More in

AI Workforce Transformation

What AI-Native New Hires Actually Expect (And Why Most Companies Aren't Ready)

Jun 12, 2026

What an AI-Native CRM Actually Looks Like for Mid-Market Companies

Jun 12, 2026

How to Get Finance to Approve Your AI PoC: A Practical Guide for Executives

Jun 12, 2026

How CFOs Should Measure AI Investment Returns in Mid-Market Companies

Jun 12, 2026 · Currently reading

Why Peer-Led AI Programs Outperform Top-Down Training Rollouts

Jun 12, 2026

RevOps and AI: Why Data Alignment Comes Before Tool Deployment

Jun 12, 2026

Which Roles AI Is Actually Eliminating in Mid-Market Companies (and Which It's Creating)

Apr 14, 2026

The CAIO Is Not a Fad: Why Mid-Market Companies Are Appointing AI Executives

Apr 14, 2026

The AI Skills Gap Executives Are Getting Wrong

Apr 14, 2026

Why Every Sales and Marketing Hire in 2026 Needs AI Fluency

Apr 14, 2026

How CFOs Should Measure AI Investment Returns in Mid-Market Companies

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

The standard ROI calculation breaks when you apply it to AI investments. Not because AI doesn't generate returns, but because its returns land in categories that traditional financial models weren't built to capture.

Most CFOs are discovering this problem the hard way. They approved an AI pilot based on a projected time savings number, the pilot ran, employees reported that it was useful, and now nobody can find the time savings in the P&L. The hours didn't get turned into headcount reductions. The quality improvements didn't show up as revenue. And the CFO is sitting in a board meeting trying to explain what they got for $200,000.

This is an accounting problem as much as a technology problem. AI generates real value. But CFOs who try to measure it using the same frameworks they use for equipment purchases or SaaS subscriptions will consistently understate returns on successful investments and struggle to build the case for the next one.

Why Traditional ROI Models Fail for AI

The classical ROI model assumes a direct causal chain: investment produces output, output has a measurable dollar value, payback period is output divided by investment. This works when you're buying a machine that produces a countable widget. It breaks when the output is "better decisions" or "faster information access."

AI investments usually produce returns in three forms that don't map cleanly to the model.

Capacity returns. AI allows existing headcount to handle more volume or more complexity without adding people. The return is real, but it shows up as avoided cost rather than reduced cost, which doesn't appear on a P&L unless you're comparing to a headcount plan that was actually on the table. If the team was never going to add a person anyway, the CFO can't point to a cost avoidance number.

Quality returns. AI reduces errors, improves consistency, and raises the floor on work quality. But measuring quality improvement requires a baseline, and most companies don't have one. You don't know what your error rate was before AI until you measure it during a pilot. Retrospective measurement is possible but requires effort most finance teams don't invest in.

Speed returns. AI compresses cycle times. Contracts get reviewed faster. Reports get generated sooner. Responses go out in hours instead of days. Speed has real commercial value in most revenue-facing functions, but converting cycle time savings to dollar returns requires knowing the revenue impact of faster decision-making, which is a harder measurement than it sounds.

None of these are reasons to abandon measurement. They're reasons to build a better measurement model before committing to an AI investment, not after.

A CFO-Ready AI Returns Framework

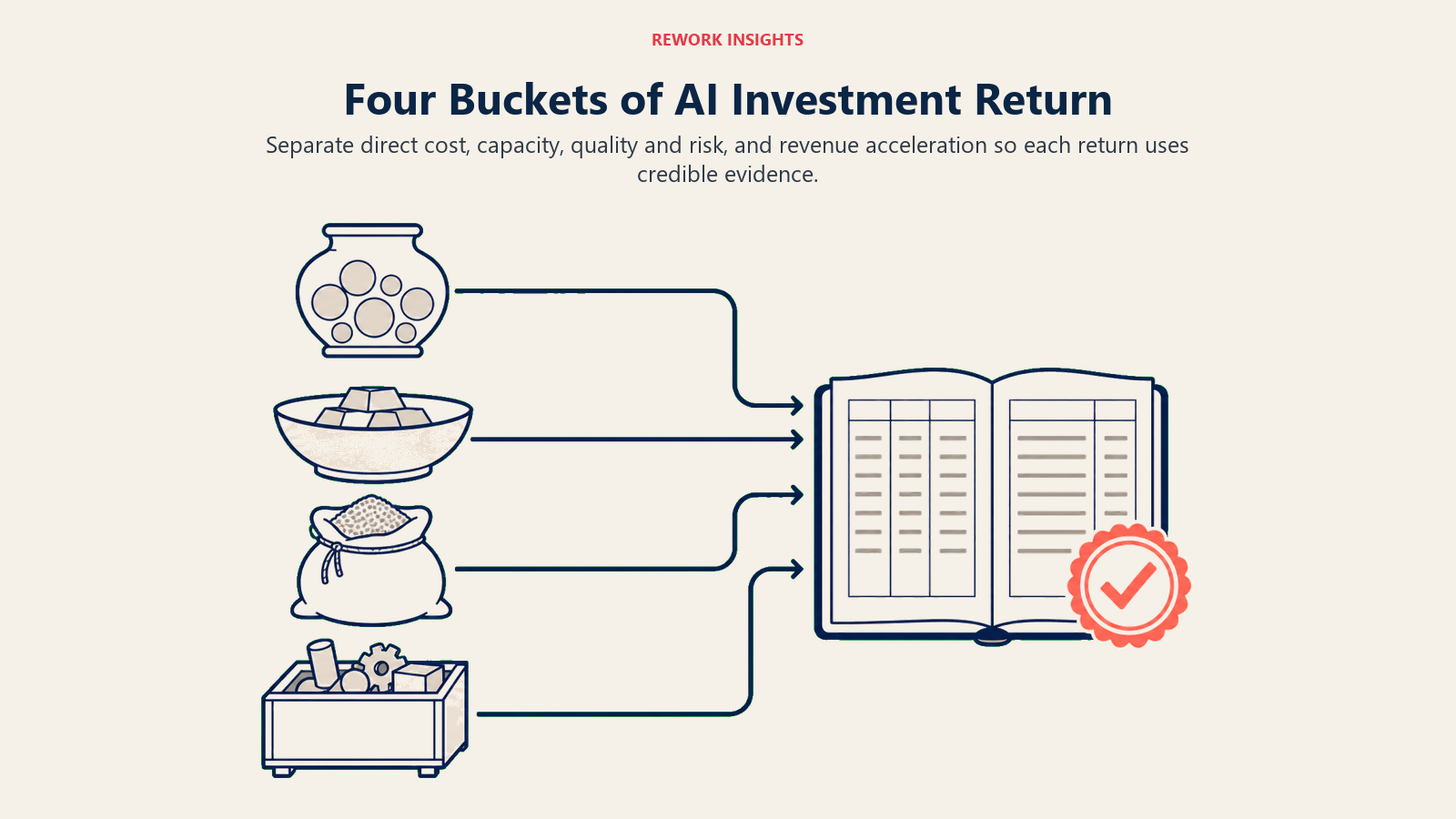

The measurement model that works for AI separates returns into four buckets and measures each differently.

Bucket 1: Direct cost reduction. The easiest category. Tools, subscriptions, or contract work that AI replaces directly. If an AI system eliminates the need for a third-party data enrichment service, that's a direct cost reduction with a clear dollar value. Start here because it's credible and auditable.

Bucket 2: Capacity expansion (avoided cost). Calculate what it would have cost to handle the same volume or complexity increase without AI. This requires two inputs: a forecast of how volume or complexity would have grown, and a unit economics model for how your team handles that growth (hours per unit, cost per hour, typical headcount threshold). The return is the delta between the AI spend and the hypothetical additional headcount or contractor cost.

For a 200-person company running AI-assisted customer support: if the team handled 40% more tickets per quarter without adding headcount, and the fully-loaded cost of a support associate is $75,000 annually, the capacity expansion return is 40% of that cost on an annualized basis, adjusted for whether that capacity was actually needed. If ticket volume genuinely grew and was handled, the return is real. If it was slack capacity, it isn't.

Bucket 3: Quality and risk reduction. Harder to quantify but defensible if you measure the right things. Common quality metrics: error rate, rework rate, customer complaint rate, contract clause miss rate, regulatory finding rate. Assign a cost to each error type based on actual historical remediation costs (not hypotheticals). Even a rough estimate of error-cost reduction is more credible than "improved quality" as an unquantified claim.

Risk reduction is similar. If AI-assisted invoice processing catches fraud at a higher rate, the return is the dollar value of fraud prevented, which can be estimated from historical loss rates and applied to the volume AI now processes.

Bucket 4: Revenue acceleration. The highest-value but hardest-to-isolate bucket. If AI cuts proposal turnaround from 5 days to 1 day, and faster proposals correlate with higher win rates in your business, the return is real. Measuring it requires a controlled comparison (AI-assisted proposals vs. standard) or a pre/post analysis with honest controls for seasonality and deal mix. Most companies can run this analysis. Most don't because it requires the discipline to track the right variables from the start.

Setting Up Measurement Before You Spend

The most common mistake is retroactively trying to measure returns on an AI investment that was approved without defining success metrics. By the time someone asks what the ROI was, the baseline is gone, the comparison group doesn't exist, and the best answer is "people said it was helpful."

Measurement infrastructure needs to be designed before the deployment, not built to justify it afterward.

For each AI investment, define: what baseline are you measuring from, what metrics will shift if the AI is working, how frequently will you sample those metrics during the pilot and after deployment, and who owns the measurement. This sounds obvious. But in practice, AI pilots routinely get deployed with no measurement plan because the pressure is on implementation, not accounting.

The running AI pilot programs guide covers pilot design, and the measurement section is worth reading before finalizing an investment request. The financial model is only as good as the data you're set up to collect, and in revenue functions that means aligning the RevOps data before the AI ever runs.

What Board Presentations Should Actually Say

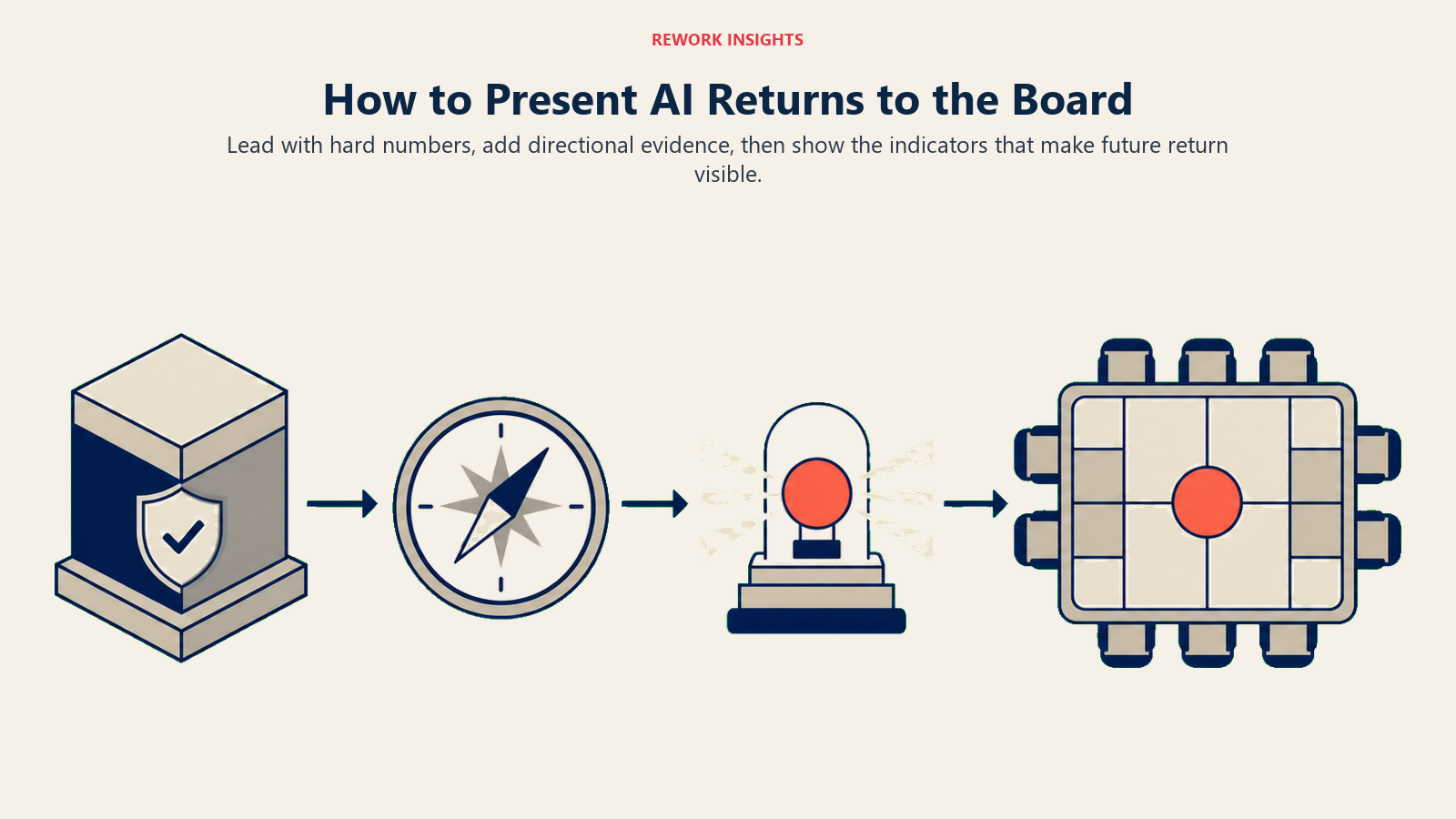

CFOs presenting AI returns to boards run into a specific problem: boards want numbers, but AI returns are often diffuse, distributed across functions, and slow to crystallize. Presenting uncertain numbers with false precision is worse than presenting honest uncertainty with a clear methodology.

The right structure for a board AI investment update has three elements.

First, the hard numbers you can stand behind. Direct cost reductions, measurable capacity expansion based on headcount plans that were real, error rate changes with dollar-cost estimates. These are the credible numbers. Lead with them.

Second, the directional metrics that support the investment thesis. Cycle time changes, adoption rates, employee productivity surveys, quality indicators that are moving in the right direction even if the dollar conversion is uncertain. These contextualize the story.

Third, the leading indicators for future return visibility. If you're six months into an AI deployment, what signals would indicate the investment is on track to generate the returns you projected? This keeps the board looking forward instead of questioning whether last quarter's spend was justified.

The CFO analysis on delayed AI upskilling is relevant here because the cost of moving slowly is a real financial variable that belongs in board-level conversations. Boards that understand the competitive cost of delay are less likely to demand perfect ROI certainty before approving AI investments.

The Benchmark Problem

Every CFO eventually wants to know how their AI returns compare to industry benchmarks. The honest answer is that reliable AI ROI benchmarks for mid-market companies are mostly vendor marketing, not independent data.

McKinsey and Gartner publish aggregate numbers across enterprise deployments, but those averages are driven by large-enterprise results that don't translate cleanly to 100-500 person companies with different tooling, different talent density, and different implementation resources. Using these numbers in a board presentation creates credibility risk if someone asks where they came from.

Build your own benchmarks from your own pilot data. Run a tight 8-week pilot, measure it properly, and use your own results as the basis for the scale investment decision. A real number from your own business is worth ten published case studies from a vendor with an obvious interest in the outcome.

One useful exception: peer benchmarking within your industry vertical. If you have relationships with finance counterparts at similar-stage companies in your sector, their AI investment experience is far more transferable than generic enterprise data. The AI tools stack for mid-market companies covers the tooling layer, and the finance measurement conversation that should accompany those decisions is exactly the framework described here.

Aligning Finance and Operations on Definitions

The last obstacle most CFOs hit is definitional disagreement between finance and the teams running AI programs. Operations defines "productivity improvement" in terms of throughput. Finance needs it in terms of dollars. Marketing defines "faster content creation" as competitive advantage. Finance needs it as cost or revenue impact. Without a shared translation layer, every AI program report will generate argument instead of alignment.

This is a governance design problem, not a technology problem. Establish before deployment: what business metrics will be the official measures of AI return, how they'll be collected, and who signs off on the data. Put finance in that sign-off chain. When finance owns part of the measurement process, the results are more credible to everyone, including finance.

The executive decision framework for AI workforce strategy provides the broader context for where AI investment decisions fit in the overall workforce and technology roadmap. But the returns measurement framework described here is what makes the financial side of those decisions defensible.

Learn More

- The Hidden Cost of Delaying AI Upskilling: A CFO-Ready Analysis

- How to Get Finance to Approve Your AI PoC

- Running AI Pilot Programs

- Measuring AI Adoption ROI

- The Executive Decision Framework for AI Workforce Strategy

- AI Tools Stack for Mid-Market Companies

- How to Talk to Your Board About AI Workforce Investment