Transaction Coordination Process: Managing Every Detail from Contract to Close

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

The reality about real estate transactions: the contract is just the beginning. You've got 30 to 45 days to coordinate 8-12 different parties, track 15-20 critical deadlines, and manage wave after wave of moving parts. Somewhere between 10-15% of deals fall apart during this phase. Not because the buyer suddenly can't afford it. Not because the property burns down. But because something (a missed deadline, a miscommunication, a lost document) created enough friction that the deal unraveled. Understanding the full real estate sales cycle helps you see where transaction coordination fits into the bigger picture.

The difference between agents who consistently close deals and those who constantly firefight isn't luck. It's transaction coordination. It's having a system that ensures nothing falls through the cracks.

What Transaction Coordination Actually Means

Transaction coordination isn't glamorous. It's not about finding buyers or selling listings. It's the operational backbone that turns signed contracts into actual closings.

At its core, transaction coordination is deadline-driven project management. You're running parallel tracks simultaneously: the buyer's financing track, the seller's obligation track, the inspection track, the title track, the appraisal track. Each has its own timeline, its own deliverables, and its own failure points. Miss one deadline and everything behind it cascades.

The complexity comes from the fact that you're not controlling all these parties. The lender moves at their pace. The title company follows their process. The appraiser has their own schedule. Your job is coordinating across all of them while keeping clients calm and deals on track.

Successful coordinators understand something important: you're not just managing information. You're managing risk. Every deadline that passes, every document that needs coordinating, every conversation with a stakeholder is either moving the deal forward or creating opportunity for failure.

Why Transaction Coordinators Exist

Most real estate teams have one: a transaction coordinator. Sometimes it's a dedicated person. Sometimes it's the agent themselves. But the role exists because transaction management is too complex for the part-time approach.

A good transaction coordinator is the quarterback of the transaction. They track deadlines. They push parties to deliver. They ensure documents flow to the right places. They catch problems before they become deal-killers. They're detail-oriented, follow-up obsessed, and methodical about process.

The return on investment is clear. Teams with strong transaction coordinators see 95%+ on-time closing rates and significantly lower fall-through rates. Teams without them? Constantly dealing with extensions, last-minute firefights, and deals that collapse at the finish line.

Understanding the Transaction Timeline

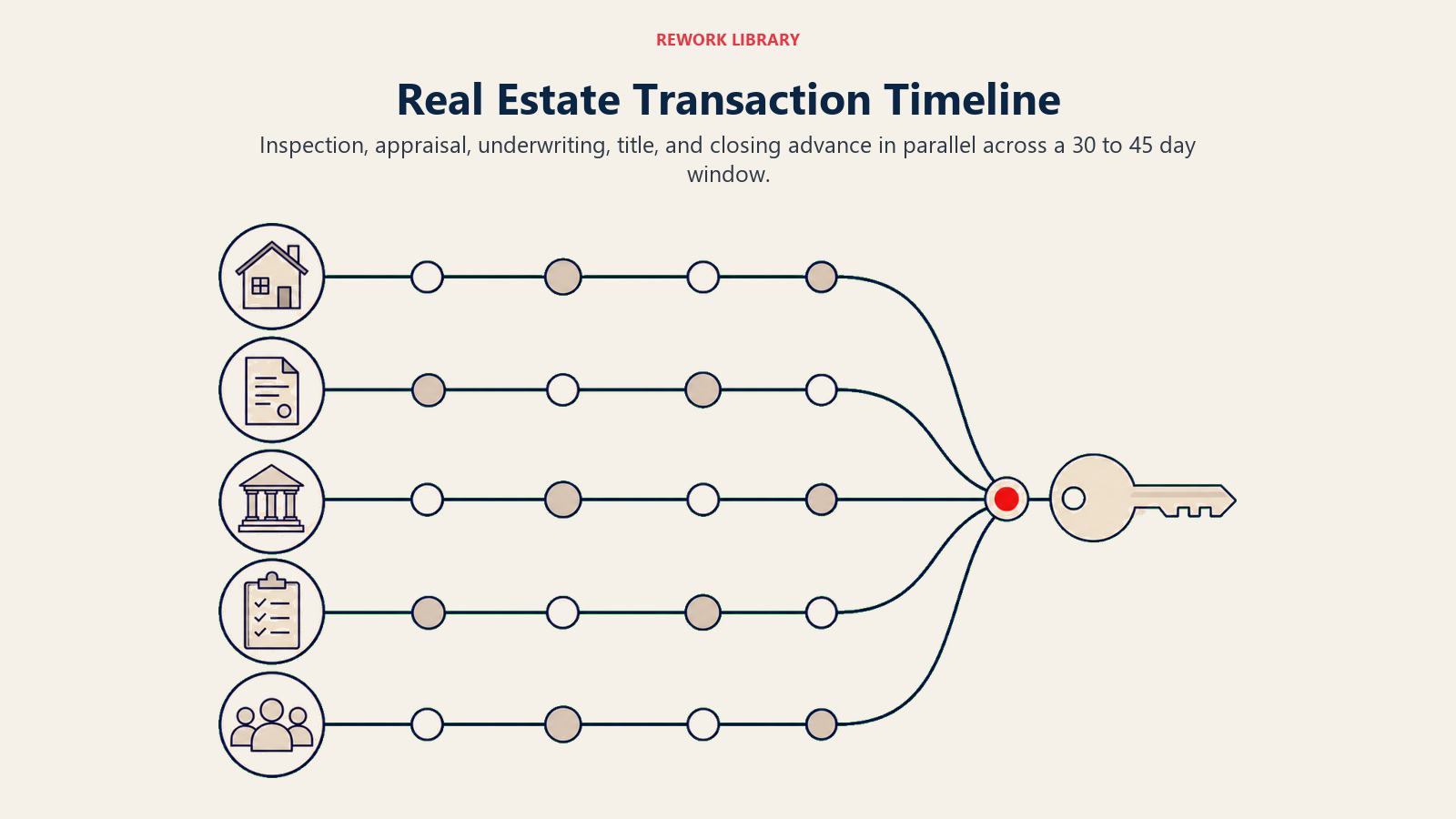

Most transactions run 30-45 days from fully executed contract to closing. The timeline varies by market and by loan type, but the structure is fairly universal.

Days 1-3 (Kickoff Phase): Everything launches at once. The contract gets distributed to all parties (buyer, seller, both agents, lender, title company). Earnest money needs depositing. Initial documents need flowing out. Inspections need scheduling. This phase is controlled chaos. The coordinator's job is making sure nothing gets missed in that first 72 hours.

Days 3-10 (Inspection Period): The home inspector is at work. The inspection report arrives and becomes the first real test. This is where many deals hit obstacles. Repair requests get negotiated. The buyer decides whether to move forward or whether issues are deal-breakers. Most inspection contingencies expire around day 7-10, so decisions happen under time pressure.

Days 7-21 (Appraisal Window): The appraiser is evaluating the property. This process usually takes 10-14 days, though it can extend. If the appraisal comes in low, you have a problem to solve. The coordinator tracks this timeline religiously because low appraisals discovered late leave no time to negotiate solutions.

Days 10-25 (Underwriting Phase): The lender's underwriting team is reviewing the buyer's financial situation, pulling documents, verifying income, running quality checks. Conditions get issued. The buyer chases down documents. This phase determines whether financing actually happens. It's also the phase where financing-related deal fallout happens most.

Ongoing (Title and Legal): Title work happens throughout the transaction. The search takes time. Problems surface. HOA documents get reviewed. Liens appear and need resolution. Surveys happen if needed. The coordinator watches this timeline because title problems surfacing late create time pressure.

Days 28-30/45 (Final Push): Final walkthrough happens. Closing disclosure gets reviewed. Closing logistics get coordinated. This is the home stretch, but it's also where late-surfacing issues can create panic.

The key insight coordinators understand: these phases overlap significantly. You can't wait for one to finish before starting another. Everything moves in parallel, and that's where coordination becomes critical.

Phase 1: Contract Acceptance to Day 1

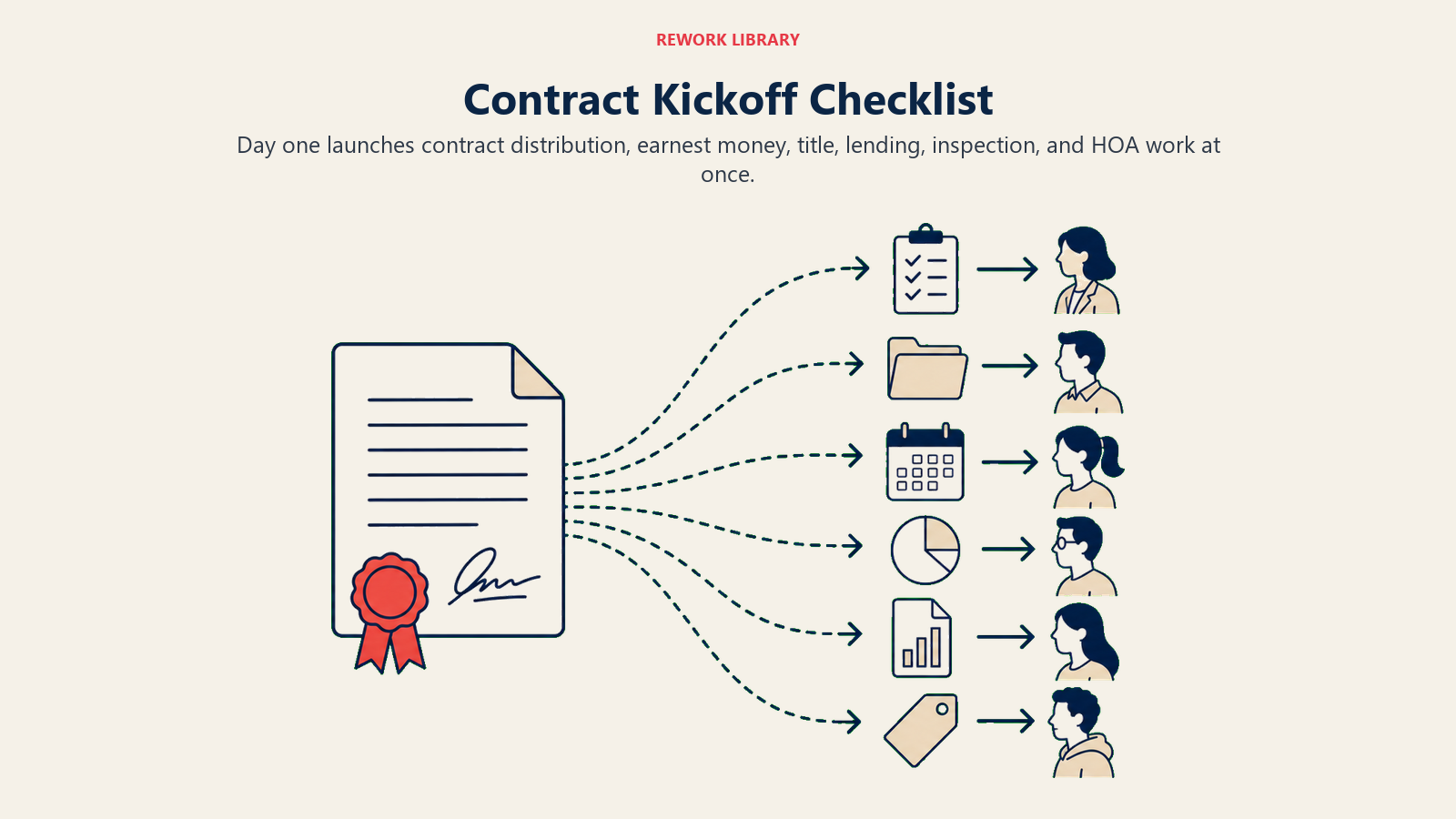

The moment that contract fully executes, the clock starts and your action list expands immediately.

Distribute the contract immediately. Every party needs a signed copy: buyer, seller, both agents, lender, title company. Don't batch this. Don't wait until end of day. Do it now. Each hour of delay creates cascading delays downstream.

Verify earnest money deposit. Most contracts require earnest money within 1-3 days. Connect your buyer with the escrow holder. Confirm the amount and wire details. Follow up the next business day to verify the money actually deposited. Never assume it happened.

Initiate title work. Give the title company everything they need to open a file immediately: buyer's name, seller's name, property address, purchase price, and your contact information. The longer they wait to start searching, the longer it takes to surface and resolve title problems.

Get the lender and buyer connected. Provide your buyer with the lender's contact information so they can start the loan application. The buyer needs to understand that this is urgent. Every day waiting to start the application is a day lost from underwriting.

Schedule the home inspection. Many contracts have 7-10 day inspection contingency periods. If the buyer waits until day 4 to contact an inspector, the inspector might not be available until day 9. Help your buyer understand that inspection scheduling is urgent. Provide recommendations for qualified inspectors.

Request HOA documents. If the property is in an HOA, request the documents from the seller or HOA management right now. These typically take 3-5 business days to gather. Late discovery of HOA issues creates last-minute complications.

Send the buyer a transaction checklist. Give them visibility into what's coming, what they need to do, and which deadlines matter. This reduces anxiety and prevents surprises. Understanding the buyer journey stages helps you tailor communication to their specific needs at each phase.

Phase 2: Inspection Contingency Coordination

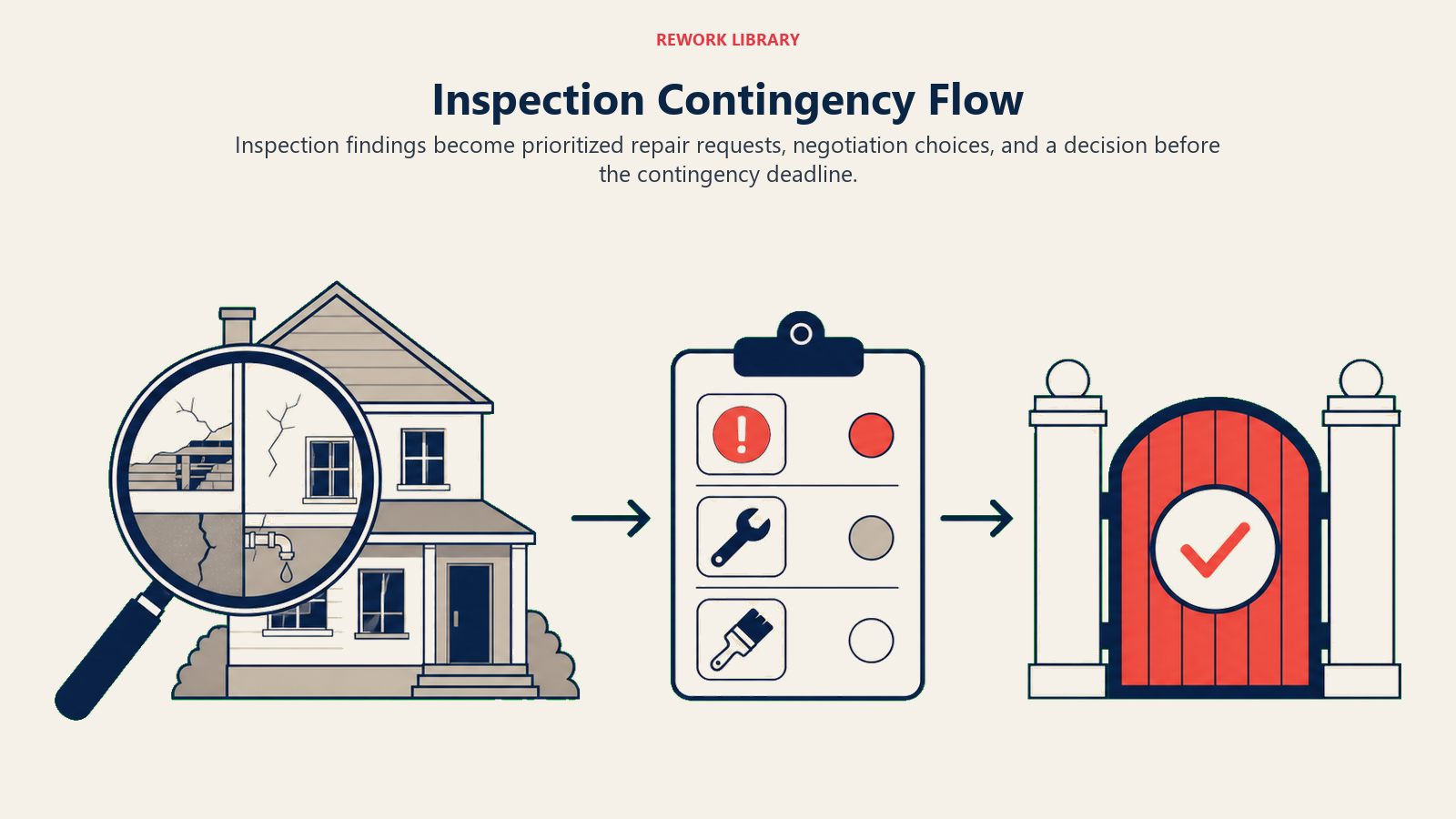

The home inspection is the first major test. This is where deals most commonly hit their first real obstacle.

Help the buyer choose a qualified inspector. Not all inspectors are equal. A thorough inspector documents everything clearly. They explain what they find in plain language. They understand the difference between deferred maintenance and actual problems.

Recommend attending the inspection. You should ideally be there. The inspection report is typically 20-30 pages. Most buyers don't understand what everything means. Your presence allows you to explain severity, distinguish cosmetic issues from functional problems, and help prioritize.

Review the inspection report with the buyer. Don't just send them the PDF and disappear. Walk through major findings. Explain what's actually a problem versus normal wear and tear. This conversation determines whether the buyer panics and walks away or calmly proceeds.

Prepare repair requests strategically. If the inspection found issues, help your buyer prioritize. Focus on structural problems, safety issues, and systems failures. Cosmetic stuff typically gets negotiated away. Too many minor requests dilutes your leverage on the important ones.

Manage the repair negotiation. The seller responds with agreement, partial agreement, or refusal. The back-and-forth negotiation can take several days. You're trying to reach agreement: will the seller fix it, provide a credit, or will the buyer accept as-is?

Hit the inspection contingency deadline. This deadline (usually day 7-10 from contract) is firm. Your buyer must decide: are they moving forward, requesting more concessions, or walking? Missing this deadline locks them in.

Coordinate re-inspections if necessary. If the seller agreed to repairs, schedule a re-inspection before the contingency deadline expires to confirm work was actually completed to satisfaction.

For comprehensive guidance on this critical phase, see Inspection Contingency Management, which details inspection selection, report analysis, and negotiation tactics.

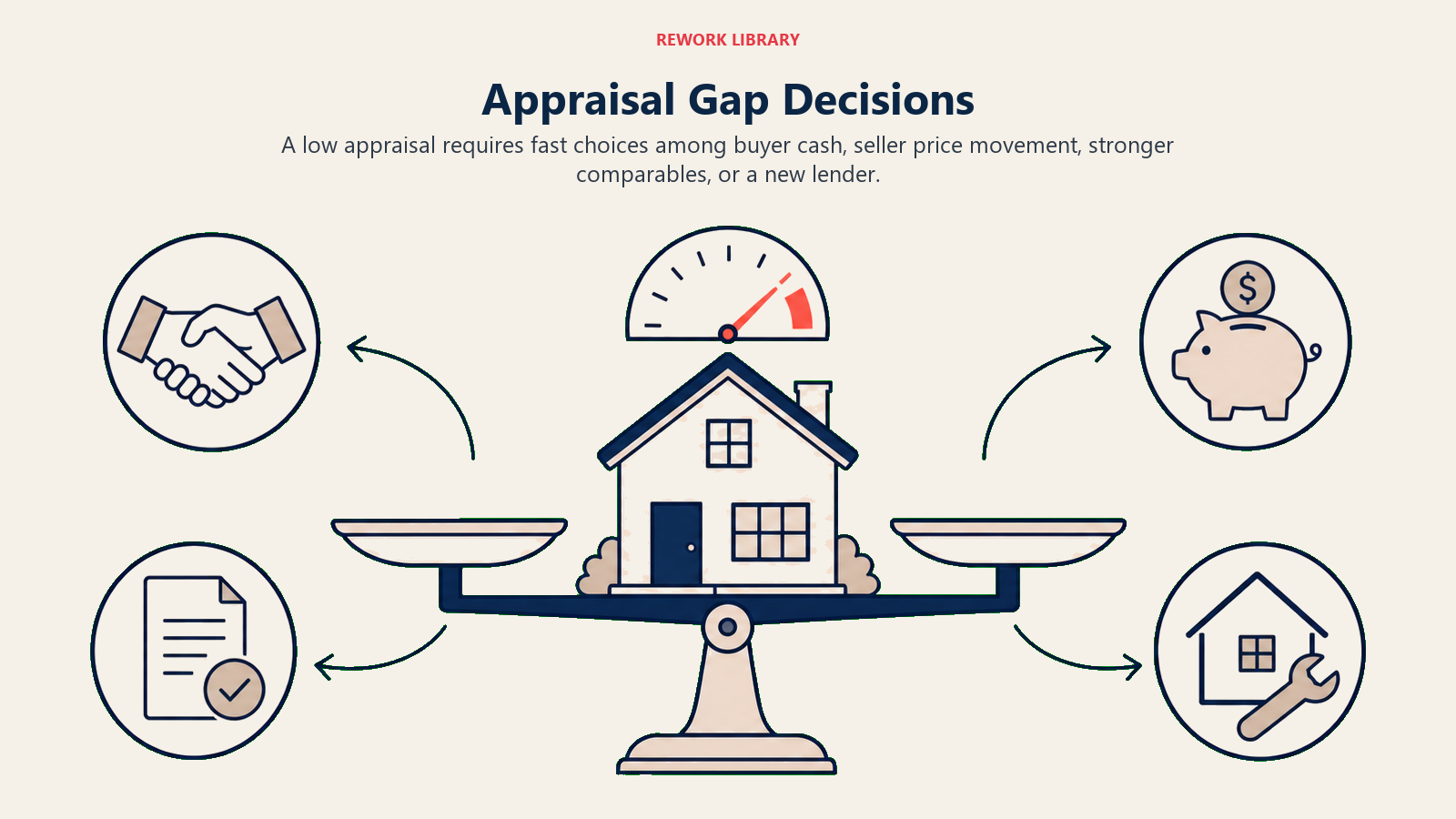

Phase 3: Appraisal Process Management

The appraisal determines whether property value supports the loan amount. It's also where deals can hit unexpected walls.

The lender orders the appraisal, not you. But you support the process. Provide the appraiser with property access. Offer comparable sales information that supports the contract price. If the appraiser asks questions, respond quickly.

Monitor for low appraisals. If the appraisal comes in below contract price, you've got a real problem. The buyer's financing might not work. They might refuse to cover the gap. The deal could collapse.

Have contingency plans ready. Can the buyer cover the appraisal gap with cash? Can the seller come down on price? Can you challenge the appraisal with better comparables? Could the buyer need to find a different lender?

Communicate the appraisal results promptly. Don't hold bad news hoping it resolves. If there's an appraisal issue, tell the parties immediately so solutions can be developed.

Remove the appraisal contingency once you're confident the property value supports the loan and the buyer is satisfied.

Learn more about managing this critical phase by reviewing Appraisal Process Management, which covers everything from appraisal ordering to resolving low valuation issues.

Phase 4: Financing and Underwriting Coordination

Financing is the most common reason deals fall apart. Underwriting is where lenders discover problems.

Maintain consistent lender contact. Don't wait for bad news. Call weekly. Ask for status updates. Learn which conditions are being issued that the buyer needs to address. Weekly check-ins catch problems early before they become blockers.

Track underwriting conditions religiously. Lenders issue conditions: "provide recent pay stubs," "verify employment," "explain that deposit," "update your asset statement." Each condition must be fulfilled. Your job is ensuring the buyer understands urgency and gets documents in fast.

Monitor rate lock decisions. Interest rates move daily. Your buyer needs to understand their rate situation and when they need to lock in. A delayed rate lock decision can become a closing problem.

Watch for underwriting red flags: Job changes (lenders hate these during underwriting), credit score drops, large deposits that can't be explained, new debt that appeared, or income that fails to verify. These are deal-killers. If you spot them, raise them immediately so solutions can be developed.

Pursue "clear to close" as the ultimate milestone. This status means underwriting is satisfied, the loan is approved, and they're ready to fund. This typically happens 3-5 days before closing. Successfully managing this financing stage is closely tied to the buyer's mortgage pre-approval process set up earlier.

Phase 5: Title and Escrow Coordination

Title issues can surface at any point and derail everything if not caught early.

Follow the title search timeline. The title company is searching for problems: liens, claims, boundary issues, HOA restrictions. This takes time. Stay on top of their timeline so problems surface early, not three days before closing.

Resolve title issues immediately. If liens appear, arrange payoffs. If claims exist, settle them. If surveys show problems, find solutions. The key is addressing issues while you have time.

Review HOA documents thoroughly. Are there special assessments pending? Restrictions your buyer should know about? Documented disputes? Condo conversion issues? Flag these for your buyer and ensure they understand implications.

Verify title insurance. The lender requires it, so it gets ordered automatically, but confirm it's ordered and the premium is accounted for in closing costs.

Request any additional documents needed. Condo documents, HOA budgets, survey certifications, affidavits for minor title issues, request these early so nothing causes last-minute delays.

To master all aspects of this critical coordination phase, review Title & Escrow Coordination, which provides detailed procedures for title search tracking and issue resolution.

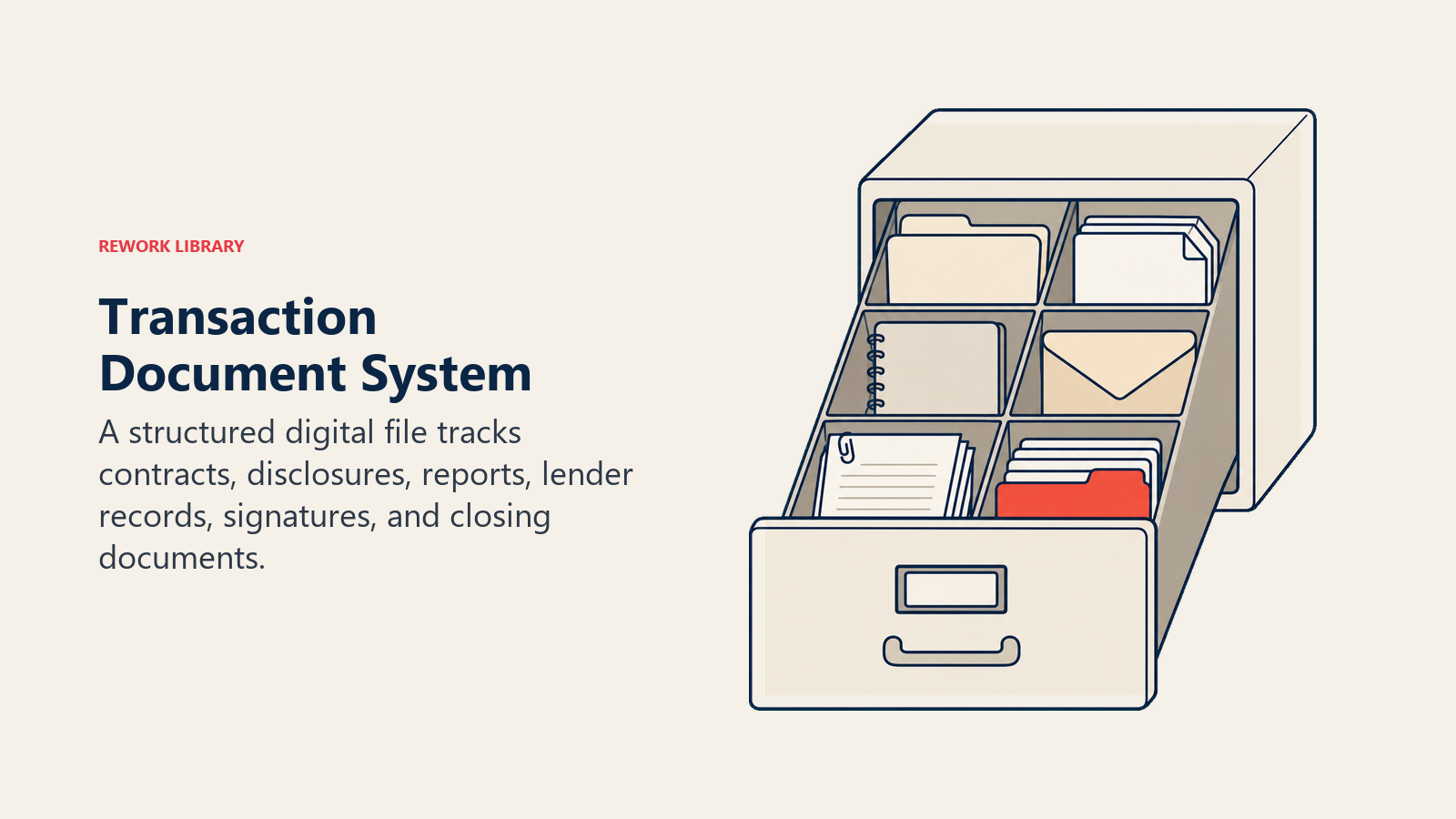

Phase 6: Document Management System

Transaction success depends on documents flowing to the right places at the right times.

Organize the digital file. Create a folder structure: contract and addenda, earnest money, inspection reports, appraisal, lender documents, title documents, HOA materials, closing documents. Everything goes in the right folder. Nothing gets lost.

Track disclosures. Real estate transactions involve multiple required disclosures: lead-based paint, property condition, HOA documents, and state-specific disclosures. Make sure all required disclosures were delivered to the buyer and they were signed off.

Manage inspection reports. Once received, the inspection report needs review by the buyer, shared with the seller if requesting repairs, and archived in the transaction file.

Organize lender documentation. Paystubs, tax returns, bank statements, employment verification, pay stubs, these documents need organized and tracked so nothing gets lost.

Coordinate e-signatures securely. Many documents now get signed electronically. Use secure platforms (not email). Maintain a record of what was signed and when.

Create a document checklist. Before closing, verify you have every document needed: signed contract, earnest money receipt, inspection reports, appraisal, loan approval letter, title commitment, HOA documents, all required disclosures, final closing disclosure.

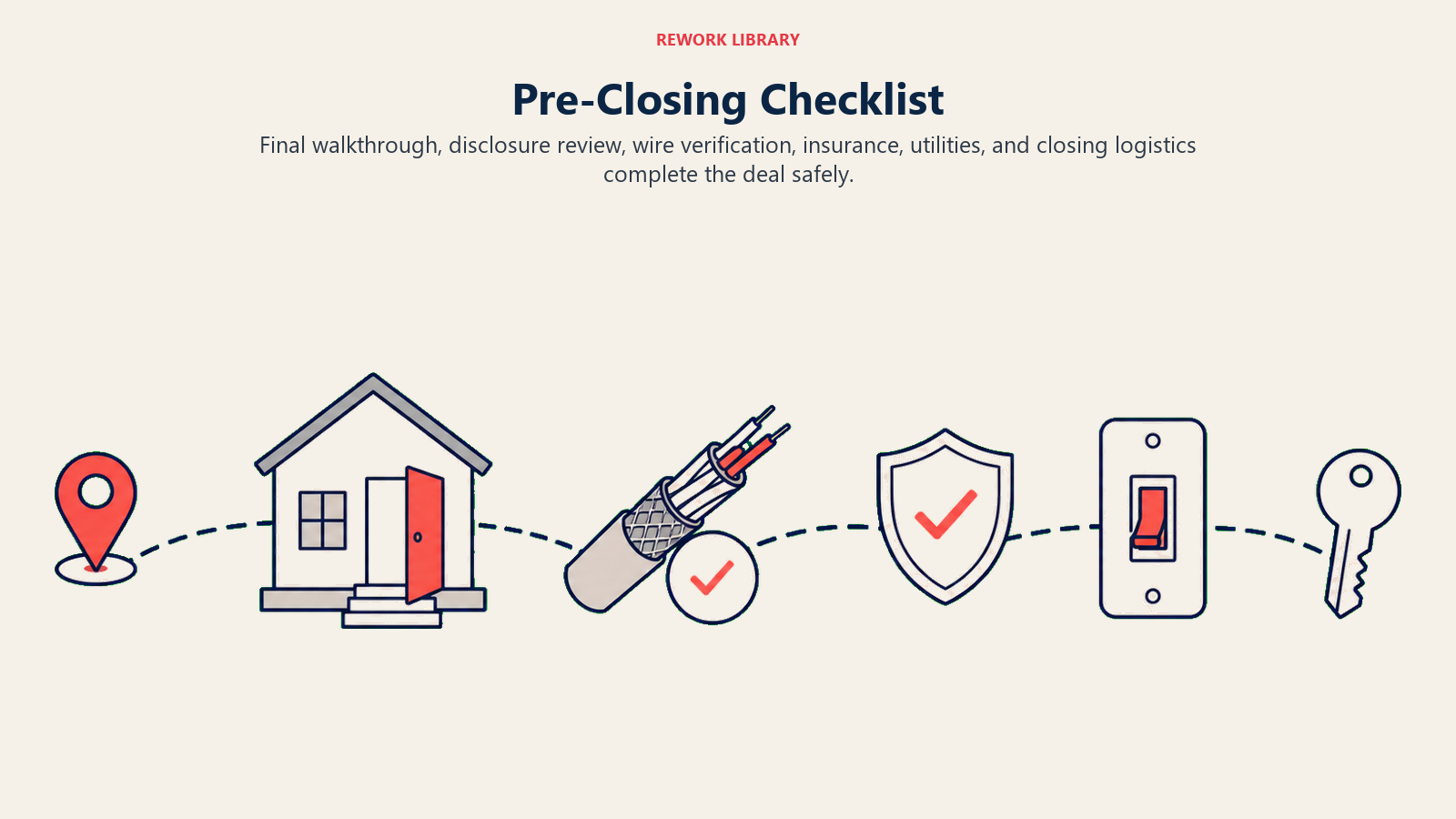

Pre-Closing Checklist and Final Steps

As you approach closing, a comprehensive checklist ensures nothing gets overlooked.

Schedule and conduct the final walkthrough. This happens 1-2 days before closing. The buyer does a final inspection: Are agreed-upon repairs actually completed? Has anything new appeared? Are utilities being transferred? Is everything ready for move-in?

Review the closing disclosure together. This document shows all financial details: interest rate, loan amount, monthly payment, all costs and credits. Review it with your buyer before closing day so there are no surprises on signing day.

Prevent wire fraud. Closing fraud is increasingly common. Verify wire instructions directly by calling the title company's main phone number (not responding to an email). Have your buyer do the same. Don't trust wire instructions that arrive via email.

Coordinate closing logistics. Know where closing is happening, what time, how long it will take. Make sure your buyer knows parking, building access, and what documents to bring.

Confirm homeowner's insurance. The lender requires proof of homeowner's insurance before funding. Make sure your buyer's insurance agent has sent the final policy to the lender.

Arrange utility transfers. Coordinate with the seller about when utilities transfer. Make sure your buyer knows they need to contact utilities to set up service for move-in day.

Prepare a closing day summary. Create a one-page document for your buyer showing: closing location and time, what to bring, expected timeline, what to expect, and your contact number if questions arise.

Attend closing or be available. Issues can pop up in final documents. You're there to keep things moving and resolve any last-minute questions or concerns.

Learn the complete pre-closing workflow by reading Closing Day Preparation, which covers final walkthroughs, document review, and day-of coordination in depth.

Stakeholder Communication Protocols

Transaction success depends on keeping everyone informed and moving in the same direction.

Your buyer: Weekly updates minimum, even if nothing has changed. Notify them of every milestone: "Contract fully executed," "Inspection scheduled," "Appraisal ordered," "Clear to close." Each milestone is progress and keeps them confident.

The seller and listing agent: Coordinate repairs, address requests, communicate timeline. Keep it professional and efficient.

The lender: Weekly status calls. Track document submission. Manage conditions. This relationship often determines whether deals close on time.

Title company: Ensure they have everything they need. Follow their timeline. Address issues immediately when they surface.

Service providers: Inspectors, appraisers, contractors, make sure they have property access, timelines are locked, and schedules don't conflict.

Insurance agent: Your buyer needs homeowners insurance ordered early. Confirm it's in place before closing.

Common Transaction Challenges and Solutions

Certain problems appear in nearly every busy transaction coordinator's career.

Financing delays: Underwriting takes longer than expected. Documents get lost. Income fails to verify. Appraisals come in low.

Solution: Submit all documents early. Don't wait for the lender to request them. Get the buyer's financials in on day one so underwriting has everything from the start. Build buffer time into your closing date.

Inspection disputes: The buyer finds expensive repairs and wants major concessions. The seller refuses to negotiate. Neither side will budge.

Solution: Help your buyer prioritize requests and focus on structural and safety issues. Position yourself as neutral mediator. Explore creative solutions: seller provides credit, repairs get split, buyer accepts as-is with a price adjustment.

Title problems: Liens appear. Boundary questions surface. HOA issues get flagged. Survey problems show up.

Solution: Ask the title company to flag any issues immediately as they're discovered, not as a package at the end. This gives you maximum time to resolve them.

Coordination breakdowns: People stop communicating. Documents get lost. Deadlines get missed. Nobody's talking to anybody.

Solution: You become the hub. Weekly updates to all parties. Documentation of all communications. Clear action items and responsible parties.

Buyer cold feet: The buyer second-guesses the price, the property, or their own financial readiness.

Solution: Stay in regular contact. Provide reassurance. Explain what's happening. Address concerns directly. Sometimes buyers just need more communication.

Last-minute surprises: Final walkthrough reveals repairs weren't done. Closing disclosure shows unexpected costs. Wire fraud attempts happen. Something appears in the final title search.

Solution: Build buffer time. Don't schedule closing for the absolute latest possible day. Have contingency plans ready for common issues.

Understand more about preventing deals from falling apart by reading Deal Fallout Prevention, which covers the warning signs and intervention strategies that save deals in crisis moments.

Building Your Transaction Coordination System

Systematic coordination requires tools, process, and discipline.

Get transaction management software. Options abound: Paperless Pipeline, BriteCore, Follow Up Boss, and others. These platforms track deadlines, send reminders, coordinate information flow, and reduce the chance of something getting missed. Pick one that integrates with your business. Choosing the right platform is part of your broader real estate CRM selection strategy.

Create a standardized checklist. The same checklist applies to every deal. Same steps, same sequence, same deadlines. This consistency prevents missed items. You execute the same process 50 times a year, that's how nothing falls through the cracks.

Set multiple deadline reminders. For every critical deadline, set alerts at 1 week before, 3 days before, and 1 day before. These reminders prevent oversights that seem obvious until they happen.

Document every communication. Keep records of calls, emails, and conversations. This protects you and eliminates confusion about who said what.

Build communication templates. Weekly updates, new party introductions, issue notifications, closing day summaries, create templates you can quickly personalize. This saves time and ensures consistency.

Create decision trees for common issues. When a low appraisal happens, what are your steps? When inspection issues arise, what's the process? Document your problem-solving approach so it's consistent and proven.

Establish escalation protocols. Know when to involve your broker. Know when to push back on a lender. Know when to extend a deadline. Have clear escalation pathways.

Measuring Coordination Success

Track these metrics to understand how well your transaction coordination is working:

On-time closing rate: What percentage of transactions close on their scheduled date? Aim for 95%+ if you're using strong coordination.

Fall-through rate: What percentage of contracts fail to close? Strong coordination keeps this below 3-5%.

Average days to close: Are you beating market average? Are your closings faster or slower than peers?

Extension requests: How often do closings need to extend? Frequent extensions signal coordination issues. Understanding your real estate metrics & KPIs provides benchmarks for transaction performance.

Issue resolution time: When problems surface, how fast do you typically solve them?

Client satisfaction: Post-closing, do buyers feel good about their experience? Did the coordination process feel smooth or chaotic?

Strong metrics in these areas show your coordination is working. Weak metrics show you need better systems, better tools, or more discipline about process.

Moving Toward Implementation

The real estate agents who consistently close deals aren't smarter or luckier than others. They've just built systems that catch issues early and manage complexity methodically.

To build your coordination system: Start with understanding the full transaction timeline. Learn what needs to happen in what sequence. Understand which deadlines are fixed and which have flexibility.

Then layer in tools. Get transaction management software. Create checklists. Set reminders. Establish communication templates.

Next, define roles. Is everything on you personally? Are you delegating to a transaction coordinator? Do you have broker support? Make expectations clear. As your business grows, you might need to consider building a real estate team structure to handle coordination systematically.

Finally, measure and iterate. Track your metrics. Find where your process breaks down. Fix it. Run the same process the next deal and measure again.

For deeper context on the earlier phases that set up smooth transactions, explore Contract to Closing Pipeline, which covers the full transaction arc from contract acceptance forward. You might also benefit from reviewing Inspection Contingency Management and Title & Escrow Coordination to master those specific phases in depth.

Most importantly: remember that this phase determines whether you actually get paid. The deal doesn't close itself. The commission isn't earned at signature, it's earned at funding. Systematic transaction coordination is what puts commissions in your account and happy clients in their new homes.

Learn More

Strengthen your transaction coordination expertise with these related resources:

- Offer Preparation & Negotiation - Master the pre-transaction phase that sets up smooth coordination

- Buyer Retention & Engagement - Keep buyers engaged throughout the long transaction timeline

- Speed-to-Lead Response - Apply urgency principles from lead response to transaction deadlines

- Client Retention Strategy - Turn smooth transaction coordination into referral generation

Senior Operations & Growth Strategist

On this page

- What Transaction Coordination Actually Means

- Why Transaction Coordinators Exist

- Understanding the Transaction Timeline

- Phase 1: Contract Acceptance to Day 1

- Phase 2: Inspection Contingency Coordination

- Phase 3: Appraisal Process Management

- Phase 4: Financing and Underwriting Coordination

- Phase 5: Title and Escrow Coordination

- Phase 6: Document Management System

- Pre-Closing Checklist and Final Steps

- Stakeholder Communication Protocols

- Common Transaction Challenges and Solutions

- Building Your Transaction Coordination System

- Measuring Coordination Success

- Moving Toward Implementation

- Learn More