More in

B2B SaaS Industry News

Salesforce Just Solved CRM's Oldest Data Problem, At a Cost

Apr 7, 2026

When Your SaaS Vendor Cuts Its R&D Team: What Enterprise Buyers Need to Watch

Mar 19, 2026

The 171% Agentic AI ROI Number: What the Data Actually Says

Mar 2, 2026

Drift Is Being Phased Out: The RevOps Checklist Before Your Conversational Workflows Go Dark

Feb 11, 2026

The $99-Per-Seat Decision: How to Evaluate Microsoft's New AI Bundle

Feb 9, 2026

The SaaS Growth Model That No Longer Requires More Engineers

Feb 4, 2026

Meeting Notes Just Hit a $1.5B Valuation: What That Signals About the Enterprise AI Context Race

Feb 3, 2026

A $1.2B CRM-Killer at $8M ARR: What Every Sales Leader Needs to Decide Before the Next Board Meeting

Feb 2, 2026

Record AI Funding in Q1 2026: What It Means for Your Sales Stack and Your Competitors

Jan 8, 2026 · Currently reading

The Agentic Sales Stack Is Attracting Unicorn Capital: What CEOs Need to Decide About Their Revenue Infrastructure

Jan 7, 2026

Record AI Funding in Q1 2026: What It Means for Your Sales Stack and Your Competitors

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

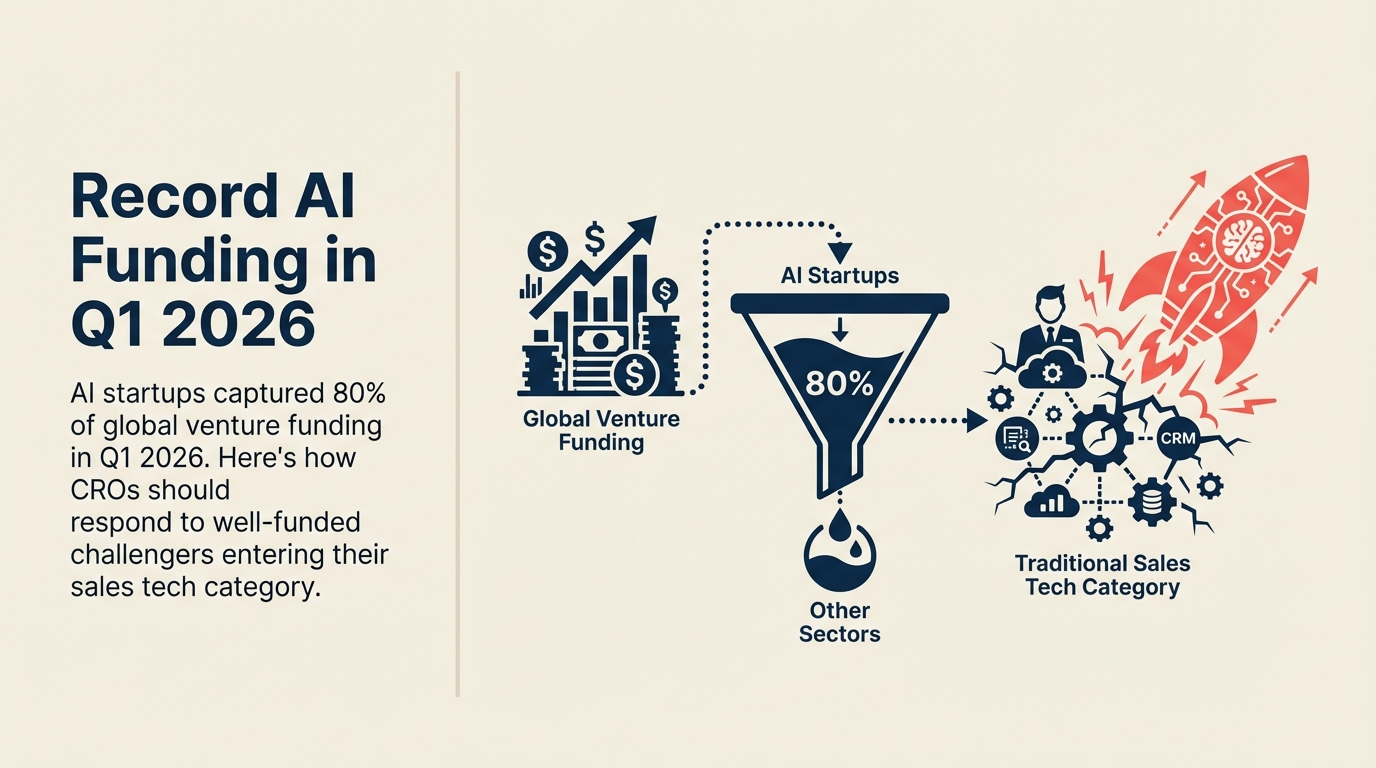

AI startups captured roughly $242 billion in Q1 2026, about 80% of all global venture funding and a record quarter. For B2B SaaS sales leaders, the news cuts two ways: your current sales tech vendors face better-funded, AI-native challengers, and so does your own company. The practical response is to audit stack durability and pilot one AI-native challenger per quarter.

The numbers from Q1 2026 are striking enough that they warrant a direct read, not a summary. If you haven't audited your current sales tech stack from a CRM perspective recently, this is a good moment to do it alongside the funding context below. Crunchbase News reported that the quarter set an all-time record for global venture investment. US-based companies alone raised $250 billion, representing 83% of global venture capital in just three months. AI startups captured approximately $242 billion of that total, or roughly 80% of all global venture funding.

To put that in context: Q1 2026's total investment was close to 70% of all venture capital deployed in all of 2025.

For CROs, this number has two practical implications that don't usually get paired in the same analysis. The first is about your current sales tech stack. The second is about the competitive landscape your company operates in. Both are moving faster than most revenue organizations have updated their planning assumptions.

Your Sales Stack Vendors Are Under Pressure

The companies that built your current CRM, sales engagement platform, forecasting tool, and conversation intelligence software were mostly funded and built in a pre-AI-native era. They're retrofitting AI capabilities onto existing architectures. The startups that raised in Q1 2026 are not.

Median Series A round sizes have risen from around $12M in prior years to approximately $18M in the current environment. That's not a statistical blip. It reflects investors funding companies that need more capital to compete at AI-native scale from the start. Vertical AI SaaS companies focused on sales, legal, and finance are raising at the upper end of that range or above.

What this creates is a specific threat pattern: a company that raised a $22M Series A in January 2026 targeting, say, AI-native sales forecasting will have 18 to 24 months of runway to build a product that doesn't need to be backward-compatible with legacy CRM architectures. They can move faster on AI integration than your existing vendor, who is simultaneously trying to maintain a multi-million-seat existing product and bolt on AI capabilities.

This doesn't mean your current stack becomes worthless immediately. But it does mean that the category your vendor occupies is being challenged by competitors with substantially more capital and fewer architectural constraints. The competitive moat that felt durable 18 months ago is narrower now.

The Intercom Signal

One concrete example of how AI-native pricing is changing the category: Intercom's AI support agent called Fin has approached $100M in annual recurring revenue, growing at approximately 3.5x, and operates as a distinct revenue stream alongside Intercom's primary ~$400M ARR platform.

According to analysis in The GTM Newsletter, Fin's pricing model is outcome-based: approximately $0.99 per resolved ticket, with a $1 million guarantee on results. That pricing structure is a fundamental shift from the seat-based SaaS model most sales and customer success tools use today. You pay for outcomes, not for licenses.

That model is arriving in sales tools next. Several of the well-funded AI startups from Q1 2026 are building toward outcome-based pricing: pay per qualified meeting booked, pay per pipeline created, pay per deal influenced. If that model gains traction in your categories, it will change the ROI conversation for every existing vendor in your stack and make it significantly harder to justify seat-based licenses that can't demonstrate direct outcome contribution. The Apollo agentic platform shift is one concrete example of how this repricing is arriving in the prospecting category specifically.

The Competitive Landscape Threat

But the funding surge doesn't only affect the companies that sell to you. It affects the companies you compete against.

If you're a CRO at a B2B SaaS company, some meaningful fraction of the $242 billion raised in Q1 2026 went into companies building in your market. And those companies are building with AI-native architectures, outcome-based pricing models, and capital reserves that allow them to undercut on price while out-maneuvering on product velocity.

The SaaS sector saw annual revenue growth of approximately 12% in 2024, with enterprise-sized firms growing at just 10%. That growth rate was already compressing before the Q1 2026 funding surge. Now you have a new cohort of well-capitalized competitors who didn't have to grow through the slower market of 2024 and 2025. They started with fresh capital in an AI-native moment.

This matters most in categories where the switching cost for your customers is moderate rather than high. If your product has deep integrations and high data lock-in, the competitive threat timeline is longer. If your product competes primarily on features and user experience, the timeline is much shorter.

A Framework for Assessing Your Stack Durability

Here's a way to evaluate whether your current sales tech investments are well-positioned or exposed:

1. Check the AI integration depth of each vendor. Surface-level AI features (a summarization button, a sentiment indicator) are table stakes now. What you want to know is whether your vendor's AI capabilities are core to the product architecture or bolted on. Ask your vendor: what percentage of their Q3 and Q4 product roadmap is net-new AI capability vs. AI packaging of existing features?

2. Assess the vendor's funding position. A legacy vendor that raised a $50M Series C in 2019 and hasn't raised since is in a different competitive position than one that raised in 2024 or 2025 with AI-native product scope. Check Crunchbase for your major vendors. Underfunded incumbents facing AI-native challengers tend to underinvest in product and over-rely on relationship sales to retain accounts.

3. Map your stack categories by disruption risk. Some sales tech categories are more at risk from AI-native challengers than others. Sales engagement platforms (sequences, email automation) are high-risk because the core value proposition, personalized outreach at scale, is exactly what AI does better than humans. Forecasting and CRM are medium-risk because data depth creates some moat. Map your vendors against this spectrum. The sales process playbook is useful here for identifying which parts of your team's workflow are most dependent on which tool categories.

4. Test one AI-native challenger per quarter. You don't need to replace your stack. But running a structured pilot against one AI-native challenger per quarter in your highest-risk category gives you both market intelligence and negotiating leverage with your current vendor. Most pilots can be scoped to 30 days with a small segment of your team.

5. Build an outcome-based ROI case for each vendor. Before outcome-based pricing arrives as a vendor offer, calculate it yourself. For each major vendor, estimate the revenue or pipeline impact attributable to the tool. If you can't make that case, your vendor can't either, and the next generation of challengers will promise to.

What to Do This Week

- Pull your current sales tech stack (every vendor, every seat count, every annual contract value) into a single view. This is the baseline for any stack assessment.

- Check the funding history of your top three spend vendors on Crunchbase. Know when they last raised, at what stage, and what the implied capital runway is.

- Identify one sales tech category where you've seen new AI-native vendor names appearing in your prospect or customer conversations. That's your first pilot candidate.

- Talk to your top AEs and SDRs about which current tools they actually use daily and which they work around. The tools your team works around are your highest replacement risk, and your best pilots will start there.

- Brief your VP of Sales Ops on the Intercom outcome-based pricing model. Whether or not Intercom is in your stack, the pricing model it's pioneering is coming to your stack. Your ops team should start modeling what outcome-based pricing would mean for your category.

Q1 2026's funding numbers aren't abstract market news. They're a countdown timer on how long your current sales tech assumptions stay valid. The CROs who treat it as a planning input rather than background noise will have a meaningful head start on the ones who don't. For the organizational shift this creates in how sales leadership operates, the sales leadership insights collection covers the strategic framing.

Frequently Asked Questions

How much did AI startups raise in Q1 2026?

AI startups captured roughly $242 billion in Q1 2026, about 80% of all global venture funding. US-based companies alone raised $250 billion, or 83% of global venture capital, in a single quarter. Total Q1 investment came close to 70% of all venture capital deployed in the whole of 2025.

Why does record AI funding matter for B2B SaaS sales leaders?

It affects both sides of the market. Your current sales tech vendors now face AI-native challengers with more capital and fewer architectural constraints, and your own company faces new well-funded competitors built for an AI-native moment. Both pressures move faster than most revenue planning assumptions account for.

What is outcome-based pricing in sales tools?

Outcome-based pricing charges for results rather than seats, for example per resolved ticket, per qualified meeting booked, or per pipeline created. Intercom's Fin agent prices near $0.99 per resolved ticket. As this model spreads to sales tools, it reshapes the ROI case for every seat-based vendor that can't tie its cost to a measurable outcome.

How should a CRO assess whether their sales stack is exposed?

Check each vendor's AI integration depth and funding position, then map categories by disruption risk. Sales engagement platforms are high-risk because AI does personalized outreach at scale well; forecasting and CRM are medium-risk because data depth creates some moat. Pilot one AI-native challenger per quarter in your highest-risk category for intelligence and leverage.

Learn More

- A $1.2B CRM-Killer at $8M ARR: What Every Sales Leader Needs to Decide: The agentic CRM story that's attracting the most attention in this funding cycle

- HubSpot Just Rewrote the AI Pricing Rulebook: How outcome-based pricing is the commercial model that AI-funded challengers are pushing toward

- Forecasting Discipline for CROs: Ensuring your forecast model reflects stack changes rather than lagging behind them

- Sales Org Design as a Growth Lever: How the funding wave in AI sales tech changes the org design calculus

Co-Founder, Rework.com

On this page

- Your Sales Stack Vendors Are Under Pressure

- The Intercom Signal

- The Competitive Landscape Threat

- A Framework for Assessing Your Stack Durability

- What to Do This Week

- Frequently Asked Questions

- How much did AI startups raise in Q1 2026?

- Why does record AI funding matter for B2B SaaS sales leaders?

- What is outcome-based pricing in sales tools?

- How should a CRO assess whether their sales stack is exposed?