What is Cash Flow? Why Profitable Companies Still Go Bankrupt

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

"But we're profitable!" The founder's confusion was real. His P&L showed $500K profit, yet he couldn't make payroll. Three weeks later, the company folded.

This happens every day. Because here's the brutal truth: You can't pay bills with profits. Only cash.

Cash Flow: The Real Story

Cash flow is simply money moving in and out of your business. Not revenue you've earned but haven't collected. Not expenses you owe but haven't paid. Actual money, actually moving.

It's like breathing:

- Cash inflow = Inhaling (customer payments, loans, investments)

- Cash outflow = Exhaling (salaries, rent, suppliers, taxes)

- Positive cash flow = Breathing normally

- Negative cash flow = Holding your breath (you can't do it forever)

The kicker? A profitable business can have negative cash flow for months. An unprofitable business can have positive cash flow. This paradox kills more companies than competition ever will.

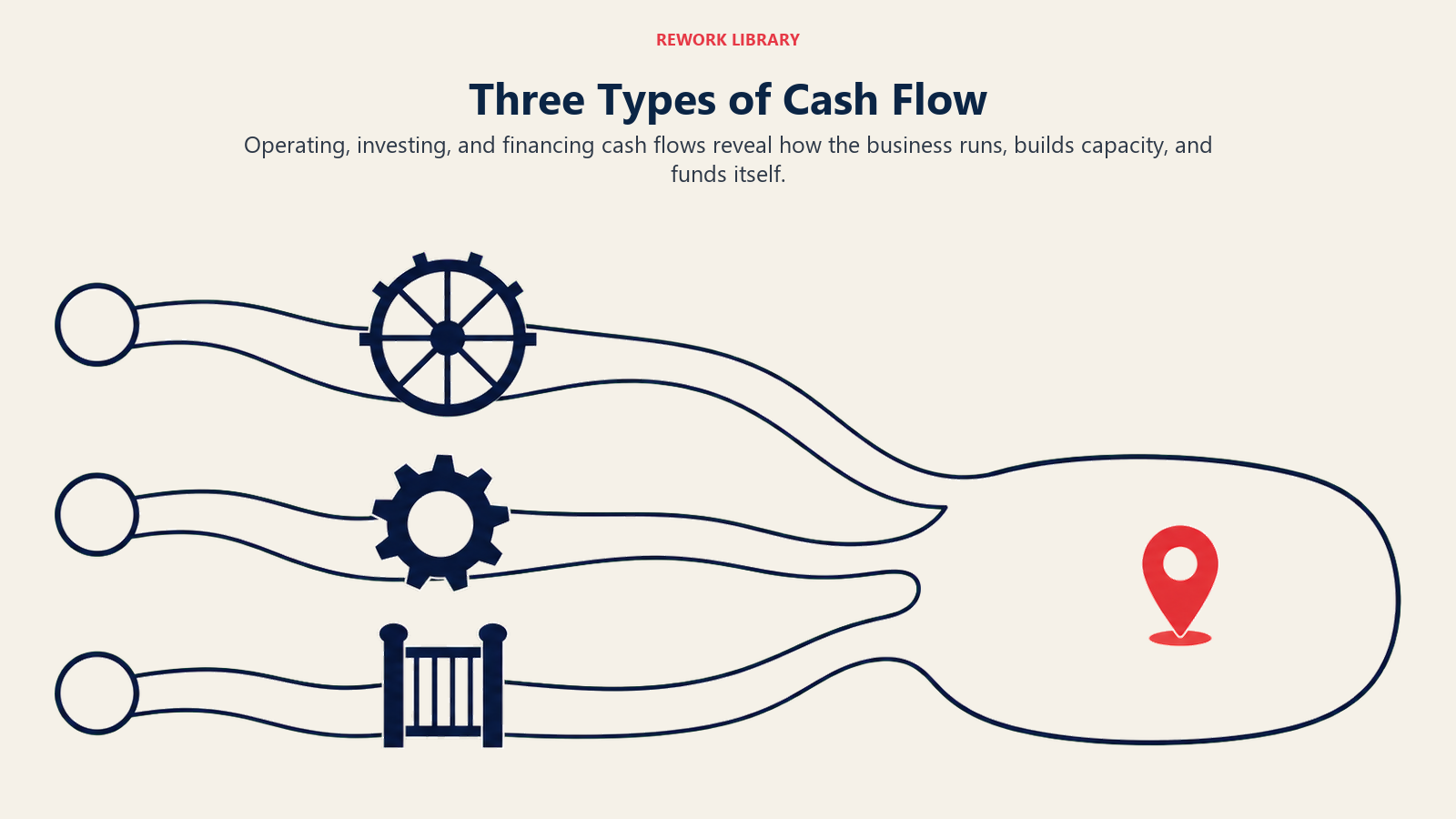

The Three Types of Cash Flow Every CEO Must Track

Separating cash activity into operating, investing, and financing streams reveals how the business runs, builds capacity, and funds itself.

1. Operating Cash Flow (CFO)

Money from your core business. This is your health check.

Healthy signs:

- Collecting faster than spending

- Growing with revenue

- Positive without financing tricks

Warning signs:

- Always waiting for that "big payment"

- Using credit cards for payroll

- Suppliers calling about overdue invoices

2. Investing Cash Flow (CFI)

Money spent on assets or earned from selling them.

Normal patterns:

- Growing companies: Negative (buying equipment)

- Mature companies: Balanced

- Struggling companies: Positive (selling assets)

3. Financing Cash Flow (CFF)

Money from loans, investors, or paid to them.

What to watch:

- Too dependent on financing = risky

- All outflow = might be too conservative

- Erratic patterns = poor planning

The Cash Flow Statement Decoded

Forget accounting speak. Here's what actually matters:

Starting Cash: What's in the bank + Money collected: From customers (not sales!) - Money paid out: To suppliers, employees, landlord = Operating cash flow: Did operations add or drain cash? - Money invested: Equipment, acquisitions + Money raised: Loans, investor funds = Ending Cash: What's left

If ending cash < starting cash repeatedly, you're in trouble.

Real Company Cash Flow Patterns

The Amazon Model (Negative to Positive)

Early years: Negative operating cash flow Strategy: Raise capital, grow fast, worry about profit later Turning point: Scale creates efficiency Today: Massive positive cash flow

When it works: Network effects, winner-take-all markets When it fails: No path to efficiency (see WeWork)

The Dell Model (Negative Cash Conversion)

The magic: Collect from customers before paying suppliers Example:

- Customer pays: Day 1

- Dell pays supplier: Day 45

- Result: 44 days of free financing

Your opportunity: Negotiate payment terms

- Collect faster: Offer 2% discount for immediate payment

- Pay slower: Push suppliers from Net 30 to Net 45

The SaaS Model (Predictable Flow)

Pattern: Annual contracts paid upfront Result: Cash flow spikes in January Challenge: Managing the rest of the year Solution: Monthly payment options (less cash but steadier)

Why Good Companies Run Out of Cash

Scenario 1: The Growth Trap

- Land huge client (yay!)

- Need to hire/buy equipment upfront

- Client pays Net 60

- You're broke on day 45

Scenario 2: The Inventory Squeeze

- Sales growing 50% yearly

- Need more inventory

- Suppliers want payment

- Cash tied up in products

Scenario 3: The Success Disaster

- Finally profitable!

- Owe taxes on profit

- But profit ≠ cash

- Tax bill bankrupts you

Your 13-Week Cash Flow Forecast

The only forecast that matters. Here's the template:

Week 1-13 columns with:

- Starting cash

- Expected collections (be pessimistic)

- Required payments (be realistic)

- Ending cash

- Minimum cash needed (usually 2 weeks expenses)

Red flags:

- Any week below minimum

- Declining trend

- Too dependent on one payment

Update this weekly. Not monthly. Weekly.

Cash Flow Optimization Tactics

Immediate (This Week)

- Invoice immediately - Same day delivery = same day invoice

- Call overdue accounts - Personal calls collect 70% more

- Pause non-critical spending - Every subscription, every purchase

- Offer payment plans - Turn big invoices into steady flow

Short-term (Next Month)

- Renegotiate terms - Even 15 extra days helps

- Factor receivables - Get 80% now vs 100% later

- Inventory management - Less stock = more cash

- Prepayment incentives - 5% discount for upfront payment

Strategic (Quarter+)

- Business model shift - Subscription vs one-time

- Customer concentration - No client over 20%

- Operating leverage - Fixed costs to variable

- Cash reserves - Target 3-6 months expenses

Tools & Technology

For Tracking

- QuickBooks Cash Flow Planner: Built-in forecasting

- Float: Dedicated cash flow forecasting

- Pulse: Visual cash flow for small business

For Improving

- Bill.com: Optimize payables timing

- Stripe/Square: Faster payment processing

- Fundbox: Invoice financing

For Analysis

- Cash flow ratios: Track trends

- Scenario planning: What-if analysis

- Automated alerts: Low balance warnings

The Psychology of Cash Management

Why CEOs fail at cash flow:

- Optimism bias - "That payment will definitely come"

- Growth obsession - Revenue over cash

- Profit fixation - P&L over cash flow statement

- Ego protection - Not wanting to "chase" payments

The mindset shift:

- Cash is king, everything else is commentary

- Better to grow slowly with cash than fast without

- Pride doesn't pay bills

Your Cash Flow Action Plan

Stop reading. Start doing:

Today:

- Check actual bank balance

- List all money owed to you

- List all money you owe

- Calculate weeks of cash remaining

This Week:

- Build 13-week forecast

- Call top 5 overdue accounts

- Identify cash flow bottlenecks

- Set up daily cash position email

This Month:

- Renegotiate payment terms

- Implement collection process

- Create cash flow dashboard

- Build emergency fund

Cash flow isn't sexy. It's not innovative. It won't get you featured in TechCrunch. But it will keep you in business when your "profitable" competitors disappear.

Master cash flow, and you master business survival. Everything else is just details.

Next steps? Understand Working Capital to optimize your cash conversion cycle, or dive into Burn Rate if you're in growth mode.

Part of the [Business Terms Collection]. Last updated: 2026-01-21

On this page

- Cash Flow: The Real Story

- The Three Types of Cash Flow Every CEO Must Track

- 1. Operating Cash Flow (CFO)

- 2. Investing Cash Flow (CFI)

- 3. Financing Cash Flow (CFF)

- The Cash Flow Statement Decoded

- Real Company Cash Flow Patterns

- The Amazon Model (Negative to Positive)

- The Dell Model (Negative Cash Conversion)

- The SaaS Model (Predictable Flow)

- Why Good Companies Run Out of Cash

- Scenario 1: The Growth Trap

- Scenario 2: The Inventory Squeeze

- Scenario 3: The Success Disaster

- Your 13-Week Cash Flow Forecast

- Cash Flow Optimization Tactics

- Immediate (This Week)

- Short-term (Next Month)

- Strategic (Quarter+)

- Tools & Technology

- For Tracking

- For Improving

- For Analysis

- The Psychology of Cash Management

- Your Cash Flow Action Plan