Mortgage Pre-Approval Process: The Agent's Guide to Financial Qualification

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

If you've been in real estate for more than a few months, you've probably experienced this: spending weeks showing homes to a buyer only to discover they can't actually afford any of them. Or worse, they get to an offer and suddenly financing falls through. This is where mortgage pre-approval becomes your secret weapon.

Working with pre-approved buyers reduces wasted time by 60-70%. But beyond just saving yourself hours of unproductive showings, understanding the pre-approval process helps you have better conversations with clients, stronger negotiations with sellers, and faster deals overall. It's a critical component of your buyer qualification framework that separates serious buyers from those just browsing.

Let's break down everything you need to know about guiding buyers through pre-approval and using that qualification to build your business.

Pre-Qualification vs Pre-Approval: Know the Difference

Before we dive into the process, it's important to understand what you're actually dealing with. These terms get thrown around interchangeably, but they mean very different things.

Pre-qualification is a rough estimate. A buyer gives a lender basic information, income, debts, savings, and the lender says something like "based on what you've told us, you could probably borrow $300,000." No documentation. No credit check. It's a starting point, nothing more.

Pre-approval is the real deal. The lender has verified everything through actual documents, run your credit report, and calculated your exact borrowing capacity. You get a formal letter stating you're approved for a specific loan amount, typically valid for 60-90 days.

Why this matters to you as an agent: sellers care about pre-approval letters. When you submit an offer with a pre-approval in hand, the listing agent knows your buyer is serious and qualified. Without it, your offer looks like one of dozens they might receive from uncertain buyers. This becomes especially critical in multiple offer situations where you need every competitive advantage.

From the buyer's perspective, pre-approval gives them confidence about their actual budget. Too many buyers walk into your office thinking they can afford $500,000 when they can really only qualify for $350,000. Pre-approval forces that reality check before they fall in love with the wrong property.

The Pre-Approval Process Explained

The pre-approval process typically takes 1-3 business days from start to finish, though some lenders can move faster with simple cases. Here's what actually happens behind the scenes:

Initial Financial Conversation

The lender's job starts with understanding your buyer's full financial picture. They'll ask about:

- Gross annual income from all sources

- Current debts and monthly obligations

- Savings and down payment funds

- Employment history and stability

- Any recent major financial events (bankruptcy, foreclosure, late payments)

This conversation determines whether the buyer is even a candidate for a loan and which programs might work best. Someone who's recently been self-employed will follow a different path than a W-2 employee, for example. This is similar to what you'll cover in your initial buyer consultation, so coordinate with lenders to avoid redundant questions.

Documentation Review

Once the lender understands the basics, they'll request documentation. This is where buyers often get stuck because they don't realize how much is needed. A typical package includes:

Identification & Employment:

- Two forms of valid ID (driver's license, passport)

- Most recent pay stubs (usually 30 days)

- W-2s or 1099s from the past two years

- Offer letter if recently hired

- Employment verification via phone or online system

Financial Documents:

- Bank statements (typically 2 months)

- Investment account statements (2 months)

- Retirement account statements if using funds for down payment

- Proof of funds if paying cash for closing costs

Tax Returns:

- Past two years of personal tax returns

- Previous two years of business tax returns (if self-employed)

- Schedule C, K-1, or other supporting documents for self-employment income

Debt Information:

- Mortgage statement if currently a homeowner

- Car loan statements

- Student loan statements

- Credit card statements or account numbers

- Any other debt obligations

The amount of documentation varies based on the loan type and individual circumstances, but lenders almost always ask for more than buyers expect.

Credit Check and Report Review

The lender pulls a full credit report and credit score. They're looking for:

- Current credit score (typically need 620+ for FHA, 680+ for conventional)

- Payment history and any late payments

- Collection accounts or charge-offs

- Recent inquiries that might indicate new debt

- Overall credit utilization (how much of available credit is being used)

If there are issues, a late payment from three years ago, a collections account, high credit utilization, the lender discusses solutions. Sometimes it's just explaining what happened. Sometimes the buyer needs to pay down debt or wait for negative marks to age before approval is possible.

Income and Employment Verification

Beyond the documents, lenders verify employment directly. They might call your employer, check via automated verification systems, or request a verification of employment letter. The goal is confirming you're still employed and earning what you claim.

Self-employed buyers face extra scrutiny here. Lenders typically want to see 2-3 years of tax returns and might request an accountant's letter. Income averaging is common for self-employed individuals, especially those in their first few years of business.

Asset and Down Payment Verification

Lenders verify that down payment funds are actually available. They look for the source of funds: savings, a gift, investment accounts. If it's a gift from family, they'll want a gift letter stating the money doesn't need to be repaid.

If the down payment is less than 20%, the lender looks at all liquid assets to make sure the buyer can cover closing costs and still have reserves after closing.

Debt-to-Income Calculation

This is the critical metric that determines actual borrowing capacity. The lender calculates:

- Front-end ratio: Housing payment (mortgage, taxes, insurance) divided by gross monthly income (usually capped at 28%)

- Back-end ratio: All monthly debt payments including housing divided by gross monthly income (usually capped at 36-43% depending on loan type)

If a buyer earns $5,000 monthly, their housing payment can typically be no more than $1,400 (28% x $5,000). If they already have $800 in car payments and $300 in student loans, their total debt can't exceed $2,150 ($5,000 x 43%), leaving only $850 for a mortgage, which isn't realistic.

Many buyers discover during pre-approval that paying off a car loan or credit card would significantly increase their borrowing power. Some do it. Some decide they'd rather keep the flexibility.

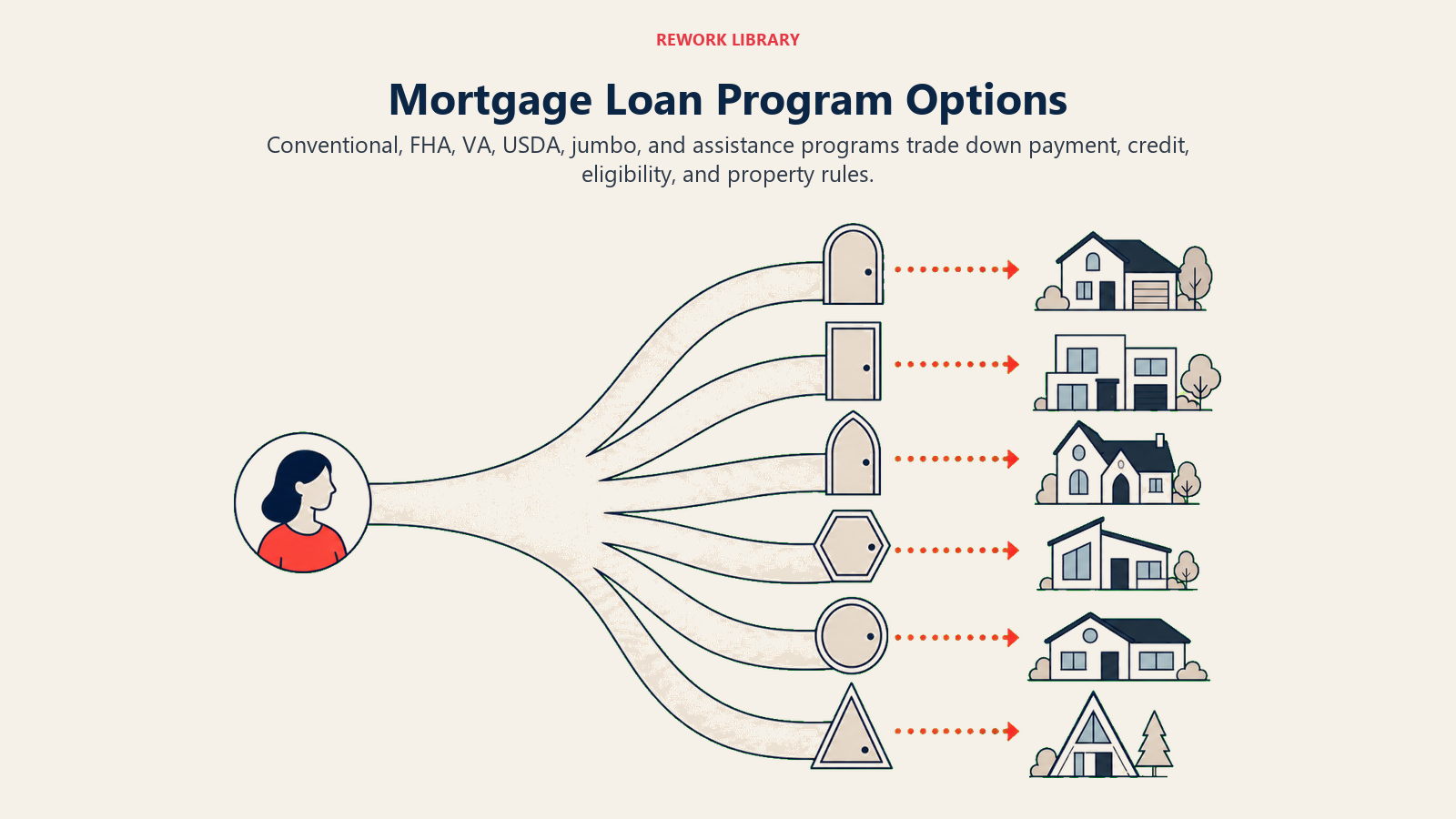

Understanding Loan Types and Programs

Pre-approval doesn't mean one-size-fits-all. Different loan programs have different requirements and benefits:

Conventional Loans

The standard option. Usually require 20% down and strong credit (680+), though many lenders go lower. Rates are typically competitive, and you get more flexibility in property types.

FHA Loans

Great for first-time buyers and those with limited down payments (as low as 3.5%). Credit score requirements are more flexible (620+). The tradeoff: mortgage insurance is required, adding to monthly payments. Limited to owner-occupied properties.

VA Loans

Available to military members, veterans, and their spouses. Often allow zero down payment and don't require mortgage insurance. VA loans typically have competitive rates and flexible credit requirements.

USDA Loans

For rural and suburban properties. Zero down payment. No mortgage insurance (though there is a guarantee fee). Great option for buyers in qualifying areas with moderate income.

Jumbo Loans

For loans exceeding conventional limits (typically $766,200+). Require strong credit and income documentation. Rates are often slightly higher than conforming loans.

First-Time Buyer Programs

Many states and municipalities offer programs with down payment assistance, favorable rates, or grants. These change frequently, so connecting buyers with local resources is valuable.

During pre-approval, the lender recommends which programs the buyer qualifies for. Some buyers qualify for multiple options and need guidance on which makes sense for their situation.

What's Actually in a Pre-Approval Letter

When the lender sends the pre-approval letter, here's what you'll see:

- Borrower name(s)

- Approved loan amount (the maximum they can borrow)

- Loan type(s) they're approved for

- Property type restrictions (single-family only, investment properties included, etc.)

- Down payment percentage(s)

- Estimated interest rate (often marked "subject to final approval")

- Estimated monthly payment

- Validity period (usually 60-90 days)

- Contingencies (conditions that must be met at closing)

- Lender contact information

The letter usually comes in two versions: one for the buyer to keep, and one for you to submit with offers.

One important distinction: the letter might say "conditional approval" or "full approval." Conditional approval means the lender has pre-approved the buyer but needs specific conditions met (like providing proof of down payment or clearing up a credit discrepancy). Full approval means they're good to go. Either way, it's solid for making offers, but conditional approvals sometimes move slower.

Your Role as the Agent

Understanding pre-approval is only half the battle. How you use that knowledge throughout the buying process makes the real difference.

Set Expectations Early

Start every buyer conversation by explaining pre-approval and why it matters. Don't just tell them to "go get pre-approved." Explain that lenders will need extensive documentation, that it typically takes 3-5 business days, and that having pre-approval before you start showing homes saves everyone time.

Many agents include pre-approval as part of their initial buyer consultation. Some even have preferred lender recommendations ready to go. Setting these expectations early is essential to your overall buyer journey stages strategy.

Build Lender Relationships

You don't need to work with dozens of lenders. Three or four solid partners who consistently deliver, communicate well, and help with problem-solving is ideal. These relationships make your life easier because:

- You know their typical timelines and requirements

- They prioritize your clients because of the relationship

- You can quickly troubleshoot issues

- You understand their personality and process

Schedule quarterly coffee meetings with your lender partners. They appreciate the business and you'll stay top of mind.

Follow Up on Status

After your buyer applies for pre-approval, don't just assume everything's moving forward. Check in every other day. Ask if the lender has received all documents. Flag any missing items before they delay the timeline.

This is especially important if you're in an active market where multiple offers happen. You might have a great property coming on and need pre-approval finalized within 48 hours. The same speed-to-lead response principles apply to internal process management.

Understand Buying Power

Pre-approval gives you a real number, but it's not always the whole story. A buyer approved for $500,000 might be more comfortable buying at $450,000. Conversely, some buyers are approved for less than they expected and need to adjust expectations.

Have a real conversation about:

- What their actual budget is (not just what they're approved for)

- Whether they want to keep financial cushion

- If they're prioritizing payment amount or staying in a specific neighborhood

- Their comfort level with debt-to-income at the higher end of approval

Identify Financial Red Flags

During pre-approval conversations, red flags sometimes emerge that could affect the deal. Employment changes, gift fund sources that create legal issues, recent big purchases that mess with debt ratios, or credit problems that affect financing.

These conversations are delicate. You're not a lender or financial advisor, but you're in a position to notice when something might derail the deal. A heads-up to the buyer ("Your lender mentioned they want to verify that job change, make sure you have that documentation ready") can prevent last-minute surprises. This awareness is crucial for deal fallout prevention throughout the transaction.

Working Effectively with Lenders

Your relationship with lenders isn't transactional. It's collaborative. You're both trying to help the same client actually buy a home.

Communication Protocols

Establish how you prefer to communicate. Some agents want daily updates on active pre-approvals. Others prefer to let lenders work unless there's an issue. Be clear about your preferences and respect theirs.

If you're submitting multiple offers on behalf of the same buyer, make sure the lender knows. Lenders see credit inquiries and sometimes get concerned when they see multiple hard inquiries from different sources.

Introduce Your Buyer the Right Way

Don't just send a lender a buyer's contact info. Call the lender, introduce the buyer, and explain their situation. This personal touch gets better service and shows the lender you're serious about the relationship.

Some agents even do a three-way call to make the introduction and answer initial questions together.

Manage Timeline Expectations

If you have a deadline, a property inspection, an offer expiration, a closing date, communicate it to the lender early. They'll prioritize accordingly. Nothing frustrates lenders more than finding out at the last minute that pre-approval was needed "yesterday."

Problem Solving

Problems come up. Credit score is lower than expected. Down payment funds can't be documented. Employment status is complicated. Don't treat the lender as an obstacle. Work with them to find solutions.

Sometimes it's requesting a manual underwrite. Sometimes it's finding a different loan program. Sometimes it's the buyer taking a different approach to their finances. The lender wants to find a yes, help them do it.

Common Qualification Issues and Solutions

Even with good pre-approval guidance, you'll encounter situations where the numbers don't initially work.

Insufficient Down Payment

Issue: Buyer doesn't have enough for down payment.

Solutions:

- Explore down payment assistance programs (many states offer these)

- Negotiate seller contribution toward closing costs (frees up buyer's cash)

- Consider lower down payment options (FHA at 3.5%, conventional at 5%)

- Gift funds from family (with proper documentation)

- Delay closing to save more

High Debt-to-Income Ratio

Issue: Other debt prevents qualifying for desired loan amount.

Solutions:

- Pay down credit cards or car loans before closing

- Increase down payment (lowers loan amount, lowers payment)

- Extend loan term (lowers monthly payment, though increases interest)

- Co-borrower with additional income

- Explore different loan programs with higher DTI allowances (some go to 50%)

Credit Score Problems

Issue: Recent late payment, collection account, or low overall score.

Solutions:

- Dispute errors on credit report (legitimate if inaccurate)

- Pay delinquent accounts current

- Request manual underwrite with lender (sometimes they approve anyway if circumstances explain issues)

- Wait 30-60 days for negative items to age

- Become an authorized user on someone else's good credit account (sometimes helps short-term)

Employment Gaps or Changes

Issue: Recent job change or employment gap concerns lender.

Solutions:

- Provide written explanation of gap

- Obtain written offer letter from new employer

- Document income consistency despite different employers

- Use co-borrower with stable employment

- Wait 30 days in new job before applying (shows stability)

Self-Employment Documentation

Issue: Lender needs proof of income stability for self-employed buyer.

Solutions:

- Provide 3 years of tax returns (more history = more comfort)

- Get accountant's letter explaining business status

- Show business is established (at least 2 years)

- Include bank statements showing deposits

- Consider co-borrower for additional income stability

Gift Funds

Issue: Down payment is gift money, which requires special documentation.

Solutions:

- Provide gift letter from donor (doesn't need to be repaid)

- Show proof that gift funds are actually available

- Document relationship between buyer and donor

- Get written explanation if donor is not a relative

- Be ready for lender to request bank statements from donor

Special Buyer Situations

Some buyers don't fit the standard pre-approval mold. Here's how to handle common variations:

Cash Buyers: Even without financing, proof of funds is needed. This strengthens offers and proves you can close. Bank statements, investment account screenshots, or proof of liquid assets all work.

Foreign Nationals: More stringent documentation requirements. May need employment visa verification, proof of funds from overseas accounts, and possibly ITIN (Individual Taxpayer Identification Number) instead of SSN.

Investment Property Buyers: Treated differently than owner-occupied. Usually requires 20-25% down, sometimes higher. Debt-to-income calculations might include existing investment property mortgages.

Bridge Loan Scenarios: Buyer is financing purchase before selling current home. Lender considers both mortgages in debt calculations, which sometimes requires bridge loan or proof of equity.

Co-Borrowers and Non-Occupant Co-Signers: Multiple people on the loan increases complexity. All income is counted and all debt is considered. Sometimes a co-signer actually hurts the application if they have poor credit or high debt.

Using Pre-Approval to Strengthen Offers

Pre-approval is more than just qualification, it's a negotiation tool.

When you submit an offer with strong pre-approval, you're signaling to the seller: "This buyer is real. They can close." This matters whether you're working with buyers or helping sellers evaluate offers through your listing appointment strategy.

In competitive markets, consider:

Customizing the Pre-Approval: Ask your lender if they can note specific property types or address ranges on the pre-approval, showing it's customized to this property. Some lenders do this, some don't, but it's worth asking.

Requesting an Expedited Timeline: If pre-approval was just completed, ask the lender if they can process quickly. An appraisal can happen within days if the lender prioritizes it.

Negotiating Appraisal Contingencies: A strong pre-approved buyer can sometimes reduce appraisal contingencies or agree to cover appraisal shortfalls. This makes the offer more attractive to sellers. Understanding the appraisal process management helps you set realistic expectations.

Escalation Clauses: If you expect multiple offers, an escalation clause tied to proof of pre-approval shows the buyer is ready to move if needed.

The pre-approval letter itself, clean, straightforward, recent, is your strongest negotiation card. Use it.

Moving Forward

Mortgage pre-approval isn't just a checkbox on your buyer intake process. It's the foundation of efficient, professional buyer representation. When you understand the process deeply, you can guide buyers confidently, anticipate and solve problems before they derail deals, and build the kind of lender relationships that keep deals moving forward.

Next steps? Connect with your lender partners and learn their specific requirements and timelines. Create a simple checklist of documents buyers need. When a new buyer walks in, hand them that checklist before they even start the pre-approval conversation. This systematic approach should integrate seamlessly with your lead scoring for real estate to identify which prospects are worth prioritizing.

The agents who take pre-approval seriously close more deals, waste less time, and build reputation for having buyers who are ready to actually purchase. That efficiency compounds over a career.

Learn More

Ready to strengthen your buyer qualification system? These related resources will help you build a comprehensive approach:

- Buyer Qualification Framework - Develop comprehensive buyer profiles beyond financial qualification

- Initial Buyer Consultation - Master the first conversation that sets expectations

- Contract to Closing Pipeline - Navigate the post-approval transaction process

- Offer Preparation & Negotiation - Use pre-approval strategically in competitive situations

- Transaction Coordination Process - Keep deals on track from approval through closing

Senior Operations & Growth Strategist

On this page

- Pre-Qualification vs Pre-Approval: Know the Difference

- The Pre-Approval Process Explained

- Initial Financial Conversation

- Documentation Review

- Credit Check and Report Review

- Income and Employment Verification

- Asset and Down Payment Verification

- Debt-to-Income Calculation

- Understanding Loan Types and Programs

- Conventional Loans

- FHA Loans

- VA Loans

- USDA Loans

- Jumbo Loans

- First-Time Buyer Programs

- What's Actually in a Pre-Approval Letter

- Your Role as the Agent

- Set Expectations Early

- Build Lender Relationships

- Follow Up on Status

- Understand Buying Power

- Identify Financial Red Flags

- Working Effectively with Lenders

- Communication Protocols

- Introduce Your Buyer the Right Way

- Manage Timeline Expectations

- Problem Solving

- Common Qualification Issues and Solutions

- Insufficient Down Payment

- High Debt-to-Income Ratio

- Credit Score Problems

- Employment Gaps or Changes

- Self-Employment Documentation

- Gift Funds

- Special Buyer Situations

- Using Pre-Approval to Strengthen Offers

- Moving Forward

- Learn More