RevOps and Finance: How to Align Forecasting, Planning, and Revenue Data

Finance and RevOps both care about predictable revenue, but they approach it from different angles.

Finance owns the plan, budget, bookings targets, revenue recognition, cash discipline, scenario planning, and board reporting. RevOps owns the operating data, process, systems, and cadence that make revenue performance inspectable before the quarter is over.

When the partnership works, finance can trust the revenue system. When it breaks, finance builds shadow models, RevOps loses credibility, and leaders spend meetings reconciling numbers instead of deciding what to do.

The relationship should be simple: finance owns the financial model, RevOps owns the operating evidence, and both teams agree on the definitions that connect them.

McKinsey's research on B2B growth points to the pressure behind this partnership: growth is harder to sustain when commercial motions become more complex. Finance needs a clear plan. RevOps needs to make the operating reality visible early enough to act. Gartner has reported that fewer than half of sales leaders and sellers have high confidence in forecast accuracy, which is exactly the kind of system problem finance and RevOps should solve together.

Key operating facts

- Finance owns the plan, but RevOps owns much of the operating evidence behind the plan.

- Forecast quality depends on stage rules, close-date hygiene, manager inspection, and CRM trust.

- Pipeline coverage should be reviewed by segment, source, stage quality, and close period, not only total dollars.

- Board reporting needs stable definitions and visible caveats.

- A strong RevOps-finance partnership reduces shadow models and creates one planning conversation.

The division of ownership

The best relationship is not finance versus RevOps. It is plan owner plus operating system owner.

| Area | Finance owns | RevOps owns |

|---|---|---|

| Revenue plan | Target, budget, model assumptions | Operational inputs and conversion assumptions |

| Forecast | Financial rollup and scenario planning | Forecast process, CRM data quality, stage rules |

| Pipeline coverage | Target coverage expectations | Pipeline reporting and stage hygiene |

| Board reporting | Financial narrative | Operating metrics and source data |

| Systems | Billing and finance systems | CRM, revenue workflows, reporting definitions |

| Planning calendar | Financial planning milestones | Operating data readiness |

Finance should not have to police every CRM field. RevOps should not have to invent the financial plan. The two teams need a shared operating contract.

Why the partnership breaks

Finance and RevOps often disagree because they are answering different questions.

Finance asks:

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

- Will we hit the plan?

- What are the risks to bookings, revenue, cash, and margin?

- Which assumptions changed?

- What should the board hear?

- How much hiring or spend can the company support?

RevOps asks:

- Is the pipeline real?

- Are stages accurate?

- Are handoffs working?

- Are source, segment, and owner fields clean?

- Are managers inspecting the right risks?

- Can the CRM explain what leaders believe?

Both sides are right. The failure happens when these questions are not connected.

If finance only sees the plan, it may miss the operating reasons behind a miss. If RevOps only sees the CRM, it may miss the planning impact of bad data. The partnership should turn operating signals into planning judgment.

Forecast quality is a shared system

Forecast quality depends on more than rep judgment.

It depends on:

- Stage criteria

- Close-date hygiene

- Opportunity completeness

- Commit rules

- Manager inspection

- CRM data quality

- Sales leadership judgment

- Finance scenario assumptions

RevOps should govern the operating inputs. Finance should help define the planning output required. Sales leadership still owns the number, but the number must be inspectable.

This is why forecast governance should include finance context, not only sales process rules.

Shared forecast operating model

RevOps and finance should agree on the forecast operating model before the quarter is under pressure.

That model should include:

- Forecast categories and entry criteria

- Stage definitions and expected evidence

- Close-date hygiene rules

- Commit criteria

- Manager inspection expectations

- Rollup calendar

- Finance scenario assumptions

- Process for late-quarter changes

- Caveat rules for weak data

A practical weekly rhythm:

| Timing | RevOps role | Finance role |

|---|---|---|

| Before forecast call | Flag stale deals, weak stages, missing data, aging risk | Compare forecast to plan and prior scenarios |

| During forecast call | Support inspection and capture process issues | Listen for assumption changes and risk movement |

| After forecast call | Update data-quality actions and process fixes | Update scenario view and executive summary |

| Monthly review | Report forecast accuracy and hygiene trend | Compare forecast behavior to planning model |

The goal is not to make finance police the CRM. The goal is to prevent finance from needing a separate version of reality.

Pipeline coverage needs quality context

Finance often asks: do we have enough pipeline to hit the plan?

RevOps should answer with pipeline coverage by segment, source, motion, close period, and stage quality. A single coverage number is not enough. Three times coverage in weak early-stage pipeline is not the same as three times coverage in qualified late-stage opportunities.

Use pipeline coverage ratio with stage aging and win rate context.

| Coverage view | Why finance needs it |

|---|---|

| Coverage by quarter | Shows whether pipeline supports near-term plan |

| Coverage by segment | Shows whether enterprise, mid-market, or SMB risk differs |

| Coverage by source | Shows whether pipeline creation mix is healthy |

| Coverage by stage | Shows whether pipeline is mature enough |

| Coverage by owner | Shows manager or rep-level risk |

| Coverage by aging band | Shows stale pipeline that may not convert |

Pipeline coverage is useful only when it is adjusted for quality.

Planning inputs RevOps should provide

Finance planning improves when RevOps provides operating inputs, not just end-of-quarter results.

Useful inputs include:

- Pipeline creation by source, segment, region, and motion

- Conversion rates by lifecycle stage

- Sales cycle length by segment

- Win rate by source and deal size

- Average selling price movement

- Stage aging and slippage trend

- Lead-to-opportunity acceptance rates

- Renewal and expansion signals

- Rep capacity and ramp assumptions

- CRM data-quality caveats

These inputs should not be scattered across one-off dashboards. They should sit in a documented model that both teams understand.

See revenue data dictionary for how to define the fields behind these assumptions.

Board-ready reporting

Finance needs numbers that survive scrutiny.

RevOps should provide:

- Source-to-revenue performance

- Pipeline created versus target

- Forecast accuracy trend

- Conversion by stage

- Sales cycle trend

- Retention and expansion indicators

- Data-quality caveats

- Metric definition changes

The key is consistency. If definitions change every month, board reporting becomes storytelling without a stable base.

Board reporting partnership

Finance should own the board narrative. RevOps should make sure the operating evidence behind that narrative is stable.

For example, if the board deck says enterprise pipeline is improving, RevOps should be able to show:

- Which segment definition is being used

- How pipeline was sourced

- Whether stage distribution changed

- Whether aging risk improved or worsened

- Whether win rate assumptions are stable

- Whether pipeline creation is enough for future quarters

If the board deck says forecast accuracy improved, RevOps should show whether that came from better process or easier target setting. Those are different stories.

This is where source-of-truth discipline matters. Board metrics should not be rebuilt manually each month with silent definition changes. They should connect to source-of-truth revenue data and clear caveats.

Metric definition governance

Finance and RevOps should jointly govern metrics that affect planning or executive reporting.

Examples include:

- ARR

- Bookings

- Pipeline created

- Qualified pipeline

- Commit

- Best case

- Pipeline coverage

- Net revenue retention

- Gross revenue retention

- Expansion pipeline

- Churn reason

For each metric, define:

- Business meaning

- Data source

- Formula

- Owner

- Refresh cadence

- Known exclusions

- Where it appears in reporting

The definition does not need to be complicated. It needs to be stable.

When a metric changes, RevOps should document the change, finance should approve planning impact, and leaders should know whether historical comparisons are still valid.

Revenue planning calendar

The partnership works best when both teams share a calendar.

Common planning moments include:

- Annual plan build

- Quarterly target review

- Monthly forecast review

- Board reporting cycle

- Hiring capacity review

- Territory and quota planning

- Pipeline generation review

- Renewal and expansion forecast review

RevOps should prepare operating evidence before each planning moment. Finance should make clear which assumptions are needed and how they will be used.

This removes a common problem: finance asks for data at the last minute, RevOps rushes the pull, definitions are unclear, and everyone loses trust in the output.

Annual plan build workflow

The annual plan is where RevOps and finance should work together earliest.

A good planning workflow has stages.

| Stage | Finance needs | RevOps provides |

|---|---|---|

| Baseline | Prior-year actuals and financial model | Funnel, pipeline, win rate, cycle, and capacity history |

| Assumptions | Growth, hiring, spend, margin, cash view | Conversion, ramp, segment, source, and productivity assumptions |

| Stress test | Downside and upside scenarios | Pipeline coverage, capacity gaps, source risk, stage aging |

| Target setting | Bookings and revenue targets | Territory, quota, capacity, and pipeline requirements |

| Operating plan | Monthly or quarterly path | Cadence, dashboard, and inspection model |

RevOps should not wait until targets are final. If RevOps enters after the plan is set, the company may discover too late that pipeline creation, rep capacity, territory design, or conversion assumptions do not support the plan.

Forecast accuracy scorecard

Finance needs to know whether forecast quality is improving.

A practical scorecard includes:

- Forecast accuracy by quarter

- Forecast accuracy by segment

- Forecast accuracy by manager

- Commit conversion rate

- Best-case conversion rate

- Close-date slip rate

- Stage aging

- Amount change after commit

- Deals created and closed in the same period

- Forecast category changes after cutoff

This scorecard should not be used to embarrass managers. It should reveal which parts of the forecast system need better rules, coaching, or inspection.

Example: if one segment misses forecast because late-stage deals keep slipping, the fix may be stage criteria and close-date inspection. If another segment misses because commit deals shrink after finance cutoff, the fix may be discount governance or procurement-stage visibility.

Data caveats finance should expect

RevOps should bring caveats before finance finds the issue.

Useful caveats include:

- "Enterprise pipeline source is reliable after April 1, when source rules changed."

- "Expansion pipeline excludes customer-led expansion until CS opportunity creation is complete."

- "Forecast accuracy by manager is not comparable before the stage definition change."

- "Pipeline coverage includes renewal expansion only in the customer segment view."

- "Close-date push count is underreported before the CRM migration."

- "New logo ARR excludes multi-year services attached to first contract."

Caveats do not weaken the report. They show finance where the data can and cannot support planning decisions.

Create a finance-facing operating packet

RevOps can reduce ad hoc requests by maintaining a recurring finance packet.

The packet can include:

- Forecast summary

- Pipeline coverage by segment and quarter

- Pipeline creation versus target

- Conversion rates by stage

- Sales cycle trend

- Win rate by segment and source

- Rep capacity and ramp view

- Data-quality caveats

- Metric definition changes

- Open operating risks

This packet should be short enough to review monthly. It should not become a 40-page dashboard export. The point is to give finance the operating context needed to update scenarios and prepare leadership.

Align on scenario language

Finance often thinks in scenarios. RevOps often thinks in operating signals.

The partnership improves when both teams connect the two.

| Finance scenario | RevOps signal |

|---|---|

| Upside case | Best-case pipeline with strong stage evidence |

| Base case | Commit plus historically reliable conversion |

| Downside case | Commit risk, close-date slip, weak late-stage coverage |

| Hiring acceleration | Rep capacity, ramp curve, territory readiness |

| Spend reduction | Source efficiency, pipeline creation risk, conversion trend |

This helps RevOps understand why finance asks for certain cuts of the data. It also helps finance see which operating signals should change scenario confidence.

Capacity and hiring assumptions

Finance often needs RevOps most when headcount, quota, and pipeline assumptions meet.

For sales capacity planning, RevOps should provide:

- Rep count by role

- Ramp assumptions

- Quota capacity

- Attainment distribution

- Pipeline per rep

- Territory or segment capacity

- Conversion assumptions

- Sales cycle by motion

- Manager span

Finance can model hiring and spend only if the operating assumptions are credible. RevOps should also show where assumptions are weak. A planning model built on optimistic ramp or stale conversion rates creates downstream pressure later.

Compensation and crediting

Finance and RevOps also meet around compensation.

Compensation plans depend on clean rules:

- Which bookings count?

- Which products count?

- How are expansions credited?

- How are split deals handled?

- What happens when account ownership changes?

- Which source of truth decides customer status?

- How are clawbacks handled?

RevOps should not own compensation design alone, but it often owns the data and process that calculate credit. If CRM ownership, opportunity source, close date, or product fields are weak, compensation disputes increase.

Billing and closed-won handoff

Finance depends on clean closed-won handoff.

Closed-won data should support:

- Billing setup

- Contract review

- Customer status

- Revenue start date

- Product and package

- Discount treatment

- Payment terms

- Renewal date

- Implementation or onboarding risk

If sales closes a deal but finance cannot bill it without manual follow-up, the revenue process is not complete. RevOps should treat billing handoff as part of the revenue operating model, not a finance-only cleanup task.

When finance should challenge RevOps

Finance should challenge RevOps when:

- Forecast categories do not match deal behavior

- Close dates move repeatedly without explanation

- Pipeline coverage looks healthy but conversion is weak

- Dashboard definitions change without governance

- Source attribution does not match spend decisions

- CRM data quality caveats are not visible in executive reporting

These challenges are healthy when they focus on the system. They become unhealthy when finance treats the CRM as useless or RevOps treats planning questions as interference.

The best posture is shared skepticism. Finance pressure-tests the plan. RevOps pressure-tests the operating evidence.

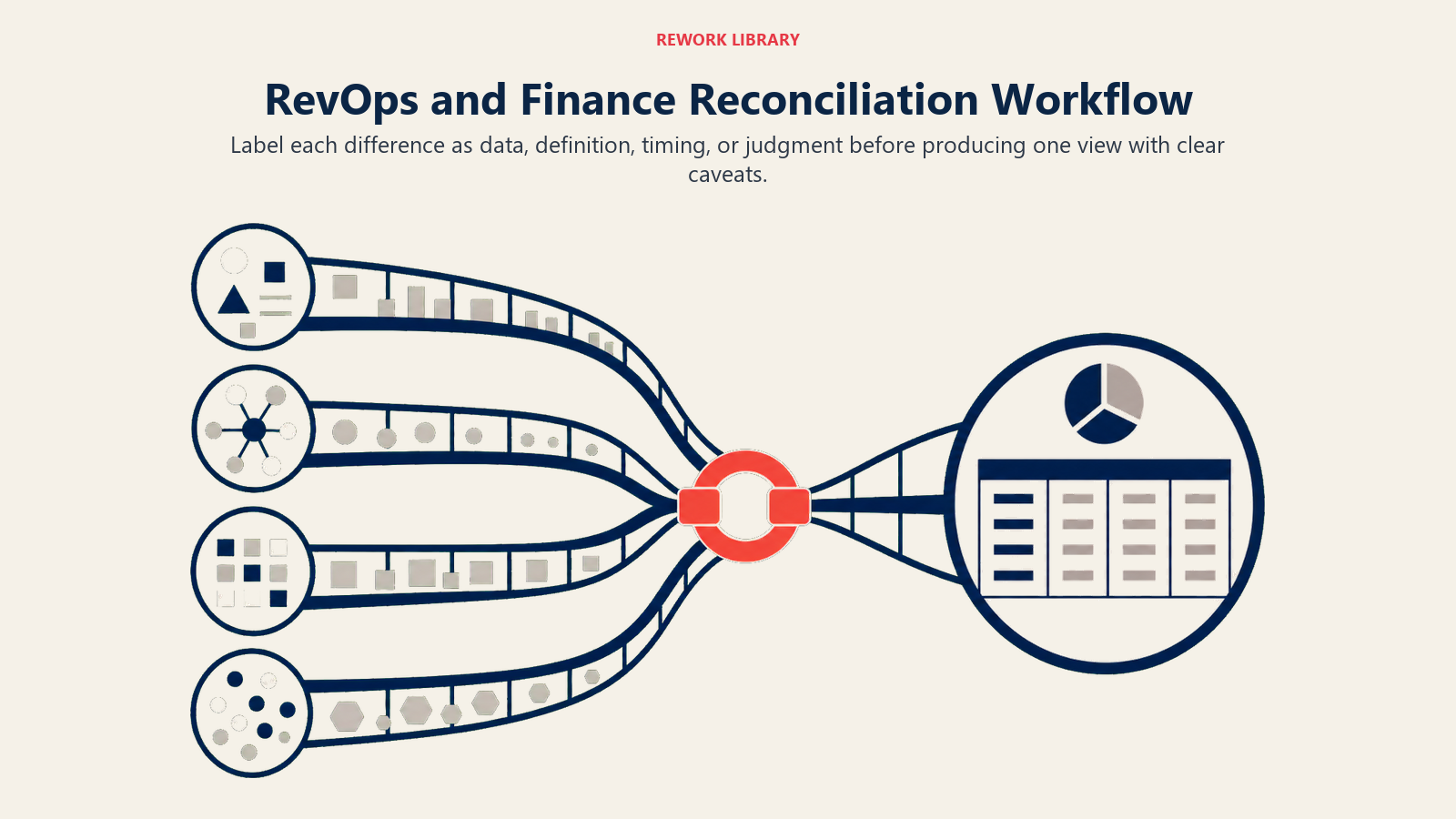

Reconciliation workflow

Finance and RevOps should reconcile numbers before executive meetings, not during them.

A practical workflow:

- RevOps prepares the operating view from CRM and revenue systems.

- Finance prepares the plan view and prior forecast assumptions.

- Both teams compare definitions, time periods, exclusions, and segment cuts.

- Differences are labeled as data issue, definition issue, timing issue, or judgment issue.

- RevOps fixes operating data issues or documents caveats.

- Finance updates planning scenarios or documents assumptions.

- Leaders receive one view with clear caveats.

The labels matter.

A data issue means records are wrong or incomplete. A definition issue means teams are using different rules. A timing issue means one system is fresher than another. A judgment issue means the data is correct, but leaders disagree on likelihood.

Treating all differences as "bad data" creates noise. The partnership improves when the teams can name the kind of difference they are seeing.

What RevOps should bring to finance

RevOps should bring more than dashboards.

Useful finance-facing outputs include:

- A monthly data-quality note

- Funnel conversion trend with caveats

- Pipeline coverage by quality band

- Forecast accuracy by manager or segment

- Stage slippage analysis

- Closed-won handoff completeness

- Renewal and expansion risk summary

- Changes to metric definitions

- Upcoming systems changes that affect reporting

These outputs help finance model the business with better judgment. They also show where operating fixes can improve future planning.

What finance should bring to RevOps

Finance should bring planning context that helps RevOps prioritize.

Useful inputs include:

- Which assumptions drive the plan

- Which segments carry the most risk

- Which board metrics need stable definitions

- Which forecast changes affect hiring or spend

- Which pipeline gaps matter most by quarter

- Which revenue motions are under review

This prevents RevOps from optimizing low-value workflows while high-value planning risks sit unresolved.

For example, a field cleanup project may seem useful. But if finance is trying to understand whether enterprise pipeline can support next quarter's hiring plan, RevOps may need to prioritize stage hygiene and coverage analysis first.

Partnership checklist

Use this checklist in the monthly RevOps-finance review:

- Are forecast categories still being used consistently?

- Did any metric definitions change?

- Are board metrics tied to documented data sources?

- Which pipeline segments carry the most plan risk?

- Are close dates and stage aging improving or getting worse?

- Does finance trust the CRM view enough to use it in planning?

- Does RevOps understand which assumptions finance is pressure-testing?

- Are renewal and expansion signals included where they affect the plan?

The review should end with a short action list. Some actions belong to RevOps, such as fixing stage hygiene or documenting a metric. Some belong to finance, such as updating scenario assumptions. Some belong to sales or customer success leadership, such as improving manager inspection or handoff compliance.

Common failure modes

Finance builds a shadow model and stops trusting the CRM. This may feel faster, but it removes pressure to fix the operating system.

RevOps defends CRM data without caveats. If the data is incomplete, RevOps should say so clearly. Trust grows when caveats are visible.

Sales changes forecast categories without finance context. This breaks planning comparability.

Board metrics use different definitions from operating dashboards. Leaders then spend time explaining mismatches instead of performance.

Pipeline coverage ignores stage quality. A large early-stage number can hide weak late-stage conversion.

Renewal and expansion signals are excluded from planning. In recurring revenue, post-sale data belongs in revenue planning.

What good looks like

The partnership is working when finance no longer needs to rebuild the revenue story from scratch, and RevOps no longer has to guess which operating fixes matter most to the plan.

Forecast calls produce planning insight, not only deal updates. Board metrics match operating dashboards. Pipeline coverage includes quality. Sales capacity planning uses real conversion and ramp assumptions. Data caveats are visible before leaders make decisions.

That is the practical goal: one planning conversation backed by one operating system, with clear caveats when the data is not yet good enough.

Maturity model

| Stage | Behavior | RevOps-finance move |

|---|---|---|

| Reconciliation | Teams compare numbers after conflict appears | Create shared definitions |

| Reporting | RevOps provides dashboards and finance adjusts models | Add caveats and planning inputs |

| Operating partnership | Forecast, pipeline, and planning assumptions are reviewed together | Run monthly review cadence |

| Trusted planning system | Finance uses operating data directly in planning | Maintain source-of-truth model and governance |

Most teams move forward by reducing shadow models. That requires better definitions, clearer caveats, and a regular review rhythm.

Finance alignment packet

RevOps and finance should maintain a shared packet for planning conversations.

Include:

- Forecast definition and category rules.

- Pipeline coverage assumptions.

- Sales capacity assumptions.

- Revenue recognition caveats.

- Renewal and expansion forecast logic.

- Data caveats.

- Manual adjustments and reasons.

- Owner for each assumption.

This reduces shadow modeling. Finance can still challenge assumptions, but both teams should know which operating data produced the plan.

Frequently Asked Questions about RevOps and Finance

Should finance own RevOps?

Sometimes RevOps reports to finance, especially in companies where planning discipline is the main issue. But RevOps still needs strong partnership with CRO, sales, marketing, and customer success leadership.

Who owns forecast accuracy?

Sales owns the forecast outcome, RevOps owns the process and data quality, and finance owns planning implications. All three need a shared cadence.

Why does finance distrust CRM data?

Usually because stage definitions, close dates, required fields, and forecast categories are inconsistent. That is a RevOps governance problem, not only a user behavior problem.

What should RevOps and finance review monthly?

Forecast quality, pipeline coverage, metric definition changes, data-quality caveats, plan risks, and operating fixes that affect future planning.

Learn more

Senior Operations & Growth Strategist

On this page

- The division of ownership

- Why the partnership breaks

- Forecast quality is a shared system

- Shared forecast operating model

- Pipeline coverage needs quality context

- Planning inputs RevOps should provide

- Board-ready reporting

- Board reporting partnership

- Metric definition governance

- Revenue planning calendar

- Annual plan build workflow

- Forecast accuracy scorecard

- Data caveats finance should expect

- Create a finance-facing operating packet

- Align on scenario language

- Capacity and hiring assumptions

- Compensation and crediting

- Billing and closed-won handoff

- When finance should challenge RevOps

- Reconciliation workflow

- What RevOps should bring to finance

- What finance should bring to RevOps

- Partnership checklist

- Common failure modes

- What good looks like

- Maturity model

- Finance alignment packet

- Learn more