage?

Not exactly. First-mover advantage is about being early. Contrarian strategy is about being right about something the market has wrong. You can be a contrarian entrant into an established market by holding a different belief about how customers will evolve, even if you enter years after the market leaders. And you can be an early mover into a new market while still following consensus about what that market wants.

The leaders who build durable competitive advantage rarely do it by being better at the same game as their competitors. They do it by seeing something clearly that the market has missed, having the conviction to act on that view before the evidence is obvious to everyone, and building an organizational position that is hard to copy by the time the consensus catches up. That sequence, from insight to conviction to position, is what contrarian strategy actually looks like in practice. See what is leadership for the broader strategic leadership context, and succession planning for how contrarian views about talent markets shape long-term leadership decisions.