Deal Fallout Prevention: Protecting Your Commission from Contract to Close

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

You've worked months on this deal. The contract is signed, contingencies are in motion, and you're mentally spending your commission. Then, three weeks before closing, you get the call. The buyer's having second thoughts. The inspection report is scarier than anyone expected. The appraisal came in low.

This is where deals die.

The reality is sobering: between 12-15% of real estate contracts never make it to closing. For a typical agent doing $4-5 million in annual volume, that translates to roughly $18,000 lost per failed deal. It's not just lost income. It's wasted time, emotional energy, and credibility damage.

But most deal fallouts aren't sudden surprises. They're predictable. And they're preventable with the right transaction coordination process.

The difference between agents who protect their deals and those who don't comes down to one thing: a systematic early warning system combined with targeted intervention at critical pressure points. This guide walks you through exactly how to implement that.

Understanding Your Fallout Risk Profile

Before you can prevent a deal from falling apart, you need to know which deals are most vulnerable.

Start by building a risk assessment framework that you apply to every transaction. This isn't about paranoia. It's about resource allocation. Some deals need intense monitoring from day one. Others cruise through with minimal intervention.

High-risk indicators include:

- First-time homebuyers with limited down payments

- Buyers stretching to afford the property

- Non-local buyers you've never worked with before

- Transactions in shifting market conditions

- Sellers with multiple property exits

- Back-to-back closings where one depends on the other

A thorough buyer qualification framework helps you identify these risks before they become problems.

Financial red flags look like:

- Pre-qualification (not pre-approval) with loose lending criteria

- Recent job changes or employment gaps

- Self-employed buyers without verified income history

- Significant debt-to-income ratios

- Gift funds with unclear source documentation

Seller motivations matter too. Sellers who are desperate tend to inflate property condition, miss disclosure deadlines, or create friction. On the flip side, sellers with multiple contingent offers may drag their feet on critical items.

The key is scoring these factors early (ideally at contract signature) so you know which deals need your constant attention.

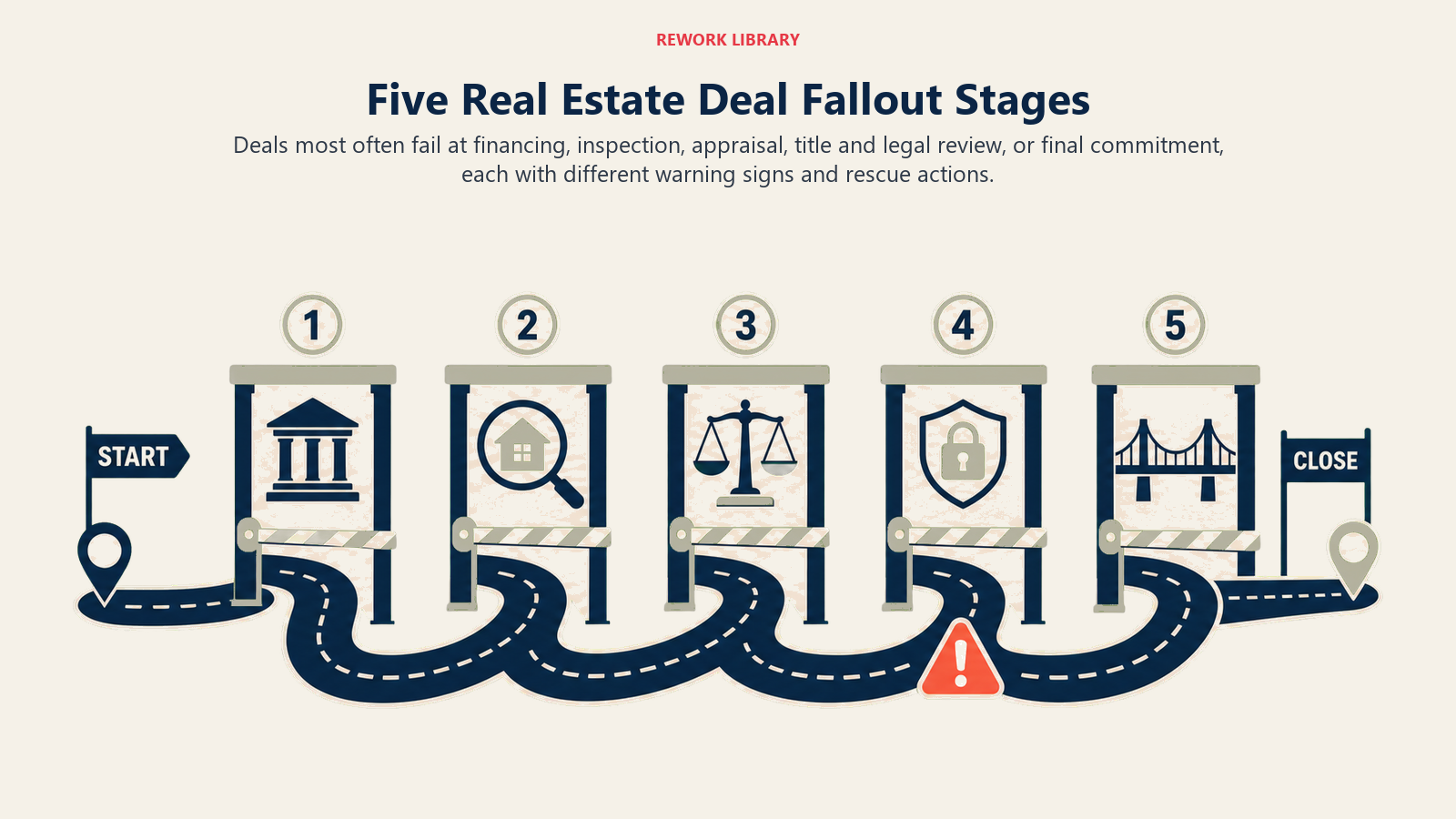

The Five Fallout Stages: Where Deals Actually Die

Fallouts cluster around specific moments in the transaction timeline. Understanding where your risk lives helps you focus your energy.

Inspection Period (35% of fallouts)

The inspection period is ground zero for deal fallouts. Buyers see issues they didn't anticipate, sellers feel accused, contractors provide shocking repair estimates. Emotions run high and logic runs low.

Effective inspection and contingency management is your first line of defense against inspection-related fallouts.

Your job starts before the inspector even shows up. Walk the property with the buyer beforehand and point out what you already know about. "This roof is original to 1998. We'll likely see that noted, and here's what comparable repairs cost in this market." You're managing expectations, not creating surprises.

When it comes to inspector selection, you can't tell a buyer who to hire. But you can share recommendations. An inspector who's been in your market for years tends to give more realistic assessments than someone who applies national standards to local conditions.

During the inspection, show up. Your presence does three things: it keeps the inspector focused on actual problems rather than cosmetic issues, it lets you hear concerns in real-time rather than through a written report that spirals into drama, and it signals to the buyer that you're invested in moving forward together.

The repair conversation is where most deals derail. Create a framework: What's structural? What's cosmetic? What's a building code violation versus a maintenance issue? This separates real problems from negotiation theater.

Appraisal Gap (25% of fallouts)

You priced the property competitively. The buyer got approved. The appraisal comes in $25,000 below contract price.

Now what?

This happens in 10-15% of transactions, and it's almost entirely preventable. The solution starts before you ever list the property. Use recent comparable sales data, not hopeful thinking, to validate the listing price. If comps support $485,000 and you price it at $510,000, you're creating appraisal risk.

Understanding appraisal process management and applying sound pricing strategy and negotiation principles from the start prevents most appraisal gaps.

When you do have a gap, most agents immediately look for problem-solving, which usually means pressuring the seller to accept a lower price. But you have other options. Can the buyer contribute more down payment? Can you negotiate a credit back to closing costs? Can the seller's agent pull additional comps that justify higher value?

The reality: if the appraisal is low, the market probably says the price was optimistic. Accept that faster than your seller wants to, and you'll preserve deals that others lose.

Financing Fallout (20% of fallouts)

A buyer's pre-approval is a starting point, not a guarantee. Mid-transaction financial changes sink deals.

Following a structured mortgage pre-approval process from the beginning sets proper expectations. Your lender protocols should include touchpoints at specific moments: after inspection (when buyers sometimes panic-spend), two weeks before closing (when last-minute changes happen), and immediately before final walkthrough. A simple text like "Just confirming everything's still solid on your financing?" catches problems early.

Watch for employment verification timing. Some lenders verify employment three times: at pre-approval, before appraisal, and before final walkthrough. A buyer who changes jobs in week four of a six-week closing might be fine. A buyer who changes jobs in week five might lose their loan.

Advise buyers against large purchases during the closing period. A new car means a hard credit inquiry and a payment that changes debt ratios. A furniture purchase on credit opens new accounts. These aren't huge deals in isolation, but they can tip a buyer with marginal credit from approval to denial.

Final Walkthrough (10% of fallouts)

Your buyer's final walkthrough is supposed to be a formality. The property condition shouldn't have changed since inspection. But sometimes it has. Sellers remove items, deferred maintenance gets worse, or the property just feels different when it's about to change hands.

Most final walkthrough disasters are about emotion, not substance. A buyer gets cold feet and invents problems. Your job is separating real issues from buyer's remorse, then fixing the real ones before closing. Proper closing day preparation minimizes last-minute surprises.

Cold Feet & Buyer's Remorse (10% of fallouts)

Sometimes the deal dies because a buyer simply changed their mind. They're not having inspection issues or appraisal problems. They're having existential doubts.

This is where psychology meets transaction management. You prevent this through consistent reinforcement of why they made this decision. Check in after major milestones. Send emails with photos of their soon-to-be home. Introduce them to neighbors on social media. The goal isn't to manipulate. It's to keep the emotional reality of ownership present.

When doubt appears anyway, don't panic-pitch. Listen. Often the doubt isn't about the house; it's about the enormity of the decision. Remind them that these feelings are normal, that most buyers experience them, and that they've already done the due diligence that proves this is a sound decision.

Building Your Early Warning System

The best time to intervene is before the problem becomes a crisis. You need a communication monitoring protocol.

Buyers and sellers should hear from you on a regular schedule: week one after contract, week two, before appraisal, after appraisal, after inspection, one week before closing, three days before closing. That's eight touchpoints minimum. Some are transactional ("here's your appraisal report"). Others are relationship-focused ("wanted to check in and see how you're feeling about everything").

A robust contract to closing pipeline ensures these touchpoints happen consistently across all your transactions.

The real insight comes from monitoring changes in communication patterns. A buyer who's been responsive suddenly ghosts you. A seller who was chatty becomes one-word responder. Tone shifts in emails. These aren't proof of a problem, but they're signals to probe deeper.

When you detect a shift, pick up the phone rather than texting. A five-minute conversation catches problems that three rounds of texts miss.

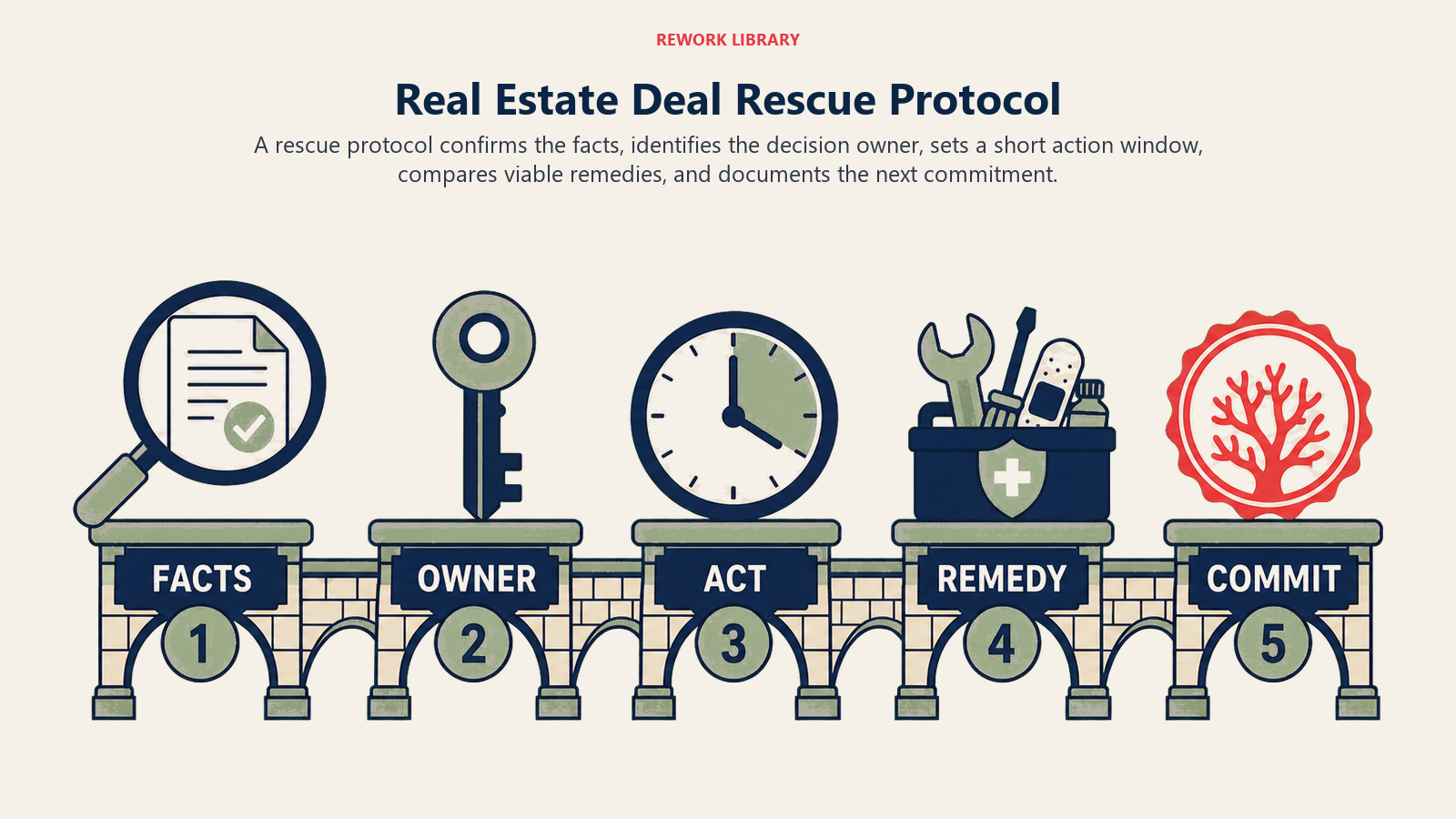

Your Deal Rescue Protocol

Despite prevention efforts, some deals still need emergency intervention.

When a fallout threat appears, move quickly through these steps:

First: Assess what's actually at stake. Is this a real problem or a negotiation tactic? Is the buyer actually ready to walk or just expressing frustration?

Second: Get all parties talking. Many deals fail because communication breaks down, not because the core issues are unsolvable. A three-way call with buyer, seller, and both agents often reveals solutions that seemed impossible in writing.

Third: Brainstorm alternatives. Can't agree on repairs? Do a credit instead. Appraisal gap? Split it. Financing concern? Get a new lender quote. Most "dead" deals have at least one viable path forward.

Fourth: Know when to let go. Sometimes a deal should fall apart. A buyer who's been coerced into a stretch property isn't going to be happy, and unhappy clients create more problems down the line. A seller who's being forced to sell below market will resent you. Not every deal is worth saving.

Your decision framework: Is this deal good for both parties? Can we solve the actual problem or just delay it? Is my involvement creating value or enabling bad decisions?

If it's not, let it go. Your reputation is built on deals that close with both parties feeling good about the outcome, not on the raw number of closings.

Connecting the Full Transaction Picture

Deal fallout prevention doesn't happen in isolation. It's woven into every aspect of your transaction process.

Your initial buyer consultation at the front end determines which properties actually fit your buyer's financial and emotional reality. Buyers who are in the right property rarely get cold feet.

Your listing appointment strategy sets realistic expectations with sellers about what the market will support, preventing appraisal gaps before they happen.

Your seller qualification framework identifies potential issues before you even take the listing.

Your title and escrow coordination with your closing team surfaces issues weeks before closing rather than days before.

And your closing day preparation ensures that nothing surprising happens at the final moment.

Fallout prevention is really about building a complete transaction system where every step sets up the next one for success.

The Numbers That Matter

Track three metrics:

Fallout rate: What percentage of your contracts actually close? Industry average is 85-88%. You should be targeting 92%+.

Time-to-rescue: How long from first warning sign to intervention? Every day that passes makes solution harder. Catching a problem at day 3 is infinitely easier than day 17.

Resolution success rate: Of deals in danger, what percentage do you save? You won't save them all, and you shouldn't try. But if you're successfully retaining 80%+ of at-risk deals, your system is working.

The Mindset Shift

What separates agents who lose deals from agents who protect them: the first group treats fallout prevention as a reactive emergency protocol. They only activate it when a deal starts falling apart.

The second group treats it as a proactive system. Every transaction gets consistent monitoring. Every risk factor gets assessed. Every communication pattern gets tracked.

When a real threat appears, they're not improvising. They're executing a practiced response.

Fallouts aren't random. They're predictable. And predictable means preventable.

Start with one transaction. Apply the framework. See what surfaces. Then apply it to the next one. Within a quarter, you'll have a system running on autopilot, protecting deals before problems even become visible.

That's when commissions stop falling through the cracks.

Learn More

Strengthen your transaction management system with these related resources:

- Offer Preparation & Negotiation - Set yourself up for success by crafting stronger offers that are less likely to fall apart during due diligence.

- Buyer Retention & Engagement - Keep buyers emotionally invested throughout the transaction process to prevent cold feet and buyer's remorse.

- Real Estate Metrics & KPIs - Track your fallout rate and other critical metrics to identify patterns and improve your prevention systems.

- Transaction Coordinator Role - Learn how bringing on a dedicated transaction coordinator can strengthen your early warning system and intervention protocols.