La Pregunta sobre el Modelo de Precios de IA para SaaS

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

Toda empresa SaaS con funcionalidades de IA eventualmente enfrenta la misma pregunta: ¿incluirla en el plan base, ponerla detrás de un nivel premium o cobrar por consumo?

No existe una respuesta universalmente correcta. Pero la respuesta incorrecta es costosa, y más empresas lo han descubierto de la manera difícil después de lanzar y fijar precios a funcionalidades de IA.

Este artículo es para fundadores y líderes de ingresos que están trabajando activamente en esta decisión. No una encuesta de proveedores. Un framework para razonar sobre las compensaciones dada su producto, mercado y estructura de costos específicos.

Los Tres Modelos de Precios para IA en SaaS

Los patrones que han emergido en el mercado se dividen en tres modelos distintos, cada uno con una lógica central diferente.

Modelo 1: Incluido en los niveles existentes. La IA está incluida en el plan base o nivel estándar. Los usuarios no pagan más para acceder a ella. La apuesta es que la IA impulsa el engagement y la retención, lo que protege los ingresos a través de un menor churn incluso si no aumenta el ARPU directamente.

Modelo 2: Nivel premium o complemento. La IA está disponible a un precio más alto, ya sea como un complemento separado o como una funcionalidad diferenciadora de un nivel superior. La apuesta es que la IA entrega suficiente valor demostrado como para que los usuarios paguen más por ella, o que la IA desbloquea una nueva persona compradora dispuesta a pagar en un punto de precio diferente.

Modelo 3: Precios basados en uso o consumo. El acceso a la IA se cobra por uso, ya sea medido en llamadas de API, tokens generados, consultas ejecutadas u outputs producidos. La apuesta es que el valor de la IA se correlaciona con el uso, por lo que los clientes que obtienen más valor pagan más.

Cada modelo es internamente consistente. Cada uno tiene situaciones donde es claramente la elección correcta y situaciones donde fracasa.

Key Facts: Modelos de Precios de IA en SaaS

- El 68% de los proveedores de SaaS restringió las funcionalidades de IA a niveles premium en 2025, mientras que el 37% planeaba ajustes de precios dentro de los 12 meses a medida que la presión competitiva se construía hacia la inclusión (Getmonetizely, 2025)

- Para 2025, el 85% de los líderes de SaaS habían adoptado modelos de precios basados en uso o híbridos, con el 61% usando precios híbridos que combinan una suscripción base con componentes de IA basados en uso (Flexera, 2025)

- El 78% de los líderes de TI experimentaron cargos inesperados en una factura de SaaS debido a modelos de precios de consumo o IA, destacando el problema de pronóstico con los paquetes de IA de precio fijo (Zylo, 2025)

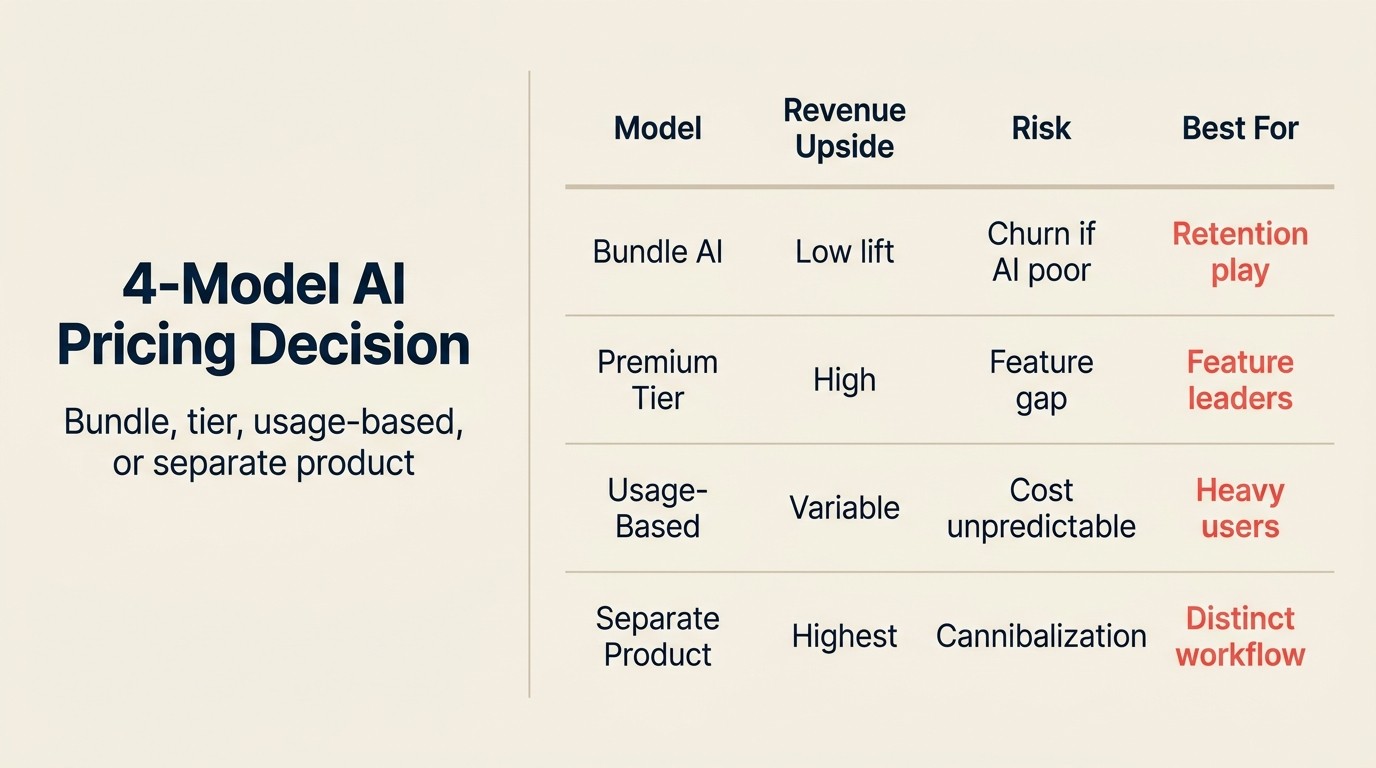

La Decisión de Precios de IA en 4 Modelos

La Decisión de Precios de IA en 4 Modelos es un framework de evaluación secuencial que mapea la funcionalidad de IA de cada empresa SaaS a una de cuatro estructuras de precios. Bundled: la IA está incluida en todos los niveles pagados; optimiza para la adopción y la retención en lugar del ARPU. Add-on: la IA es un módulo con precio separado; apropiado cuando la IA entrega una capacidad demostrablemente diferente del producto base. Usage-based: la IA se cobra por consumo (tokens, consultas, outputs); mejor para herramientas para desarrolladores y productos de API donde el valor se correlaciona con el volumen de uso. AI-tier: un nuevo nivel de precios definido por el techo de capacidad de IA en lugar del conteo de asientos; defendible cuando el nivel de IA permite resultados mediblemente diferentes, no solo una ejecución más rápida. La secuencia de decisión es: viabilidad de adopción, luego impacto en la retención, luego estructura de costos, luego contexto competitivo.

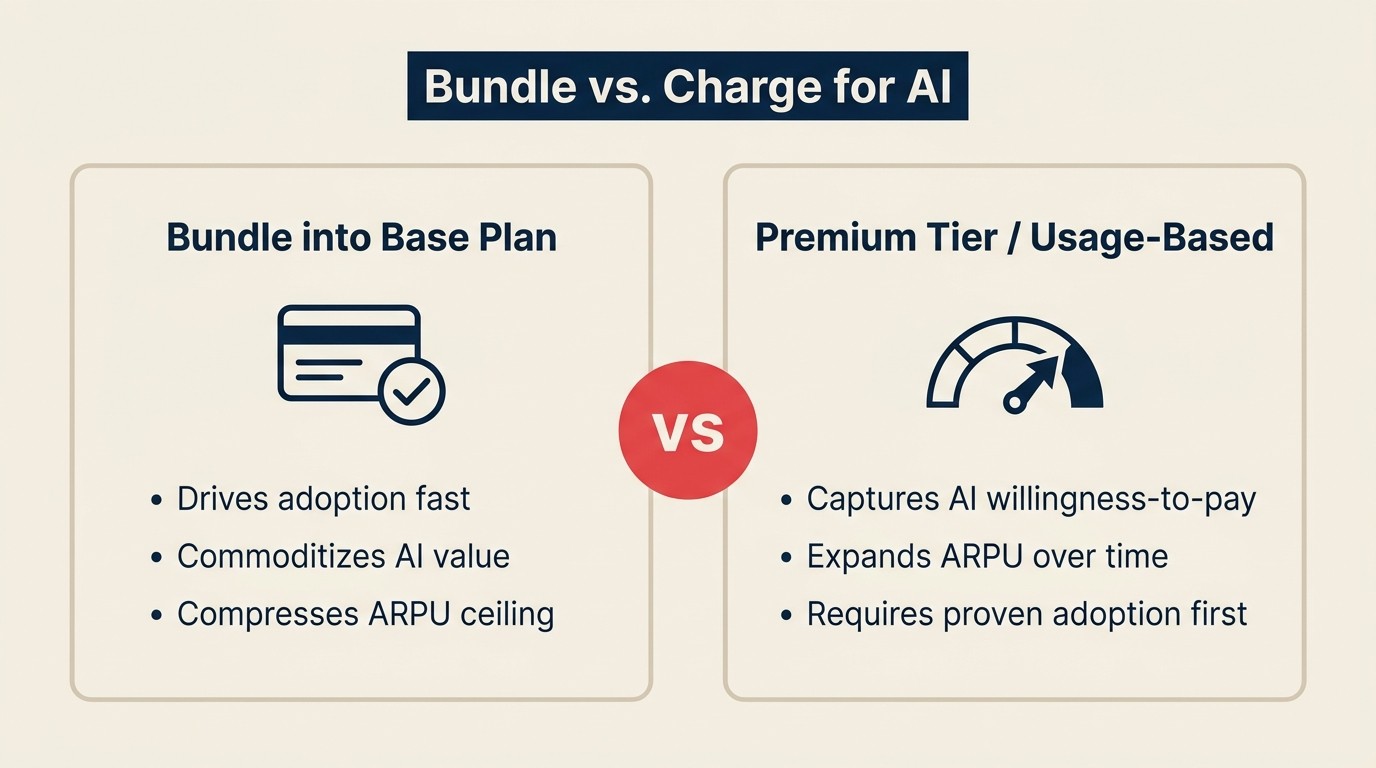

Incluir la IA en el Precio: El Argumento de la Retención

Lo más importante que hay que entender sobre incluir la IA en el precio es que es principalmente una decisión de retención, no de ingresos.

Cuando la IA está incluida en el nivel base, suceden dos cosas. Primero, cada usuario encuentra la funcionalidad de IA en su workflow normal. La adopción es alta por defecto porque no hay fricción, no hay decisión de actualización, no hay ciclo de onboarding separado. Segundo, a medida que los usuarios construyen hábitos alrededor de la funcionalidad de IA, el producto se vuelve más adherente. El churn disminuye porque alejarse de su producto significa renunciar a un workflow de IA que está integrado en cómo trabajan.

El enfoque de Notion ilustra esto. Cuando se lanzó Notion AI, tenía un precio como complemento separado a $8 por usuario por mes. La adopción fue moderada. En 2024, Notion pasó a incluir IA en todos los planes pagados. La adopción aumentó notablemente. Más importante aún, los usuarios que usan Notion AI como parte de su workflow diario de escritura tienen significativamente menos probabilidades de producir churn. La IA se convirtió en un activo de retención, no solo en una línea de ingresos.

Figma tomó un camino similar. Las capacidades de IA se integraron en la experiencia del producto en lugar de estar bloqueadas. El resultado es que la IA no es algo en lo que los usuarios de Figma piensen en comprar. Es simplemente parte de usar Figma.

El caso para incluir la IA en el precio es más fuerte cuando: su funcionalidad de IA está integrada en un workflow de alta frecuencia, sus competidores se están moviendo hacia la inclusión (haciendo que el bloqueo premium sea una desventaja competitiva) y su principal riesgo es el churn en lugar del ARPU. Funcionalidades de IA como producto: dónde añadirlas explica cómo identificar los puntos de inserción de alta frecuencia que hacen que la inclusión sea defendible.

El riesgo de incluirla en el precio es que los costos de API de LLM son reales y escalan con el uso. Si su funcionalidad de IA obtiene alta adopción y su costo por usuario activo sube $5 por mes pero su ARPU no cambia, ha comprimido su margen. La decisión de incluirla en el precio requiere un modelo de costo cuidadoso antes de comprometerse. ¿Cuánto margen tiene antes de que los números no cuadren?

Nivel Premium: El Argumento de los Ingresos

Los precios premium de IA son defendibles cuando la funcionalidad de IA entrega resultados demostrablemente diferentes, no solo una ejecución más rápida del mismo workflow.

GitHub Copilot es el ejemplo más claro. El nivel individual a $10 por usuario por mes es el punto de entrada estándar. GitHub Copilot Enterprise, a $39 por usuario por mes, añade funcionalidades como ajuste de modelos personalizados en su base de código, controles de políticas para empresas e integración más profunda con las funcionalidades empresariales de GitHub. El precio más alto está justificado por una persona compradora diferente (empresa con requisitos de seguridad) y un conjunto de capacidades demostrablemente diferente (contexto específico de la base de código, no solo completación de código general).

Ese es el modelo que funciona para los precios premium de IA. Hay un salto de capacidad entre niveles, no solo una etiqueta.

El modelo premium falla cuando se usa para bloquear funcionalidades que deberían estar en el plan base. Si su funcionalidad de IA es genuinamente un acelerador del workflow para tareas diarias, ponerla detrás de un premium fuerza una decisión que la mayoría de los usuarios no tomarán. No actualizan. Solo trabajan sin la IA, y el hábito nunca se forma. Cuando están evaluando la renovación, la funcionalidad de IA nunca fue parte de su experiencia diaria, por lo que no se registra como razón para quedarse.

HubSpot aprendió una versión de esta lección. Las iteraciones anteriores de las funcionalidades de IA de HubSpot estaban bloqueadas detrás de niveles Enterprise más altos. Los datos de adopción mostraron que los usuarios que nunca encontraron las funcionalidades tenían menos probabilidades de expandir. Las decisiones de producto más recientes de HubSpot se han movido hacia hacer que la IA sea fundamental en todos los niveles, con IA avanzada para casos de uso más complejos en niveles superiores. La lógica de niveles cambió de "pagar para acceder a la IA" a "pagar por IA más sofisticada".

Salesforce Einstein Copilot tiene un precio de $50 por usuario por mes además de las licencias de Salesforce existentes. Ese es un costo adicional significativo para los grandes usuarios empresariales. Salesforce puede mantener ese precio porque: los compradores empresariales están acostumbrados al alto gasto en Salesforce, las funcionalidades están genuinamente diferenciadas del Einstein Analytics estándar, y la persona compradora (operaciones de ventas empresariales) tiene métricas claras de ROI a las que señalar.

Los precios premium de IA funcionan cuando puede responder "¿qué resultado permite el nivel de IA que el nivel base no puede, y cuál es el valor en dólares de ese resultado?" Si no puede responder eso claramente, el nivel de precios tendrá dificultades. 5 Dimensiones del ROI de IA proporciona el framework para cuantificar lo que un nivel de IA realmente entrega en resultados de negocio medibles.

Basado en Uso: El Argumento de la Alineación de Valor

Los precios de IA basados en uso alinean el precio con el valor entregado, al menos en teoría.

Stripe Sigma cobra por la ejecución de consultas. Los precios de la API de OpenAI cobran por token. Las funcionalidades de Salesforce Einstein tienen componentes basados en uso para predicciones y generaciones de IA. La lógica es clara: los clientes que ejecutan más consultas, generan más outputs o toman más decisiones asistidas por IA presumiblemente obtienen más valor, por lo que pagan más.

Los desafíos prácticos son reales.

Primero, el uso es difícil de predecir. Los compradores empresariales en particular no les gustan los costos variables difíciles de presupuestar. Un compromiso anual fijo es más fácil de aprobar que una factura mensual que depende de cuánto use su equipo la IA. Los precios basados en uso pueden ralentizar los ciclos de negociación empresarial y aumentar la frecuencia de conversaciones sobre gestión de costos.

Segundo, la correlación entre uso y valor no siempre es estrecha. Un equipo que ejecuta cincuenta consultas de IA por mes y toma una decisión de alta calidad a partir del output puede obtener más valor que un equipo que ejecuta quinientas consultas y trata los outputs como ruido. El uso no mide los resultados.

Tercero, los precios basados en uso crean una dinámica de comportamiento donde los usuarios piensan antes de usar la IA, lo cual es lo contrario de lo que se quiere para la formación de hábitos. La carga cognitiva de "¿vale la pena ejecutar esta consulta?" reduce la adopción al margen.

Los precios basados en uso funcionan mejor para herramientas de desarrolladores y productos de API donde el comprador es técnico, está cómodo con la facturación variable y tiene un modelo de consumo claro con el que trabajar. Es más difícil para los productos SaaS horizontales donde los usuarios finales no piensan en términos de llamadas de API. El análisis de a16z sobre modelos de precios de IA encuentra exactamente esta división: los productos de API nativos de IA se inclinan hacia el uso basado, mientras que los productos SaaS orientados a humanos tienden a retener estructuras de suscripción o incluidas porque la facturación basada en uso crea fricción cognitiva que suprime la adopción.

Dinámicas Competitivas

Sus precios no se establecen de forma aislada. Se establecen en un mercado.

Si sus tres principales competidores han incluido la IA en sus planes base, no puede bloquearla de forma premium eficazmente sin perder pruebas. Un prospecto que evalúa cuatro opciones de CRM donde tres incluyen IA y la suya cuesta $X más por usuario por mes para la IA elegirá consistentemente una de las tres. No porque su IA sea peor. Porque la contabilidad mental de "costo adicional por algo que la competencia incluye" crea fricción en la etapa de comparación.

Por el contrario, si nadie en su mercado ha incluido la IA todavía y los clientes están acostumbrados a pensar en la IA como un complemento, los precios premium tempranos pueden funcionar. Está capturando ingresos de los primeros adoptadores que valoran mucho la funcionalidad antes de que la norma del mercado cambie hacia la inclusión.

La dinámica competitiva que la mayoría de las empresas SaaS están subestimando en este momento: el cambio de la IA como una funcionalidad premium a la IA como una expectativa de base está ocurriendo más rápido de lo que los equipos de precios se están ajustando. Lo que justificaba un nivel premium en 2023 es una expectativa incluida en 2026. La ventana para los precios premium de IA en la mayoría de las categorías de SaaS horizontal se está reduciendo. La investigación de OpenView sobre precios basados en uso muestra que el 38% de las empresas SaaS ahora usan alguna forma de precios basados en uso, frente al 27% en 2023, y que las empresas públicas basadas en uso superan al índice SaaS más amplio en NRR, lo que sugiere que la presión competitiva sobre las estructuras de precios está aumentando en toda la categoría. La carrera armamentista de IA en SaaS documenta cómo la presión competitiva está comprimiendo estas ventanas de precios.

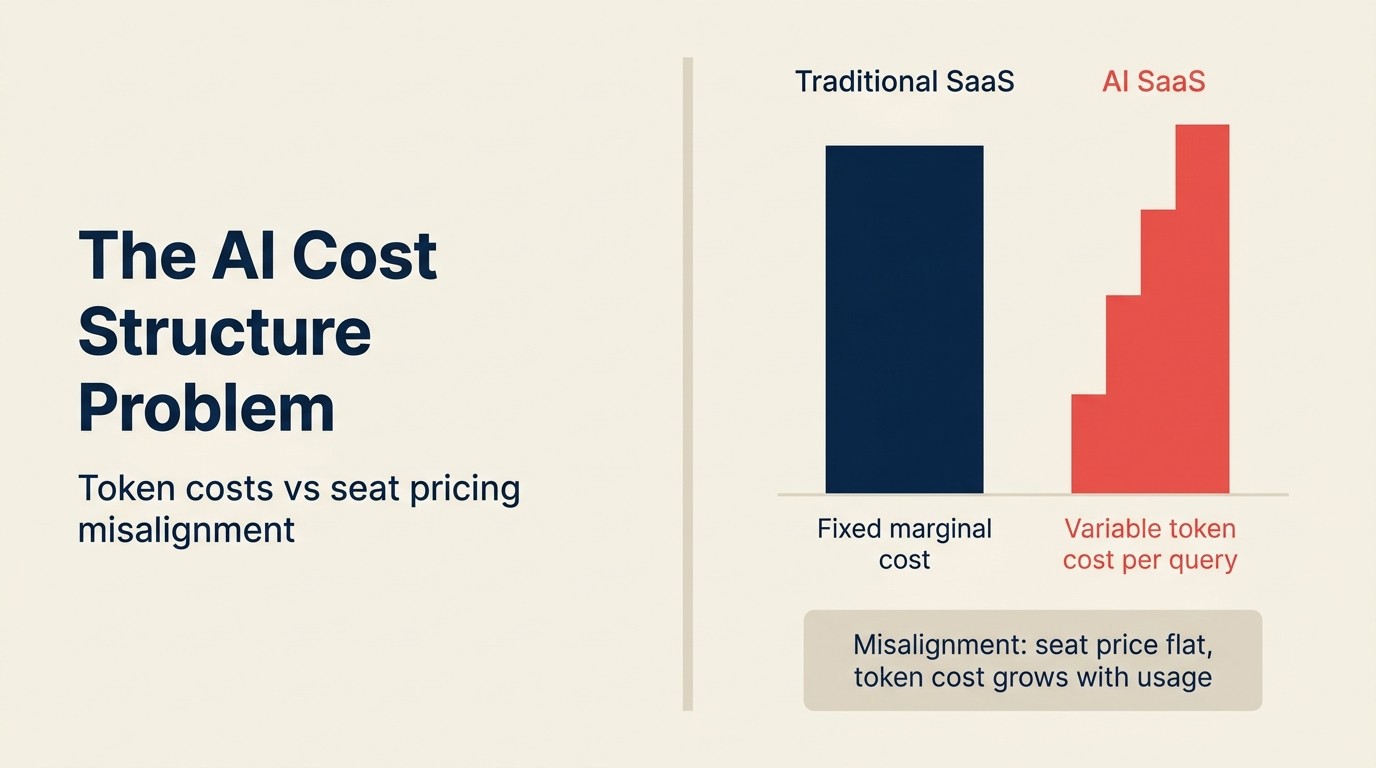

El Problema de la Estructura de Costos

Los costos de API de LLM son reales y no son fijos.

Una llamada de API típica de clase GPT-4 cuesta aproximadamente $0.01 a $0.05 dependiendo de la longitud de entrada/salida y el modelo específico. Si su funcionalidad de IA sirve a 10,000 usuarios activos y cada usuario realiza 20 acciones asistidas por IA por mes, está ejecutando 200,000 llamadas de API por mes. A un promedio de $0.02, eso son $4,000 por mes en costos de infraestructura de LLM, o aproximadamente $0.40 por usuario activo por mes.

Para la mayoría de los productos SaaS, eso es absorbible. Pero escala con el uso activo, no con los asientos. Si vende 10,000 asientos pero solo 2,000 están activos, los 2,000 usuarios activos impulsan sus costos. Si la adopción mejora a 8,000 usuarios activos, sus costos se cuadruplican, pero sus ingresos podrían no cambiar si la IA está incluida en el precio.

Antes de comprometerse con un modelo de precios de IA incluido, necesita una proyección de costos realista:

- ¿Cuál es el costo estimado de la API de IA por usuario activo por mes con los patrones de uso actuales?

- ¿Cuál es el costo proyectado con el doble de adopción y cinco veces más adopción?

- ¿Los precios de IA incluidos siguen funcionando a esos niveles de adopción?

Las empresas que se equivocan en esto son las que lanzan IA incluida con bajos niveles de adopción donde los costos son insignificantes, y luego se encuentran comprimiendo el margen seis meses después cuando la funcionalidad despega.

Algunas empresas SaaS abordan esto con límites de uso suaves: "Funcionalidades de IA incluidas, uso razonable, uso a nivel empresarial a petición." Esto es pragmático pero crea ambigüedad que los clientes notan.

La Pregunta sobre la Canibalización

Algunas empresas SaaS temen que sus funcionalidades de IA automaticen el valor por el que actualmente cobran por asiento.

Este miedo es más agudo en productos donde la propuesta de valor es en parte "darle a cada usuario su propio workspace". Si la IA puede hacer el trabajo de cinco usuarios, ¿por qué está pagando por cinco asientos?

La respuesta honesta es que este riesgo de canibalización es real en algunos productos y mínimo en otros. Para los productos donde el valor principal es la colaboración y el contexto compartido entre humanos, la IA aumenta el workflow en lugar de reemplazar a los humanos. Para los productos donde el valor principal es la ejecución de tareas individuales, el riesgo es mayor.

La estrategia defensiva no es evitar construir IA. Es asegurarse de que sus funcionalidades de IA fortalezcan el caso de uso de colaboración en lugar de permitir que los usuarios individuales hagan más con menos asientos. Las funcionalidades que presentan información en todo el equipo, apoyan las transferencias y mejoran la coordinación son tanto más defendibles estratégicamente como más difíciles de reemplazar con herramientas de IA independientes.

"Los precios premium de IA son defendibles cuando puede responder la pregunta: ¿qué resultado permite el nivel de IA que el nivel base no puede, y cuál es el valor en dólares de ese resultado? Si no puede responder eso claramente, el nivel de precios tendrá dificultades. La inclusión es defendible cuando el impacto de retención de IA es real y los competidores se están moviendo hacia la inclusión." (Rework Analysis, 2025)

"La economía conductual de los precios de IA basados en uso crea una dinámica donde los usuarios piensan antes de usar la IA, lo cual es lo contrario de lo que se quiere para la formación de hábitos. Los precios fijos eliminan la carga cognitiva. Los precios de uso la vuelven a añadir. Para el SaaS horizontal con usuarios finales humanos, esa carga suprime la adopción al margen." (Rework Analysis, basado en la investigación de precios de IA de a16z, 2025)

Comparación de Modelos de Precios de IA

| Modelo de Precios | Mejor Ajuste | Riesgo | Perfil de Ingresos |

|---|---|---|---|

| Incluido (en todos los niveles) | IA de alta frecuencia con impacto medible en retención | Compresión de costos de LLM a medida que escala la adopción | Protege el NRR; sin aumento directo del ARPU |

| Add-on | IA que entrega capacidad claramente diferenciada | Baja adopción si los usuarios base no actualizan | Aumento del ARPU de los usuarios convertidos |

| Basado en uso | Herramientas para desarrolladores, productos de API, compradores técnicos | Costos impredecibles; suprime la adopción en SaaS orientado a humanos | Variable; alinea el precio con el valor |

| Nivel de IA (definido por capacidad) | Compradores empresariales con métricas claras de ROI | Requiere una brecha de resultado demostrable frente al nivel base | ARR premium del segmento empresarial |

Fuentes: Bessemer Venture Partners AI Monetization Playbook 2025, a16z AI Pricing Models Research 2025, Getmonetizely Pricing Guide 2026

Rework Analysis: La ventana para bloquear la IA de forma premium en el SaaS de mercado medio se está reduciendo. Lo que justificaba un complemento de IA separado en 2023 es una expectativa incluida en 2026. Los equipos que fijan precios a la IA como complemento en categorías donde los tres principales competidores han incluido deben modelar la brecha de conversión de prueba a pagado frente a la ganancia de ARPU de las conversiones de complemento. Si la inclusión reduce el churn en 5 puntos porcentuales, los números del NRR típicamente superan a los precios de complemento a menos que la conversión del complemento supere el 35%. La adopción de complementos de SaaS horizontal cae muy por debajo de ese umbral.

Lo que el Mercado de 2025-2026 nos Dice

Mirando las principales plataformas SaaS, está emergiendo un patrón.

Linear incluye funcionalidades de IA en todos los planes pagados. Sin nivel de IA separado. La apuesta es que la creación de issues asistida por IA y los resúmenes son fundamentales para el workflow diario del desarrollador.

Notion pasó de complemento a incluido. Los datos de uso impulsaron la decisión.

GitHub Copilot mantiene un modelo por niveles con una diferenciación de capacidad clara entre Individual y Enterprise. Los niveles están justificados por diferencias de resultado demostradas.

HubSpot está moviendo la IA más profundamente en el producto en todos los niveles, con IA más sofisticada reservada para niveles superiores, pero IA básica ampliamente disponible.

Zendesk incluye funcionalidades de IA en todos los niveles con límites de uso; volumen premium de agentes de IA disponible en niveles superiores.

Salesforce mantiene precios premium de IA en el nivel Enterprise donde el comprador tiene alta disposición a pagar y métricas claras de ROI.

Rework incluye las capacidades de IA como parte de los niveles del producto en lugar de bloquearlas por separado, manteniendo el precio sencillo en torno a los paquetes Starter y Standard. Esto se adapta al caso de uso orientado al equipo donde el valor compuesto de la IA proviene del contexto compartido entre usuarios.

El patrón: la IA se está moviendo hacia una expectativa de base en todo el SaaS de mercado medio. Los precios premium de IA se mantienen principalmente en el nivel empresarial donde la diferenciación de capacidad es genuina y el comprador está acostumbrado a los precios de complemento.

El Framework de Decisión

No existe una respuesta universal sobre precios de IA. Pero aquí está la secuencia analítica:

Empiece con la adopción. Si la adopción de IA es baja, la pregunta no es el precio. Es el punto de inserción. Las funcionalidades de IA con baja adopción no justifican los precios premium y no benefician la retención independientemente de cómo se fijen los precios.

Luego el impacto en la retención. ¿La funcionalidad de IA, cuando se usa, se correlaciona con un menor churn? Si es así, la inclusión protege ese valor. Si la correlación es débil, los precios premium son más defendibles porque no está dejando una palanca de retención sobre la mesa.

Luego la estructura de costos. A los niveles proyectados de adopción de IA, ¿cuál es el costo por usuario activo por mes? ¿Puede absorber eso en los márgenes del plan actual, o los números requieren precios basados en uso o un nivel premium para seguir siendo viable?

Luego el contexto competitivo. ¿Cuál es la expectativa del mercado? Si los competidores están incluyendo, necesita un argumento sólido de por qué los clientes pagarán extra por el suyo.

Trabaje honestamente esas cuatro preguntas y el modelo de precios generalmente se vuelve claro. Las empresas que saltan directamente a "¿qué pagarán los clientes por esto?" a menudo terminan con una estructura de precios que funciona a corto plazo y crea problemas cuando las dinámicas competitivas cambian. a16z señala que la IA está ahora impulsando un cambio hacia los precios basados en resultados a medida que las empresas nativas de IA como Decagon comienzan a fijar precios por resolución en lugar de por asiento, lo que sugiere que está emergiendo un cuarto modelo de precios más allá de los tres cubiertos aquí, uno que eventualmente presionará más directamente los niveles tradicionales de SaaS.

Leer Más:

- 5 Dimensiones del ROI de IA: cuantificando el valor del nivel de IA en términos que aceptarán compradores y directorios

- Funcionalidades de IA como Producto: Dónde Añadirlas: encontrando los puntos de inserción de alta frecuencia que justifican la inclusión

- La Carrera Armamentista de IA en SaaS: Velocidad de Lanzamiento: cómo la presión competitiva comprime las ventanas de precios de IA

- Comprar vs. Construir Funcionalidades de IA para SaaS: la decisión de construir/comprar afecta la estructura de costos y las opciones de precios

- Cómo la IA Remodela el Modelo Operativo SaaS: contexto más amplio sobre el impacto de la IA en los modelos de negocio SaaS

Co-Founder, Rework.com

On this page

- Los Tres Modelos de Precios para IA en SaaS

- La Decisión de Precios de IA en 4 Modelos

- Incluir la IA en el Precio: El Argumento de la Retención

- Nivel Premium: El Argumento de los Ingresos

- Basado en Uso: El Argumento de la Alineación de Valor

- Dinámicas Competitivas

- El Problema de la Estructura de Costos

- La Pregunta sobre la Canibalización

- Comparación de Modelos de Precios de IA

- Lo que el Mercado de 2025-2026 nos Dice

- El Framework de Decisión