El Mapa del Panorama de Proveedores de Patrones de AI

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Hay cientos de proveedores de AI. Los procesos de adquisición se extienden por meses no porque los compradores sean lentos, sino porque la mayoría de los operadores no tienen un framework para categorizar lo que están evaluando. Cada proveedor afirma ser "impulsado por AI" y "listo para empresas." Cada Demo parece capaz. Cada página de precios oscurece lo que realmente está comprando.

El pensamiento por patrones elimina el marketing del proveedor de inmediato. En lugar de preguntar "¿qué funcionalidades tiene este proveedor?", pregunte: "¿Qué patrón sirve este proveedor?" La respuesta le dice qué problema empresarial está resolviendo el producto, qué tan madura es la categoría del producto, quién debe ser propietario de la decisión de adquisición internamente y cómo evaluar si la versión del patrón del proveedor se ajusta a su caso de uso.

Este es un mapa de orientación, no una guía de compra. Le indica qué categorías de productos existen para cada patrón y qué tan madura es cada categoría. No le dice a qué proveedor comprar. Esa decisión requiere su modelo de datos específico, sus requisitos de integración y su revisión de seguridad. Para clasificaciones independientes de proveedores dentro de categorías de patrones específicas, el Gartner Magic Quadrant for Conversational AI Platforms y el Forrester Wave for AI Decisioning Platforms, Q2 2025 son las dos evaluaciones de analistas más referenciadas en la adquisición de AI empresarial.

Cómo usar este mapa

Para cada patrón, encontrará: el nombre de la categoría del producto (cómo los proveedores se denominan a sí mismos en este mercado), la calificación de madurez (alta/moderada/emergente), el perfil típico del comprador interno y una descripción de cómo está estructurado el panorama de proveedores.

Los nombres de proveedores aparecen solo como ejemplos de categoría. No son clasificaciones ni endorsements.

Key Facts: Escala del Mercado de Proveedores de AI

- El mercado de AI empresarial alcanzó los 114.870 millones de dólares en 2026 y se proyecta que crecerá a una CAGR del 18,9% hasta 2031, alcanzando los 273.000 millones de dólares. (Mordor Intelligence, 2026)

- El mercado de asistentes de reuniones de AI por sí solo fue valorado en 3.000 millones de dólares en 2025 y se proyecta que alcanzará los 6.280 millones de dólares para 2035, impulsado por más del 45% de las empresas que buscan análisis de sentimiento y seguimiento de decisiones desde los datos de reuniones.

- Gartner predice que el AI conversacional automatizará aproximadamente el 70% de las interacciones de soporte al cliente en empresas para finales de 2027, frente al 50% en 2025, lo que convierte a los patrones orientados al soporte en las categorías de proveedores de más rápida maduración.

RAG Assistant: AI de base de conocimiento y búsqueda empresarial

Categoría del producto: Búsqueda de AI empresarial, asistente de conocimiento interno, copiloto de empresa, plataforma RAG

Madurez: Alta

Comprador típico: TI, RRHH, Operaciones de Soporte, oficina del CIO

La categoría de RAG Assistant es una de las más concurridas en el AI empresarial. Abarca tres segmentos de mercado distintos.

Plataformas de ecosistemas principales: Las grandes empresas de tecnología han incorporado capacidades tipo RAG en sus suites de productividad. Microsoft Copilot en Office 365 y SharePoint, Google Workspace AI y productos integrados similares sirven a equipos que ya están dentro de esos ecosistemas. El esfuerzo de integración es bajo; la dependencia del proveedor es alta.

Búsqueda empresarial dedicada con AI: Productos como Glean construyen la recuperación de conocimiento como un producto independiente que indexa en múltiples sistemas (CRM, correo electrónico, Slack, Google Drive, Confluence) y genera respuestas. La propuesta de valor es la recuperación entre sistemas, no solo dentro de una plataforma.

Soluciones puntuales para contextos específicos: La función Q&A de Notion, Confluence AI, la base de conocimiento de AI de Zendesk y productos similares sirven RAG dentro del alcance de una herramienta específica. Estos tienen menor complejidad pero cobertura más estrecha.

Al evaluar, pregunte: ¿qué sistemas indexa el producto y puede conectarse a todos los lugares donde realmente vive su conocimiento organizacional?

Scoring + Routing: CRM predictivo y triaje inteligente

Categoría del producto: Puntuación de leads de AI, análisis predictivo de ventas, inteligencia de ingresos, AI de enrutamiento de tickets

Madurez: Alta para la puntuación de leads de ventas; moderada para el enrutamiento de soporte, selección de RRHH y otras aplicaciones

Comprador típico: RevOps, Sales Operations, Operaciones de Soporte

La puntuación de leads de ventas tiene una categoría de proveedor madura integrada en las principales plataformas de CRM. La puntuación predictiva de leads de HubSpot, Salesforce Einstein y las herramientas dedicadas de análisis de RevOps (MadKudu, 6sense en contextos ABM) sirven el patrón de Scoring and Routing. El mercado es lo suficientemente maduro como para que las configuraciones predeterminadas produzcan resultados útiles para los movimientos de ventas B2B estándar.

El AI de enrutamiento de tickets de soporte está integrado en la mayoría de las principales plataformas de helpdesk (Zendesk, Freshdesk, Intercom) como una funcionalidad nativa. La lógica de enrutamiento suele ser más simple que la puntuación de ventas, pero la categoría es igualmente madura.

El AI de puntuación de reclutamiento (selección de currículums, clasificación de candidatos) es un sub-mercado distinto con proveedores dedicados. Este sub-mercado enfrenta un escrutinio regulatorio adicional en torno al sesgo algorítmico en las decisiones de empleo, lo que afecta tanto los requisitos de cumplimiento del proveedor como la gobernanza interna.

Al evaluar, pregunte: ¿el modelo de puntuación predeterminado del proveedor refleja su industria y movimiento de negocio, o requerirá un reentrenamiento significativo antes de ser útil en su contexto?

Vision Extract: Procesamiento inteligente de documentos

Categoría del producto: Procesamiento inteligente de documentos (IDP), automatización de cuentas por pagar, plataformas OCR+AI, verificación de documentos KYC

Madurez: Alta para tipos de documentos estándar (facturas, recibos, identificaciones); moderada para formatos especializados

Comprador típico: Finanzas, equipos de cuentas por pagar/cobrar, Operaciones, Cumplimiento

Esta categoría se divide claramente por tipo de documento. Los documentos financieros estándar (facturas, órdenes de compra, recibos) tienen un mercado de proveedores maduro con altas tasas de precisión. Los proveedores incluyen Klippa, Mindee, Kofax y ABBYY, junto con las plataformas de automatización de cuentas por pagar (Tipalti, Bill.com) que integran la extracción como parte de un flujo de trabajo más amplio.

La verificación de documentos de identidad (pasaportes, licencias de conducir, identificaciones nacionales) es un sub-mercado distinto utilizado principalmente por fintechs, bancos y empresas con requisitos KYC. Los proveedores aquí (Veriff, Jumio, Onfido) son especializados y operan bajo marcos regulatorios significativos.

Los tipos de documentos especializados específicos de su industria (formularios de inspección de manufactura, formularios de admisión de atención médica, contratos propietarios) típicamente requieren datos de entrenamiento personalizados sobre un modelo base del proveedor. Ningún proveedor tiene un modelo listo para producción para su formato de documento específico a menos que su formato sea un estándar de la industria.

Al evaluar, pregunte: ¿el modelo del proveedor ha sido entrenado en documentos que se parecen a los suyos y puede demostrar precisión en sus tipos de documentos específicos antes de que firme?

Meeting Intelligence: Inteligencia de conversación

Categoría del producto: Inteligencia de conversación, inteligencia de ingresos, grabación de llamadas + AI, AI de entrenamiento de ventas

Madurez: Muy alta

Comprador típico: Liderazgo de ventas, RevOps, liderazgo de Customer Success

Esta es una de las categorías de patrones más maduras en el AI empresarial. Gong, Clari Copilot, Chorus (ahora ZoomInfo), Fireflies y Otter for Business sirven el patrón de Meeting Intelligence con despliegues en producción a escala. El Pipeline central (grabación, transcripción, extracción de temas, envío al CRM) es un commodity. La diferenciación está en los análisis de entrenamiento, la detección de riesgo de negocio y la profundidad de la integración con el CRM.

La categoría también está bajo presión de las propias plataformas de colaboración. Zoom, Microsoft Teams y Google Meet ofrecen resúmenes nativos de reuniones con AI con integración directa de calendario y CRM. Para equipos que quieren transcripción y resumen básicos, las opciones nativas de la plataforma son cada vez más competitivas con las herramientas dedicadas de inteligencia de conversación.

La decisión entre proveedores dedicados y capacidades nativas de la plataforma suele depender de la profundidad del entrenamiento y los análisis entre reuniones. Las herramientas nativas de la plataforma resumen reuniones individuales. Las herramientas dedicadas de inteligencia de conversación analizan patrones a través de cientos de llamadas, rastrean métricas de entrenamiento a lo largo del tiempo y se integran profundamente con el contexto del negocio en el CRM.

Al evaluar, pregunte: ¿necesita resúmenes reunión por reunión, o necesita análisis de patrones en toda su biblioteca de llamadas?

Anomaly Agent: Múltiples sub-mercados con diferentes niveles de madurez

Categoría del producto: Detección de fraude, monitoreo AIOps, detección de amenazas de seguridad, detección de anomalías de gastos

Madurez: Alta para fraude e infraestructura; moderada para anomalías de procesos empresariales

Comprador típico: Finanzas/Riesgos (fraude), Ingeniería/DevOps (infraestructura), Seguridad (amenazas), Finanzas/RRHH (anomalías de gastos y procesos)

Este patrón tiene cuatro sub-mercados distintos que rara vez se superponen en el panorama de proveedores.

Detección de fraude: Una de las aplicaciones de AI más maduras que existen. Stripe Radar, Sift, Forter y la puntuación de fraude integrada en los procesadores de pago han estado en producción a escala durante años. Estos proveedores tienen ventajas de datos (entrenados en patrones de transacciones de toda la industria) que las construcciones internas no pueden igualar.

Monitoreo de infraestructura y aplicaciones (AIOps): Datadog, New Relic, Dynatrace y Splunk proporcionan detección de anomalías en métricas, logs y trazas. La categoría es madura y está integrada en las cadenas de herramientas de DevOps.

Detección de amenazas de seguridad: Las plataformas SIEM (CrowdStrike, Sentinel, Splunk SIEM) tienen la detección de anomalías como una funcionalidad central. Este sub-mercado es especializado y generalmente es propiedad de Seguridad en lugar de las operaciones de TI.

Detección de anomalías de procesos empresariales: Detectar patrones de gastos inusuales, desviaciones de políticas de RRHH, anomalías de la cadena de suministro o desviaciones de procesos operativos es el sub-mercado menos maduro. Algunas plataformas de gestión de gastos (Ramp, Brex) están incorporando esto. Pero para las anomalías de procesos empresariales no financieros, a menudo está en territorio de construcción o trabajando con herramientas de monitoreo de propósito general adaptadas a su caso de uso.

Al evaluar, pregunte: ¿a cuál sub-mercado sirve realmente este proveedor y sus datos de entrenamiento y modelo de referencia reflejan su proceso específico?

Generative Research: Asistente de investigación de AI

Categoría del producto: Asistente de investigación de AI, AI de inteligencia competitiva, automatización de investigación de cuentas

Madurez: Emergente. Variación significativa en el manejo de fuentes y la calidad de la salida.

Comprador típico: Equipos de estrategia, ventas (investigación de cuentas), marketing (inteligencia competitiva), funciones de analistas

La categoría de investigación generativa es joven y fragmentada. Las herramientas de AI de propósito general (Perplexity, You.com Pro, ChatGPT con Browse) sirven este patrón para la investigación de fuentes públicas. Las herramientas dedicadas de inteligencia competitiva están proliferando pero aún están madurando.

La diferenciación clave a evaluar en esta categoría es el acceso a las fuentes. Diferentes proveedores tienen acceso a diferentes tipos de fuentes: web pública, archivos de noticias, bases de datos financieras, datos de industria propietarios y repositorios de documentos internos. La calidad de la investigación es una función de qué fuentes puede acceder realmente el producto, no solo de lo que produce la capa de generación.

Una segunda diferenciación es la fidelidad de las citas. Algunas herramientas producen investigaciones bien citadas con fuentes rastreables. Otras alucinan citas o parafrasean tan agresivamente que la fuente original no es recuperable. Esto importa significativamente para cualquier investigación que se usará externamente o se distribuirá a los tomadores de decisiones.

Al evaluar, pregunte: ¿cuáles son las fuentes reales de las que extrae este producto y puede demostrar la precisión de las citas en una tarea de investigación de su dominio?

Document Review: AI de contratos y más

Categoría del producto: AI de contratos, AI legal, revisión de documentos de cumplimiento, CLM (gestión del ciclo de vida de contratos) con AI

Madurez: Alta para la revisión de contratos; emergente para dominios especializados

Comprador típico: Legal, Compras, Cumplimiento

El AI de revisión de contratos es una categoría madura. Spellbook, Harvey, Ironclad AI y LexCheck están creados específicamente para el análisis de documentos legales. Las plataformas CLM más grandes (Ironclad, Conga, Icertis) han integrado la revisión de AI como parte de herramientas de flujo de trabajo de contratos más amplias. La categoría tiene despliegues en producción comprobados en empresas grandes y del mercado medio.

La categoría se adelgaza a medida que se aleja de los contratos legales estándar. La revisión de declaraciones de impuestos, la comparación de pólizas de seguros, la revisión de cumplimiento regulatorio en contextos no legales y la revisión de documentos técnicos están servidas por una mezcla de herramientas especializadas y soluciones personalizadas. Pocos proveedores han productizado estas aplicaciones con la misma madurez que la revisión de contratos legales.

Al evaluar, pregunte: ¿ha procesado este proveedor documentos en su dominio específico y puede mostrar benchmarks de precisión en tipos de documentos similares a los suyos?

Workflow Copilot: Altamente fragmentado por contexto

Categoría del producto: Copiloto de AI, asistente de AI específico del rol, AI de productividad horizontal, copiloto de dominio

Madurez: Alta para el trabajo horizontal (escritura, codificación); moderada para el específico del dominio

Comprador típico: Varía según el contexto: TI/Ingeniería para copilotos de codificación, Operaciones para copilotos de dominio, jefes de función específica

Esta es la categoría más fragmentada en el panorama de proveedores. El patrón es extremadamente versátil, lo que significa que se ha productizado en docenas de contextos específicos.

Copilotos horizontales: Microsoft 365 Copilot (correo electrónico, documentos, reuniones), GitHub Copilot (código) y ofertas similares a nivel de plataforma sirven el trabajo amplio del conocimiento horizontal. Estos son productos maduros y de alta adopción con grandes despliegues en producción a escala.

Copilotos específicos del dominio: Los copilotos de ventas (integrados en Salesforce, HubSpot o como add-ons dedicados), los copilotos de soporte (en Zendesk, Intercom), los copilotos de finanzas y los copilotos de marketing sirven contextos de flujo de trabajo específicos. El AI de ventas de Rework entra en esta categoría. La calidad y la profundidad de la integración varían significativamente.

Infraestructura para construir copilotos: Para los equipos que construyen su propio copiloto de dominio, las APIs de proveedores de LLM (Anthropic, OpenAI, Google), los frameworks de orquestación y los proveedores de bases de datos vectoriales proporcionan los bloques de construcción.

Al evaluar, pregunte: ¿qué tan profunda es la integración con la herramienta específica donde vive este copiloto? Un copiloto que está añadido a un CRM que no puede leer es menos útil que uno que es nativo del flujo de trabajo.

Personalization Engine: Maduro para e-commerce, creciendo para B2B

Categoría del producto: Motor de recomendaciones, plataforma de contenido dinámico, personalización de AI, CDP con activación de AI

Madurez: Alta para e-commerce; moderada para B2B SaaS y plataformas de contenido

Comprador típico: Marketing, Producto, E-commerce

Dynamic Yield, Bloomreach y Monetate sirven el mercado de personalización de e-commerce con plataformas maduras y de alta escala. La categoría tiene una profundidad significativa en recomendaciones de productos, precios dinámicos y personalización de contenido a nivel de página.

En B2B SaaS, Mutiny e Intellimize se centran en la personalización de sitios web (contenido diferente para visitantes de diferentes empresas o industrias). Segment y CDPs (Customer Data Platforms) similares proporcionan la capa de datos de comportamiento que consumen los motores de personalización. El segmento B2B es menos maduro que el e-commerce pero está creciendo.

La personalización en el producto para SaaS (adaptar la experiencia del producto basándose en el comportamiento del usuario) se construye principalmente de forma personalizada o mediante plataformas de análisis de producto que permiten indicadores de funcionalidades dirigidos y mensajería en la aplicación (Amplitude, Mixpanel con funcionalidades de experimentación).

Al evaluar, pregunte: ¿el modelo de personalización de este proveedor maneja su estructura de usuarios (usuarios individuales, usuarios a nivel de cuenta, visitantes anónimos) y el volumen de su contenido?

Autonomous Agent: En etapa temprana, alta actividad

Categoría del producto: Plataforma de AI agent, automatización de flujos de trabajo agénticos, framework de agentes

Madurez: Emergente. Alta actividad de mercado, despliegues en producción comprobados a escala limitados.

Comprador típico: Oficina del CTO, equipos de ingeniería de AI/ML, Operaciones

La categoría de Autonomous Agent es la más activa en términos de nuevos anuncios de proveedores y la menos madura en términos de despliegues empresariales comprobados. LangChain, CrewAI y AutoGen proporcionan frameworks para construir agentes. Las plataformas de agentes específicas de verticales están proliferando en contextos de desarrollo de ventas, soporte al cliente e ingeniería de software.

La brecha de madurez de la categoría es significativa: los frameworks existen, pero las herramientas de gobernanza (aprobaciones, trazas de auditoría, rutas de escalación) todavía se están desarrollando. La mayoría de los despliegues empresariales de agentes autónomos están en contextos controlados y acotados (un agente de investigación que nunca escribe en sistemas externos, un agente de código que opera solo en un entorno de pruebas) en lugar de en flujos de trabajo de producción totalmente agénticos.

Al evaluar, pregunte: ¿cómo luce la infraestructura de manejo de errores y escalación del proveedor? Un agente autónomo sin una ruta de escalación clara para los casos que no puede resolver es un riesgo de auditoría, no una herramienta de productividad.

| Patrón | Madurez de la categoría | Valor típico del contrato empresarial | Criterio de evaluación clave | ¿Existe opción nativa de plataforma? |

|---|---|---|---|---|

| RAG Assistant | Alta | $15.000-$150.000/año | ¿Qué sistemas indexa el producto? | Sí (Microsoft, Google) |

| Scoring + Routing | Alta (ventas) / Moderada (otros) | $20.000-$100.000/año | ¿El modelo predeterminado del proveedor se ajusta a su movimiento de negocio? | Sí (Salesforce, HubSpot) |

| Vision Extract | Alta (estándar) / Moderada (especializado) | $10.000-$80.000/año | ¿El proveedor ha entrenado en sus tipos de documentos? | Parcial (plataformas de automatización de cuentas por pagar) |

| Meeting Intelligence | Muy alta | $20.000-$150.000/año | ¿Nativa de plataforma vs. profundidad de análisis entre llamadas? | Sí (Zoom, Teams, Meet) |

| Anomaly Agent | Alta (fraude/infra) / Moderada (proceso empresarial) | $30.000-$500.000/año (fraude) | ¿Los datos de entrenamiento reflejan su proceso específico? | Sí (Stripe, Datadog, CrowdStrike) |

| Generative Research | Emergente | $5.000-$50.000/año | ¿A qué fuentes accede realmente el producto? | Sí (Perplexity, ChatGPT Browse) |

| Document Review | Alta (contratos) / Emergente (dominios) | $20.000-$200.000/año | ¿Benchmarks de precisión en sus tipos de documentos? | Sin plataforma nativa dedicada |

| Workflow Copilot | Alta (horizontal) / Moderada (dominio) | $10.000-$50.000/año (horizontal) | ¿Qué tan profunda es la integración de contexto con su herramienta principal? | Sí (Microsoft 365, GitHub) |

| Personalization Engine | Alta (e-commerce) / Moderada (B2B) | $30.000-$200.000/año | ¿Coincidencia de estructura de usuarios (individual vs. a nivel de cuenta)? | Parcial (Segment, CDPs) |

| Autonomous Agent | Emergente | $50.000-$500.000+ (plataforma + servicios) | ¿Infraestructura de manejo de errores y escalación? | Sin plataforma nativa madura |

"La capacidad del proveedor en las categorías de patrones de AI cambia sustancialmente en 18 meses. Los proveedores de inteligencia de conversación que dominaban en 2023 enfrentan competencia directa de los resúmenes nativos de Zoom, Teams y Google Meet en 2026. Los compradores deben evaluar según los requisitos de capacidad del patrón, no solo según el posicionamiento actual del proveedor." (Rework Vendor Landscape Analysis, 2026)

El Mapa de Proveedores de Patrones

El Mapa de Proveedores de Patrones es un framework de evaluación que clasifica a los proveedores de AI según cuál de los 10 patrones ACE sirven, en lugar de por categoría de marketing. El framework tiene cuatro dimensiones de evaluación: (1) madurez de la categoría (alta, moderada o emergente), (2) perfil típico del comprador interno (quién debe ser propietario de esta decisión), (3) la única pregunta de evaluación más importante para esa categoría de patrón, y (4) si existe una opción nativa de plataforma que reduzca la sobrecarga de integración. Usar el Mapa de Proveedores de Patrones antes de cualquier conversación con un proveedor reduce el tiempo de evaluación al eliminar a los proveedores cuyo patrón no coincide con el requisito e identificar rápidamente si una opción nativa de plataforma es viable para su contexto.

Rework Analysis: La escala de 114.000 millones de dólares del mercado de AI empresarial en 2026 ha creado una fragmentación significativa de proveedores, con cientos de proveedores que afirman capacidades "impulsadas por AI" que pueden mapearse a patrones subyacentes muy diferentes. En la experiencia de adquisición de Rework, los compradores que organizan la evaluación de proveedores por patrón en lugar de por lista de funcionalidades reducen los ciclos de evaluación de un promedio de 16 semanas a 8 semanas, porque el framework de patrones filtra inmediatamente a los proveedores que resuelven un problema diferente al que tiene el comprador.

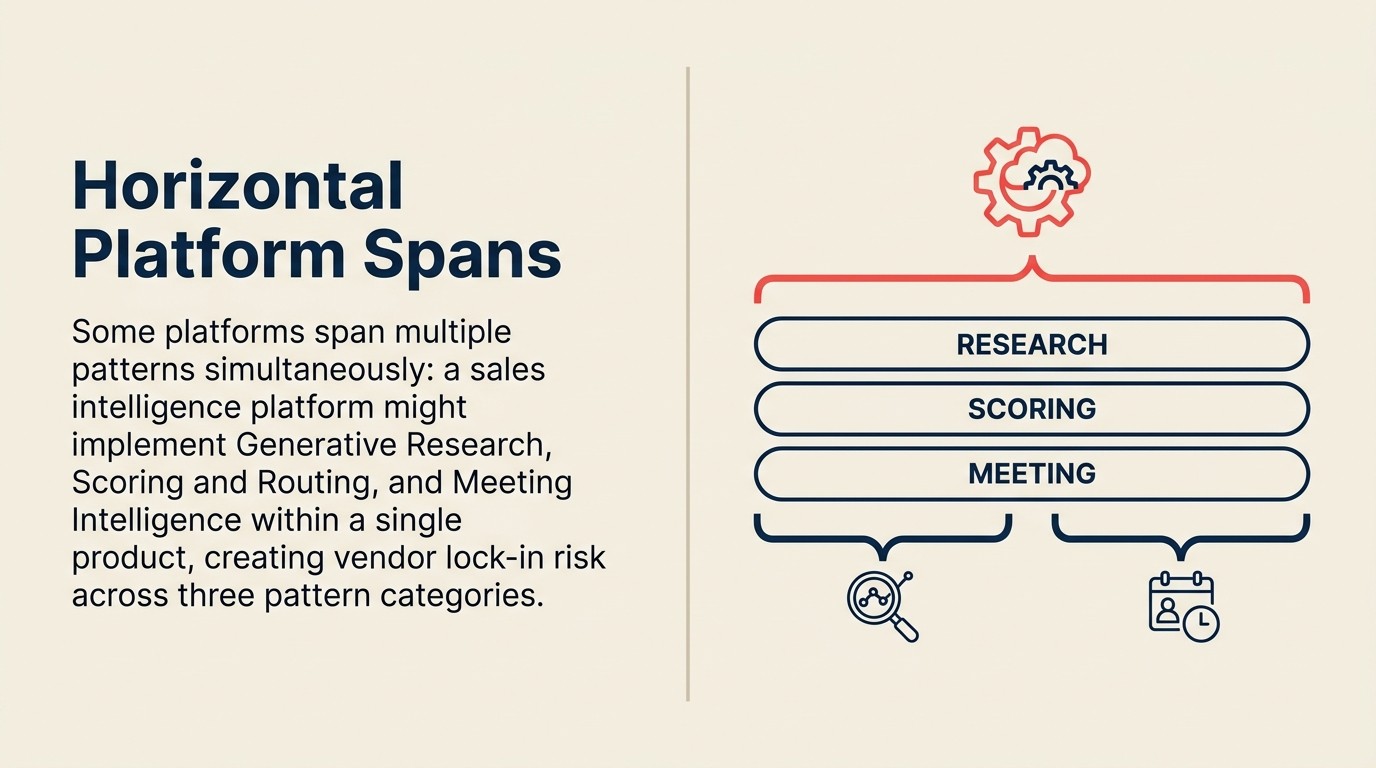

Plataformas horizontales que abarcan múltiples patrones

Algunos proveedores sirven de 3 a 4 patrones a través de un enfoque de plataforma. Salesforce sirve Scoring + Routing, Workflow Copilot, Meeting Intelligence y Generative Research dentro de su capa de AI. HubSpot sirve patrones similares dentro de su ecosistema de CRM. Microsoft 365 Copilot abarca Workflow Copilot, RAG Assistant y Meeting Intelligence.

La consolidación de plataformas tiene ventajas reales: contrato único, modelo de datos único, autenticación integrada y sin movimiento de datos entre sistemas. También tiene riesgos reales: acepta la versión del plataforma de cada patrón, que rara vez es la mejor en su clase en todas las dimensiones.

La decisión de consolidar en una plataforma versus comprar soluciones puntuales de mejor en su clase se reduce al costo de integración versus el compromiso de capacidad. Si las versiones de los patrones de su plataforma existente son el 80% de tan capaces como las mejores soluciones puntuales, la consolidación generalmente vale la pena. Si necesita una capacidad del 95% en un patrón crítico, la solución puntual de mejor en su clase vale la sobrecarga de integración.

Aplicar el panorama de proveedores

El framework de patrones hace que la evaluación de proveedores sea más rápida y más honesta. Antes de cualquier conversación con un proveedor, responda:

- ¿Qué patrón sirve este proveedor?

- ¿Es esta una categoría madura o emergente para ese patrón?

- ¿La versión del patrón del proveedor se adapta a su tipo de dato y caso de uso?

- ¿Qué personalización necesitará hacer sobre el producto base del proveedor?

Estas cuatro preguntas generan los criterios de evaluación correctos para cualquier conversación con un proveedor de AI. Vea Elegir el Patrón de AI Correcto para su Problema para la selección de patrones antes de la evaluación del proveedor. Vea Decisión de Comprar vs. Construir por Patrón de AI para cuando el panorama de proveedores no tiene lo que necesita.

Los requisitos de gobernanza que afectan qué proveedores son viables en su contexto están en Requisitos de Gobernanza por Patrón de AI. Y para cómo las elecciones de proveedores afectan su Roadmap plurianual, vea Secuenciación de Patrones de AI en un Roadmap Plurianual.

El mercado se mueve lo suficientemente rápido como para que cualquier evaluación específica de un proveedor quede obsoleta en 12 meses.

Preguntas Frecuentes

¿Qué es el Mapa de Proveedores de Patrones?

El Mapa de Proveedores de Patrones es un framework de evaluación que clasifica a los proveedores de AI según cuál de los 10 patrones ACE sirven, en lugar de por categoría de marketing. Usar la clasificación basada en patrones reduce significativamente los ciclos de evaluación de proveedores porque filtra a los proveedores que resuelven un problema diferente e identifica inmediatamente si existe una opción nativa de plataforma.

¿Qué categorías de patrones de AI tienen los ecosistemas de proveedores más maduros?

Meeting Intelligence (inteligencia de conversación) es la categoría más madura, con calificaciones de madurez muy altas y despliegues en producción a escala. RAG Assistant, Scoring and Routing para ventas y Vision Extract para documentos estándar también son categorías de alta madurez. Generative Research y Autonomous Agent son las menos maduras, con Autonomous Agent mostrando alta actividad de mercado pero despliegues empresariales comprobados limitados.

¿Cuándo supera una opción nativa de plataforma a un proveedor dedicado de mejor en su clase?

Las opciones nativas de plataforma ganan cuando su versión del patrón es el 80% o más tan capaz como la mejor solución puntual, y cuando la reducción de la sobrecarga de integración es significativa. Para los resúmenes de reuniones (Zoom, Teams, Google Meet), la opción nativa de plataforma es ahora competitiva para equipos que necesitan transcripción y resumen básicos. Para los análisis entre reuniones, las métricas de entrenamiento y la profundidad del CRM, los proveedores dedicados siguen siendo más fuertes. La compensación de consolidación: contrato único y modelo de datos versus posible compromiso de capacidad en los patrones que más importan.

¿Con qué frecuencia se deben actualizar las evaluaciones del panorama de proveedores?

Anualmente como mínimo. El mercado de proveedores de AI cambia sustancialmente en 12-18 meses. Los proveedores que no tenían competencia de plataforma nativa en 2024 enfrentan una competencia significativa de Zoom, Teams y Microsoft 365 Copilot en 2026. Los proveedores en categorías emergentes (Autonomous Agent, Generative Research) están madurando rápidamente. Comprometerse con contratos de varios años para proveedores de categorías emergentes sin derechos de reevaluación es un riesgo significativo de adquisición.

¿Cuál es la pregunta más importante que hacerle a un proveedor de AI en cualquier categoría de patrón?

La pregunta de evaluación clave específica del patrón importa más, pero la pregunta universal en todos los patrones es: "¿Ha sido desplegado su producto en producción para un caso de uso que coincida con el mío y puede conectarme con un cliente de referencia en mi industria?" Un proveedor con una Demo convincente y ninguna referencia de producción en su caso de uso le está vendiendo software de categoría emergente a precios de categoría madura.

¿Cómo afecta la consolidación de proveedores en una plataforma a la calidad de los patrones de AI?

La consolidación de plataformas intercambia la capacidad de soluciones puntuales por la simplicidad de integración. Salesforce, HubSpot y Microsoft 365 sirven cada uno de 3 a 4 patrones dentro de sus ecosistemas. Sus versiones de cada patrón rara vez son las mejores en su clase en todas las dimensiones. Si necesita el 80% de la capacidad de mejor en su clase en múltiples patrones y quiere una sobrecarga de integración mínima, la consolidación de plataformas generalmente vale la pena. Si un patrón específico es crítico y la versión de la plataforma ofrece el 60% de lo que entrega un proveedor dedicado, la solución puntual de mejor en su clase vale la inversión de integración.

Gartner predice que para finales de 2027, el AI conversacional automatizará aproximadamente el 70% de las interacciones de soporte al cliente en empresas, frente al 50% en 2025. La capacidad del proveedor en las curvas de madurez anteriores cambiará sustancialmente en 18 meses. El framework de patrones no cambiará. Úselo como su lente de evaluación estable.

Co-Founder, Rework.com

On this page

- Cómo usar este mapa

- RAG Assistant: AI de base de conocimiento y búsqueda empresarial

- Scoring + Routing: CRM predictivo y triaje inteligente

- Vision Extract: Procesamiento inteligente de documentos

- Meeting Intelligence: Inteligencia de conversación

- Anomaly Agent: Múltiples sub-mercados con diferentes niveles de madurez

- Generative Research: Asistente de investigación de AI

- Document Review: AI de contratos y más

- Workflow Copilot: Altamente fragmentado por contexto

- Personalization Engine: Maduro para e-commerce, creciendo para B2B

- Autonomous Agent: En etapa temprana, alta actividad

- El Mapa de Proveedores de Patrones

- Plataformas horizontales que abarcan múltiples patrones

- Aplicar el panorama de proveedores