The CFO Conversation on AI Budget: How to Walk In Prepared

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

The CFO meeting is in 45 minutes. You need approval for $350,000 in AI infrastructure and tooling. You have a slide deck. You're about to discover that the CFO's first question has nothing to do with the technology.

It's "What problem does this solve for the business?"

Not "Which large language model are you using?" Not "What's the API cost?" Not even "What's the return on investment?" Those come later. The first question is about business problem definition, and if you can't answer it in two sentences without jargon, the meeting goes sideways before the second slide. The ACE Framework gives you the vocabulary to answer that first question precisely: name the capability (Ingest, Analyze, Predict, Generate, or Execute) and the business process it addresses, and you'll speak a language that cuts through AI jargon.

This article is an insider briefing, not a framework. It prepares you for a real conversation with a real chief financial officer (CFO) who has seen five AI proposals this quarter and approved zero of them. Here's what they actually ask, what answers satisfy them, and how to structure a budget conversation that ends with approval rather than a request to "come back with more data."

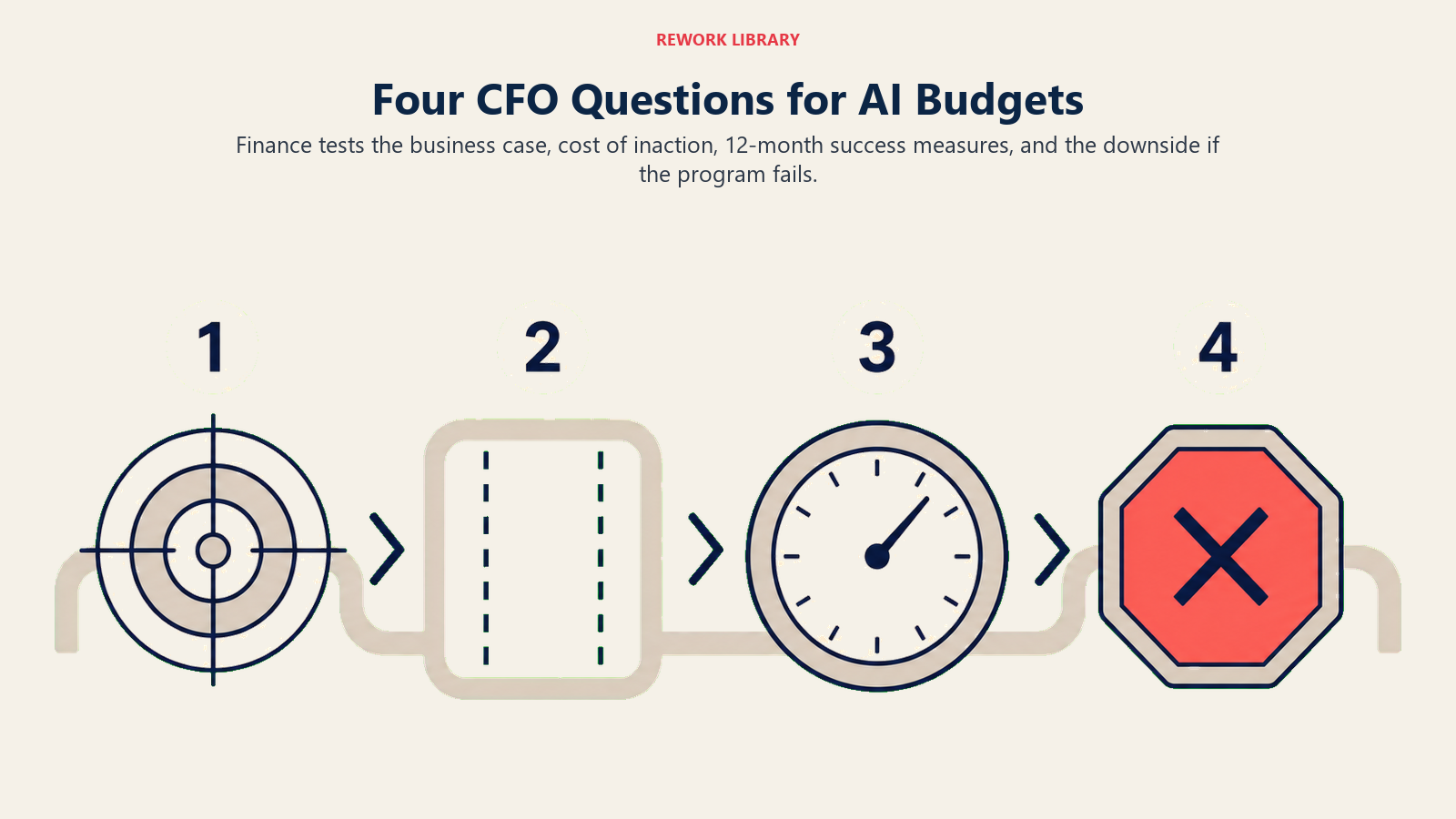

What CFOs actually ask about AI budget

Key Facts: CFO AI Budget Reality

- 83% of CFOs plan AI budget increases above 15% over the next two years, with 42% expecting increases above 30%, yet only 15-25% have scaled AI past the pilot stage. (Bain)

- 87% of CFOs expect AI to be extremely or very important to their finance operations in 2026, while simultaneously reporting that tech budgets allocated to AI have not been matched by clearly demonstrated returns. (Deloitte CFO Signals)

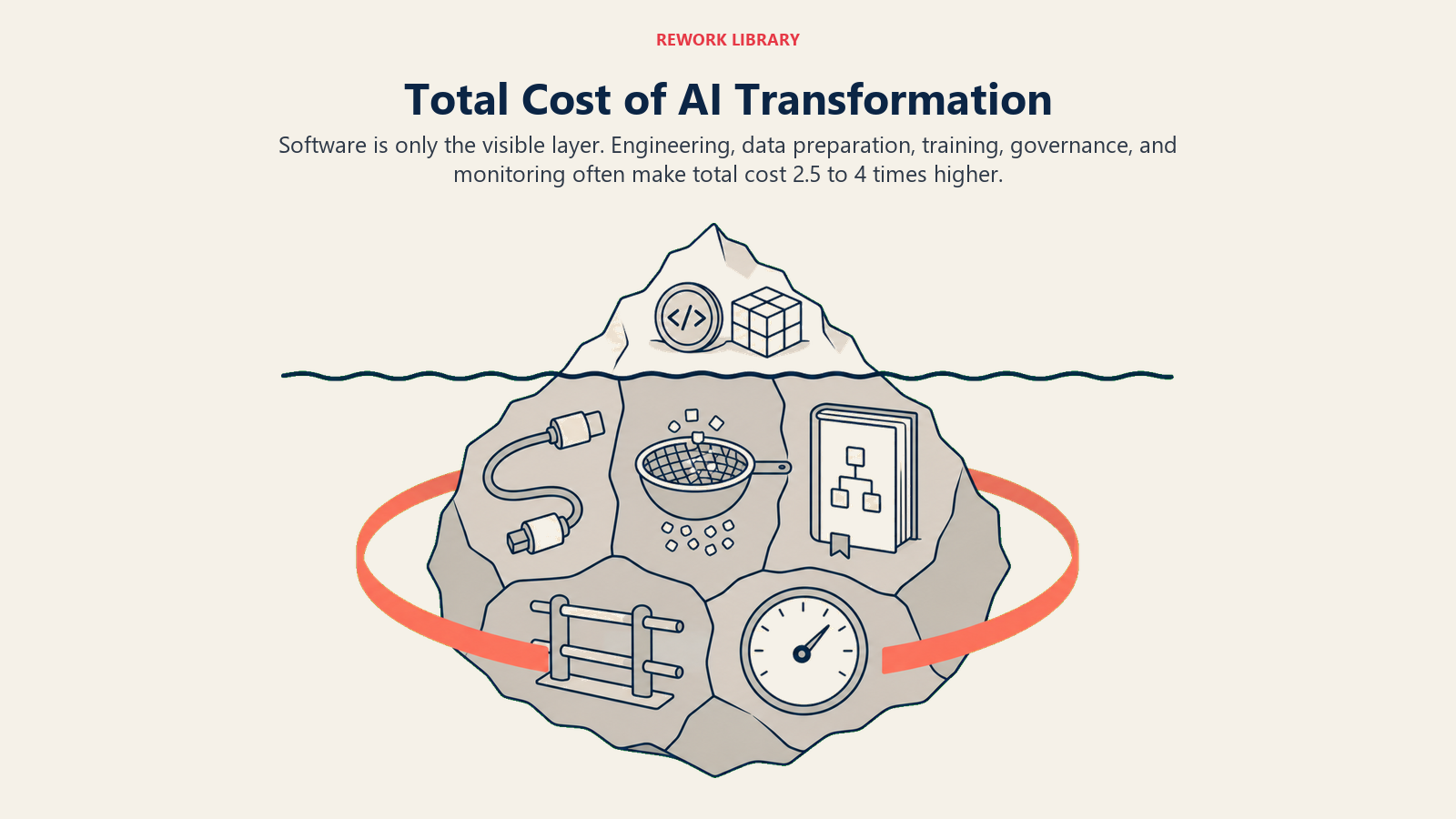

- The realistic total cost of a mid-market AI transformation is 2.5-4x the software licensing cost when internal labor, data preparation, and change management are included. (Deloitte)

Most AI budget presentations fail because they answer questions the CFO didn't ask while avoiding the ones they did. Deloitte's Q4 2025 CFO Signals survey found that 87% of CFOs expect AI to be extremely or very important to their finance operations in 2026, while simultaneously reporting that tech budgets allocated to AI have not been matched by clearly demonstrated returns. The gap between enthusiasm and evidence is exactly where these four questions live.

"What's the business case, not the technology case?"

CFOs have an allergy to technology-forward budget pitches. "We need vector database infrastructure and an embeddings pipeline" is a technology case. "We need to cut our invoice processing cost from $14 per invoice to $1.50 while reducing accounts payable (AP) cycle time by 60%" is a business case. The technology that delivers it matters, but it's not what the CFO is buying.

The answer to this question needs three components: the current state (cost, time, error rate, or constraint), the target state, and the measurement method. "Right now our sales team spends 90 minutes per week on CRM data entry. We project AI automation reduces that to 15 minutes, freeing the equivalent of 1.5 full-time equivalents (FTEs) across the team. We'll measure actual time savings via work log sampling in the first 90 days."

That's a business case. The AI doing the work is a footnote.

"What happens if we don't invest?"

This is the competitive risk question in disguise. CFOs who ask it aren't being hostile. They're doing their job: evaluating the opportunity cost of the budget against what the organization risks by staying where it is.

A weak answer: "We'll fall behind on AI." A strong answer: "Our three largest competitors have each publicly announced AI-driven process investments in the last 18 months. If their cost-to-serve drops 20-30% and ours doesn't, we enter the next pricing negotiation at a structural disadvantage we can't explain away with product differentiation." Then stop talking.

The "what if we don't" answer should be specific about competitive dynamics, not abstract about trends. If you can't name competitors or cite specific actions, do the research before the meeting.

"How do we measure success at 12 months?"

This is the question that exposes vague return on investment (ROI) promises. A CFO who has been burned by previous technology investments asks this to find out whether you have a real measurement plan or a collection of aspirational metrics that will be quietly dropped when results disappoint.

The answer is a short list: three to five metrics, each with a current baseline, a 12-month target, and the measurement method. "Analyst hours on manual data processing: currently 22 hours/week across the team, target 8 hours/week, measured via weekly time-tracking reports. First-draft content output: currently 8 pieces per month, target 18 pieces per month at equivalent quality grade, measured via publication count and editorial review score."

Committing to specific numbers with specific measurement methods signals you've thought beyond the demo. It also creates accountability for the program, which CFOs appreciate even though program owners sometimes fear it.

"What's the risk if it doesn't work?"

This question is about downside protection, not pessimism. CFOs manage risk for a living. They want to know you've modeled the failure scenario, not just the success scenario.

Prepare for this by separating the budget into three buckets: costs you'll recover (software subscriptions you can cancel, contractors you can end), costs you'll partially recover (sunk time on integration work, internal change management), and costs you won't recover (reputational cost of failed rollout, team morale impact). The AI Risk Register: What to Track gives you the risk scoring format that turns these failure scenarios into quantified risk estimates the CFO can evaluate on the same scale as projected ROI. Then name the most likely failure mode. "The most likely failure scenario is insufficient rep adoption of the AI scoring tool. We've designed the rollout to include training and a 90-day review gate. If adoption is below 40% at 90 days, we pause scale-up before committing to the next phase."

That answer shows you've thought about failure, have a leading indicator (adoption rate, not revenue), and have a decision gate. That's what responsible budget management looks like.

Framing AI as capital allocation, not IT expense

Most AI budgets are submitted as operating expenses or IT line items. That framing immediately positions the request as a cost to be minimized rather than an investment to be evaluated. It also makes the CFO compare your AI program against headcount, software renewals, and facilities costs, which is the wrong comparison set.

AI infrastructure investments have more in common with building a factory than buying software licenses. A factory creates productive capacity that compounds over time. Early AI infrastructure (data pipelines, integration work, governance tooling, training data curation) creates capability that future AI projects build on for free. The second AI project is cheaper to deploy than the first because the integration work is already done. The third is cheaper still.

Capital assets have depreciation schedules because the value they create accumulates across years, not months. When you frame AI infrastructure this way, a $350,000 budget conversation becomes a discussion about the useful life of the investment (3-5 years for most infrastructure), the expected return in years 2 and 3 when the marginal cost of new use cases drops sharply, and the option value of capabilities you haven't even identified yet. For the specific total cost of ownership (TCO) math across Buy, Integrate, and Build paths, The Build vs. Buy vs. Integrate Decision shows how the infrastructure investment framing changes the 3-year cost picture significantly.

One framing that consistently resonates: "This isn't a software purchase. It's building the infrastructure that makes every subsequent AI initiative cost half as much to deploy. We're buying capabilities, not features."

The total cost of transformation model

The fastest way to lose a CFO's trust is to come back three months after approval asking for more money to cover costs that should have been in the original budget. Present all the costs upfront, including the ones that are awkward to admit.

Visible costs (typically in the original ask):

- Software licensing and API costs

- Infrastructure (compute, storage, vector databases)

- External implementation or integration support

Hidden costs (typically excluded from the original ask):

- Internal engineering time for integration work (often 2-4x the software cost)

- Data preparation and cleaning (frequently underestimated by 50%)

- Change management and training program design and delivery

- Governance infrastructure (policy writing, audit tooling, incident response design)

- Ongoing model evaluation and monitoring

A realistic total cost of transformation for a mid-market company doing its first serious AI build is typically 2.5-4x the software licensing cost when you include internal labor. Present this honestly. CFOs who discover hidden costs mid-program don't lose trust in AI. They lose trust in the program lead. Deloitte's research on AI and tech investment ROI consistently identifies hidden implementation and change-management costs as the most common reason AI programs miss their promised returns.

The Honest Cost of AI Transformation has the full breakdown with benchmarks by company size.

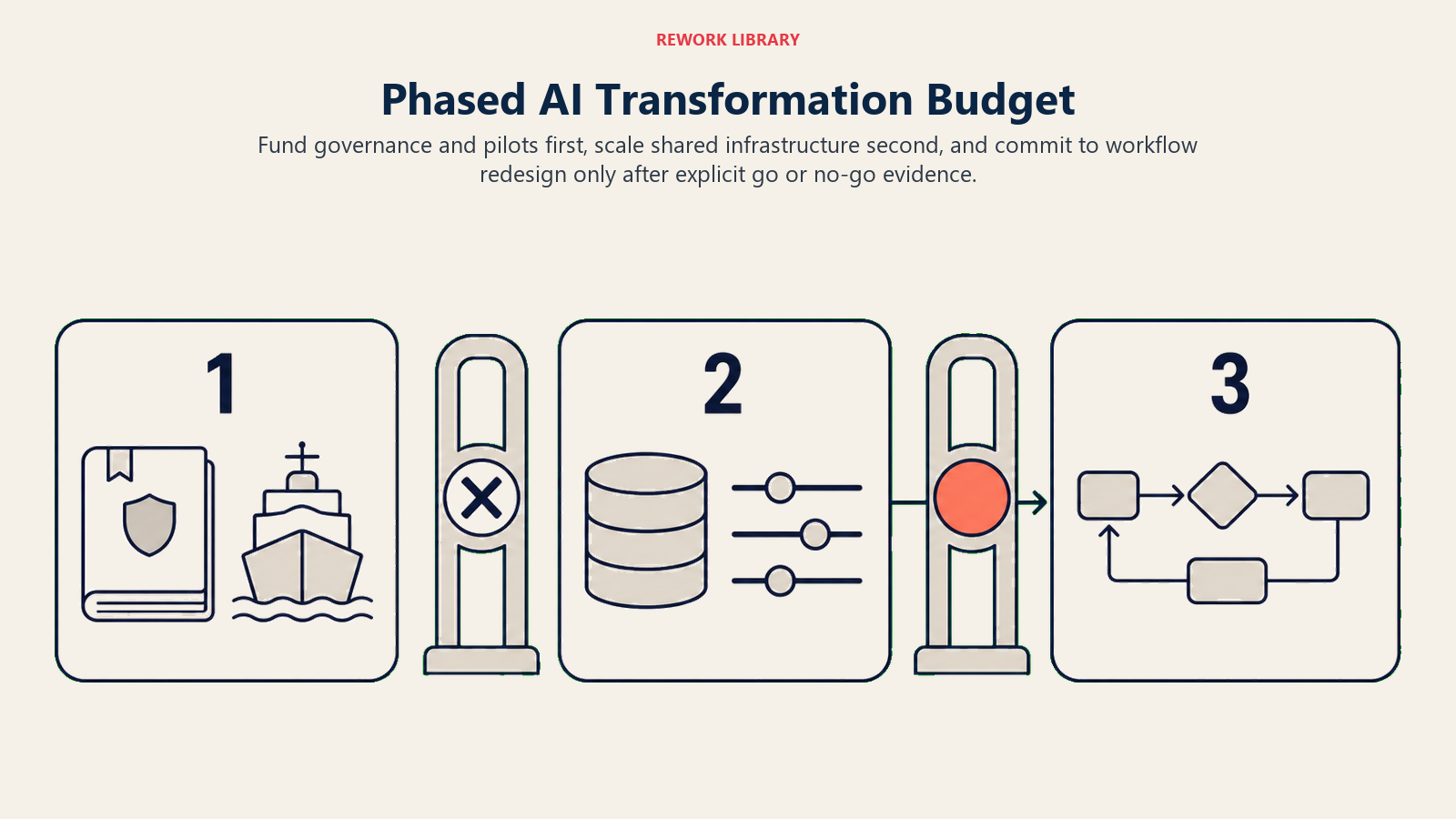

The phased budget structure

The phased structure gives the CFO control over risk while still funding enough work to prove whether AI transformation can create measurable value.

One of the most effective structures for gaining CFO approval is the phased commitment model. Rather than asking for the full transformation budget upfront, present a staged investment thesis where each phase has its own business case, measurement gate, and go/no-go decision point.

Phase 1 (Months 1-6): Governance and pilot Budget: Lower. Typically $50,000-$150,000 for mid-market. Purpose: Establish policy, choose initial use cases, run controlled pilots on highest-confidence ROI cases. Exit criteria: Pilot ROI validated within 20% of projections, governance framework in place, team trained.

Phase 2 (Months 7-18): Infrastructure and scale Budget: Larger. Typically 2-4x Phase 1. Purpose: Deploy infrastructure that will serve multiple use cases. Integrate with core systems. Scale the use cases that passed Phase 1 validation. Exit criteria: Infrastructure serving 3+ use cases, integration work complete, measurable productivity gains in pilot cohorts.

Phase 3 (Year 2+): Org redesign and advanced use cases Budget: Variable, tied to outcomes from Phase 2. Purpose: Workflow redesign around AI capabilities. Advanced Predict and Execute use cases. Possible headcount reallocation. Exit criteria: AI capabilities embedded in core workflows, ROI compounding across use cases.

CFOs are more comfortable approving Phase 1 with a clear gate than approving the full transformation budget at once. The gate gives them control. The phasing shows you've thought about sequencing rather than just asking for maximum budget upfront.

From the 5 Stages of AI Maturity perspective, Phases 1-3 above correspond roughly to moving from Stage 1 (Ad-hoc) through Stage 3 (Scaled). Presenting the phased budget in these terms helps CFOs understand that the investment is building toward a defined end state, not funding an open-ended capability expansion.

The 3-Frame CFO Pitch

The 3-Frame CFO Pitch structures AI budget proposals around the three value frames CFOs actually evaluate: cost avoidance (what growth we won't need to fund because AI handles the volume), option value (what we can do faster or cheaper when market conditions require a response), and competitive defense (what cost-to-serve disadvantage we accept if we don't move). Each frame speaks to a different part of the CFO's risk and return calculus. Together, they make a budget case that does not depend on unproven revenue uplift claims to survive a finance review.

Quotable: "CFOs have an allergy to technology-forward budget pitches. 'We need vector database infrastructure and an embeddings pipeline' is a technology case. 'We need to cut invoice processing cost from $14 to $1.50 while reducing AP cycle time by 60%' is a business case."

Quotable: "The phased commitment model consistently outperforms lump-sum AI budget requests. CFOs approve Phase 1 more readily than full transformation budgets, because the go/no-go gate gives them control without halting progress."

Quotable: "A realistic total cost of AI transformation for a mid-market company is 2.5-4x the software licensing cost once internal engineering time, data preparation, change management, and governance infrastructure are included." (Deloitte)

| Budget Framing | What CFO Evaluates | Why It Works | Common Mistake |

|---|---|---|---|

| Cost avoidance | Counterfactual headcount at current growth rate | Ties to existing budget lines | Avoidance not in approved budget = not real savings |

| Option value | Speed-to-respond when market condition triggers | Reduces risk premium on AI investment | Too abstract without named trigger conditions |

| Competitive defense | Competitor cost structure at successful deployment | Converts AI from "nice to have" to strategic necessity | Can't name specific competitors or cite evidence |

Rework Analysis: Based on CFO approval patterns, AI budget proposals that use the 3-Frame structure and include a phased commitment with clear go/no-go gates are approved at significantly higher rates than single-ROI-number proposals. The phased structure reduces the CFO's downside exposure while keeping the program moving, which is the core tension that most AI budget presentations fail to resolve.

The competitive risk frame

The "what happens if we don't invest" answer deserves its own section because it's the most underused frame in AI budget presentations.

Most operators present AI investment as upside (we'll be more efficient, we'll move faster). CFOs evaluate upside claims skeptically because they've heard them before. What they hear less often is a specific, credible argument for why not investing creates structural disadvantage. That argument tends to land.

The competitive risk frame works like this: identify where AI is reducing cost-to-serve or compressing cycle time in your market. Name competitors who are visibly deploying (public announcements, product releases, job postings for AI roles are all evidence). Then calculate what happens to your cost position if they succeed and you don't.

For example: if your largest competitor deploys AI-assisted customer success and reduces their customer success (CS) headcount by 30% while maintaining retention rates, their CS cost-to-serve drops significantly. They can pass some of that as competitive pricing pressure or absorb it as margin. Either way, you're at a structural disadvantage in your next enterprise contract renewal if your costs haven't moved.

This argument isn't fear-based speculation. It's capital allocation logic. CFOs understand it because it's how they think about every other infrastructure investment. You don't invest in ERP modernization because it's exciting. You invest because a competitor operating on a modern ERP has a 15% cost advantage in order processing that compounds over time.

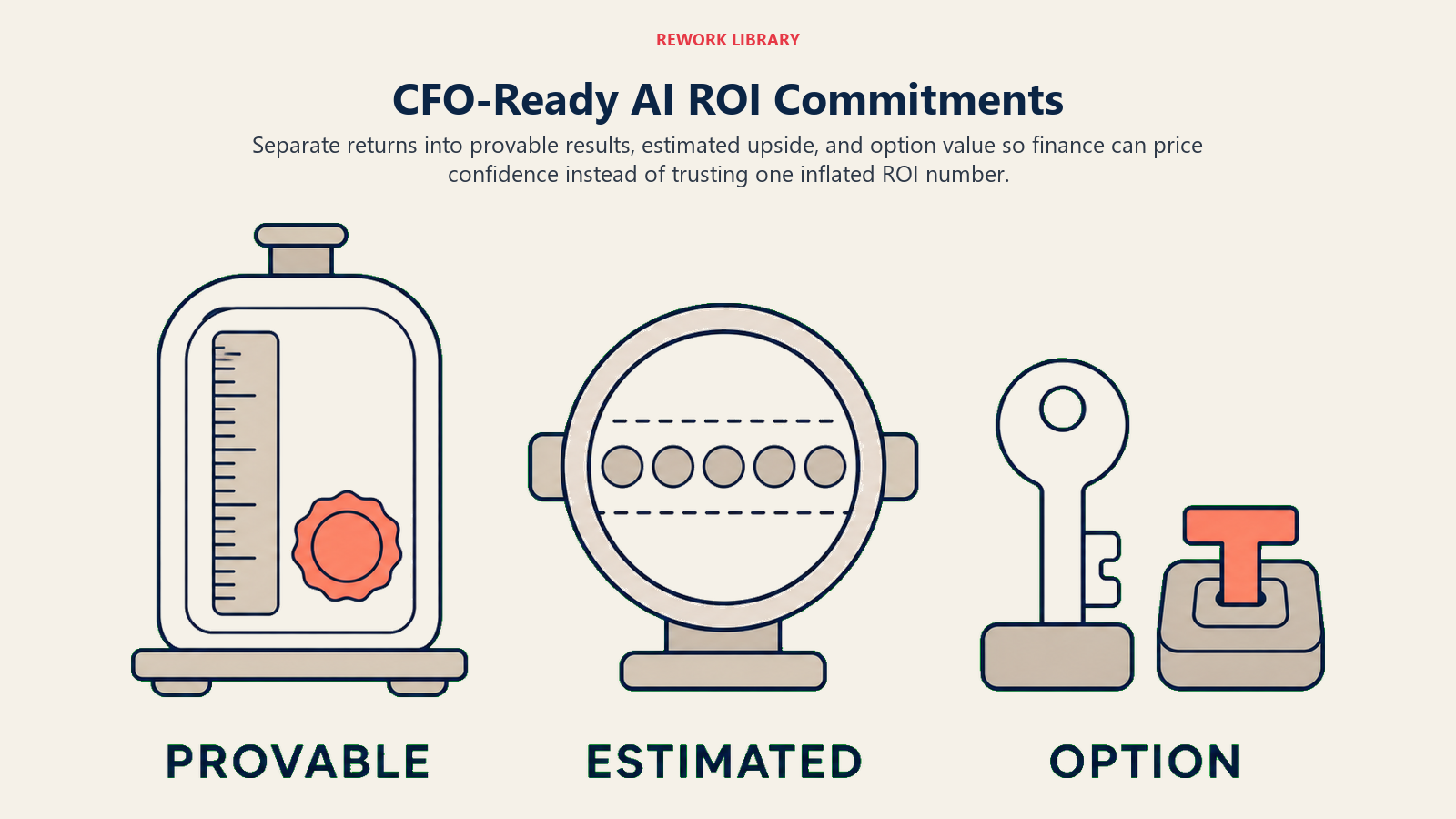

The ROI commitment CFOs can accept

Here's the honest version of the ROI conversation, which works better than the oversold version:

"We can prove the following with certainty: [X hours saved, Y reduction in specific process cost, Z increase in throughput for this specific workflow]. We expect the following but cannot prove it yet because we don't have a measurement baseline: [conversion rate improvement estimate, churn reduction estimate]. We're investing in [capability] as a strategic option: if [specific market condition] happens, this capability means we can [specific response] without the 6-12 month deployment lead time."

That's three commitment levels: provable, estimated, and option-value. Most AI programs have all three types of expected return. Presenting them honestly, rather than blending them into a single optimistic ROI number, signals intellectual honesty. CFOs who have been burned by inflated ROI projections respond to this framing better than to confident projections with no confidence intervals.

The 5 Dimensions of AI ROI gives you the vocabulary for each commitment level. The Why AI ROI Is Hard to Prove article is worth reading before the CFO meeting so you understand the attribution problems before they ask. And ROI by ACE Capability lets you walk into the room knowing the measurement difficulty and typical return window for each capability in the proposal.

Before you walk into the room: a preparation checklist

Run through these in the 24 hours before the meeting.

Business case

- Can you state the problem in one sentence without technical jargon?

- Do you have a current baseline for the primary metric (cost, time, error rate)?

- Can you state the target state and timeline?

Competitive risk

- Can you name two competitors who are visibly investing in AI in your market?

- Can you explain what their cost structure looks like at successful deployment?

Total cost

- Have you included internal labor time, not just software licensing?

- Have you included data preparation, governance infrastructure, and change management?

Measurement plan

- Do you have 3-5 specific metrics with baselines?

- Do you know how you'll collect the data for each metric?

- Is there a 90-day gate built in?

Downside scenario

- What's the most likely failure mode?

- What's the early warning indicator?

- What's the decision gate before the next phase of spend?

Phasing

- Is the ask structured as a phase, not a full transformation budget?

- Is there a clear go/no-go decision point after Phase 1?

The CFO meeting goes wrong when the program lead walks in with a technology story and the CFO wants a business story. It goes right when you walk in speaking the language CFOs use to evaluate every other capital allocation decision: business problem, measurement plan, competitive context, total cost, phased commitment, honest downside scenario.

The Buy vs. Build for SaaS AI Features article is worth reading before the meeting too, because CFOs often ask about make-vs-buy logic and the answer shapes the total cost model significantly.

Frequently Asked Questions

What do CFOs actually ask about AI budget proposals?

CFOs consistently ask four questions: What is the business case (not the technology case)? What happens if we don't invest? How do we measure success at 12 months? And what is the risk if it doesn't work? Most AI budget proposals fail because they answer the technology questions and avoid these four business questions.

How should AI budget be framed to a CFO?

Frame AI investment as capital allocation, not IT expense. AI infrastructure has more in common with building a factory than buying software licenses. Early investment creates productive capacity that compounds as marginal deployment cost drops over time. Presenting a phased commitment model with clear go/no-go gates is consistently more effective than requesting the full transformation budget upfront.

What is the true total cost of AI transformation?

The realistic total cost is 2.5-4x the software licensing cost for a mid-market company. Hidden costs routinely omitted from initial proposals include internal engineering time for integration (often 2-4x the software cost), data preparation and cleaning (frequently underestimated by 50%), change management and training, governance infrastructure, and ongoing model evaluation. According to Deloitte, hidden implementation costs are the most common reason AI programs miss projected returns.

What is the 3-Frame CFO Pitch for AI budget?

The 3-Frame CFO Pitch structures AI budget proposals around cost avoidance (what growth costs AI will absorb), option value (what becomes possible at speed when market conditions require it), and competitive defense (what structural disadvantage accepting the status quo creates). These three frames address the CFO's core risk and return concerns without depending on unproven revenue uplift claims.

How should the AI budget failure scenario be addressed?

Separate the budget into three buckets: recoverable costs (software subscriptions you can cancel), partially recoverable costs (sunk integration time), and unrecoverable costs (reputational impact, team morale). Name the most likely failure mode, identify its early warning indicator, and propose a decision gate before the next phase of spend. This preparation signals risk-management competence, not pessimism.

How do CFOs evaluate competitive risk from AI investment?

The competitive risk argument works when it names specific competitors who are visibly investing, estimates what their cost structure looks like at successful deployment, and calculates the structural disadvantage your organization accepts if they succeed and you don't. Abstract arguments about "falling behind on AI" do not land. Specific cost-to-serve comparisons tied to contract renewal or pricing competitiveness do.

Co-Founder, Rework.com

On this page

- What CFOs actually ask about AI budget

- "What's the business case, not the technology case?"

- "What happens if we don't invest?"

- "How do we measure success at 12 months?"

- "What's the risk if it doesn't work?"

- Framing AI as capital allocation, not IT expense

- The total cost of transformation model

- The phased budget structure

- The 3-Frame CFO Pitch

- The competitive risk frame

- The ROI commitment CFOs can accept

- Before you walk into the room: a preparation checklist