BCG Matrix vs. GE-McKinsey-Matrix im Vergleich

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Die Debatte BCG Matrix vs. GE-McKinsey-Matrix läuft auf Geschwindigkeit versus Differenziertheit hinaus. Beide Tools helfen Führungskräften dabei zu entscheiden, wo sie innerhalb eines Unternehmensportfolios investieren, halten oder desinvestieren sollen. Sie beantworten diese Frage jedoch auf sehr unterschiedliche Weise. Das falsche Tool für Ihre Situation zu wählen, kostet Zeit oder führt schlimmstenfalls zu einer irreführenden Empfehlung.

Was ist der Unterschied zwischen der BCG- und der GE-McKinsey-Matrix?

Beide sind Portfolioanalyse-Frameworks, die zur Kapital- und Ressourcenzuweisung auf Geschäftseinheiten oder Produktlinien eingesetzt werden. Die BCG Matrix (entwickelt von der Boston Consulting Group) verwendet ein einfaches 2x2-Raster mit zwei Achsen: Marktwachstumsrate und relativer Marktanteil. Sie ordnet jede Einheit einem von vier Quadranten zu: Stars, Cash Cows, Question Marks oder Dogs. Die GE-McKinsey-Matrix verwendet ein 3x3-Raster, das Einheiten nach Branchenattraktivität und Wettbewerbsstärke bewertet, wobei jede Dimension aus mehreren gewichteten Faktoren zusammengesetzt wird. Diese reichhaltigere Struktur ermöglicht feinere Unterscheidungen, erfordert aber auch mehr Daten und mehr Urteilsvermögen.

Wichtige Fakten

- Die BCG Matrix wurde 1970 von Bruce Henderson bei der Boston Consulting Group entwickelt und gehört damit zu den ältesten formalen Portfolio-Planungstools, die noch immer weit verbreitet sind. (Quelle: BCG, 1970)

- Die GE-McKinsey-Matrix wurde von McKinsey and Company für General Electric Anfang der 1970er Jahre als direkte Reaktion auf die Einschränkungen des BCG-Rasters entwickelt, insbesondere auf die Notwendigkeit, mehr Faktoren als nur Wachstum und Anteil zu erfassen. (Quelle: McKinsey, 1971)

- Ende der 1970er Jahre wurden Portfolio-Planungsframeworks von etwa der Hälfte aller Fortune-500-Unternehmen genutzt, wie eine im Journal of Business Strategy zitierte Studie belegt (Haspeslagh, 1982).

- Ein prägnanter Merksatz: „Die BCG Matrix stellt zwei Fragen schnell; die GE-McKinsey-Matrix stellt ein Dutzend sorgfältig."

Was ist die BCG Matrix?

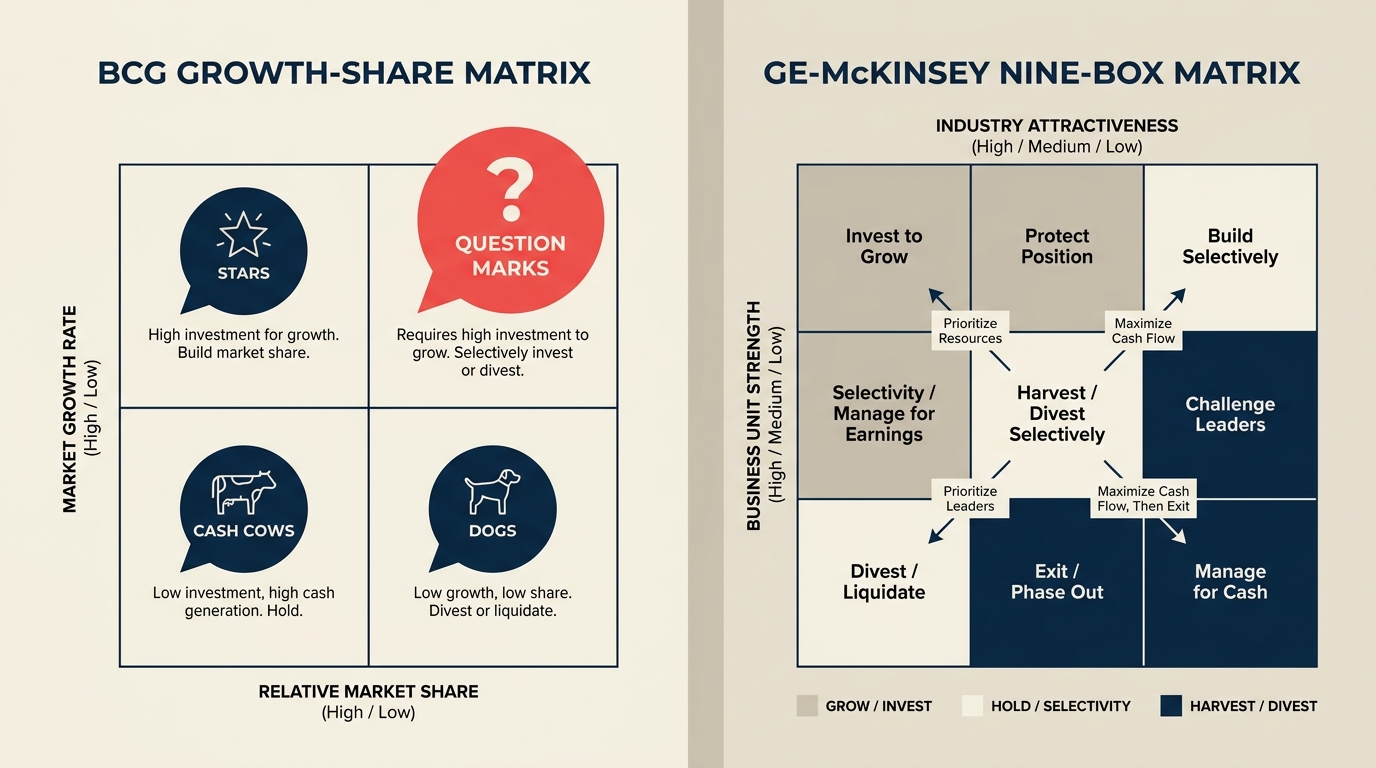

Die BCG Matrix ist ein zweidimensionales Raster, das eine Geschäftseinheit oder ein Produkt nach Marktwachstumsrate (vertikale Achse) im Verhältnis zum relativen Marktanteil (horizontale Achse) darstellt. Jede Achse wird an einem Schwellenwert unterteilt, wodurch vier Zellen entstehen.

Stars (hohes Wachstum, hoher Anteil): Einheiten, die in wachsenden Märkten führend sind. Sie verbrauchen Kapital, um das Wachstum zu erhalten, sollen aber mit zunehmender Marktreife zu Cash Cows werden.

Cash Cows (geringes Wachstum, hoher Anteil): Marktführer in reifen Märkten. Sie generieren mehr Kapital als sie verbrauchen und sind damit die primäre Finanzierungsquelle des Portfolios.

Question Marks (hohes Wachstum, geringer Anteil): Einheiten in schnell wachsenden Märkten ohne dominanten Marktanteil. Die Entscheidung lautet: Investieren, um ein Star zu werden, oder aussteigen.

Dogs (geringes Wachstum, geringer Anteil): Einheiten in stagnierenden Märkten ohne Wettbewerbsvorteil. Klassische Kandidaten für Desinvestitionen, obwohl einige stetige Nischenerträge erzielen.

Die BCG Matrix lässt sich schnell anwenden. Sie benötigen zwei Datenpunkte pro Einheit: die Wachstumsrate des Marktes und den Anteil der Einheit relativ zu ihrem größten Konkurrenten. Diese Einfachheit ist ihr größter Vorteil und ihre größte Einschränkung.

Was ist die GE-McKinsey-Matrix?

Die GE-McKinsey-Matrix ist ein 3x3-Raster, das jede Geschäftseinheit auf zwei zusammengesetzten Dimensionen bewertet: Branchenattraktivität (vertikale Achse) und Wettbewerbsstärke (horizontale Achse). Jede Dimension fasst mehrere Faktoren zusammen.

Faktoren der Branchenattraktivität umfassen typischerweise Marktgröße, Wachstumsrate, Gewinnmargen, Wettbewerbsintensität, technologische Anforderungen sowie ökologische und regulatorische Faktoren. Faktoren der Wettbewerbsstärke beinhalten Marktanteil, Markenstärke, Produktionskapazität, Gewinnmargen im Vergleich zu Wettbewerbern und technologische Kompetenz.

Jedem Faktor wird ein Gewicht zugewiesen und anschließend auf einer Skala von 1 bis 5 bewertet. Der gewichtete Durchschnitt positioniert jede Einheit auf dem 3-Punkte-Maßstab (niedrig, mittel, hoch) für jede Achse.

Das 3x3-Raster ergibt drei strategische Zonen.

Investieren und Wachsen (obere linke Zellen, hohe Attraktivität und hohe Stärke): Ressourcen einsetzen, Wachstum aggressiv verfolgen.

Selektivität (mittlere Diagonalzellen, mindestens eine Achse mittel): Selektiv investieren, spezifische Schwächen verbessern oder Position halten.

Ernten oder Desinvestieren (untere rechte Zellen, geringe Attraktivität und geringe Stärke): Für Kapitalfluss managen, dann aussteigen, sofern kein klarer Verbesserungspfad besteht.

Da die Bewertung Urteilsvermögen erfordert, können zwei Teams zu unterschiedlichen Platzierungen für dieselbe Einheit gelangen. Diese Subjektivität ist die am häufigsten genannte Schwäche der GE-McKinsey-Matrix.

BCG vs. GE-McKinsey: Gegenüberstellung

| Dimension | BCG Matrix | GE-McKinsey-Matrix |

|---|---|---|

| Rastergröße | 2x2 (4 Zellen) | 3x3 (9 Zellen) |

| Vertikale Achse | Marktwachstumsrate | Branchenattraktivität (zusammengesetzt) |

| Horizontale Achse | Relativer Marktanteil | Wettbewerbsstärke (zusammengesetzt) |

| Anzahl der Faktoren | 2 (einer pro Achse) | Viele (typischerweise 6-12 gewichtete Faktoren pro Achse) |

| Komplexität | Gering | Hoch |

| Subjektivität | Gering (datengetrieben) | Hoch (Gewichtungen und Bewertungen sind urteilsabhängig) |

| Am besten geeignet für | Große Portfolios mit schnellem Screening-Bedarf; frühe Priorisierung | Diversifizierte Konzerne; Entscheidungen mit erheblichem Kapitaleinsatz |

| Haupteinschränkung | Ignoriert Rentabilität, Markenstärke, Synergien und viele andere Variablen | Faktorgewichtungen können manipuliert werden; zeitaufwendig in der Anwendung |

| Ergebnis | Quadranten-Bezeichnung mit implizierter Strategie | Zonenposition mit priorisierter Investitionsguidance |

| Entwickelt von | Bruce Henderson, BCG, 1970 | McKinsey für General Electric, frühe 1970er Jahre |

Wann welche Matrix einsetzen

Verwenden Sie die BCG Matrix, wenn:

- Sie einen schnellen Erstdurchlauf eines großen Portfolios benötigen.

- Daten zu Marktwachstum und Marktanteil leicht verfügbar und zuverlässig sind.

- Das Publikum ein einfach kommunizierbares Framework benötigt (Board-Präsentationen, Investoren-Präsentationen).

- Sie in einer einzelnen Branche arbeiten, in der der Marktanteil stark mit der Rentabilität korreliert.

Verwenden Sie die GE-McKinsey-Matrix, wenn:

- Das Portfolio mehrere Branchen mit sehr unterschiedlichen Attraktivitätsprofilen umfasst.

- Eine Entscheidung genügend Kapital auf dem Spiel hat, um den zusätzlichen Bewertungsaufwand zu rechtfertigen.

- Der Marktanteil allein kein guter Indikator für die Wettbewerbsposition ist (Dienstleistungen, B2B, regulierte Branchen).

- Sie Nuancen aufdecken müssen, die ein 2x2-Raster verbergen würde, etwa eine kleine Einheit in einer hochattraktiven Nische.

Viele Strategieteams führen zuerst eine BCG-Analyse für einen breiten Überblick durch und wenden die GE-McKinsey-Matrix dann auf die zwei oder drei Einheiten an, bei denen die BCG-Analyse ein mehrdeutiges oder umstrittenes Signal liefert.

Wie man eine Matrix auswählt und anwendet

Schritt 1: Analyseeinheiten definieren

Listen Sie alle Geschäftseinheiten, Produktlinien oder Marken auf, die Sie bewerten möchten. Stellen Sie sicher, dass jede eine vertretbare Marktdefinition hat. Ohne diese werden die Achsen beider Matrizen bedeutungslos. Für die BCG Matrix berechnen Sie den relativen Marktanteil jeder Einheit (Anteil Ihrer Einheit geteilt durch den Anteil des größten Konkurrenten). Für die GE-McKinsey-Matrix listen Sie die Faktoren auf, die Sie zur Bewertung von Attraktivität und Stärke verwenden werden, und einigen Sie sich auf Gewichtungen, bevor die Bewertung beginnt.

Schritt 2: Matrix passend zur Entscheidungskomplexität wählen

Wenn Sie eine vollständige Portfolioüberprüfung eines diversifizierten Konzerns durchführen, wählen Sie standardmäßig die GE-McKinsey-Matrix. Wenn Sie Produktinvestitionen in einem einzelnen Markt priorisieren, reicht die BCG Matrix in der Regel aus. Starten Sie im Zweifelsfall mit der BCG Matrix für den Überblick, und nutzen Sie dann die Analyse des Wettbewerbsvorteils oder Porter's Five Forces, um Einheiten zu vertiefen, die unentschieden nahe der Mitte liegen.

Schritt 3: Achsen bewerten

Für die BCG Matrix: Plotten Sie jede Einheit nach Wachstumsrate im Vergleich zum relativen Marktanteil. Ziehen Sie die Trennlinien beim branchendurchschnittlichen Wachstum und bei 1,0 für den relativen Anteil. Für die GE-McKinsey-Matrix: Bewerten Sie jeden Faktor für jede Einheit, wenden Sie Gewichtungen an, berechnen Sie den zusammengesetzten Wert und platzieren Sie die Einheit im 3x3-Raster. Dokumentieren Sie Ihre Gewichtungen und Bewertungen, damit Stakeholder Annahmen hinterfragen können statt Schlussfolgerungen.

Schritt 4: Strategieimplikation pro Zelle ablesen

BCG-Zellen tragen implizite Strategien: in Stars investieren, Cash Cows melken, bei Question Marks schnell entscheiden und Dogs aussteigen, sofern kein strategischer Grund für deren Beibehaltung besteht. GE-McKinsey-Zonen folgen einer ähnlichen Logik, jedoch mit mehr Abstufung: Einheiten in der mittleren Diagonale erfordern eine ehrliche Einschätzung, ob ein Weg in die Invest-Zone existiert. Kombinieren Sie das Matrix-Ergebnis mit der Ansoff-Matrix, um Wachstumsoptionen konkret zu machen.

Beispiel

Angenommen, ein Konsumgüterunternehmen hat fünf Produktlinien: Premium-Kaffee, Eigenmarken-Cerealien, Sprudelwasser, pflanzliche Snacks und eine rückläufige Konservensuppen-Linie.

BCG-Platzierungen:

| Produkt | Marktwachstum | Relativer Anteil | Quadrant |

|---|---|---|---|

| Premium-Kaffee | Hoch (12%) | Hoch (1,4x Marktführer) | Star |

| Pflanzliche Snacks | Hoch (18%) | Gering (0,3x Marktführer) | Question Mark |

| Sprudelwasser | Mittel (6%) | Hoch (1,1x Marktführer) | Cash Cow (Grenzfall) |

| Eigenmarken-Cerealien | Gering (2%) | Mittel (0,8x Marktführer) | Dog (Grenzfall) |

| Konservensuppe | Gering (1%) | Gering (0,5x Marktführer) | Dog |

GE-McKinsey-Platzierungen (vereinfacht):

| Produkt | Branchenattraktivität | Wettbewerbsstärke | Zone |

|---|---|---|---|

| Premium-Kaffee | Hoch (4,2/5) | Hoch (4,0/5) | Investieren und Wachsen |

| Pflanzliche Snacks | Hoch (4,5/5) | Gering (2,1/5) | Selektivität |

| Sprudelwasser | Mittel (3,1/5) | Mittel (3,4/5) | Selektivität |

| Eigenmarken-Cerealien | Mittel (2,8/5) | Mittel (2,9/5) | Selektivität (beobachten) |

| Konservensuppe | Gering (1,8/5) | Gering (2,0/5) | Ernten oder Desinvestieren |

Die GE-McKinsey-Analyse zeigt, dass Sprudelwasser in der Selektivitätszone liegt und nicht als klare Cash Cow einzustufen ist, was eine genauere Betrachtung erfordert, ob die Wettbewerbsposition der Einheit nachlässt. Die BCG Matrix allein hätte „halten und ernten" empfohlen, was möglicherweise die falsche Entscheidung wäre.

Häufige Fehler

BCG-Achsen als einzige Treiber behandeln. Marktanteil ist eine nützliche Faustregel, aber kein vollständiges Bild der Wettbewerbsposition. Eine Einheit mit geringem Anteil in einem fragmentierten Markt kann hochprofitabel sein. Überprüfen Sie BCG-Ergebnisse stets mit tatsächlichen Margen- und Cashflow-Daten. Nutzen Sie SWOT-Analyse oder eine PESTEL-Analyse, um den Kontext zu überprüfen.

Falsche Präzision beim GE-McKinsey-Scoring. Da die Matrix gewichtete Scores auf eine oder zwei Dezimalstellen ergibt, behandeln Teams die Ergebnisse manchmal als objektiver, als sie tatsächlich sind. Ein Wert von 3,2 vs. 3,4 bei der Branchenattraktivität ist nicht statistisch bedeutsam, wenn die Faktoren von einem einzelnen Analysten bewertet wurden. Einigen Sie sich auf Faktordefinitionen und Gewichtungen, bevor das Scoring beginnt, nicht danach.

Den „Was bedeutet das?" Schritt überspringen. Beide Matrizen liefern eine Platzierung, keine Entscheidung. Die Zuweisung zu einem Quadranten oder einer Zone ist der Beginn des strategischen Gesprächs, nicht sein Ende. Verbinden Sie das Ergebnis mit einem Ressourcenzuweisungsgespräch, das auf finanzielle Ziele ausgerichtet ist.

Portfolio-Interdependenzen ignorieren. Keine der Matrizen berücksichtigt Synergien zwischen Einheiten, etwa gemeinsame Produktion, Marken-Halo oder Distributionsnetzwerk. Ein Dog, der Kunden an einen Star weiterleitet, kann eine Beibehaltung rechtfertigen, auch wenn die Matrix Desinvestition empfiehlt.

Häufig gestellte Fragen

Ist die GE-McKinsey-Matrix besser als die BCG Matrix? Nicht kategorisch. Die GE-McKinsey-Matrix erfasst mehr Variablen und liefert differenziertere Ergebnisse, aber diese Tiefe geht mit mehr Subjektivität und mehr Aufwand einher. Für schnelle Screenings oder Single-Industry-Portfolios ist die BCG Matrix oft die bessere Wahl. Für Multi-Industry-Konzerne, die große Kapitalallokationsentscheidungen treffen, rechtfertigt die GE-McKinsey-Matrix ihre Komplexität.

Wer hat die BCG Matrix entwickelt? Bruce Henderson, Gründer der Boston Consulting Group, entwickelte die BCG Matrix im Jahr 1970. Sie basiert auf der Beobachtung, dass Erfahrungskurveneffekte dazu führen, dass Kosten mit steigendem kumulierten Produktionsvolumen vorhersehbar sinken, was den relativen Marktanteil zu einem sinnvollen Indikator für Kosteneffizienz macht.

Was sind die zwei Achsen der GE-McKinsey-Matrix? Branchenattraktivität (vertikal) und Wettbewerbsstärke (horizontal). Jede Achse ist ein zusammengesetzter, über mehrere Faktoren gewichteter Wert, was das Tool von den Einzelfaktor-Achsen der BCG Matrix unterscheidet.

Können Sie beide Matrizen zusammen verwenden? Ja, und viele Strategieteams tun dies. Ein verbreiteter Ansatz besteht darin, die BCG Matrix für ein breites Portfolio-Screening zu verwenden, die Einheiten zu identifizieren, die in mehrdeutigen oder umstrittenen Positionen liegen, und dann die GE-McKinsey-Matrix speziell auf diese Einheiten anzuwenden, um eine tiefere Analyse durchzuführen.

Was hat die BCG Matrix ersetzt? Nichts hat sie vollständig ersetzt, da Einfachheit weiterhin wertvoll ist. Einige Teams sind zu ganzheitlicheren Portfolio-Modellen übergegangen, die Rentabilität, Customer Lifetime Value oder optionsbasiertes Denken einbeziehen, aber BCG und GE-McKinsey bleiben die Referenz-Frameworks, die in Business Schools gelehrt und in Boardroom-Diskussionen verwendet werden. Beide erscheinen neben Tools wie der SWOT vs. TOWS-Analyse und PESTEL vs. SWOT in modernen Strategie-Toolkits.

Die Wahl zwischen BCG und GE-McKinsey spiegelt letztendlich wider, wie viel Präzision eine Entscheidung erfordert. Beginnen Sie mit dem einfacheren Tool, prüfen Sie die Ergebnisse kritisch, und wechseln Sie zur GE-McKinsey-Matrix, wenn der Einsatz oder die Komplexität des Portfolios den zusätzlichen Aufwand rechtfertigt.

Weiterführende Artikel

Senior Operations & Growth Strategist

On this page

- Was ist der Unterschied zwischen der BCG- und der GE-McKinsey-Matrix?

- Was ist die BCG Matrix?

- Was ist die GE-McKinsey-Matrix?

- BCG vs. GE-McKinsey: Gegenüberstellung

- Wann welche Matrix einsetzen

- Wie man eine Matrix auswählt und anwendet

- Schritt 1: Analyseeinheiten definieren

- Schritt 2: Matrix passend zur Entscheidungskomplexität wählen

- Schritt 3: Achsen bewerten

- Schritt 4: Strategieimplikation pro Zelle ablesen

- Beispiel

- Häufige Fehler

- Häufig gestellte Fragen

- Weiterführende Artikel