Going Private: What Executives and Boards Need to Know Before Taking a Public Company Private

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

When a publicly traded company takes itself private, the decision is rarely simple. There's a short version: the buyers think the business is worth more than the public market is pricing it, and the transaction structure lets them capture that value. But the short version leaves out most of what actually matters to the executives and board members who have to make it work.

Going-private transactions have accelerated as a strategic option for mid-market and larger public companies. The motivations range from escaping the quarterly earnings treadmill to executing a transformation that requires patient capital to correcting a valuation disconnect that public investors haven't resolved. Understanding what these transactions actually involve, and what they require of management, is essential before any serious evaluation.

Key Facts

- Going-private transactions in the US totaled over $200 billion annually in peak years, with PE-backed take-privates representing the largest share by value, according to PitchBook private equity data.

- The typical take-private premium is 25-40% above the undisturbed share price, though complex situations and competitive auction processes can push premiums higher, per Deloitte's M&A transaction research.

- Harvard Law School's Forum on Corporate Governance documents that companies taken private by PE firms typically show EBITDA margin improvements of 2-5 percentage points within 3 years of the transaction, driven primarily by cost discipline rather than revenue growth in the early years.

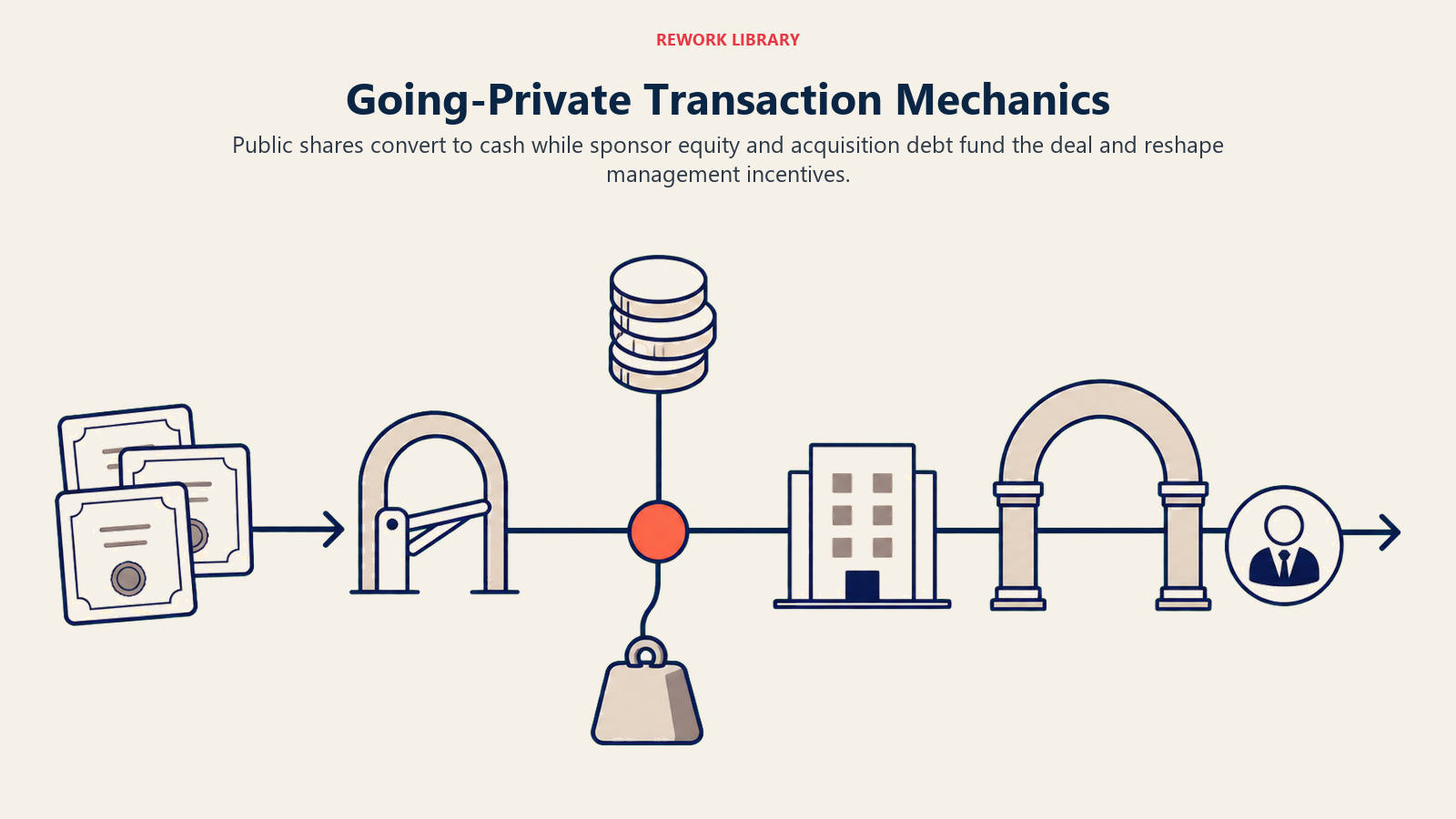

What "Going Private" Actually Means

A going-private transaction takes a publicly traded company off a stock exchange and into private ownership. The public shareholders are bought out, typically at a premium to the pre-announcement stock price. After the transaction closes, the company no longer files public financial statements, no longer has publicly traded equity, and is no longer subject to the reporting requirements, proxy rules, and scrutiny that come with public market status.

The most common forms are:

Leveraged buyout (LBO): A private equity firm (or consortium) acquires the company using a combination of equity capital and significant debt, with the debt typically placed on the acquired company's balance sheet. The acquired company's cash flows service that debt. The PE firm aims to improve the business, reduce debt, and exit (through a sale, secondary buyout, or re-IPO) in a 4-7 year timeframe.

Management buyout (MBO): The existing management team, often with private equity backing, acquires control of the company. The management team usually rolls over equity and takes on meaningful financial risk alongside the PE sponsor. The alignment between management incentives and business outcomes tends to be sharper in an MBO structure.

Take-private by a strategic acquirer: A larger company or a group of private investors acquires the public company outright, paying public shareholders and delisting the shares. This is different from a PE LBO in that the acquirer may have strategic rather than purely financial motivations.

Sponsor-to-sponsor: A PE firm that already owns a company may take it public and then take it private again, or one PE firm may acquire from another. These are secondary transactions and common in the mid-market.

Why Companies Go Private

The motivations for going-private vary by situation, but several patterns recur.

Escaping short-termism. Public markets price companies on near-term earnings and guidance. For businesses that need to invest heavily today for returns in 3-5 years, the public market structure creates a structural conflict. Management teams that would invest in a multi-year transformation instead find themselves managing to the next quarter to avoid a stock price drop that triggers activist pressure or board scrutiny. Going private removes that structural pressure, though it replaces it with PE return expectations that have their own timeline constraints.

Valuation disconnects. Sometimes public markets persistently misprice a business. This is most common when a company doesn't fit neatly into analyst coverage categories, when the business has a complex structure that obscures its underlying economics, or when the company is too small to attract institutional investor attention. If the public float is thin and trading volume is low, the market price may not reflect what a well-informed strategic or financial buyer would pay.

Transformation that requires disruption. Some businesses need to be broken down and rebuilt in ways that would be extremely difficult under public scrutiny: restructuring the cost base, exiting legacy businesses, changing pricing models, or making acquisitions that compress earnings in the short term before adding value. Private ownership provides operating space to absorb short-term pain.

Regulatory or reporting cost burden. For smaller public companies, the cost of Sarbanes-Oxley compliance, SEC reporting, investor relations, and the management attention required for quarterly calls can be disproportionate to the benefits of public market access. Going private reduces this overhead, though it doesn't eliminate governance requirements entirely.

The Mechanics of a Going-Private Transaction

Understanding how these transactions work helps management teams engage constructively rather than being passengers in a process.

Deal Structure and Pricing

Going-private transactions are typically priced at a premium to the undisturbed share price (the price before any transaction speculation appeared in the market). For PE-led transactions, that premium typically ranges from 20% to 40%. Boards have a fiduciary obligation to maximize shareholder value, which means the negotiating dynamic involves the acquirer wanting to minimize the premium and the board wanting to maximize it.

Special committees of independent directors are typically formed to evaluate going-private proposals and negotiate on behalf of public shareholders. Investment banks are hired to provide fairness opinions. These processes are both genuinely important and significantly time-consuming.

Leverage and Capital Structure

In an LBO, the deal is funded with some equity from the PE sponsor and a significant debt load, often 4-7x EBITDA depending on market conditions and the stability of the business's cash flows. That debt typically includes a senior secured term loan, sometimes a revolving credit facility, and potentially junior capital in the form of subordinated debt or preferred equity.

The interest payments on that debt come out of the company's cash flow before any investment in growth, before any improvement to employee compensation, and before any return to the equity holders. Understanding the post-close capital structure is essential: a company that generated $30M in free cash flow pre-transaction may find that $20M of that goes to debt service, leaving $10M for everything else.

The upside of leverage is that equity returns are amplified when the business performs well. A PE sponsor putting in $200M of equity in a $1B transaction that exits at $1.4B has generated a 2x return on equity even though the enterprise value only increased 40%. That's the math that makes LBOs attractive.

Management Rollover and Incentives

In most PE-backed going-private transactions, the management team is expected to roll over a portion of their existing equity (receiving PE fund equity or management equity in the new structure) and to accept a new incentive plan. Management equity in PE-backed companies typically vests based on returns at exit, not time, which creates strong alignment but also concentrates personal financial risk.

The negotiation of management equity terms is one of the most consequential parts of any going-private transaction for the executives involved. The size of the management equity pool, the exercise price of options, the return thresholds for vesting, and the treatment of equity in different exit scenarios all determine whether management participation is genuinely valuable or largely notional.

What Changes After Going Private

The governance, operational, and cultural changes after a going-private transaction are often more significant than management teams anticipate.

Board composition and oversight. The PE sponsor typically controls the board. This is not the same as a public company board with independent directors and a mix of perspectives. PE-backed boards meet more frequently, engage more deeply with operating details, and have direct financial stakes in outcomes. Management teams used to public company boards sometimes experience this as a step up in accountability, and sometimes as a step into a more directive ownership relationship.

Reporting and transparency. The company no longer files public financials, but the PE sponsor and lenders still require detailed reporting. Monthly management accounts, rolling 13-week cash flow forecasts, and regular board packages replace the quarterly 10-Q process. The external audience is smaller but the internal reporting discipline often intensifies.

The exit horizon. PE funds have defined lives, typically 10 years, with investment periods of 3-5 years and a target holding period for individual investments. Management teams in PE-backed companies operate with the knowledge that the business will be sold again within a finite window. That concentrates focus and creates urgency, but it also means strategic decisions are made in the context of what maximizes value at a specific exit point rather than what's optimal over an indefinite horizon.

Cost management. PE owners are typically more aggressive about cost than public company shareholders. The first 100 days after closing often include a detailed operational review and identification of cost reduction opportunities. Management teams who've been reluctant to take restructuring actions in a public context sometimes find the PE ownership model forces decisions they knew were correct but had avoided.

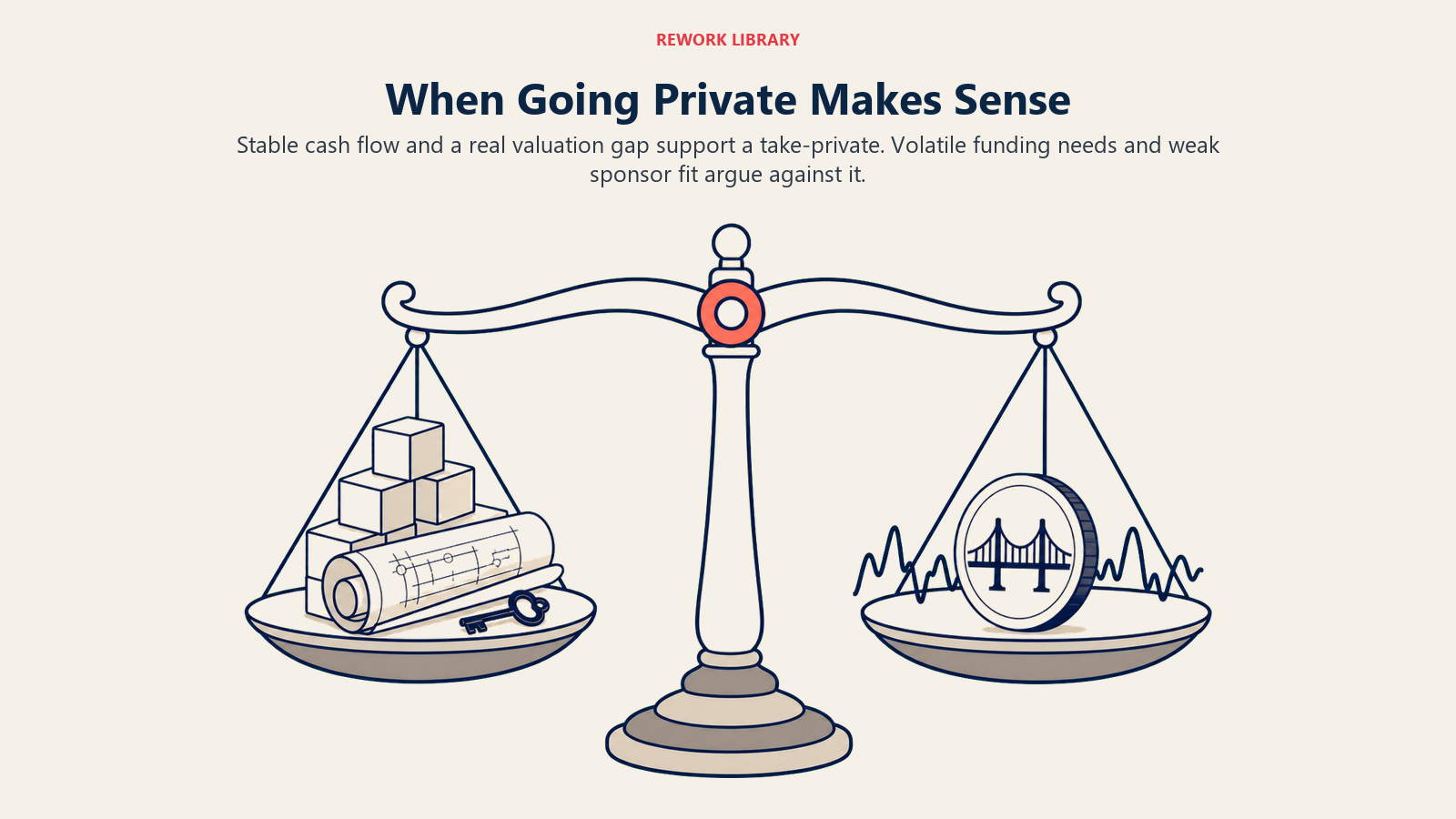

When Going Private Makes Sense (and When It Doesn't)

Going private is not inherently superior or inferior to remaining public. It's a structural choice that fits some situations better than others.

It tends to make sense when:

- The business has strong, stable cash flows that can service debt

- The management team is aligned on a transformation plan that requires 3-5 years of execution without public market interference

- There is a genuine valuation disconnect that a transaction can correct

- The PE sponsor has relevant sector experience and relationships that add operating value beyond capital

It tends not to make sense when:

- The business needs ongoing capital market access for acquisitions or organic investment

- The cash flows are too variable or uncertain to support meaningful leverage

- The management team isn't prepared for the accountability intensity of PE ownership

- The valuation gap isn't wide enough to absorb transaction costs, deal fees, and the premium required to take out public shareholders

For mid-market executives considering a going-private transaction, the most useful framing is to think about what public market status is actually providing versus what it costs. If the answer is "we have public currency for acquisitions we're not making, institutional investors who don't understand our story, and quarterly earnings pressure that prevents the investments we know we need to make," the case for going private deserves serious evaluation.

The decision connects directly to how the company thinks about its corporate strategy and long-term value creation approach. It's a structural tool, not a strategy by itself. The business still has to perform.

Related reading:

- Corporate Strategy: Choosing Where to Compete and How to Win

- Business Model Canvas: Mapping How Your Business Creates Value

- Growth Strategy Frameworks for Mid-Market Companies

- EBITDA: What It Measures and When to Use It

- Free Cash Flow and Why It Matters More Than Profit

- Technology Investment Strategy - How technology capital allocation decisions change under PE ownership

- Business Metrics Overview - The operational metrics PE sponsors watch most closely after a going-private transaction

Co-Founder, Rework.com