Title & Escrow Coordination: Mastering the Transaction Management Backbone

A sobering stat: 23% of closing delays happen because someone dropped the ball on title or escrow coordination. Not because of big problems. Just coordination gaps.

A sobering stat: 23% of closing delays happen because someone dropped the ball on title or escrow coordination. Not because of big problems. Just coordination gaps.

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

A title company didn't get documents. An escrow officer waited on information nobody told them they needed. An HOA packet sat in someone's inbox for three days. These aren't exotic issues. They're predictable, preventable coordination failures that derail the contract to closing pipeline.

And here's the thing: buyers and sellers don't care whose fault it is. When closing gets pushed back two weeks because of a title snag nobody caught early, you're the one who looks disorganized. You're the agent they remember as "that person who couldn't keep things on track."

The agents who close deals smoothly? They're not lucky. They have systems built into their transaction coordination process. They know how to work with title and escrow teams. They catch problems before they become emergencies.

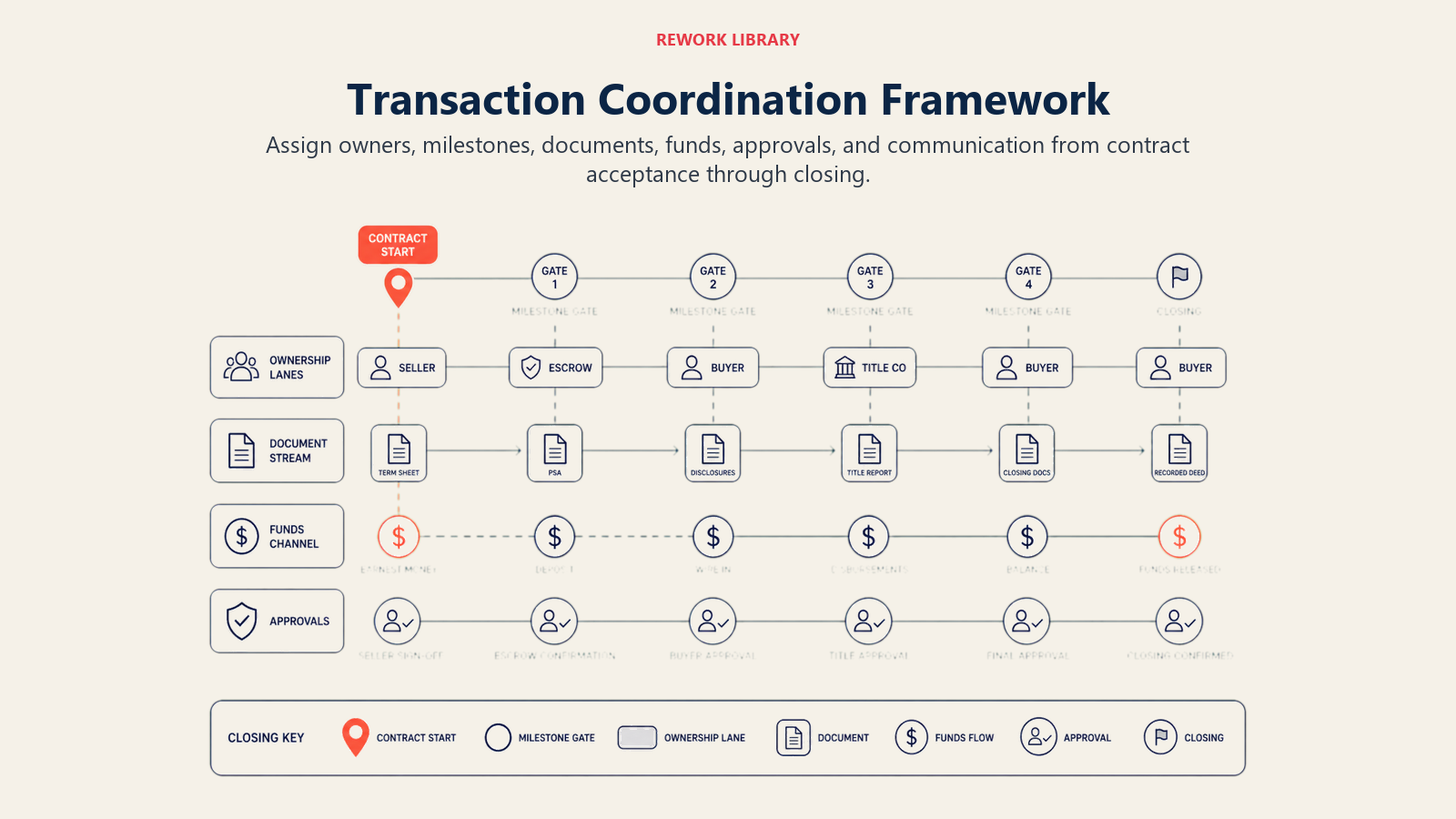

The Transaction Coordination Framework

Good title and escrow coordination starts before you even open a file. You need relationships, processes, and communication systems that run without you having to think about every step.

Title Company Selection Criteria

Not all title companies are created equal. Some are fast. Some are thorough. Some are terrible at both. What matters when choosing who you'll work with: Response time and availability. You need people who answer calls and emails quickly. If your title officer takes 48 hours to respond during a transaction, you're already behind. Error rates. How often do they catch issues early versus letting them surface the day before closing? Ask for examples of how they've prevented problems. Technology capabilities. Can they accept digital signatures? Do they have online document portals? Can they wire funds electronically? If everything requires printing, signing, and scanning, your transactions will drag.

Proactive communication. The best title companies update you without being asked. They flag potential issues the moment they see them. They don't wait for you to check in.

Most agents pick a title company once and never revisit the decision. That's a mistake. Review your partners annually. If delays keep happening with the same company, switch.

Escrow Officer Relationship Building

Your escrow officer can make or break a transaction. Building a real relationship pays off.

Meet them in person. Have coffee. Understand how they work. Ask what makes their job easier. Learn their preferred communication method, some like email, others prefer text, a few still use phone calls.

When you open files consistently with the same officers, they learn your style. They know what you'll need before you ask. They anticipate problems based on past transactions.

This isn't schmoozing. It's operational efficiency. When your escrow officer knows you're organized and reliable, they'll go to bat for you when things get complicated.

Initial File Opening Protocol

The first 24 hours after acceptance determine how smoothly everything else goes.

As soon as you have a signed contract:

Send the fully executed purchase agreement immediately. Don't wait until Monday. Don't wait until you're back at the office. Email it to title and escrow within an hour of acceptance.

Include all contact information. Buyer's agent, seller's agent, lender, inspector, everyone involved. Make it easy for the escrow officer to reach people without hunting down phone numbers.

Flag any unusual contract terms. Seller rent-backs, personal property inclusions, repair credits, anything non-standard needs to be highlighted in your transmittal email.

Request preliminary title report within 48 hours. Don't just assume it'll happen. Explicitly request it and set the timeline expectation.

Confirm earnest money deposit timeline. Make sure everyone knows when funds are due and where they're being sent.

Most coordination problems trace back to a messy file opening. Get this right and everything downstream gets easier.

Communication Cadence Establishment

Set expectations for how often everyone communicates.

Weekly status calls or emails work for most transactions. Pick a consistent day, like every Tuesday at 10am, and stick to it. On that call, review:

- What's been completed since last update

- What's pending and who's responsible

- Any potential issues on the horizon

- Next steps and deadlines

For more complex transactions, increase frequency to twice weekly. For standard deals in the final week, go to daily check-ins.

The key is consistency. Everyone involved should know when they'll hear from you. No surprises, no wondering if something's been forgotten.

Integrate these communication practices into your broader real estate sales cycle to ensure consistency across all client touchpoints.

Pre-Contract Title Preparation

The best agents start the title process before closing, sometimes before they even have an accepted offer.

Preliminary Title Review Timing

Request a preliminary title report as soon as you have a listing or a buyer under contract. But for complex properties, estates, properties owned by trusts, homes with multiple liens, get title work started earlier. When you list a property, order a preliminary report within the first week. Why? Because if there's a title issue, you want to know before you bring a buyer to the table. This proactive approach should be integrated into your listing marketing plan from day one. Clouds on title, unreleased liens, boundary disputes, these take time to resolve. Discover them after acceptance and you're racing against contingency deadlines. Discover them before listing and you can fix them calmly.

Common Title Issues Identification

Most title problems fall into predictable categories:

Unreleased liens. The seller refinanced three years ago but the old lender never recorded a release. Or they paid off a second mortgage and assumed it was handled. It wasn't.

Divorce decree complications. The property was awarded to one spouse, but both names are on title. Or the decree says it's settled but documents were never recorded.

Estate and trust issues. A parent died, the trust says the property goes to the kids, but title was never transferred. Now you need probate or trust certification.

HOA liens. Unpaid assessments sitting there for months or years. These have to be paid before closing, usually from seller proceeds.

Easement problems. An easement that gives the neighbor access through the property. Or an unrecorded easement that the neighbor claims exists. These can derail financing.

Property line disputes. Survey shows the fence is three feet over the boundary. Or the driveway encroaches on the neighbor's lot.

Most of these are solvable. But they take time. The earlier you identify them, the more options you have.

Proactive Title Clearing Strategies

When you find a problem, don't just alert everyone and hope it gets fixed. Take ownership of the solution.

Get payoff statements immediately. If there's a lien, contact the lienholder and request a payoff quote. Find out exactly what's needed to release it.

Connect sellers with resources. If they need an attorney to draft a deed or prepare an affidavit, give them names. Don't make them figure it out.

Follow up daily. Title issues don't resolve themselves. Check in every single day until the problem is cleared.

Have backup plans. If one approach isn't working, identify alternatives. Sometimes paying a disputed amount into escrow and settling post-close is the only way to keep the deal alive.

Title Exception Negotiation

Some title issues can't be cleared. They become exceptions, things the buyer has to accept or negotiate.

Standard exceptions are normal: property taxes, HOA rules, recorded easements everyone knows about. These rarely cause problems.

Non-standard exceptions require negotiation. If there's an easement the seller didn't disclose, should they credit the buyer? If there's a lien that will take months to clear, can it be paid from escrow?

Work with the buyer's lender to understand which exceptions kill financing and which are acceptable with proper documentation. This coordination becomes especially critical when working with the mortgage pre-approval process early in the transaction. Know the difference before you promise solutions.

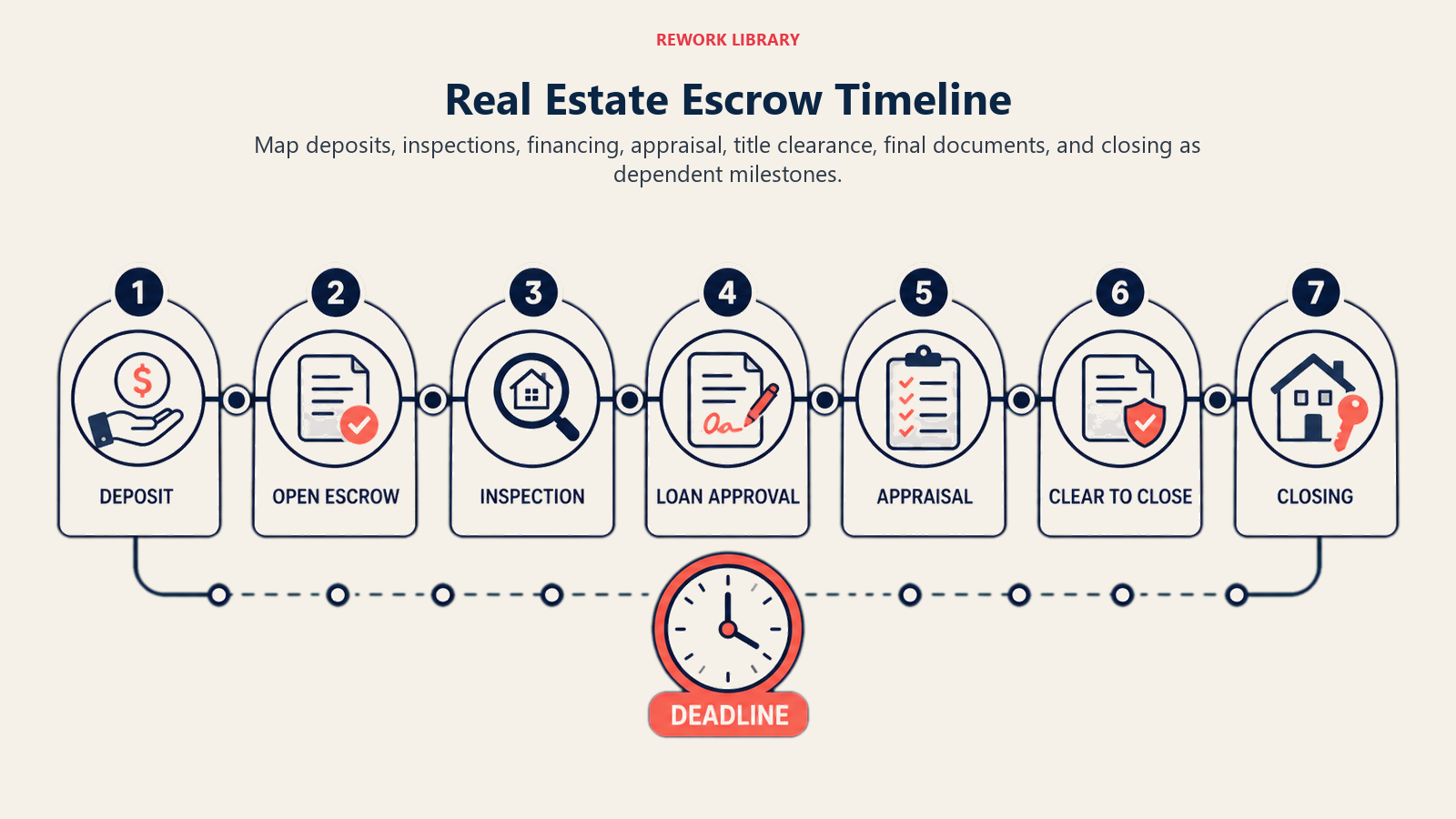

Escrow Timeline Management

Escrow isn't passive. It requires active management of deadlines and milestones.

Critical Milestone Tracking

Every transaction has key dates:

- Earnest money deposit deadline

- Inspection period end

- Appraisal deadline

- Financing contingency removal

- Final walkthrough date

- Closing date

Miss one and you risk the deal falling apart. Create a timeline document on day one. Share it with everyone. Update it when dates change.

Use a system, a transaction management platform, a spreadsheet, even a calendar with alerts. Don't rely on memory. These milestones should align with your real estate sales cycle tracking to ensure nothing falls through the cracks.

Contingency Deadline Monitoring

Most deals fall apart during contingency periods. Not because the buyer wants out, but because deadlines pass and create technical contract problems.

Know exactly when each contingency expires. Three days before, confirm with all parties that everything's on track. If something's delayed, negotiate an extension before the deadline passes. Understanding inspection and contingency management is crucial here.

Never let a deadline slip silently. If the inspection period ends Tuesday and the buyer hasn't removed contingency, you need written extension or formal notice, depending on which side you represent.

Earnest Money Deposit Coordination

Earnest money should hit escrow within days of acceptance. If it doesn't, you have a problem.

Confirm with the buyer: How are they sending funds? Wire, cashier's check, personal check? Each method has different timelines.

If using wire transfer, verify banking details directly with the escrow company. Call them. Don't rely solely on emailed instructions, wire fraud is real and common.

Track the deposit until escrow confirms receipt. Don't assume it happened. Verify.

Document Flow Management

Transactions generate mountains of paperwork: disclosures, inspections reports, repair agreements, loan documents, final settlement statements.

Organize everything in a central location. If you're using a transaction management system, upload everything. If not, use a shared folder with clear naming conventions.

Keep the escrow officer in the loop. Any amendment, addendum, or material document should go to escrow immediately. They can't prepare accurate closing statements without complete information.

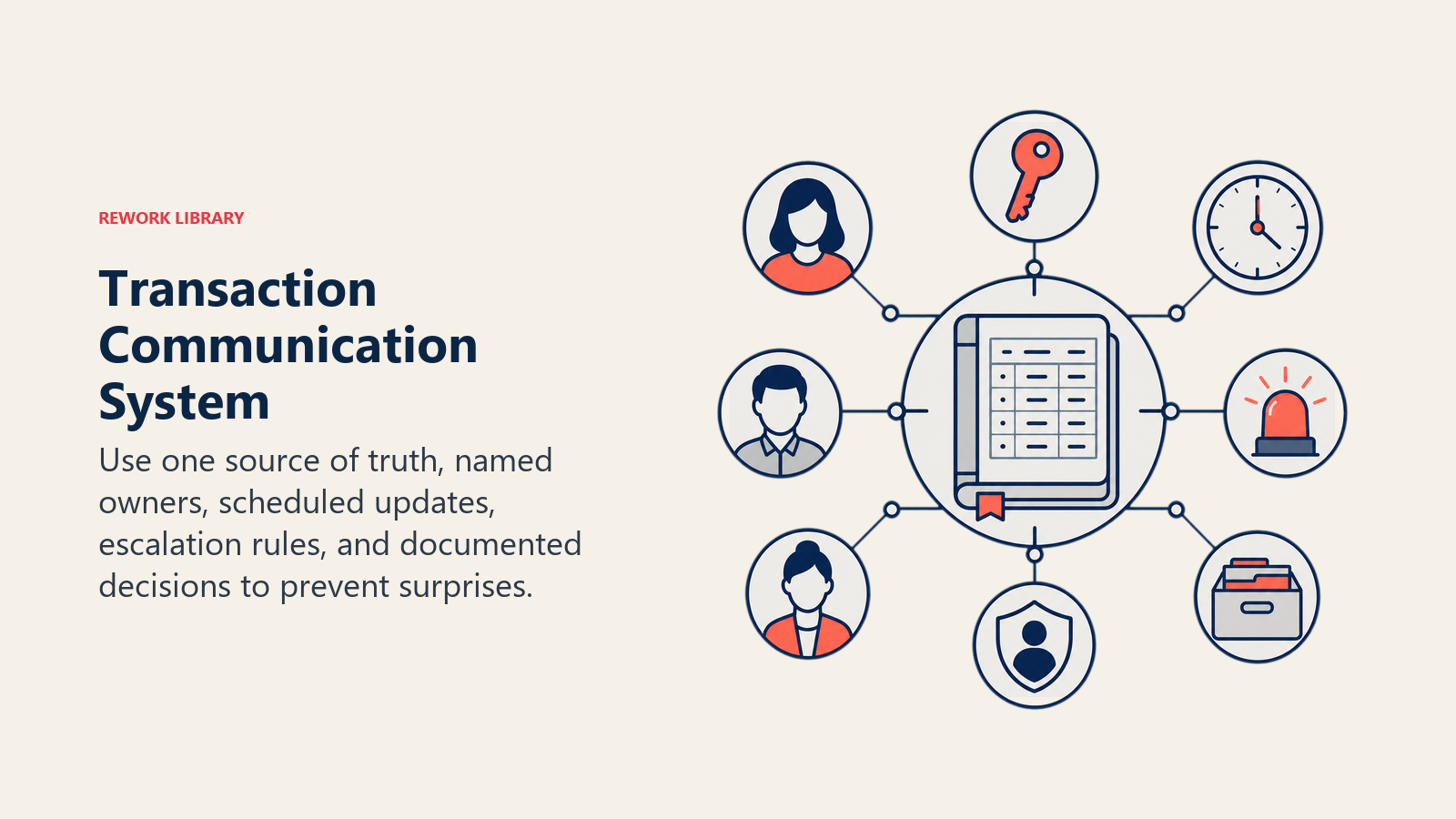

Communication Systems

Coordination happens through communication. Random check-ins aren't enough. You need structure.

Weekly Transaction Update Protocols

Every Monday (or pick your day), send a status update to all parties. Include:

- What's been completed

- What's pending and due dates

- Any issues or concerns

- Next steps

This takes five minutes. It prevents the "I haven't heard from my agent in two weeks" problem. It keeps everyone aligned.

Client Communication Templates

Create templates for common updates:

- "Offer accepted, here's what happens next"

- "Inspection completed, review scheduled"

- "Appraisal ordered, expect results by [date]"

- "One week until closing, here's your checklist"

Templates ensure consistency and save time. You're not reinventing communication for every transaction. Build these templates into your drip campaign strategy for automated yet personalized client updates.

Lender Coordination Checkpoints

The lender is the most critical relationship during escrow. If they don't fund, nothing else matters.

Check in with the lender weekly. Ask:

- Is underwriting complete?

- Any conditions outstanding?

- Is clear-to-close issued?

- When will docs be sent to escrow?

Don't wait for problems. Proactively monitor loan progress. Many delays happen because agents assume everything's fine until it isn't.

Agent-to-Agent Alignment Calls

If you represent the buyer, talk to the listing agent regularly. If you represent the seller, stay in touch with the buyer's agent.

Most agent-to-agent conflict comes from misalignment and surprise. A quick call every few days prevents most problems.

"Hey, just checking in. Everything on track from your side?" That's often all it takes.

Build these practices into your deal fallout prevention strategy to catch problems before they kill deals.

Common Transaction Pitfalls

Even with good systems, certain problems show up repeatedly.

Cloud on Title Discovery (Late Stage)

You're a week from closing. Title comes back with an issue nobody saw before. Now what?

First, find out why it wasn't caught earlier. If it's a title company error, they need to solve it fast. If it's new information, assess whether it can be resolved in time.

Options: pay off the issue from escrow, extend closing, negotiate repairs, or in worst cases, cancel the deal. None are great, but late is better than never.

HOA Document Delays

HOAs are notoriously slow. You request documents and hear nothing for weeks.

Order HOA documents immediately after acceptance. Don't wait. Many HOAs take 10-15 days minimum. Include this as a critical step in your seller qualification framework to set proper expectations upfront.

If they're slow, escalate. Call the management company. Email the board. Pay rush fees if available. The cost of a rush fee is nothing compared to a delayed closing.

Survey Discrepancies

The survey shows something unexpected. A fence line is wrong. A structure encroaches. The lot size doesn't match records.

Get the survey done early if required. Many lenders require it, and waiting until the last minute creates problems.

If there's a discrepancy, determine if it affects financing. Some issues are dealbreakers. Others can be addressed with affidavits or indemnity agreements.

Wire Fraud Prevention Protocols

Wire fraud is common and devastating. Scammers impersonate escrow officers and send fake wiring instructions.

Verify all wiring instructions over the phone. Call the escrow company using a number you looked up independently, not one from an email.

Warn your clients. Tell them: "You will receive wiring instructions by email. Before you send money, call me and call the escrow company to verify everything. Never trust email alone."

This is one conversation that can save someone hundreds of thousands of dollars.

Technology and Tools

Manual coordination doesn't scale. Use technology to automate what you can.

Transaction Management Platforms

Platforms like Dotloop, SkySlope, or TransactionDesk organize everything in one place: documents, timelines, tasks, communication. When evaluating options, review your real estate CRM selection to ensure your tools work together seamlessly.

These aren't optional anymore. If you're managing transactions with email and folders, you're creating unnecessary risk.

Choose a platform, learn it, use it consistently. The time investment pays for itself within a few transactions.

Digital Signature Workflows

Wet signatures are slow. Digital signatures through DocuSign or similar platforms speed everything up.

Set up templates for common documents. Train your clients how to sign electronically. Make sure title and escrow accept digital signatures.

Document Tracking Systems

Know where every document is at all times. Has the buyer signed the disclosure? Did the seller submit the repair agreement? Is the lender's approval letter in the file?

Use checklists and tracking systems. Manual memory doesn't work when you have multiple transactions running simultaneously.

Automated Reminder Systems

Set reminders for every deadline. Not the day of, three days before. That gives you time to follow up if something's missing.

Calendar alerts, task management apps, CRM reminders, whatever you use, make sure nothing falls through the cracks.

Choose systems that integrate seamlessly to avoid manual data entry and reduce coordination errors.

Quality Assurance Checklist

Before closing, run through a final quality check.

Pre-Closing File Review

Three days before closing, review the entire file:

- All contingencies removed

- All inspections complete

- Repairs finished (or credits agreed)

- Lender clear-to-close issued

- Title cleared (or exceptions accepted)

- HOA documents delivered

- Insurance binder received

If anything's missing, resolve it immediately.

Settlement Statement Verification

Review the HUD-1 or closing disclosure carefully. Check:

- Purchase price correct

- Earnest money credited

- Commission accurate

- Prorations calculated correctly

- Agreed-upon credits included

- Loan amounts match expectations

Errors happen. Catch them before closing, not after.

Final Walkthrough Coordination

Schedule the final walkthrough 24-48 hours before closing. Confirm:

- Property is in agreed-upon condition

- Repairs were completed satisfactorily

- Seller has vacated (unless rent-back agreed)

- No new damage occurred

If issues arise, address them before closing. Don't close with unresolved problems hoping they'll get fixed later. They won't.

Post-Closing File Documentation

After closing, organize the file. Save:

- Fully executed purchase agreement

- All disclosures and amendments

- Inspection reports

- Title policy

- Final settlement statement

- Closing documents

You'll need these for future reference, tax purposes, and potential disputes. Don't let files become disorganized messes.

Putting It All Together

Title and escrow coordination isn't glamorous. It's not what attracts people to real estate. But it's what separates professionals from amateurs.

The agents who close deals smoothly, on time, without drama? They have systems. They communicate proactively. They catch problems early. They don't wait for others to manage the transaction.

Build relationships with reliable title and escrow partners. Open files immediately and completely. Track every deadline. Communicate constantly. Use technology to reduce manual coordination. Master these fundamentals and you'll outperform agents who rely on luck and hope.

Do this consistently and you'll become the agent everyone wants to work with. Buyers and sellers will trust you. Other agents will know you're professional. Title and escrow teams will prioritize your deals. This operational excellence creates the foundation for long-term success in your real estate growth model.

Most agents react. Great agents coordinate. Be a coordinator.

Learn More

Build a comprehensive transaction management approach:

- Transaction Coordination Process - Master framework for managing deals from contract to close

- Closing Day Preparation - Final 48 hours checklist and systems

- Deal Fallout Prevention - Protecting deals from contract to close

- Inspection & Contingency Management - Navigate contingency periods successfully

- Appraisal Process Management - Coordinate appraisals and handle value challenges

- Contract to Closing Pipeline - Complete post-contract transaction workflow

Senior Operations & Growth Strategist

On this page

- The Transaction Coordination Framework

- Title Company Selection Criteria

- Escrow Officer Relationship Building

- Initial File Opening Protocol

- Communication Cadence Establishment

- Pre-Contract Title Preparation

- Preliminary Title Review Timing

- Common Title Issues Identification

- Proactive Title Clearing Strategies

- Title Exception Negotiation

- Escrow Timeline Management

- Critical Milestone Tracking

- Contingency Deadline Monitoring

- Earnest Money Deposit Coordination

- Document Flow Management

- Communication Systems

- Weekly Transaction Update Protocols

- Client Communication Templates

- Lender Coordination Checkpoints

- Agent-to-Agent Alignment Calls

- Common Transaction Pitfalls

- Cloud on Title Discovery (Late Stage)

- HOA Document Delays

- Survey Discrepancies

- Wire Fraud Prevention Protocols

- Technology and Tools

- Transaction Management Platforms

- Digital Signature Workflows

- Document Tracking Systems

- Automated Reminder Systems

- Quality Assurance Checklist

- Pre-Closing File Review

- Settlement Statement Verification

- Final Walkthrough Coordination

- Post-Closing File Documentation

- Putting It All Together

- Learn More