More in

AI at Work News

OpenAI Opened ChatGPT Advertising to Small Businesses at Any Budget

Jun 6, 2026

AI Is Everywhere at Work. Only 1 in 10 Say It Transformed the Job

Jun 6, 2026

Vibe Coding's $10.5B Moment: AI Now Starts Most New Software Builds

Jun 6, 2026

AI Agents Now Have More System Access Than Your Employees. Few Are Secured

Jun 5, 2026

Should You Build Your AI or Buy It? Watch What the Giants Bought.

Jun 5, 2026

Uber Caps Employee AI Spending at $1,500 Per Seat After a Budget Blowout

Jun 5, 2026

Trump's AI Executive Order Is Deregulatory. Your Compliance Risk Didn't Move

Jun 4, 2026

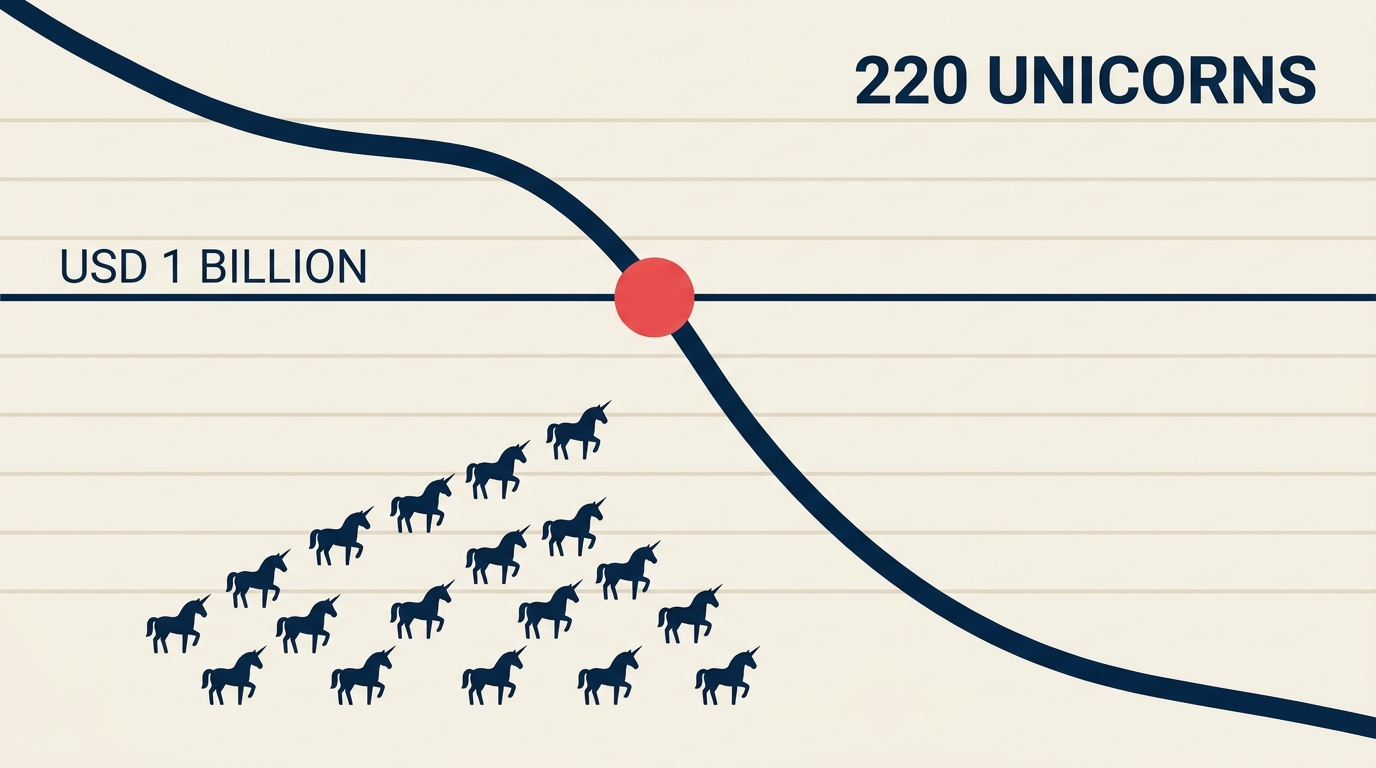

AI Pushed 220 Unicorns Below $1B. Pre-ChatGPT Companies Face a Reckoning

Jun 4, 2026 · Currently reading

Token Prices Fell 67% This Year. Your AI Bill Is Going Up Anyway

Jun 3, 2026

Small Businesses Using AI Report Higher Revenue and Shorter Workdays

Jun 3, 2026

AI Pushed 220 Unicorns Below $1B. Pre-ChatGPT Companies Face a Reckoning

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

They raised at peak multiples, hired aggressively, and built products that looked durable in 2021. Now hundreds of those companies are stuck in a trap with no clean exit.

CNBC reported on June 1 what many founders have been quietly living for the past two years: companies built before ChatGPT changed the game are being squeezed from both sides. More than $250 billion has flowed toward OpenAI and Anthropic ahead of their expected mega-IPOs, pulling the oxygen out of the broader venture market. And AI-native competitors are now building, at a fraction of the cost, what pre-2022 startups spent years and hundreds of millions of dollars constructing.

The result, per PitchBook data cited by CNBC, is that more than 220 companies that once held unicorn status (valued at $1 billion or more) have now fallen below that threshold. The list includes names most CEOs would recognize: Glossier, Savage X Fenty, AG1, The Farmer's Dog. Not obscure bets. Companies with real revenue, real customers, and real teams. The valuation collapse is not about bad products. It's about the re-underwriting of an entire generation of businesses.

The Numbers Behind the Trap

The repricing matters because it shows how quickly pre-AI assumptions can become liabilities when capital markets and product economics shift at the same time.

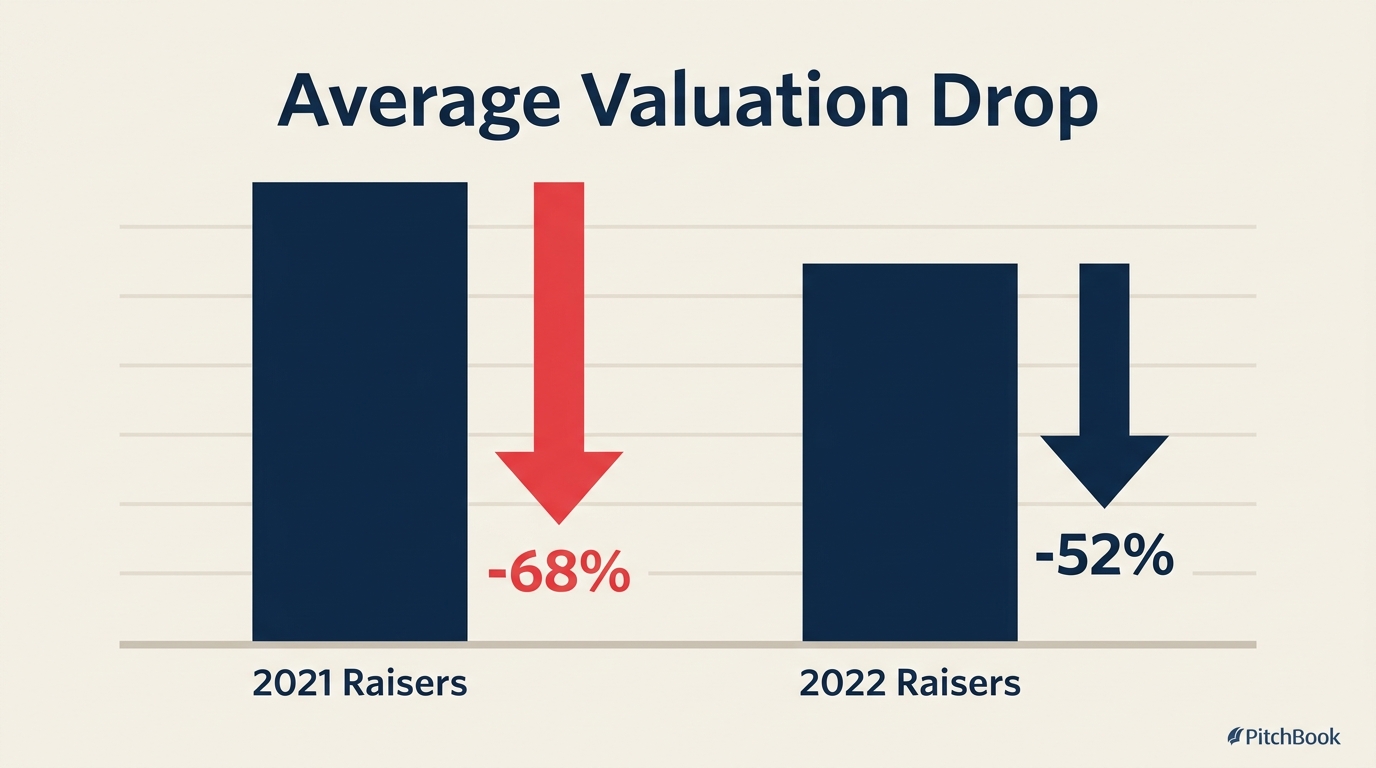

The scale of the repricing is stark when you look at the PitchBook cohort data. Startups whose last round closed in 2021 were worth roughly 68% less, on average, by the end of last year. Those that raised in 2022 were down about 52%. That's not a correction. That's a structural rewrite of what the business was worth once the macro shifted and AI changed the competitive cost structure underneath it.

The financing trap works like this: valuations from 2021 and 2022 are too high to justify a new venture round (a flat or down round signals distress to employees, customers, and future investors), but the companies aren't profitable enough to go public. And the public markets for tech IPOs remain selective, increasingly focused on AI-native businesses with clear unit economics at scale. So these companies are caught between a last-round valuation they can't grow into and an exit path they can't reach.

David Zhu, the former head of engineering at DoorDash, put it plainly in comments reported by CNBC: workflow-driven enterprise software companies will be either "disrupted or dead" within the next decade as AI agents take over the coordination and data-entry work that once required human-staffed platforms.

Key Facts

- 220+ companies that once held unicorn valuations have fallen below the $1B threshold (PitchBook, via CNBC)

- Startups whose last raise was in 2021 were worth about 68% less by end of last year; 2022 raisers were down about 52% (PitchBook)

- More than $250 billion has flowed to OpenAI and Anthropic ahead of their expected IPOs, concentrating capital away from the pre-ChatGPT cohort (CNBC)

Why AI-Native Challengers Have a Structural Cost Advantage

The core issue isn't that pre-ChatGPT companies built bad products. It's that the cost to build those same products just dropped by an order of magnitude.

Samir Kaul, a partner at Khosla Ventures, described what changed after late 2022 in terms CNBC highlighted: you can now have roughly 50 engineers accomplish what would have required 500 five years ago. New founders code in plain English. They ship faster, spend less, and can reach feature parity with legacy platforms without the years of accumulated headcount that make incumbents expensive to run.

A venture investor in the CNBC piece noted that by 2023, their post-ChatGPT portfolio companies were already outearning most of their pre-ChatGPT investments. That's a two-year window in which the competitive landscape shifted enough to reprice an entire cohort of companies.

For CEOs of pre-ChatGPT businesses, the competitive threat isn't abstract. The challenger isn't raising $50 million to outmarket you. They're raising $5 million, shipping an AI-native version of your core workflow in six months, and undercutting your pricing because their cost to serve is a fraction of yours.

This capital concentration story connects directly to the Anthropic IPO and what it signals about where AI investment is heading. And the same AI-native cost advantage is reshaping how enterprise CRM and go-to-market tools compete, as AI-native startups challenge Salesforce incumbents.

The Pre-ChatGPT Re-Underwriting Test

The dividing line for which companies face existential pressure isn't the founding date. It's whether the business's core value sits in a layer an AI agent can now reproduce cheaply. A company founded in 2019 that sells proprietary data, a hard-to-replicate network, or a compliance-intensive service may be fine. A company founded in 2022 that automates a workflow with no defensible data moat may not be.

Here's the test every CEO of a company that raised before 2023 should run:

Question 1. Moat check. Is the core value of our product a workflow, a data-entry layer, or a system-of-record that an AI agent can now perform natively? If yes, the moat is eroding and the erosion speed is faster than the typical three-to-five year competitive window.

Question 2. Valuation trap. Was our last raise in 2021 or 2022 at a multiple we cannot realistically grow into given current growth rates? If yes, the company needs an honest plan: a down round, a recapitalization, or a profitability pivot before the cash runway ends. Pretending the last valuation is still relevant destroys more value than acknowledging it early.

Question 3. Cost-to-serve delta. Can an AI-native competitor reach our customers at a fraction of our cost? Model what unit economics look like if a competitor starts at 50 engineers doing what your 500 are doing. That's not a hypothetical scenario anymore. It's the starting point for new entrants right now. The AI cost economics for enterprise tools are shifting fast enough that this model needs updating quarterly, not annually.

Question 4. Which side of the line. Are we on the disrupting side or the disrupted side? And what one workflow could we rebuild AI-native this quarter before a challenger does it to us?

The last question is the most actionable. Most companies can't rebuild their entire platform in a year. But most companies can pick one core workflow, rebuild it AI-native, and use that as both a defensive moat and a proof of concept for the broader transformation. Where AI investment is flowing in the GTM stack shows where challengers are already targeting incumbents.

Why the Financing Trap Is Worse Than It Looks

The 220-unicorn figure from PitchBook understates the problem. It only counts companies that once crossed $1 billion in valuation. But the same structural pressure applies to any startup that raised at elevated 2020 to 2022 multiples and is now neither growing fast enough to justify another venture round nor profitable enough for an IPO.

The investors are tracking it too. AI decision frameworks for CEOs are increasingly focused on the question of which legacy positions are defensible and which aren't. And the macro labor analysis, including Goldman's research on net job drag from AI, reinforces that the cost-to-serve repricing extends beyond software into every workflow-driven business.

The companies in the worst position are those with four specific characteristics: raised in 2021 or 2022 at peak multiples, core product is a workflow coordination layer, headcount-heavy cost structure, and two years or less of runway left. If that's your situation, the options table looks like this:

A down round or recap, done with enough runway to negotiate from a position of relative strength, preserves more value than waiting. A profitability pivot, where the company cuts to a sustainable cost structure and stops chasing venture-scale growth, can stabilize the business long enough to find a strategic exit or organic path. A sale or merger, while the company still has meaningful revenue and product, often produces better outcomes than a distressed sale after runway runs out. The window for all of these options is smaller than most boards are acknowledging.

What to Do This Quarter

The CNBC reporting describes a problem at the cohort level. But the decision is individual. Here's the short list for a CEO whose company raised before 2023:

Audit the moat against the test. Run the four questions above on your actual core product, not the aspirational roadmap. Be honest about which workflows are defensible and which aren't. This is a board conversation, not a management team exercise.

Reset valuation expectations proactively. The companies that are navigating this best are the ones that had the down-round or recap conversation with their investors six months ago. The ones that waited are having it now with less leverage. If the last round valuation isn't supportable by current metrics, surface that at the next board meeting and frame the options.

Pick one workflow to rebuild AI-native this quarter. Not a full platform rebuild. One workflow, built from scratch with AI as the primary actor, not as a feature layered onto existing architecture. Use it to prove internal capability and create a defensible wedge against challengers who are starting from scratch.

If the financing trap is real, evaluate M&A while you control the timing. A strategic buyer is far more interested in a company with 18 months of runway and a clear AI roadmap than in a distressed asset. The valuation conversation is hard either way, but it's substantially better when you initiate it than when your options are running out.

The pre-ChatGPT reckoning isn't coming. It's already here. The question is whether your company is running the test and acting on it, or waiting for the situation to clarify.

Frequently Asked Questions

What does "pre-ChatGPT startup" mean in this context?

In this context, a pre-ChatGPT startup is a company that raised its primary funding rounds before late 2022, when the release of ChatGPT fundamentally changed the cost structure for building software and the investor appetite for AI-native businesses. These companies built their products and their valuations in a market where AI capabilities were far more limited and expensive to access.

Why are pre-2022 startups losing value?

Two forces are working against them simultaneously. First, the capital that once funded a broad venture market has concentrated around a small number of AI companies, including OpenAI and Anthropic, tightening funding for everyone else. Second, AI-native competitors can now build comparable products with far fewer engineers and much lower operating costs, which undercuts the competitive moat and the pricing power of incumbents. PitchBook's data shows startups whose last raise was in 2021 were worth roughly 68% less by the end of last year.

How can a CEO tell if their company is at risk?

The clearest signal is whether the company's core product is a workflow coordination layer or a data-entry system that AI agents can now replicate. If yes, and if the company raised at 2021 or 2022 valuations it hasn't grown into, the financing trap is real. The four-question re-underwriting test in this article is a structured way to assess exposure: moat check, valuation trap, cost-to-serve delta, and which side of the disruption line the company sits on.

Related Reading

- Anthropic's $96.5B IPO Filing and What It Means for the AI Vendor Calculus

- AI-Native Startups vs. Salesforce: The Agent-First CRM Debate

- Where $200M in AI Sales Funding Is Going and What It Signals for the GTM Stack

- PwC's 74/20 Divide: Which CEOs Are Capturing AI's Economic Gains

- Enterprise AI Bills Are Rising While Token Prices Are Falling

- BCG AI Radar 2026: The CEO as AI Decision-Maker

Co-Founder, Rework.com

On this page

- The Numbers Behind the Trap

- Why AI-Native Challengers Have a Structural Cost Advantage

- The Pre-ChatGPT Re-Underwriting Test

- Why the Financing Trap Is Worse Than It Looks

- What to Do This Quarter

- Frequently Asked Questions

- What does "pre-ChatGPT startup" mean in this context?

- Why are pre-2022 startups losing value?

- How can a CEO tell if their company is at risk?