More in

Revenue Operations Insights

The True Cost of Software Sprawl (It's Not the Licenses)

Jun 12, 2026

Pipeline Hygiene as a Cultural Practice, Not a Data Problem

Apr 7, 2026

The RevOps Maturity Model: From Reactive to Strategic

Apr 6, 2026

Attribution Is Broken. Here's What to Measure Instead

Mar 9, 2026

CAC Payback: The Metric That Actually Predicts SaaS Survival

Feb 6, 2026 · Currently reading

CAC Payback: The Metric That Actually Predicts SaaS Survival

Turn this article into takeaways for your work.

Each assistant summarizes the article only for you and suggests best practices for your work.

In a zero-interest-rate world, CAC payback was a nice-to-have. Post-2022, it's an existential signal. Companies running 24-month payback periods are quietly burning runway while their dashboards show green ARR growth. The ones that survive aren't necessarily the ones growing fastest. They're the ones whose RevOps leaders understand what their payback number actually means, what distorts it, and how to act on it when the number moves.

This isn't about calculating CAC payback. You know how to do that. This is about using it as a strategic operating lever.

The Calculation Most Companies Get Wrong

There are two versions of CAC payback floating around boardrooms, and they produce wildly different numbers.

Marketing-only CAC takes total marketing spend divided by new customers. It's clean, easy to pull from your CRM attribution report, and almost always wrong for decision-making purposes.

Fully-loaded CAC includes sales salaries and commissions, marketing spend, sales tooling, SDR costs, and a reasonable allocation of RevOps overhead tied to new business acquisition. That tooling line is where the true cost of software sprawl shows up in CAC long before it ever reaches EBITDA. This number is typically 40 to 80% higher than marketing-only CAC at mid-market SaaS companies, and it's the one that predicts survival. OpenView Partners' SaaS benchmarks confirm that fully-loaded CAC divergence from marketing-only CAC is one of the most common sources of unit economics misreporting at growth-stage companies.

The payback formula is straightforward: Fully-Loaded CAC divided by (Average Contract Value × Gross Margin) × 12 = Payback in Months. Where most teams fail isn't the math. It's in the inputs. RevOps leaders pulling CAC data from Salesforce or HubSpot attribution reports are often capturing only the marketing-sourced costs, not the full cost of the sales motion. If your CRM attribution records touch points but not rep time or commission, your CAC is understated. This is one reason keeping your CRM data model clean and consistent matters before you trust any cohort-level cost calculation.

Three checks to run before trusting your CAC number:

- Does your CAC include sales compensation for the deals in the cohort? Not blended sales salaries, but the actual commission plus base allocation for reps who closed those specific customers.

- Are you using New ARR (not TCV) in the denominator? Total contract value inflates payback favorably for multi-year deals.

- Is gross margin calculated on the new cohort's product mix, or are you using company-average gross margin? These diverge significantly for companies selling services alongside software.

Benchmarks by Segment, and Why Using the Wrong One Costs You

CAC payback benchmarks vary so much by segment that comparing yourself to an industry average is often worse than useless. Here's what the data from firms like KeyBanc, Bessemer, and Lenny Rachitsky's surveys generally shows:

SMB SaaS (ACV under $15k): 6 to 12 months is healthy. Under 6 months suggests you might be underpricing. Over 18 months is a warning sign that your low-ACV model won't generate enough LTV to sustain the acquisition cost.

Mid-market SaaS (ACV $15k to $100k): 12 to 18 months is the standard healthy range. Most investors expect sub-18 for growth-stage companies. Beyond 24 months in this segment typically means your sales cycle length or discounting behavior is creating a structural problem. According to Bessemer Venture Partners' State of the Cloud benchmarks, median CAC payback for public SaaS companies has extended significantly since 2022 as capital efficiency replaced growth rate as the primary investor metric.

Enterprise SaaS (ACV $100k+): 18 to 24 months is accepted because enterprise LTV is higher and NRR typically exceeds 120%. The calculation has a different risk profile because you're betting on expansion, not just retention. Understanding how net revenue retention drives SaaS unit economics helps frame why enterprise payback tolerances are higher.

The error RevOps leaders make is benchmarking against general SaaS averages when their business is concentrated in one segment. An enterprise-focused company with a 22-month payback looks alarming against a 12-month benchmark, but it's actually in a healthy range for their motion. Conversely, an SMB-focused company with 18-month payback that benchmarks against enterprise norms will think it's fine when it's not.

Four Things That Distort CAC Payback

Even when you've got the right formula and the right benchmarks, the number can lie. These four distortions are the ones worth auditing every quarter.

Channel mix shifts. If you shifted spend heavily toward outbound SDR motions in Q3, your Q3 cohort's CAC will look higher than Q2's even if nothing changed in your underlying economics. Inbound leads convert faster and cheaper than outbound. When channel mix shifts, payback changes without the underlying business model changing. Pull payback by channel cohort, not just overall. This is also why pipeline stages need to map to actual buyer behavior rather than rep activity. Stage accuracy determines which cohort a deal belongs to.

Rep ramp timing. New reps take 6 to 9 months to reach full productivity. If you hired aggressively in H1 and they closed their first deals in Q3, you're carrying the cost of their ramp in the CAC numerator but only counting their initial (smaller) deals in the denominator. Your Q3 payback looks terrible. But it's a temporary ramp effect, not a structural problem. The fix is to track payback on ramped-rep cohorts separately from first-deals-from-new-reps cohorts.

Product mix changes. If you launched a new product tier or a professional services add-on, deals involving that new offering may have lower gross margins than your standard software deals. When those deals enter your payback calculation using blended margin, you're underestimating the true payback for those cohorts.

Upfront discounting. Multi-year prepays and heavy upfront discounts reduce the monthly revenue figure in your payback denominator. A deal that could have been $10k MRR over 24 months shows up as a smaller effective monthly figure when discounted for prepayment. Your payback looks worse even though the deal economics are actually favorable over the contract term. This is where RevOps needs to flag whether payback should be calculated on nominal or discounted contract value.

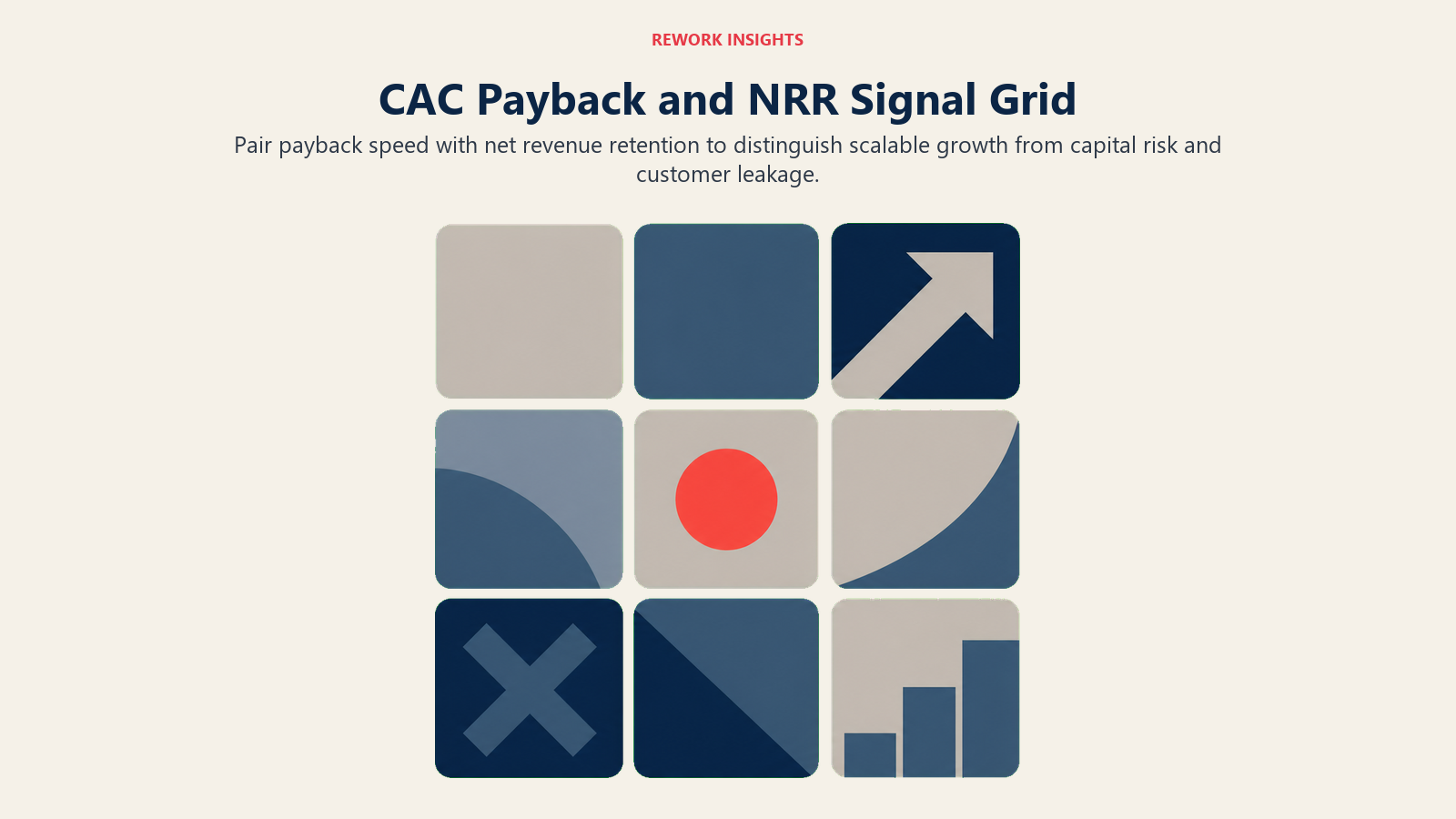

The Payback Signal Grid

Rather than treating CAC payback as a standalone metric, map it against Net Revenue Retention. The combination is more diagnostic than either number alone.

Payback Signal Grid:

| NRR < 100% | NRR 100-115% | NRR > 115% | |

|---|---|---|---|

| Payback < 12 mo | Growth trap: fast acquisition, leaky bucket | Healthy SMB/PLG motion | Exceptional, scale spend immediately |

| Payback 12-18 mo | Capital risk: churn is destroying acquisition ROI | Standard healthy SaaS | Good expansion offsetting acquisition cost |

| Payback > 18 mo | Existential: burning cash on customers who leave | Marginal, needs improvement | Enterprise acceptable if LTV > 5x ACV |

The top-right quadrant (short payback, high NRR) is where you accelerate hiring and spend. You're acquiring customers cheaply and expanding them efficiently. The bottom-left quadrant (long payback, low NRR) is where you cut go-to-market spend and fix retention before adding more acquisition fuel.

Most companies live in the middle cells, which is where the nuanced decision-making happens. A 16-month payback with 108% NRR isn't alarming, but it's not license to grow headcount aggressively either.

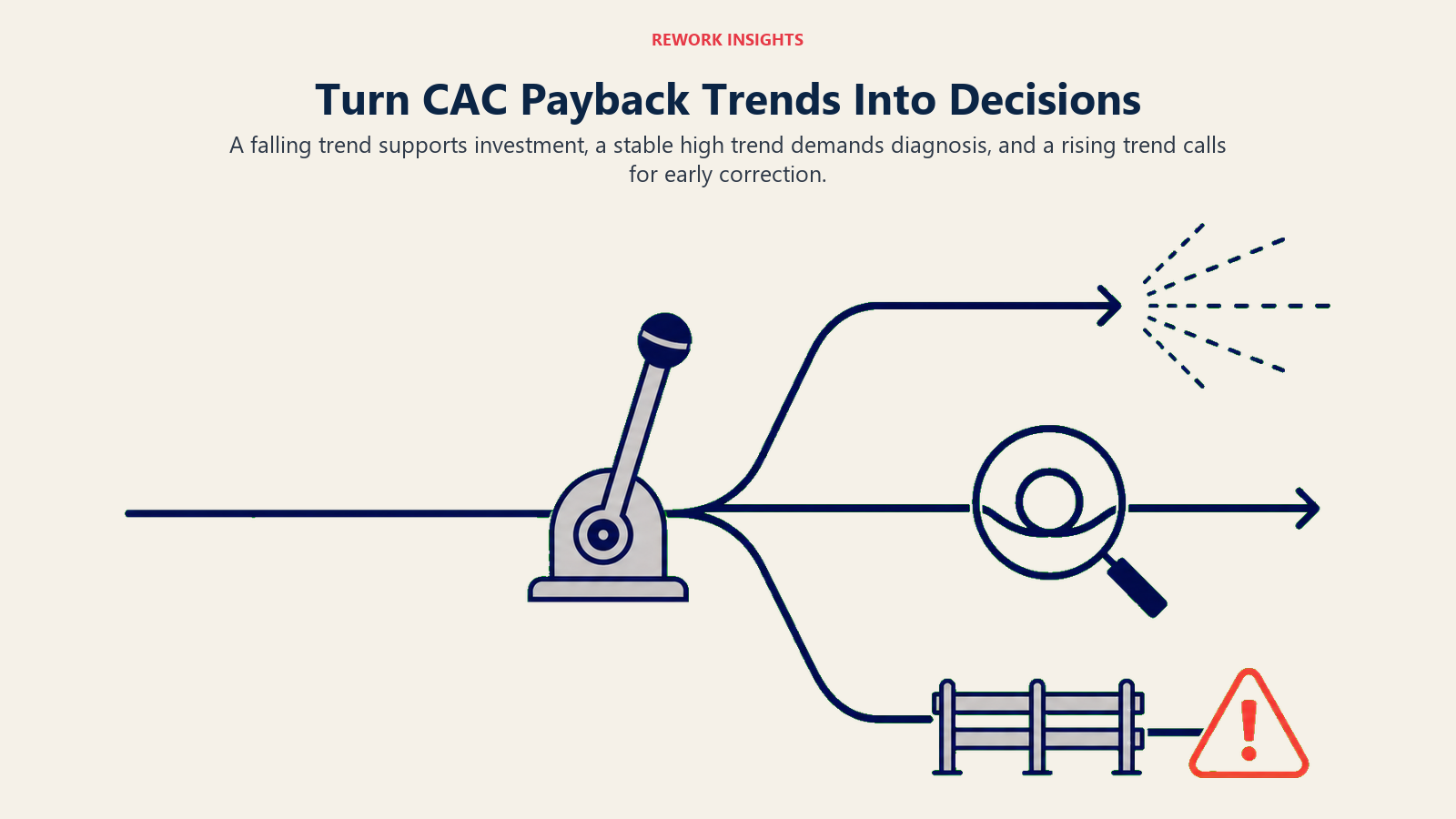

From Metric to Decision

CAC payback trends are what drive operating decisions. Not the point-in-time number.

When payback is trending down: Your acquisition efficiency is improving. This is typically the right time to increase go-to-market investment, accelerate hiring in sales and SDR, and expand into new segments or geographies. The signal is: you've found a motion that works. Now is when you pour fuel on it.

When payback is stable but higher than benchmarks: Investigate the distortion factors above before making cuts. More often than not, it's ramp timing or channel mix. If after cleaning those out the number is still elevated, the issue is usually either pricing discipline (too much discounting), target market fit (selling to customers who don't actually fit your ICP), or sales cycle length that can be compressed.

When payback is trending up: This is the early warning sign that matters most. Companies don't usually see payback spike suddenly. It drifts up over 2 to 3 quarters before it becomes a crisis. If you catch it drifting, you still have time to course-correct by reducing discounting, tightening ICP, or rebalancing channel mix before the board notices.

Three questions RevOps should ask every quarter to validate the number:

- What changed in channel mix this quarter, and have I pulled payback by channel cohort to isolate those effects?

- Did we hire a significant number of new reps this quarter, and are their first-deal economics dragging the overall number?

- Are we comparing against the right segment benchmark for where our new business is actually coming from this quarter?

These three checks take about 90 minutes and will catch most of the distortions before they create false conclusions.

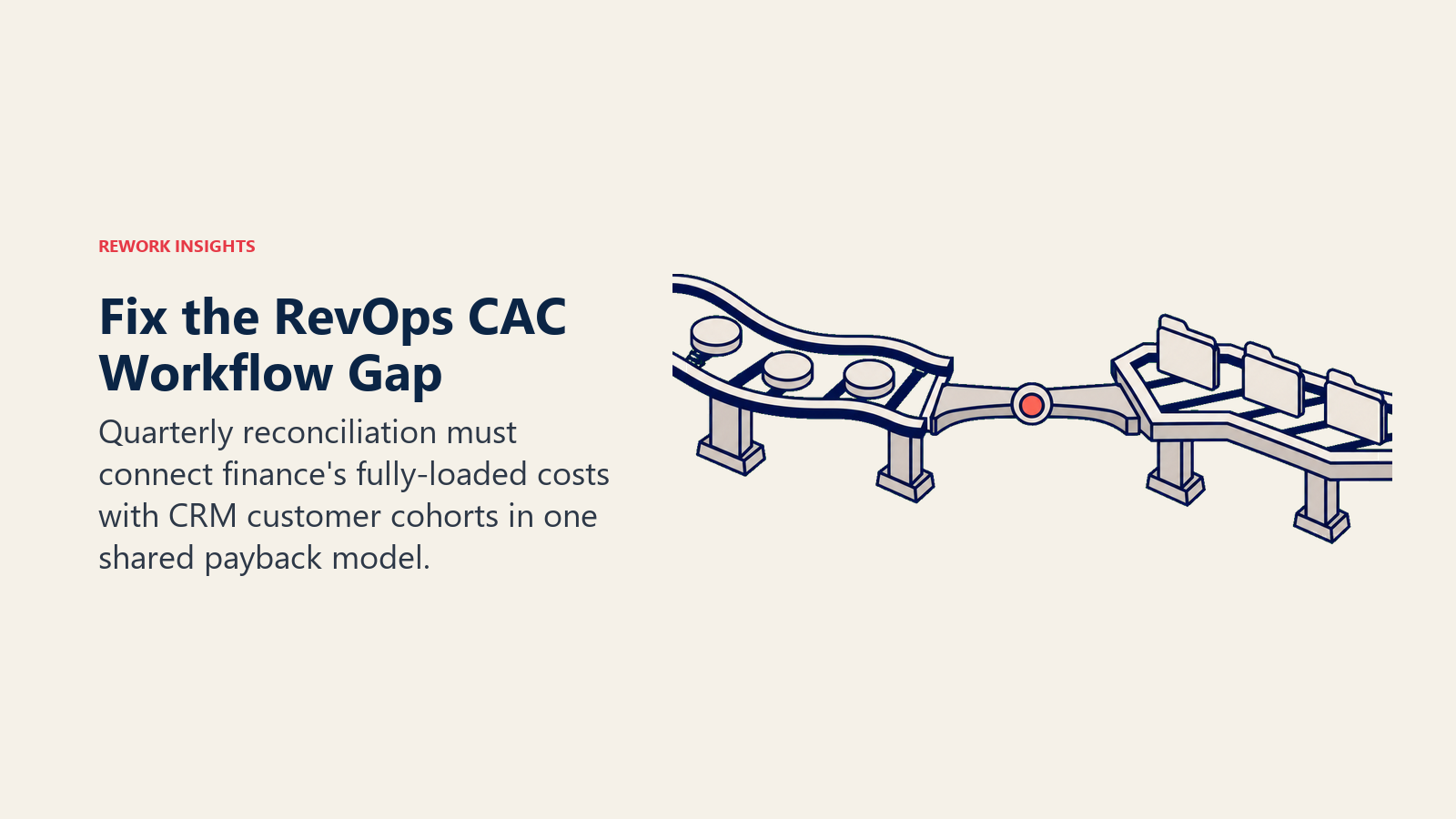

What Breaks in Most RevOps CAC Workflows

The operational failure point is usually between the finance team and RevOps. Finance tracks spend. RevOps tracks pipeline and CRM data. Neither has a shared model that combines both into a quarterly cohort calculation. A RevOps framework that connects your CRM to financial metrics closes this gap more reliably than one-off reconciliation rituals.

If you're using Salesforce, you likely have campaign attribution but not a fully-loaded cost view. If you're using HubSpot, your deal pipeline and marketing attribution are in the same tool, but sales compensation data almost certainly lives in a separate spreadsheet or HRIS. The gap between those systems is where CAC payback distortion hides.

The fix isn't a new tool. It's a quarterly reconciliation ritual where RevOps pulls new customer cohort data from the CRM, finance pulls the fully-loaded costs for that cohort's acquisition period, and someone calculates payback from the combined dataset. This takes about two hours per quarter with a clean model. It's worth doing.

The Investors Are Watching This Metric More Than You Think

As of 2025, most growth-stage SaaS investors are using CAC payback as a primary filter for growth investment decisions, ahead of ARR growth rate in many cases. The reason is simple: high growth with poor payback means you need continuous outside capital to fund each new customer. Poor payback plus slowing growth is a terminal combination. SaaStr's analysis of public SaaS company benchmarks, particularly Jason Lemkin's writing on efficient growth, has consistently positioned CAC payback as the single number that separates capital-efficient SaaS from growth-at-any-cost narratives that fell apart post-2022.

RevOps leaders who present CAC payback trends to the board, with distortion factors explained and a clear narrative about the trajectory, build significantly more credibility than those who show it as a raw number. The analytical maturity to say "our payback worsened 3 months this quarter, here's why it was ramp timing, and here's why we expect it to normalize next quarter" is what separates RevOps as a strategic function from RevOps as a reporting service.

That's the actual job. Not calculating the number. Explaining what it means and what you're doing about it.

Learn More

- Attribution Is Broken. Here's What to Measure Instead: Why your CRM attribution data is structurally unreliable for investment decisions

- Pipeline Hygiene as a Cultural Practice, Not a Data Problem: The behavioral foundations that make your CRM data trustworthy enough to build CAC models on

- The RevOps Maturity Model: From Reactive to Strategic: How strategic RevOps leaders build the influence to act on metrics like CAC payback

Co-Founder, Rework.com