Nassim Taleb on Risk and Decision-Making: What Business Leaders Get Wrong About Uncertainty

Nassim Nicholas Taleb is not a CEO or a founder in the conventional sense. He spent part of his career as a trader and risk analyst before becoming a researcher and essayist. But his documented frameworks on risk, probability, and organizational resilience have had a direct influence on how sophisticated business leaders think about strategy, hiring, supply chain design, and decision-making under uncertainty.

His four-book Incerto series ("Fooled by Randomness," "The Black Swan," "The Bed of Procrustes," and "Antifragile") lays out a coherent philosophy of risk that differs sharply from standard business school treatments. His central argument: most organizations and most leaders systematically underestimate the impact of rare, high-magnitude events and overestimate the predictive power of their models.

For executives managing organizations at scale, Taleb's frameworks are among the most operationally relevant available.

The Black Swan Framework

Taleb's most-cited concept is the "black swan," a term he borrowed from history to describe events that meet three criteria: they are rare, they have extreme impact, and they appear obvious in retrospect even though they were not predicted in advance.

The Black Swan of the 2008 financial crisis met all three criteria. So did COVID-19 for global supply chains. So did the sudden emergence of large language models for many industries betting on different AI development curves.

Taleb's key insight for business leaders: standard risk management frameworks focus on events with known probability distributions. They model the risks they can see and quantify. Black Swans are not in these models -- not because they're unknowable in principle, but because the tools being used can't see them.

The practical implication isn't "predict the unpredictable." It's design organizations to survive black swans rather than optimizing for average-case performance. An organization that is optimized purely for efficiency in normal conditions -- lean inventory, just-in-time supply chains, minimal cash reserves, maximum leverage -- is highly fragile to rare, large disruptions. The companies that survived COVID supply chain shocks best were not the ones with the most efficient supply chains. They were the ones that had built in redundancy and slack that looked like waste in normal conditions.

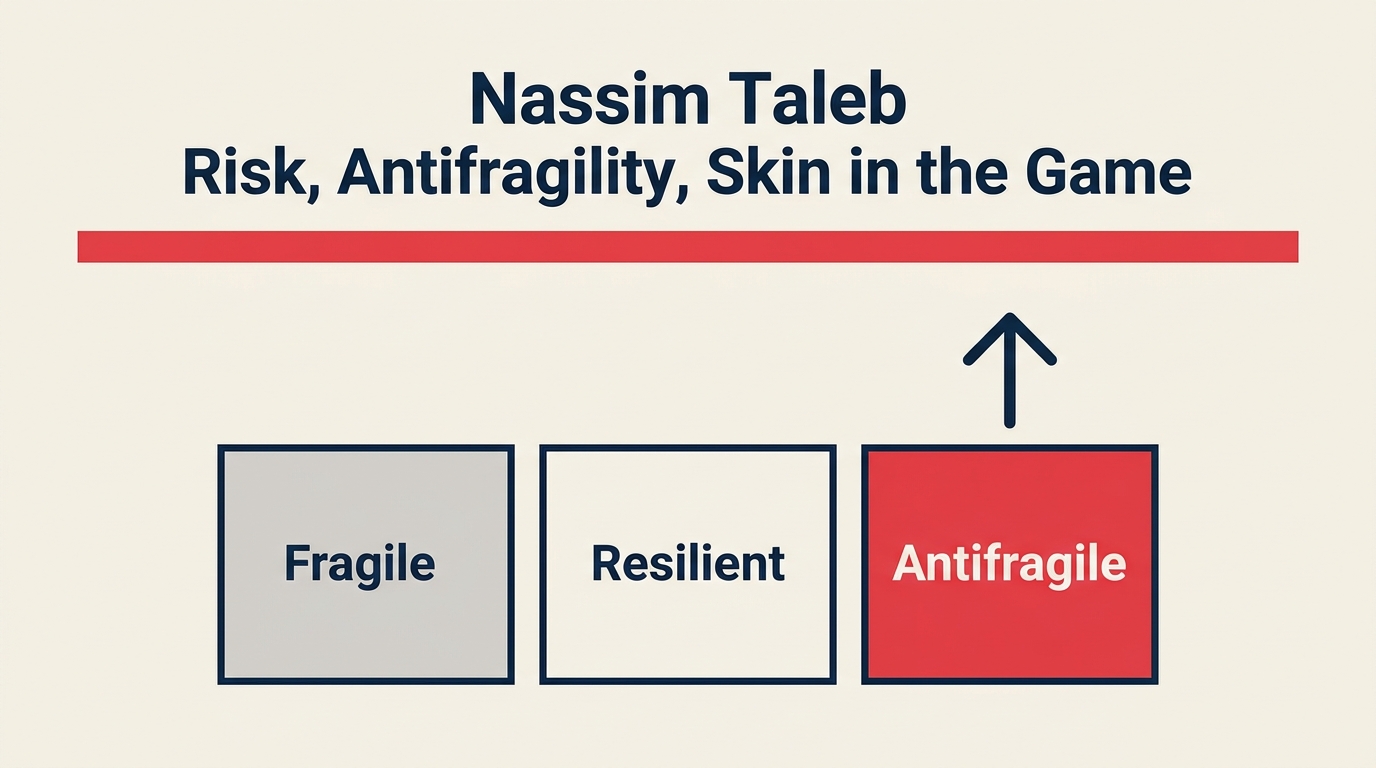

Antifragility: Beyond Resilience

Taleb introduced the term "antifragile" to describe systems that don't just survive volatility and stress but actually improve from them. The distinction:

| State | Response to stress |

|---|---|

| Fragile | Breaks when stressed (glass) |

| Resilient | Absorbs stress and returns to prior state (steel) |

| Antifragile | Improves when stressed (immune system, muscle) |

Most corporate risk management aims for resilience. Taleb argues the better target is antifragility.

What makes an organization antifragile? Taleb's documented answer: many small experiments with capped downside and uncapped upside. If each experiment can fail completely but the failure is small and the success can compound, the portfolio of experiments improves as it encounters adversity. Failed experiments produce information and updated strategies. Successful experiments expand.

This is operationally different from how most organizations manage R&D, sales experiments, or market expansion. Most organizations make large, concentrated bets with defined ROI targets and cut experiments that miss early milestones. Taleb's framework suggests a different structure: many small bets where the downside is genuinely capped (not "we'll lose $10M if this fails" but "we'll lose $500K"), and where failure explicitly generates learning that informs subsequent experiments.

Amazon's documented culture of "two-pizza teams" launching independent initiatives is the closest corporate approximation of this structure.

Skin in the Game

Taleb's third major framework, covered extensively in his 2018 book "Skin in the Game," addresses asymmetric risk in decision-making.

His core argument: when the people making decisions don't bear the consequences of those decisions, the decisions are systematically worse. This applies to corporate executives who manage with equity upside but limited personal downside, to consultants who recommend restructuring without being responsible for outcomes, and to risk models built by analysts who won't personally lose if the models fail.

The business leader implications are direct:

Compensation design. Leaders whose compensation is primarily salary bear limited consequence for bad decisions. Leaders with significant equity exposure that only vests over long periods have genuine skin in the game. Taleb's framework supports the academic research on executive compensation showing that performance-linked equity over multi-year periods produces better decision quality than short-term bonus structures.

Consultant accountability. When you hire advisors whose compensation doesn't depend on the recommendations working, you're introducing agents without skin in the game. Taleb's framework suggests structuring advisory relationships so that consultants have some share of outcomes, not just deliverables.

Operational decisions by non-operators. Strategy decisions made exclusively by executives who don't interact with customers, suppliers, or the operational work are often fragile for the same reason. The people with skin in the specific decision are the ones who should be in the decision process.

Via Negativa: What to Remove, Not What to Add

One of Taleb's less-cited but highly applicable principles is "via negativa," borrowed from religious philosophy. The idea: progress often comes from removing what's harmful or unnecessary rather than from adding what's beneficial.

In medicine, Taleb's argument is that removing unhealthy practices often produces more benefit than adding treatments. In business, the principle is that identifying and eliminating the specific things that are generating fragility -- excessive debt, single-supplier dependencies, critical processes with no redundancy, culture of hiding bad news -- is often more valuable than building new capabilities.

For leaders doing strategic planning: before asking "what should we add?" ask "what is making us fragile that we could remove?" The answer often produces higher-leverage improvements than the addition question.

Barbell Strategy for Resource Allocation

Taleb developed what he calls the "barbell strategy" as a practical risk management framework. The idea: allocate most resources to highly safe positions and a small portion to highly speculative positions. Avoid the middle ground, which appears moderate-risk but often has hidden fragility.

Applied to business:

- Put 80-90% of resources into core, high-confidence activities with stable cash generation

- Put 10-20% into genuinely experimental initiatives with capped downside but asymmetric upside

- Avoid the "middle barbell" of medium-confidence, medium-investment bets that feel prudent but don't have either the stability of core operations or the asymmetric upside of genuine experiments

This is counter to how most companies do portfolio planning, which tends toward a large middle: many medium-size bets that are "strategic but not speculative." Taleb's framework predicts that this middle-barbell portfolio performs worse in volatile environments than a proper barbell structure.

Epistemic Humility and Over-Forecasting

Taleb's most consistent intellectual target is what he calls "epistemic arrogance": overconfidence in the accuracy of predictions and models. He documents extensively how economists, risk analysts, and strategic planners systematically overestimate how much their models tell them about the future.

For business leaders: the operational implication is to invest less in forecast accuracy and more in decision robustness. The question is not "what will happen?" but "what decision holds up well across the range of plausible outcomes?" A strategy that is excellent if Q4 revenue lands at forecast but catastrophic if it misses by 20% is a fragile strategy. A strategy that is reasonably good across a wide range of outcomes is more antifragile.

This argues for scenario planning over point forecasting in strategic decision-making -- not "what will next year look like?" but "what does our strategy assume, and how fragile is it to each of those assumptions being wrong?"

What Directors Can Take From Taleb

Design for black swan survival. Efficiency and resilience trade off. Some amount of slack (inventory buffer, cash reserve, supplier redundancy, headcount buffer) looks like waste in normal conditions but is the difference between survival and crisis when conditions aren't normal.

Build the antifragile portfolio. Restructure R&D and innovation investment as many small experiments with capped downside, rather than a few large bets with unbounded downside. Use failures as information to improve subsequent experiments.

Apply the skin-in-the-game test. Before acting on external advice, ask whether the advisor bears any consequence if the recommendation is wrong. Adjust the weight you give the advice accordingly.

Replace point forecasts with robustness questions. In strategic planning, ask "what assumptions does this strategy require?" and "what happens if those assumptions are wrong by 20%?" Decisions that hold up under a wide range of assumptions are more defensible than decisions that require accurate forecasting.

Key Facts

- Taleb's Incerto series has sold millions of copies worldwide and is widely assigned in finance, strategy, and risk management courses

- "The Black Swan" (2007) was prescient about the 2008 financial crisis; it was published the year before

- His "antifragile" concept introduced a vocabulary for organizational resilience that goes beyond traditional risk management

- "Skin in the Game" (2018) directly influenced conversations about executive compensation and accountability structures in corporate governance