Tahap Kematangan AI SaaS: Di Mana Posisi Anda, dan Apa Langkah Selanjutnya?

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Sebagian besar perusahaan SaaS berpikir mereka lebih maju dalam AI daripada yang sebenarnya. Itu bukan kritik. Itu adalah masalah struktural dalam cara pengadopsian AI diukur.

Pertanyaan yang diajukan oleh sebagian besar tim kepemimpinan adalah "berapa banyak alat AI yang kita gunakan?" Jawabannya biasanya setidaknya lima: ChatGPT untuk beberapa hal, Notion AI untuk dokumen, GitHub Copilot untuk engineer, Gong atau Clari untuk sales, mungkin alat AI health scoring untuk CS. Berdasarkan jumlah, jawabannya terlihat seperti perusahaan yang sudah maju.

Tetapi model kematangan bukan tentang jumlah alat. Ini tentang seberapa dalam AI tertanam dalam workflow yang menghasilkan pendapatan. Tim yang menggunakan ChatGPT untuk memoles email sales dan tim yang AI sales-nya terhubung ke AI CS mereka, mengumpankan sinyal ekspansi kembali ke penargetan pipeline, tidak berada di tahap yang sama. Mereka dipisahkan oleh kesenjangan yang biasanya membutuhkan 18-24 bulan untuk diatasi.

Lima tahap dalam model kematangan Level 5 ACE Framework hadir untuk menjawab pertanyaan yang berbeda: bukan "seberapa banyak AI yang Anda gunakan?" tetapi "apa yang sebenarnya dilakukan AI terhadap metrik operasional Anda?" Perbedaan tersebut menentukan posisi Anda. Dan posisi Anda menentukan apa yang harus dilakukan selanjutnya. Artikel strategi 5 Tahap Kematangan AI yang lebih luas mencakup bagaimana kemajuan ini berlaku di semua industri, tidak hanya SaaS.

The SaaS 5-Stage AI Curve

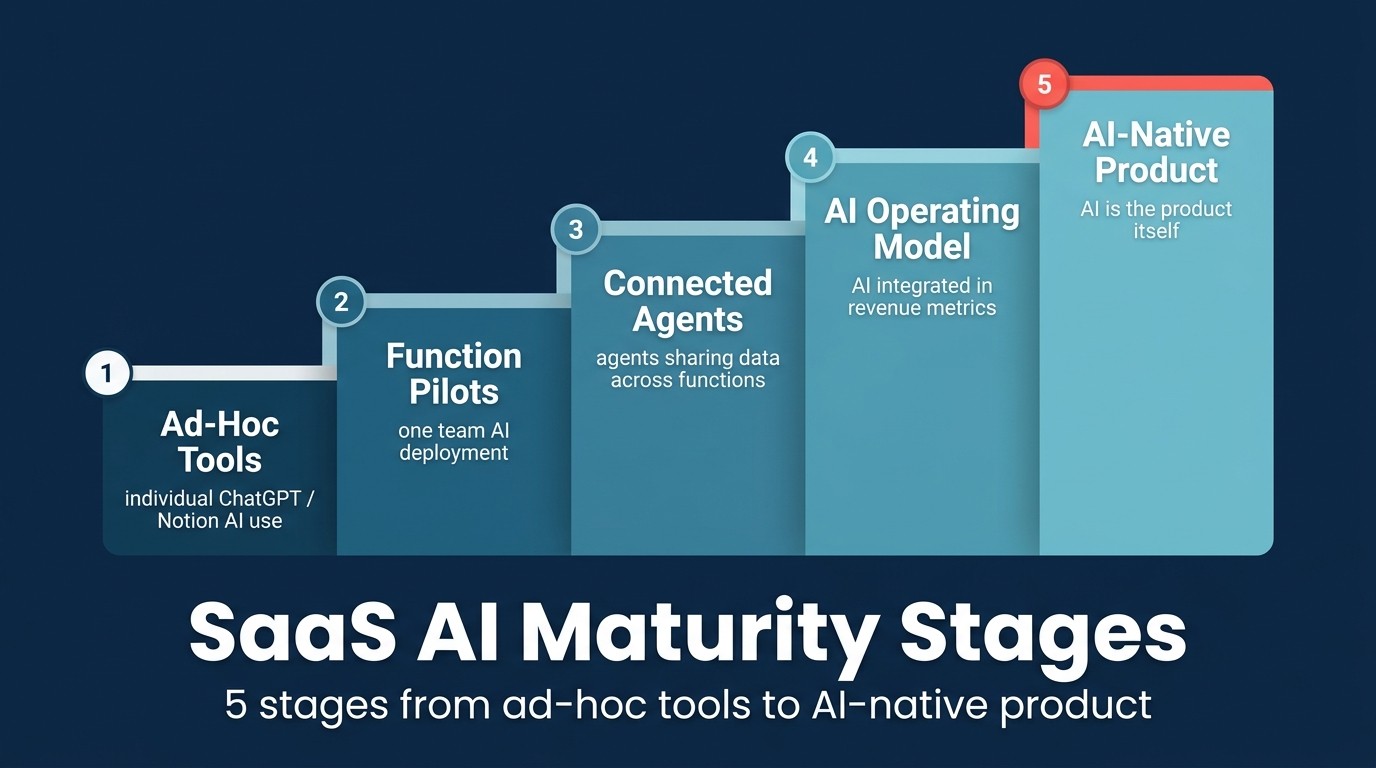

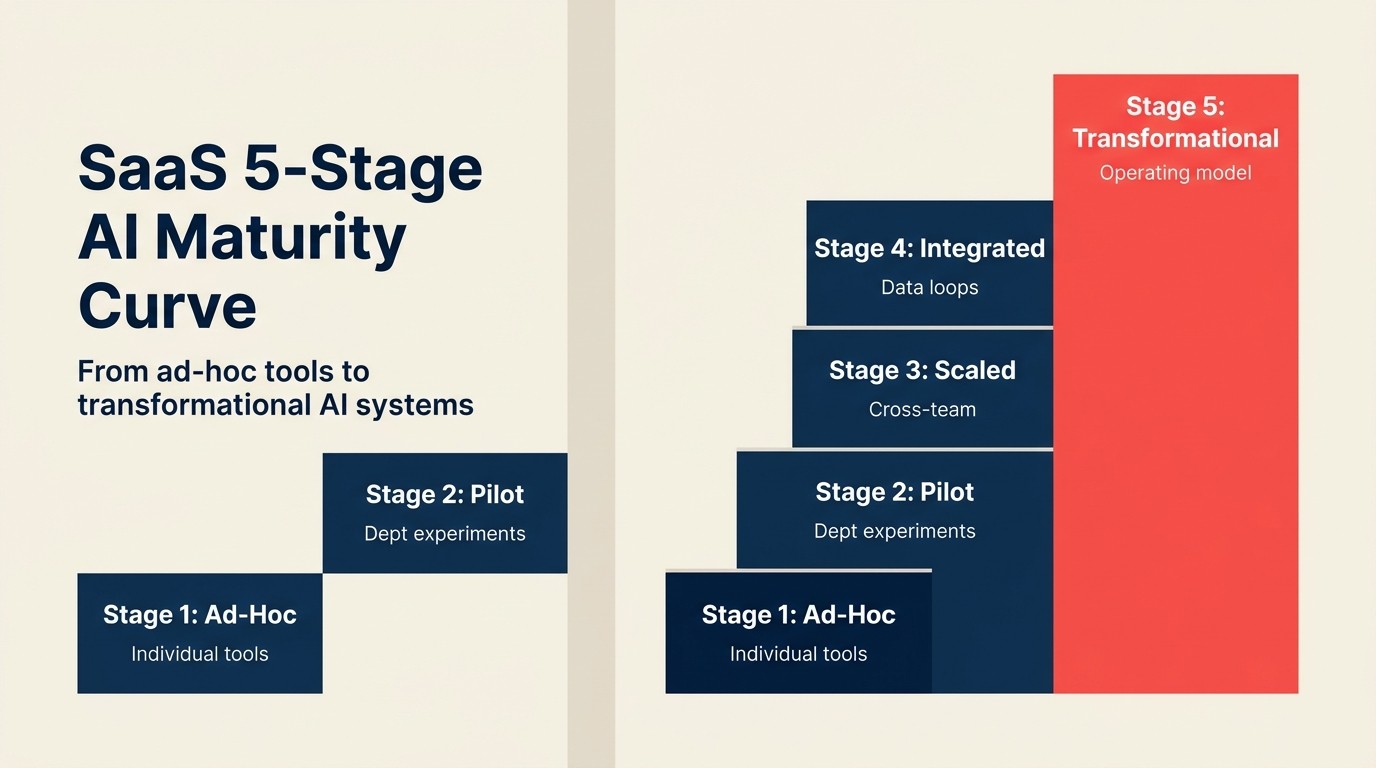

The SaaS 5-Stage AI Curve adalah model kematangan diagnostik yang memetakan perusahaan SaaS ke salah satu dari lima tahap operasional berdasarkan seberapa dalam AI tertanam dalam workflow yang menghasilkan pendapatan, bukan berdasarkan jumlah alat atau level pengeluaran. Tahap 1 (Ad-hoc): alat individual, tanpa pengukuran. Tahap 2 (Pilot): satu proyek AI terstruktur dengan pemilik, use case, dan metrik keberhasilan yang ditentukan. Tahap 3 (Scaled): fungsi yang dibantu AI terukur melampaui baseline sebelum AI. Tahap 4 (Integrated): AI agent di berbagai fungsi berbagi data dan sinyal secara real time. Tahap 5 (Transformational): AI mengubah model operasional itu sendiri; rasio headcount-terhadap-ARR berbeda dari norma industri. Setiap tahap memiliki kriteria pembuka tertentu dan failure mode khas yang mencegah kemajuan ke tahap berikutnya.

Tahap 1: Ad-hoc

Karyawan individual menggunakan alat AI tanpa strategi, koordinasi, atau pengukuran di tingkat perusahaan. ChatGPT, Claude, dan Microsoft Copilot pertama kali muncul di sini. Seseorang di tim sales mulai menggunakan ChatGPT untuk menulis email dingin. Lead engineering mulai menggunakan GitHub Copilot. Marketing manager menggunakan Notion AI. Tidak ada yang memutuskan melakukan semua ini. Hal itu hanya terjadi.

Profil tipikal:

- ARR (annual recurring revenue): pra-pendapatan hingga $5M

- Headcount: 5-50

- Jejak AI: langganan pribadi, bukan akun perusahaan

- Pengukuran: tidak ada

- Vendor stack: ChatGPT / Claude consumer tier, Microsoft 365 Copilot jika menggunakan M365

Seperti apa Tahap 1 sebenarnya dalam praktik: Tidak ada shared prompt library. Anggota tim yang berbeda mendapatkan hasil yang sangat berbeda dari alat yang sama karena tidak ada yang berbagi apa yang berhasil. Perusahaan tidak memiliki data tentang karyawan mana yang menggunakan AI, untuk apa, atau apakah hal itu membuat mereka lebih efektif. CEO mungkin antusias tentang AI; antusiasme itu tidak terhubung ke hasil yang terukur.

Failure mode nyata di Tahap 1: Bukan karena orang menggunakan alat yang buruk. Ini karena penggunaan AI yang baik tetap terjebak di kepala individu. Ketika sales rep yang menemukan workflow ChatGPT yang bagus untuk prospecting pergi, pengetahuan itu ikut pergi bersamanya.

Yang harus dilakukan di tahap ini: Audit apa yang sudah dilakukan tim Anda dengan AI. Anda akan menemukan 6-8 alat dan setidaknya beberapa power user nyata dengan workflow yang layak dibagikan. Jadikan 3 alat resmi (akun perusahaan, akses bersama), dokumentasikan 2-3 workflow yang jelas berhasil, dan tentukan satu metrik yang akan dipantau selama 90 hari. Jangan lakukan lebih dari ini. Tahap 2 membutuhkan upaya terfokus yang belum didukung oleh Tahap 1. Tahap 1 ke 2: ad-hoc ke pilot membahas transisi ini secara detail.

Key Facts: Distribusi Kematangan AI SaaS

- Adopsi AI enterprise melonjak ke 88% pada 2025, naik dari 78% setahun sebelumnya, tetapi hanya 28% enterprise yang menggambarkan adopsi AI mereka sebagai "matang" dengan AI tertanam di berbagai fungsi bisnis (Medha Cloud/Deloitte, 2025)

- Kurang dari 5% aplikasi enterprise saat ini memiliki AI agent spesifik tugas yang tertanam; pada akhir 2026 angka tersebut diproyeksikan mencapai 40% (Deloitte, 2026)

- Pemimpin digital dan AI mengungguli yang tertinggal sebesar 2-6x dalam total shareholder return, dan kesenjangan kematangan antara pemimpin dan yang tertinggal telah tumbuh 60% selama tiga tahun (McKinsey, 2025)

Tahap 2: Pilot

Proyek AI terstruktur pertama dengan pemilik yang ditentukan, use case yang ditentukan, dan metrik keberhasilan yang ditentukan. Di sinilah strategi dimulai. Bukan strategi AI sebagai dokumen visi lima tahun, tetapi eksperimen 90 hari dengan hipotesis yang jelas: "Jika kita menggunakan Gong AI di setiap discovery call, kita pikir kualitas pipeline akan meningkat sebesar X%."

Profil tipikal:

- ARR: $1M-$10M

- Headcount: 20-100

- Jejak AI: 1-2 alat AI yang dibeli perusahaan dengan pemantauan aktif

- Pengukuran: satu metrik pilot, ditinjau setiap bulan

- Vendor stack: Gong (sales call), Gainsight atau Vitally (CS health scoring), Intercom Fin (support), atau yang setara

Seperti apa Tahap 2 sebenarnya dalam praktik: Ada satu AI agent yang berjalan di satu fungsi. Tim CS menggunakan AI health scoring, atau tim sales menggunakan analisis panggilan. Seseorang memilikinya. Ada tinjauan mingguan atau dua mingguan apakah ini berhasil. Sisa perusahaan sebagian besar tidak tersentuh.

Tonggak yang menandai Tahap 2 bukan "kita membeli alat." Ini adalah "kita memiliki hasil terukur setelah 90 hari." Tanpa pengukuran, Tahap 2 hanyalah Tahap 1 dengan tagihan.

Failure mode nyata di Tahap 2: Pilot berhasil menurut metriknya tetapi tidak ada yang menskalakan. "Kita akan memperluas ke tim penuh kuartal berikutnya" menjadi penangguhan tanpa batas waktu. Penyebab umum adalah bahwa pilot dimiliki oleh satu penggemar, dan ketika orang itu beralih ke prioritas lain, momentum terhenti. Pilot Tahap 2 yang tidak memiliki "dan jika pilot berhasil, inilah rencana ekspansinya" yang dibangun sebelum peluncuran cenderung tetap menjadi pilot selamanya.

Yang harus dilakukan di tahap ini: Jalankan pilot 90 hari di satu fungsi, dengan satu metrik yang terhubung ke pendapatan. Untuk CS: delta NRR (net revenue retention) atau tingkat churn untuk akun yang dibantu AI versus kelompok kontrol. Untuk sales: tingkat konversi pipeline untuk rep yang menggunakan AI call coaching versus baseline. Kemudian, sebelum 90 hari berakhir, tulis ringkasan ekspansi yang mengasumsikan pilot berhasil. Tahap 2 ke 3: pilot ke scaled mencakup playbook ekspansi setelah data pilot masuk.

Tahap 3: Scaled

Pilot telah terbukti dan diperluas ke tim penuh atau beberapa tim. AI adalah bagian dari cara kerja dilakukan, bukan eksperimen. Dua hingga tiga AI agent berjalan di berbagai fungsi. Perusahaan memiliki infrastruktur untuk mengukurnya.

Profil tipikal:

- ARR: $5M-$30M

- Headcount: 50-200

- Jejak AI: 3-5 alat AI di seluruh perusahaan, tertanam dalam workflow tim

- Pengukuran: dashboard berkelanjutan per fungsi, tinjauan AI kuartalan dalam pertemuan kepemimpinan

- Vendor stack: Gong + Gainsight/Vitally + Intercom Fin sebagai trio inti, ditambah in-product AI yang mulai muncul

Seperti apa Tahap 3 sebenarnya dalam praktik: Fungsi yang dibantu AI mengungguli yang tidak menggunakan AI dalam metrik yang Anda pantau. Tim CS Anda yang menggunakan AI health scoring memiliki tingkat peringatan dini yang lebih baik daripada sebelumnya. Rep sales Anda yang menggunakan AI call coaching menunjukkan kualitas discovery yang lebih baik berdasarkan metrik yang Anda ukur.

Tetapi fungsi-fungsinya masih belum saling berkomunikasi dari perspektif AI. AI CS Anda dan AI sales Anda adalah alat terpisah dengan data terpisah. Health score di Gainsight tidak terhubung ke penargetan ekspansi di CRM Anda. Koneksi tersebut adalah Tahap 4, dan sebagian besar perusahaan Tahap 3 belum memilikinya.

Tonggak Tahap 3: "Fungsi yang dibantu AI mengungguli yang tidak menggunakan AI." Bukan "kita menggunakan AI." Bukan "tim menyukainya." Perbedaan kinerja yang terukur.

Failure mode nyata di Tahap 3: Ekspansi horizontal tanpa kedalaman. Tim menambahkan lebih banyak alat AI tanpa menguasai yang sudah ada. Anda berakhir dengan lima alat AI, masing-masing dengan adopsi 30%, daripada dua alat AI dengan adopsi 90%. Keluasan tanpa adopsi adalah Tahap 1 dengan lebih banyak tagihan.

Yang harus dilakukan di tahap ini: Pilih 2-3 alat AI dengan adopsi tertinggi dan korelasi outcome terbaik. Gandakan usaha pada alat-alat tersebut. Perluas ke fungsi yang berdekatan hanya setelah fungsi pertama sepenuhnya diadopsi dan diukur. Jika AI CS berjalan dengan baik, tambahkan AI Sales. Jika AI Sales berjalan, investasi infrastruktur data untuk Tahap 4 menjadi investasi berikutnya. Tahap 3 ke 4: scaled ke integrated mencakup keputusan infrastruktur data yang membuka AI lintas fungsi.

Tahap 4: Integrated

AI agent di berbagai fungsi berbagi data dan sinyal. Sinyal AI Sales mengisi AI CS. Health score AI CS menginformasikan penargetan ekspansi AI Sales. Perusahaan telah membangun infrastruktur data untuk menghubungkan apa yang sebelumnya merupakan alat yang terisolasi.

Profil tipikal:

- ARR: $15M-$100M

- Headcount: 100-500

- Jejak AI: 5+ alat AI dengan koneksi data di antara mereka, ditambah fitur AI dalam produk untuk pelanggan

- Pengukuran: dashboard AI lintas fungsi; outcome AI terhubung ke metrik pendapatan

- Vendor stack: Alat yang dibuat khusus per fungsi (Gong, Gainsight, Intercom AI, Rework untuk AI ops workflow) ditambah lapisan data yang menghubungkannya

Seperti apa Tahap 4 sebenarnya dalam praktik: Pipeline ekspansi dibentuk oleh data health AI CS. Ketika health score pelanggan Anda turun di bawah ambang batas, CRM Anda secara otomatis membuat tugas ekspansi di akun tersebut. Ketika AI analisis sales call mengidentifikasi sinyal pembelian dalam percakapan, sinyal tersebut muncul di tampilan akun tim CS untuk perusahaan tersebut. Data mengalir di antara agent.

Di sinilah compounding nyata dimulai. Satu input AI menciptakan peningkatan berantai di seluruh fungsi. Dan yang terpenting: data moat dibangun. AI Anda tidak lagi hanya dilatih pada data generik. Ini belajar dari pola spesifik perilaku pelanggan Anda dalam produk Anda.

Failure mode nyata di Tahap 4: Membangun infrastruktur data tanpa tata kelola. Ketika AI agent berbagi sinyal lintas fungsi, kesalahan merambat lebih cepat. Algoritma health score yang salah dikalibrasi tidak hanya merusak outcome CS; ini mengkorupsi data ekspansi sales dan perkiraan churn keuangan. Kualitas data dan audit model menjadi persyaratan operasional di Tahap 4, bukan renungan. AI risk register: apa yang perlu dilacak mencakup kerangka tata kelola yang mencegah kesalahan AI lintas fungsi dari merambat.

Yang harus dilakukan di tahap ini: Petakan tiga aliran data AI lintas fungsi dengan nilai tertinggi dan bangun semuanya. Dokumentasikan model tata kelola data sebelum menghubungkan sistem. Tetapkan pemilik AI ops yang meninjau kinerja model setiap bulan.

Tahap 5: Transformational

AI mengubah model operasional, bukan hanya alatnya. Rasio headcount-terhadap-ARR berbeda dari norma industri karena AI menanggung beban kerja yang sebelumnya membutuhkan orang. Produk ini memiliki moat compounding berbasis AI. Dalam beberapa kasus, AI adalah produknya.

Profil tipikal:

- ARR: $50M-multi-miliar

- Headcount: terukur, tetapi tumbuh lebih lambat dari ARR relatif terhadap baseline sebelum AI

- Jejak AI: AI tertanam dalam produk inti dan semua operasi internal

- Pengukuran: metrik operasional (revenue per FTE (full-time equivalent), NRR, CAC payback) terukur berbeda dari baseline sebelum AI

- Contoh: ekosistem Salesforce Einstein, HubSpot Breeze, Jasper (AI adalah produknya)

Seperti apa Tahap 5 sebenarnya: Perusahaan di Tahap 5 tidak hanya menggunakan lebih banyak alat AI daripada perusahaan Tahap 3. Ini beroperasi secara berbeda di tingkat struktural. Support pelanggan tidak skala secara linear dengan pelanggan karena AI menangani 60-70% tiket. Output marketing tidak skala dengan headcount karena AI menghasilkan, menguji, dan mengoptimalkan konten. P&L terlihat berbeda: biaya headcount lebih rendah relatif terhadap ARR, berpotensi biaya infrastruktur lebih tinggi dari API AI.

Jasper adalah contoh Tahap 5 yang bersih: produknya adalah AI, sehingga kematangan AI dan kematangan produk adalah hal yang sama. HubSpot adalah Tahap 5 SaaS yang lebih tipikal: AI meningkatkan setiap fungsi (marketing, sales, CS, produk) dan tertanam secara mendalam dalam produk yang mereka jual. Perusahaan terlihat berbeda secara operasional dari tiga tahun lalu. Tahap 5: ketika AI membentuk ulang produk Anda mendokumentasikan apa yang dibutuhkan pergeseran struktural ini dari kepemimpinan produk dan bisnis.

Realitas jujur tentang Tahap 5 di 2026: Sebagian besar perusahaan yang berinteraksi dengan tim Anda tidak berada di Tahap 5. Sebagian besar perusahaan Series A dan B berada di Tahap 1 atau 2. Perusahaan Series C yang dijalankan dengan baik mungkin berada di Tahap 3. Tahap 4 sangat jarang di luar perusahaan dengan kapasitas data engineering yang berdedikasi. Tahap 5 adalah Salesforce, HubSpot, dan segelintir startup AI-native.

Itu bukan hal yang mengecilkan hati. Ini berarti Anda tidak setertinggal yang disarankan oleh kebisingan industri. Ini juga berarti peta jalan dari Tahap 2 ke Tahap 3 adalah proyek 12-18 bulan yang nyata dan dapat dicapai bagi sebagian besar perusahaan SaaS.

"Sebagian besar tim SaaS dapat berpindah dari Tahap 1 ke Tahap 3 dalam 18 bulan dengan urutan yang tepat. Jalurnya tidak secara teknis kompleks. Ini membutuhkan keputusan di setiap tahap tentang apa yang diukur dan siapa yang memilikinya. Tahap 1 ke 2: tetapkan pemilik pilot AI dan tentukan satu metrik. Tahap 2 ke 3: perlakukan scaling sebagai masalah produk dan tanamkan alat dalam workflow. Tahap 3 ke 4: framing investasi infrastruktur data sebagai proyek pendapatan, bukan proyek tooling." (Rework Analysis, berdasarkan penelitian kematangan AI McKinsey, 2025)

"Pertanyaan yang diajukan oleh sebagian besar tim kepemimpinan adalah 'berapa banyak alat AI yang kita gunakan?' Model kematangan menjawab pertanyaan yang berbeda: apa yang sebenarnya dilakukan AI terhadap metrik operasional Anda? Tim yang menggunakan 5 alat AI di Tahap 1 dan tim yang AI sales-nya terhubung ke AI CS mereka di Tahap 4 dipisahkan oleh kesenjangan yang biasanya membutuhkan 18-24 bulan untuk diatasi." (Rework Analysis, 2025)

"Hampir semua perusahaan berinvestasi dalam AI, tetapi hanya 1% yang percaya telah mencapai kematangan, dan hampir dua pertiga belum mulai menskalakan AI di seluruh enterprise. Kebisingan industri menciptakan kesan palsu bahwa Tahap 3-4 adalah norma. Bukan begitu. Mengakui di mana perusahaan Anda sebenarnya berada membuat peta jalan menjadi dapat dikelola." (McKinsey AI Maturity Research, 2025)

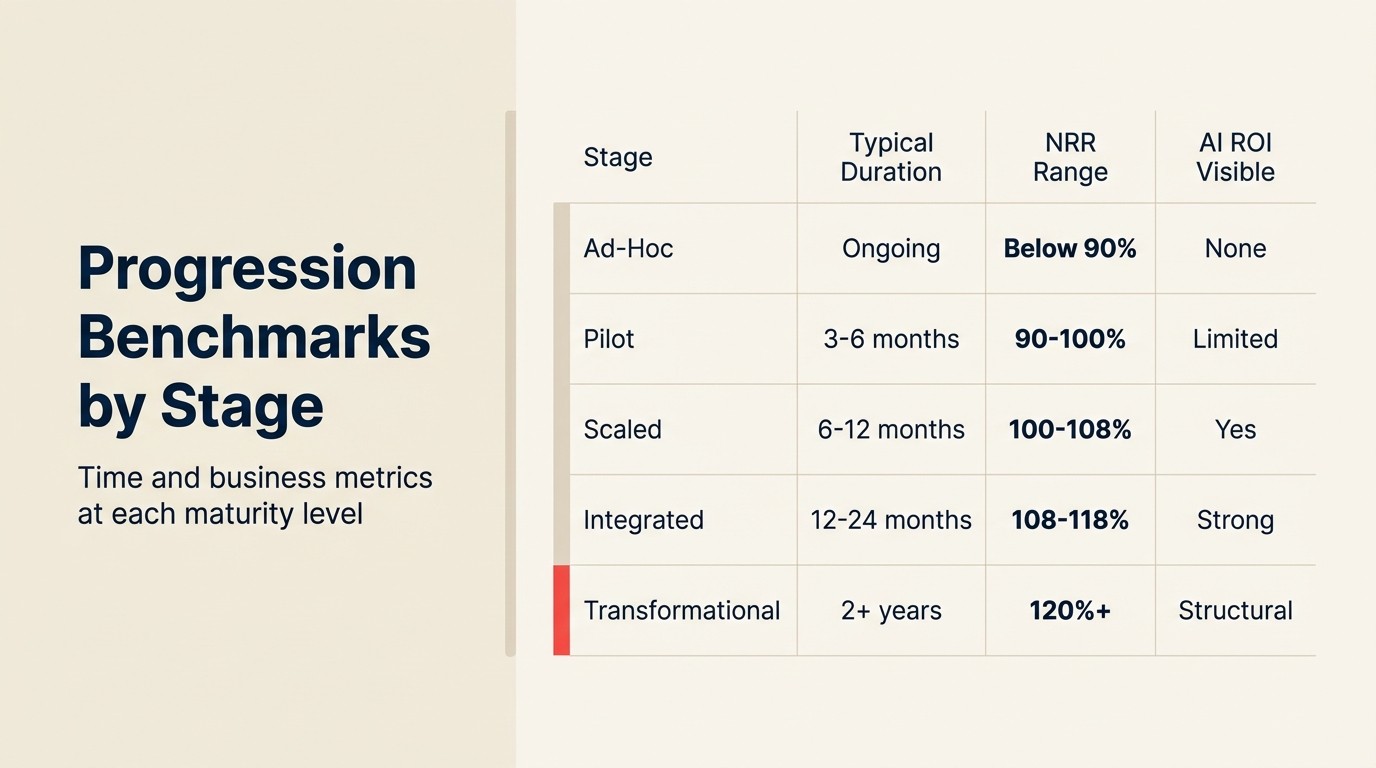

Distribusi Tahap dan Tolok Ukur Kemajuan

| Tahap | Rentang ARR | Headcount | Metrik Utama | Waktu Tipikal ke Tahap Berikutnya |

|---|---|---|---|---|

| 1: Ad-hoc | Pra-pendapatan hingga $5M | 5-50 | Tidak ada | 6-12 bulan (dengan upaya terfokus) |

| 2: Pilot | $1M-$10M | 20-100 | Satu metrik pilot, ditinjau setiap bulan | 6-12 bulan setelah pilot pertama berhasil |

| 3: Scaled | $5M-$30M | 50-200 | Kinerja fungsi dibantu AI vs. tidak dibantu AI | 12-18 bulan (investasi infrastruktur data diperlukan) |

| 4: Integrated | $15M-$100M | 100-500 | Berbagi sinyal AI lintas fungsi | 18-24 bulan (jarang, membutuhkan data engineering berdedikasi) |

| 5: Transformational | $50M+ | Terukur pada rasio lebih rendah dari baseline sebelum AI | Revenue-per-FTE vs. baseline sebelum AI | Berkelanjutan; berbasis struktural bukan tonggak |

Sumber: McKinsey AI Maturity Research 2025, Deloitte SaaS AI Agents Report 2026, BetterCloud SaaS Industry Data 2026

Di mana sebagian besar perusahaan SaaS sebenarnya berada di 2026

Distribusi jujur berdasarkan indikator yang dapat diamati:

- Tahap 1 (Ad-hoc): Mayoritas perusahaan SaaS berdasarkan jumlah. Sekitar 60-70% perusahaan dengan ARR di bawah $5M. Alat AI digunakan, tanpa strategi.

- Tahap 2 (Pilot): Sebagian besar yang didanai Series A dan awal Series B. Satu proyek AI terstruktur berjalan. Banyak perusahaan terjebak di sini selama 12-18 bulan.

- Tahap 3 (Scaled): Perusahaan Series B akhir dan Series C dengan budaya AI ops yang fungsional. Masih merupakan minoritas.

- Tahap 4 (Integrated): Jarang. Membutuhkan investasi data engineering yang sebagian besar perusahaan tunda hingga ARR membenarkannya.

- Tahap 5 (Transformational): Sejumlah kecil perusahaan yang didanai dengan baik, AI-native atau AI-forward.

Penelitian McKinsey tentang kematangan AI menemukan bahwa hampir semua perusahaan berinvestasi dalam AI tetapi hanya 1% yang percaya telah mencapai kematangan, dan hampir dua pertiga belum mulai menskalakan AI di seluruh enterprise. Kesenjangan kematangan antara pemimpin dan yang tertinggal telah tumbuh 60% selama tiga tahun, dengan pemimpin digital dan AI mengungguli yang tertinggal sebesar dua hingga enam kali dalam total shareholder return.

Kebisingan industri menciptakan kesan palsu bahwa Tahap 3-4 adalah norma. Bukan begitu. Mengakui di mana perusahaan Anda sebenarnya berada membuat peta jalan menjadi dapat dikelola.

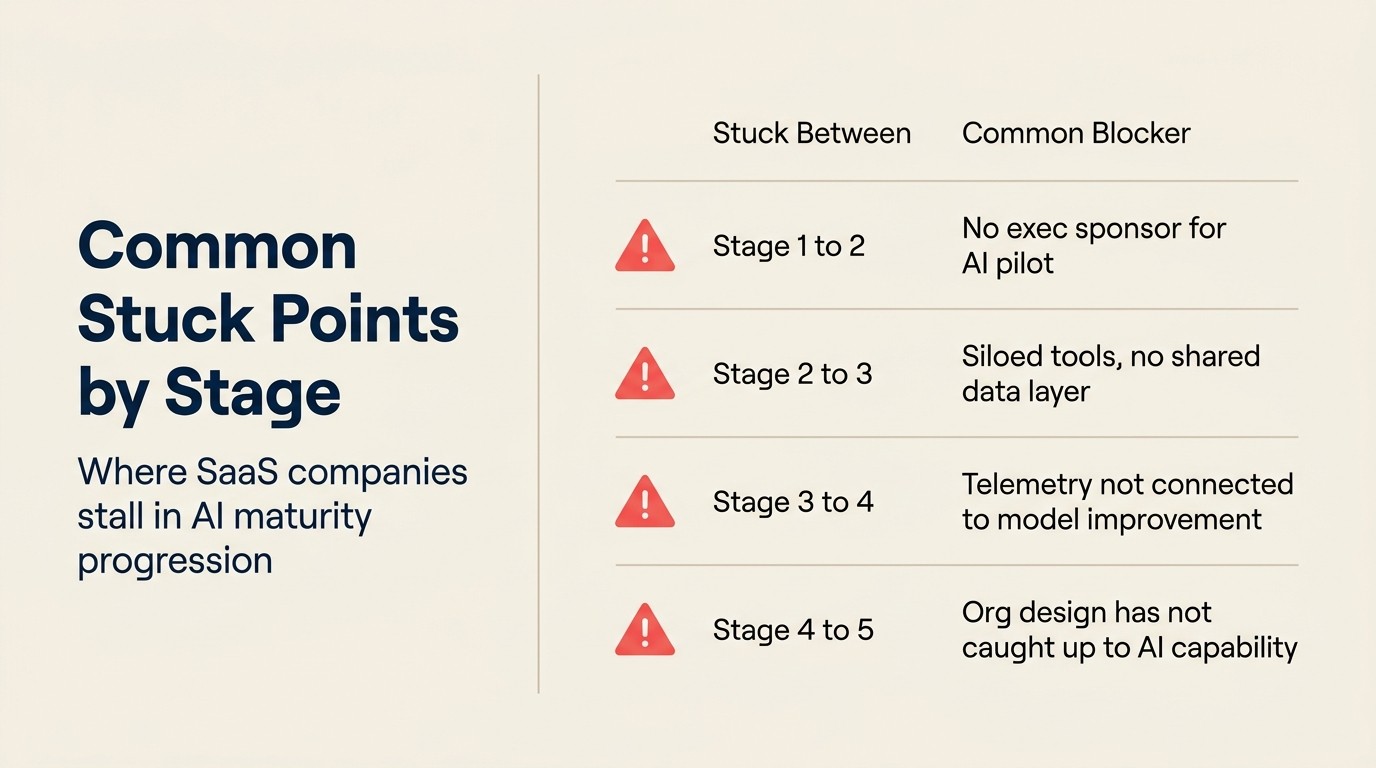

Titik macet umum antar tahap

Kemacetan Tahap 1 ke 2: Tidak ada yang memiliki AI. Antusiasme tanpa akuntabilitas tidak menghasilkan pilot. Perusahaan bersikap positif tentang AI tetapi tidak ada yang memiliki pekerjaan yang mencakup "jalankan pilot AI terstruktur dengan hasil yang terukur." Solusi: tetapkan pemilik. Tidak perlu menjadi peran AI yang berdedikasi. Ini perlu menjadi OKR eksplisit seseorang selama satu kuartal.

Kemacetan Tahap 2 ke 3: Pilot tidak dapat diskalakan. Pilot berhasil dengan satu champion yang mengelolanya. Ketika champion mencoba memperluas ke tim penuh, adopsi turun karena workflow tidak tertanam cukup dalam dan pelatihan tidak dirancang untuk peluncuran luas. Solusi: perlakukan scaling sebagai masalah produk, bukan hanya masalah ops. Alat AI perlu berada di dalam workflow, bukan di sampingnya.

Kemacetan Tahap 3 ke 4: Infrastruktur data tidak dibangun. Fungsi-fungsinya menggunakan AI secara independen. Menghubungkannya membutuhkan pekerjaan rekayasa yang tim produk dan rekayasa terus deprioritaskan demi fitur yang menghadap pelanggan. Solusi: framing investasi infrastruktur data sebagai proyek pendapatan, bukan proyek tooling. Sinyal ekspansi dari AI CS memiliki nilai dolar. Menghubungkannya ke penargetan sales memiliki dampak pipeline yang terukur.

Cara menggunakan model ini

Pertanyaan penilaian diri untuk setiap tahap:

- Pemeriksaan Tahap 1: Apakah perusahaan memiliki alat AI apa pun dengan akun di seluruh perusahaan dan kebijakan penggunaan yang ditentukan? Jika tidak, Anda berada di Tahap 1.

- Pemeriksaan Tahap 2: Apakah ada satu AI agent dalam produksi di satu fungsi, dengan hasil terukur yang ditinjau kepemimpinan setiap bulan? Jika tidak, Anda belum meninggalkan Tahap 1.

- Pemeriksaan Tahap 3: Apakah fungsi yang dibantu AI berkinerja lebih baik secara terukur daripada baseline sebelum AI mereka? Jika data tidak ada untuk menjawab ini, Anda belum diskalakan.

- Pemeriksaan Tahap 4: Apakah dua atau lebih AI agent berbagi data atau sinyal secara real time? Jika mereka adalah alat yang terisolasi, Anda berada di Tahap 3 paling banyak.

- Pemeriksaan Tahap 5: Apakah rasio revenue-per-FTE atau headcount-terhadap-ARR Anda terukur berbeda dari baseline sebelum AI Anda? Jika tidak, AI belum mengubah model operasional.

Sebagian besar tim SaaS dapat berpindah dari Tahap 1 ke Tahap 3 dalam 18 bulan dengan urutan yang tepat. Jalurnya tidak secara teknis kompleks. Ini membutuhkan keputusan di setiap tahap tentang apa yang diukur dan siapa yang memilikinya. Kerangka pengukuran AI McKinsey memvalidasi kemajuan ini: fase kematangan awal berfokus pada kinerja teknis dan adopsi, kemudian beralih ke dampak operasional, outcome strategis, dan akhirnya kinerja keuangan, yang merupakan busur yang sama yang digambarkan oleh lima tahap ini.

Model kematangan tidak ada untuk membuat perusahaan Anda terlihat tertinggal. Ini ada untuk memberi tahu Anda satu hal yang harus dilakukan selanjutnya.

"Adopsi AI enterprise melonjak ke 88% pada 2025, tetapi hanya 28% enterprise yang menggambarkan adopsi AI mereka sebagai 'matang' dengan AI tertanam di berbagai fungsi bisnis. Kesenjangan antara 'menggunakan alat AI' dan 'menerapkan AI secara matang' adalah tempat kebanyakan perusahaan SaaS sebenarnya berada. Jumlah alat bukan kematangan. Pengukuran outcome adalah kematangan." (Deloitte/Medha Cloud, 2026)

Rework Analysis: Pertumbuhan 60% kesenjangan kematangan antara pemimpin AI dan yang tertinggal selama tiga tahun tidak dijelaskan oleh akses teknologi. Pemimpin dan yang tertinggal memiliki akses ke API LLM (large language model) yang sama, alat vendor yang sama, dan anggaran yang kurang lebih proporsional. Kesenjangan ini dijelaskan oleh siapa yang memiliki outcome AI, seberapa sering outcome tersebut ditinjau, dan apakah aliran data AI lintas fungsi dibangun atau ditangguhkan. Tim di Tahap 3 yang belum membangun infrastruktur data untuk Tahap 4 tidak ketinggalan dalam teknologi. Mereka ketinggalan dalam desain organisasi. Teknologi untuk Tahap 4 tersedia. Keputusan organisasi untuk membangun lapisan data yang menghubungkan AI CS ke AI sales adalah apa yang terus ditangguhkan oleh sebagian besar tim Tahap 3.

"Enterprise menghadapi tingkat kegagalan pilot 60-70% dalam implementasi AI, tetapi kegagalannya tidak merata di seluruh tahap. Sebagian besar kegagalan terjadi pada transisi Tahap 2 ke Tahap 3, ketika champion pilot mencoba memperluas ke tim penuh dan menemukan bahwa workflow tidak tertanam cukup dalam untuk peluncuran luas. Solusinya adalah memperlakukan scaling sebagai masalah produk, bukan masalah ops." (Rework Analysis, berdasarkan penelitian MIT dan Gartner, 2025)

Pertanyaan yang Sering Diajukan

Apa itu The SaaS 5-Stage AI Curve?

Model kematangan diagnostik yang memetakan perusahaan SaaS ke lima tahap operasional berdasarkan seberapa dalam AI tertanam dalam workflow yang menghasilkan pendapatan. Tahap 1 adalah penggunaan alat individual secara ad-hoc. Tahap 2 adalah satu pilot terstruktur dengan pemilik dan metrik yang ditentukan. Tahap 3 adalah fungsi yang dibantu AI terukur melampaui baseline. Tahap 4 adalah AI agent di berbagai fungsi berbagi data dan sinyal secara real time. Tahap 5 adalah AI mengubah model operasional itu sendiri, dengan rasio headcount-terhadap-ARR yang berbeda dari baseline sebelum AI.

Di mana sebagian besar perusahaan SaaS berada dalam kurva kematangan di 2026?

Distribusi jujurnya: sekitar 60-70% perusahaan dengan ARR di bawah $5M berada di Tahap 1 (alat ad-hoc, tanpa strategi). Sebagian besar perusahaan Series A yang didanai dan awal Series B berada di Tahap 2 (satu pilot terstruktur). Tahap 3 adalah perusahaan Series B akhir dan Series C dengan budaya AI ops yang fungsional. Tahap 4 jarang dan membutuhkan investasi data engineering yang ditangguhkan oleh kebanyakan perusahaan. Tahap 5 adalah sejumlah kecil perusahaan yang didanai dengan baik, AI-native atau AI-forward. Kebisingan industri menciptakan kesan palsu bahwa Tahap 3-4 adalah norma.

Apa cara tercepat untuk berpindah dari Tahap 1 ke Tahap 2?

Tetapkan pemilik. Bukan peran AI yang berdedikasi, hanya seseorang yang OKR eksplisitnya selama satu kuartal mencakup menjalankan pilot AI terstruktur dengan hasil yang terukur. Kemacetan Tahap 1 ke 2 hampir selalu merupakan kesenjangan akuntabilitas, bukan kesenjangan kemampuan. Satu pilot, satu metrik, satu timeline 90 hari, satu orang yang bertanggung jawab. Tanpa itu, antusiasme tanpa akuntabilitas tetap berada di Tahap 1 tanpa batas waktu.

Apa yang menyebabkan kemacetan Tahap 2 ke Tahap 3?

Keberhasilan pilot diikuti oleh kegagalan scaling. Pilot berhasil dengan satu champion yang mengelolanya. Ketika champion mencoba memperluas ke tim penuh, adopsi turun karena alat AI berada di samping workflow daripada tertanam di dalamnya. Solusinya adalah memperlakukan scaling sebagai masalah produk: alat AI perlu berada di dalam workflow sebelum memperluas, bukan di sebelahnya.

Infrastruktur apa yang diperlukan untuk Tahap 4?

Koneksi data antara AI agent di berbagai fungsi. Health score AI CS perlu menginformasikan penargetan ekspansi AI sales. AI analisis sales call perlu memunculkan sinyal dalam tampilan akun CS. Ini membutuhkan lapisan data (biasanya data warehouse atau CDP) yang menghubungkan alat yang sebelumnya terisolasi. Sebagian besar perusahaan Tahap 3 memiliki alat AI. Mereka kehilangan koneksi datanya. Engineering terus mendeprioritaskan infrastruktur demi fitur yang menghadap pelanggan, yang merupakan penundaan Tahap 3-ke-4 yang paling umum.

Seperti apa Tahap 5 secara operasional?

Perbedaan struktural dalam model P&L dan headcount dibandingkan dengan baseline sebelum AI. Support pelanggan tidak skala secara linear dengan pelanggan karena AI menangani 60-70% tiket. Output marketing tidak skala dengan headcount karena AI menghasilkan dan menguji konten. Revenue-per-FTE terukur lebih tinggi dari baseline sebelum AI. Jasper (AI adalah produknya) dan HubSpot (AI meningkatkan semua fungsi dan tertanam secara mendalam dalam produk) adalah contoh paling jelas.

Apa kegagalan tata kelola yang paling umum di Tahap 4?

Membangun infrastruktur data tanpa tata kelola data. Ketika AI agent berbagi sinyal lintas fungsi, kesalahan merambat lebih cepat. Algoritma health score yang salah dikalibrasi tidak hanya merusak outcome CS. Ini mengkorupsi data ekspansi sales dan perkiraan churn keuangan. Audit kualitas data dan tinjauan kinerja model menjadi persyaratan operasional di Tahap 4, bukan overhead tata kelola opsional.

Berapa lama waktu yang dibutuhkan untuk berpindah dari Tahap 1 ke Tahap 3?

Sebagian besar tim SaaS dapat berpindah dari Tahap 1 ke Tahap 3 dalam 18 bulan dengan urutan yang tepat. Tahap 1 ke 2 membutuhkan 6-12 bulan dengan pemilik terfokus dan satu pilot terukur. Tahap 2 ke 3 membutuhkan 6-12 bulan lagi setelah pilot berhasil dan tantangan scaling diperlakukan sebagai masalah desain produk daripada peluncuran ops. Jalurnya tidak secara teknis kompleks. Ini membutuhkan keputusan di setiap tahap tentang apa yang diukur dan siapa yang memilikinya.

Pelajari Lebih Lanjut:

- 5 Tahap Kematangan AI: kerangka kematangan tingkat strategi di semua industri

- Tahap 1 ke 2: Ad-Hoc ke Pilot: kerangka keputusan transisi

- Tahap 2 ke 3: Pilot ke Scaled: memperluas dari pilot yang berhasil ke deployment tim penuh

- Tahap 3 ke 4: Scaled ke Integrated: keputusan infrastruktur data untuk AI lintas fungsi

- Tahap 5: Ketika AI Membentuk Ulang Produk Anda: apa yang dibutuhkan transformasi struktural dari kepemimpinan

- AI Risk Register: Apa yang Perlu Dilacak: tata kelola untuk sistem AI lintas fungsi Tahap 4

- ACE Framework: kosakata yang mendasari semua lima tahap kematangan

- Beli vs. Bangun untuk Fitur AI SaaS: kerangka keputusan Tahap 2-3 untuk setiap kapabilitas

- Bagaimana AI Membentuk Ulang Model Operasional SaaS: seperti apa Tahap 4-5 dalam struktur org dan P&L

Co-Founder, Rework.com